ALAMEDA COUNTY COMMUNITY DEVELOPMENT AGENCY

|

|

|

- Joella Young

- 5 years ago

- Views:

Transcription

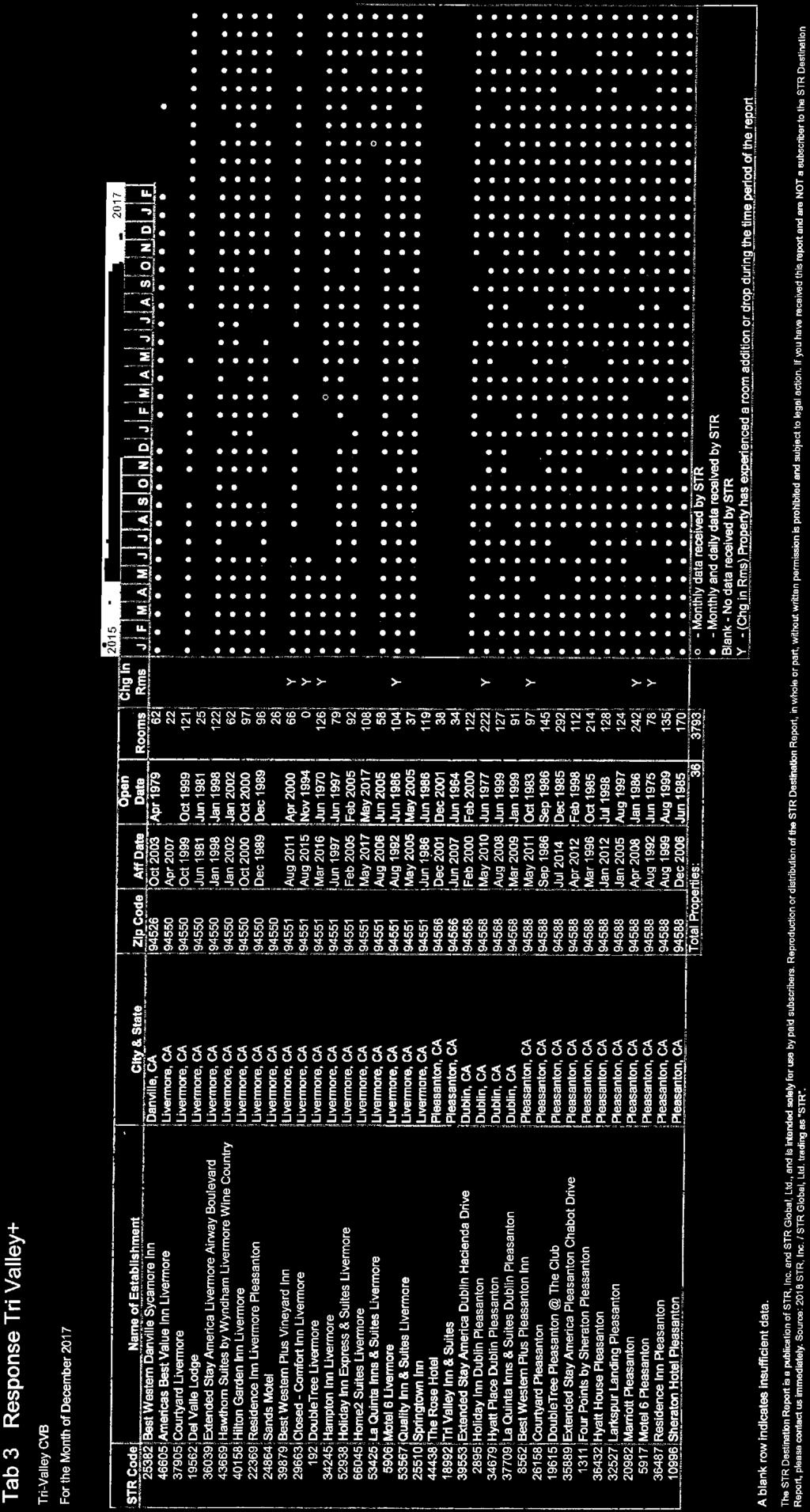

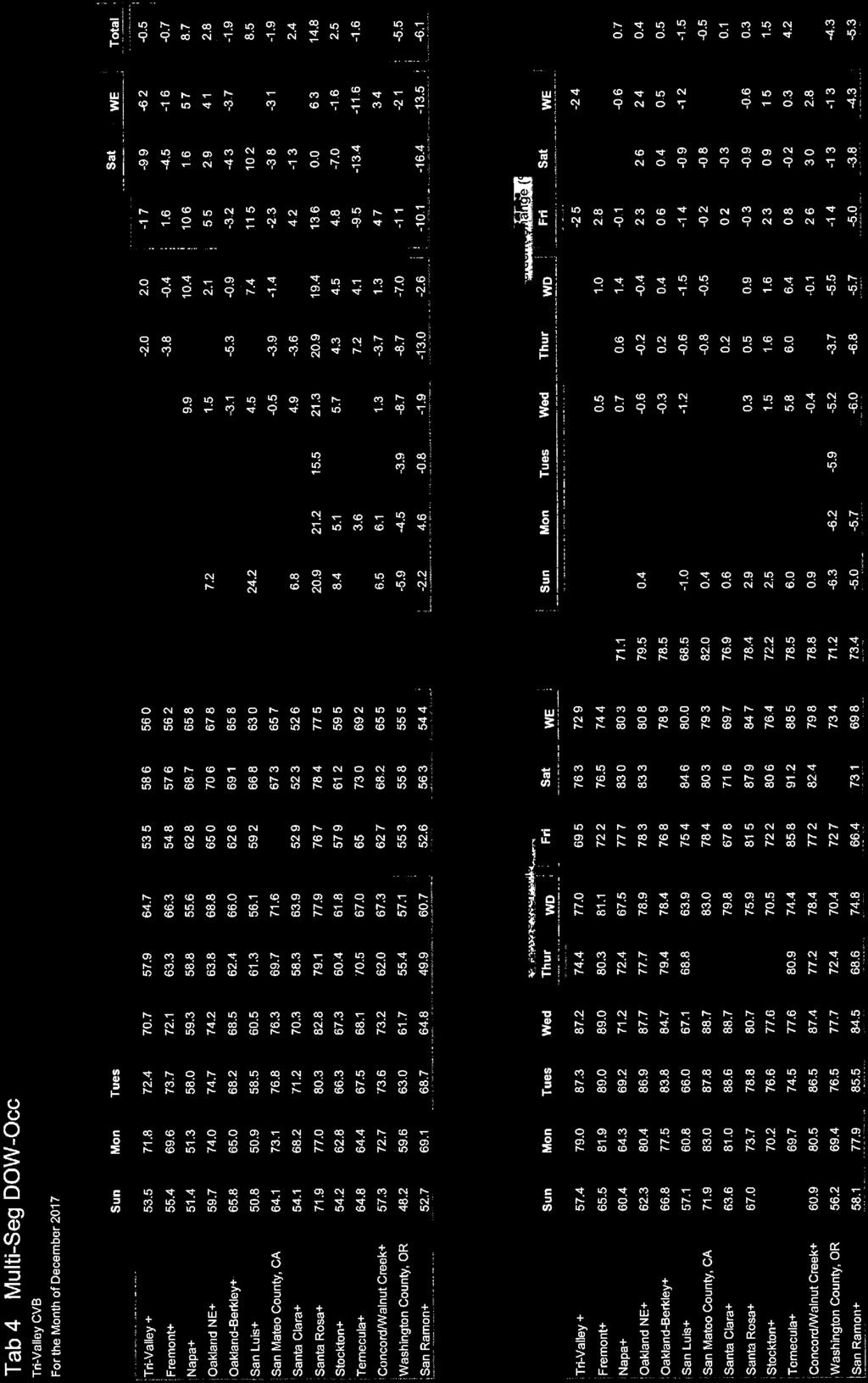

1 ALAMEDA COUNTY COMMUNITY DEVELOPMENT AGENCY P L A N N I N G D E P A R T M E N T Chris Bazar Agency Director Albert Lopez Planning Director 224 West Winton Ave Room 111 Hayward, California phone fax MEMORANDUM TO: FROM: Board of Supervisors Transportation and Planning Committee Chris Bazar, Director, Community Development Agency Albert Lopez, Planning Director DATE: March 5, 2018 SUBJECT: Bed and Breakfast Inns, South Livermore Valley Area Plan BACKGROUND COUNTY POLICY AND CODE South Livermore Valley Area Plan and ECAP: On February 3, 1993, the Board of Supervisors approved the South Livermore Valley Area Plan (SLVAP), a County planning document designed to enhance viticulture, other long-term agriculture, related job growth, and tourism in the unincorporated South Livermore Valley Area (SLVA). A similar and complementary set of polices was adopted by the City of Livermore. The SLVAP policies were incorporated into the East County Area Plan (ECAP). Those policies included provisions for allowing bed-andbreakfast establishments (B&Bs) as conditional uses. Among the policies adopted by the Board is ECAP Policy 344: - The County shall encourage the promotion of the South Livermore Valley as a premier wine-producing center by encouraging appropriate tourist-attracting and supporting uses, such as bed and breakfast establishments or other uses ECAP Program 125 also discusses appropriate commercial uses, including B&Bs; the program reads, in part: - The County shall limit new commercial uses within the Cultivated Agricultural Overlay District to appropriate small-scale uses that promote the area s image as a wine region, subject to issuance of a conditional use permit New commercial uses proposed as a part of a bonus density application should be limited to the 10% maximum area of each parcel not dedicated to cultivated agriculture, subject to appropriate coverage limitations, and should be sited to maximize efficient use of cultivated lands. Wineries and small bed-andbreakfast establishments are examples of appropriate commercial uses. Bed-and-breakfast establishments shall be limited to existing homes or homes permitted under the South Livermore Valley Area Plan; construction of separate additional structures shall not be permitted... The Alameda County Zoning Ordinance discusses B&Bs within Article VII, Combining CA (Cultivated Agriculture) Districts. Section (F)(2)(a) specifies that a Bed and breakfast establishment, if conducted within an existing or permitted dwelling: maximum of fourteen (14) rooms available for guests is a Conditional Use in the SLVA subject to review by the Board of Zoning Adjustments under Section

2 Board of Supervisors Transportation and Planning Committee Bed and Breakfast Inns, South Livermore Valley Area Plan March 5, 2018 Page 2 ECAP / Measure D Initiative and Applicable Policies: In November 2000, the Alameda County electorate approved the Save Agriculture and Open Space Lands Initiative (Measure D). The Initiative amended portions of the County General Plan, including the East County Area Plan (ECAP). The portions of the ECAP revised or enacted under the Initiative may not be amended except by voter approval, with the exception that the Board of Supervisors can impose more stringent restrictions on development and land use and it may make technical or nonsubstantive changes to the Initiative provisions. Existing and future County plans, zoning regulations, etc. must be consistent with the provisions of the Initiative. Portions of the ECAP and other planning documents that were not amended or enacted by the Initiative may still be modified without voter approval provided the modifications are consistent with the provisions of the Initiative. The Initiative added, deleted, and revised more than 60 ECAP policies and programs. Some of these amendments, along with a handful of previous ECAP policies, apply generally to land use and development standards in the South Livermore Valley Area. Planning staff has discussed the applicability of such policies and programs with County Counsel and believes that among these amendments and policies, the following may apply to B&B establishments. Staff points out that these policies mostly apply to permit findings and development standards such as visual treatment, water supply and septic management, rather than land use limitations, although one of them (addressed below) has land use implications: Policy 1 (Measure D): The County shall identify and maintain a County Urban Growth Boundary that divides areas inside the Boundary, next to existing cities, generally suitable for urban development from areas outside suitable for long-term protection of natural resources, agriculture, public health and safety, and buffers between communities. The County Urban Growth Boundary shall be the Urban Growth Boundary of the City of Pleasanton starting at its eastern junction with U.S. I-580 clockwise to U.S. I-580, west to the boundary of the East County Area Plan, north to the proposed western Urban Growth Boundary for the City of Dublin on the November 7, 2000 election ballot, to the Alameda-Contra Costa County line, east to the eastern boundary of the East Dublin Specific Plan on February 1, 2000, south to U.S. I-580, east to the city limits of the City of Livermore, the northern Livermore city limits, except where the northern city limits are below U.S. I-580 the Boundary shall be I-580, to the eastern city limits of Livermore, to the proposed southern Urban Growth Boundary for Livermore on the March 7, 2000 election ballot to U.S. I-580, and west to the City of Pleasanton Urban Growth Boundary. Policy 82 (Measure D): In areas designated Large Parcel Agriculture, the County shall permit limited agriculture enhancing commercial uses that primarily support the area s agricultural production, are not detrimental to existing or potential agricultural use, demonstrate an adequate and reliable water supply, and comply with other policies and programs of the Initiative. Policy 83 (Original ECAP): The County shall require any proposal for a visitor-serving commercial use in an agricultural area to meet all of the following criteria: The project will primarily promote agricultural products grown or processed in Alameda County; The project is compatible with existing agricultural production activities in the area; The project mitigates, to the satisfaction of the County, all potential conflicts with surrounding agricultural uses and other environmental impacts; and

3 Board of Supervisors Transportation and Planning Committee Bed and Breakfast Inns, South Livermore Valley Area Plan March 5, 2018 Page 3 The project can demonstrate an adequate and reliable water source that does not significantly diminish the availability of water to serve existing or potential agricultural use. Policy 115 (Measure D): In all cases appropriate building materials, landscaping and screening shall be required to minimize the visual impact of development. Development shall blend with and be subordinate to the environment and character of the area where located, so as to be as unobtrusive as possible and not detract from the natural, open space or visual qualities of the area. To the maximum extent practicable, all exterior lighting must be located, designed and shielded so as to confine direct rays to the parcel where the lighting is located. Large Parcel Agriculture (Measure D definition) requires a minimum parcel size of 100 acres, except as provided in Programs 40 and 41. The maximum building intensity for non-residential buildings shall be.01 FAR (floor area ratio) but not less than 20,000 square feet... One single family home per parcel is allowed provided that all other County standards are met for adequate road access, sewer and water facilities, building envelope location, visual protection, and public services. Residential and residential accessory buildings shall have a maximum floor space of 12,000 square feet. Additional residential units may be allowed if they are occupied by farm employees required to reside on-site. Apart from infrastructure under Policy 13, all buildings shall be located on a contiguous development envelope not to exceed 2 acres except they may be located outside the envelope if necessary for security reasons or, if structures for agricultural use, necessary for agricultural use. Subject to the provisions of the Initiative, this designation permits agricultural uses, visitor-serving commercial facilities (by way of illustration, tasting rooms, fruit stands, bed and breakfast inns) and similar uses compatible with agriculture. Different provisions may apply in the South Livermore Valley Plan Area, or in the North Livermore Intensive Agriculture Area. [The foregoing definition has land use implications. Recalling that the original requirement for B&B establishments includes locating within existing or permitted dwellings (which imply a residential use and associated FAR limitations of 12,000 square feet), B&Bs are also referred to as visitor-serving commercial uses, which implies the larger allowance of.01 FAR or 20,000 square feet minimum building size. This ambiguity may need to be resolved. In either case, this definition strongly implies that B&B establishments are generally compatible with agriculture.] DISCUSSION Policy 253 (Measure D): The County shall approve new development only upon verification that an adequate, long-term, sustainable, clearly identified water supply will be provided to serve the development, including in times of drought. 1. Present Conditions: Since adoption of the SLVAP, only one B&B has become established in the SLVA. This establishment is the Purple Orchid Inn, located at 4549 Cross Road, in the northeast section of the SLVA. The Purple Orchid Inn offers 10 rooms for lodging, a spa, and amenities for events such as weddings. A handful of other developers have proposed B&Bs in the SLVA in the last 25 years. Currently, the Purple Orchid Inn proposes to add two rooms to its facility, and another developer, in association with Rios-Lovell Winery, has submitted an early concept to construct a new B&B with 14 rooms, a restaurant and other amenities. All other current motels, hotels, inns and other commercial lodging establishments are located near

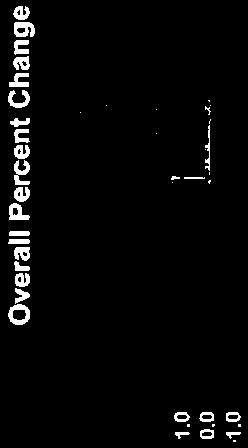

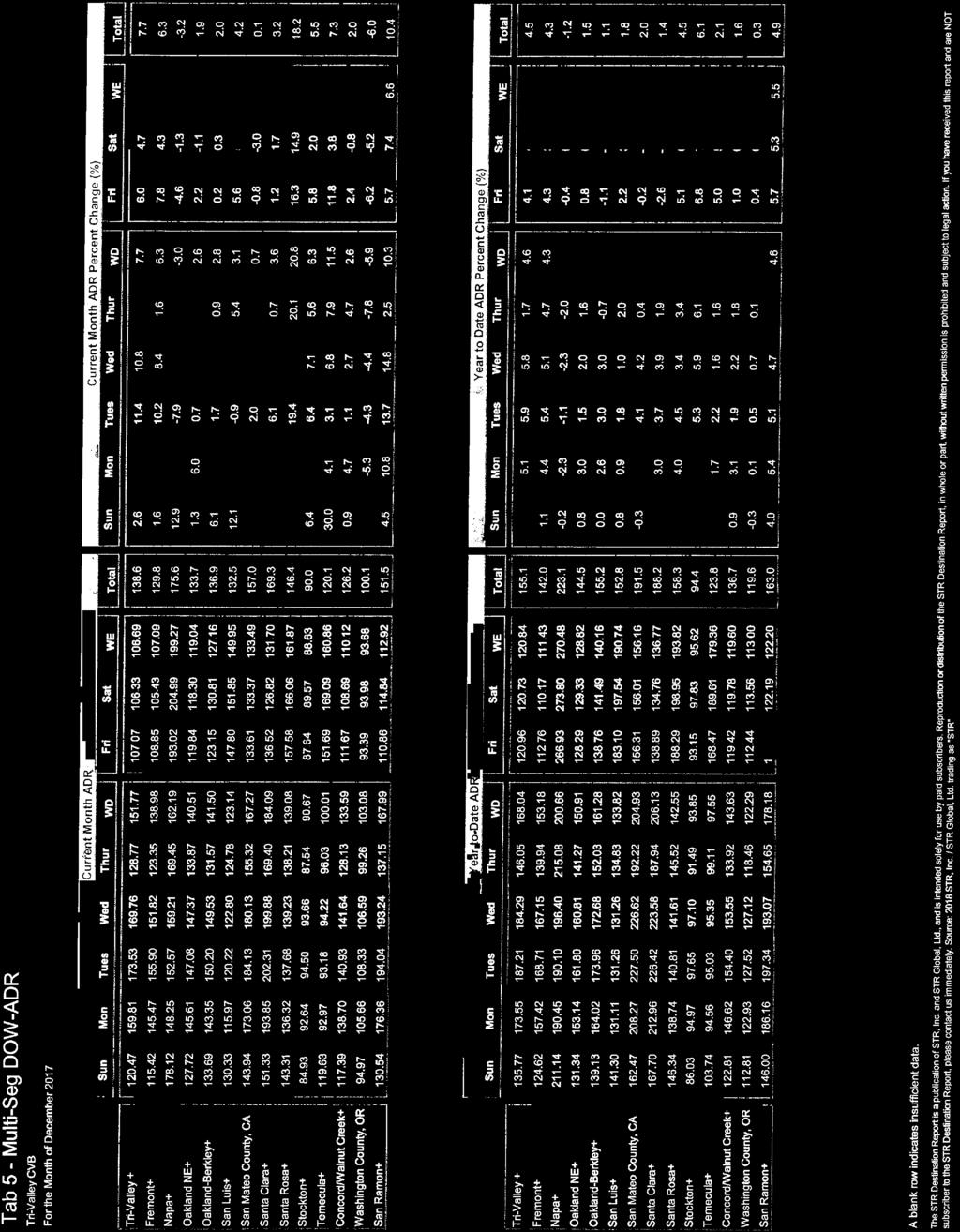

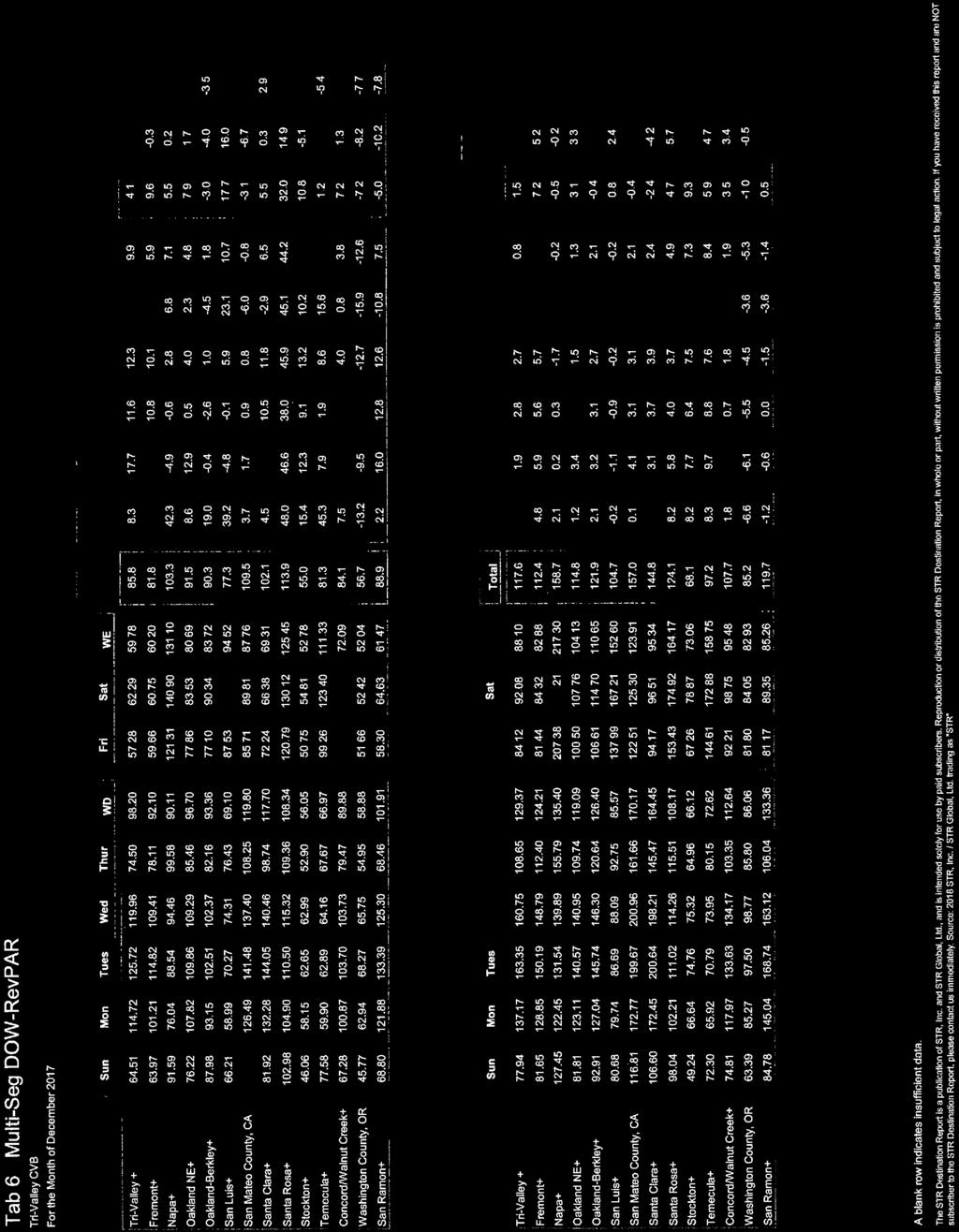

4 Board of Supervisors Transportation and Planning Committee Bed and Breakfast Inns, South Livermore Valley Area Plan March 5, 2018 Page 4 the I-580 freeway, several miles north of the SLVA. Staff also understands that the City of Livermore has tentatively approved a concept for a downtown hotel. 2. Desire and Demand for Additional B&B Establishments: Staff has investigated the demand for B&Bs or other appropriate lodging for the SLVA and the eastern Tri-Valley in general. While no hard demand-side data appears to exist, there is some information from city and private sources that suggests a desire for more lodging of different types, or at least that if the availability of lodging were greater it would make the area more accessible and would attract more multi-day visitation for both business and leisure. The accommodation and food service industries in the Tri-Valley already support almost 3,500 jobs as of 2016 (Dean Runyan Associates, Tri-Valley, California Travel Impacts, , June 2017) and occupancy for existing lodging varies from 67% - 81%, depending on the year of record and cost of lodging (CBRE Hotels, Hotel Horizons, September-November 2017 edition). These values appear to be a strong indicator of regional lodging demand, well above the long-term average. In the Tri-Valley, lodging demand is generally greater during weekdays than on weekends (STR, Inc., Tri-Valley CVB for the month of December 2017), suggesting that business and government travel are more significant attractors than leisure travel; however, this is not necessarily an indicator of lack of demand or desire for more leisure lodging with regional cultural appeal, as the existing lodging does not necessarily cater to leisure travelers looking for wine country or other regional experiences. According to a Regional Tourism Asset Assessment prepared for Visit Tri-Valley (Strategic Marketing Group [SMG], 2014), strong desire has been expressed among various community organizations to increase appropriate styles of lodging, including B&Bs and other small to mediumsized facilities, to provide greater access for tourist travelers seeking wine country and regional cultural / recreational experiences. At least some of the SMG analysis focuses on the SLVA, identifying a need for up to 150 rooms in the region, and while it recognizes the desire for small facilities such as B&Bs in a few places, it specifically describes only a single hypothetical room resort to primarily serve the dual golf course recreational opportunities of Poppy Ridge and the Course at Wente Bros. In addition, the SMG analysis discusses an overall marketing and outreach strategy for increasing tourism and visitation to the Tri-Valley region. 3. Possible Amendments to Encourage Bed and Breakfast Establishments: In order to accommodate the community desire to establish new B&Bs, it would be necessary to alter ECAP Policy 344, ECAP Program 125 and the Zoning Ordinance. Those amendments could be simple or more extensive, depending upon what the Board deems appropriate. To this end, staff seeks to answer the following questions: a. Should B&Bs continue to be limited to existing or permitted dwelling units, or could they be built as new stand-alone facilities? b. Pursuant to Question (a) above, should B&Bs then be limited to 12,000 square feet maximum floor area, as required for a residential dwelling, or should a more liberal size allowance be

5 Board of Supervisors Transportation and Planning Committee Bed and Breakfast Inns, South Livermore Valley Area Plan March 5, 2018 Page 5 adopted (e.g., 0.01 FAR or 20,000 square feet) as implied by its identification as a visitorserving commercial use? c. Should an owner / operator be required to maintain his or her residence at the B&B, as is most common, or could the establishment be owned and / or operated by an offsite person? d. Can a B&B appropriately include a full-service restaurant for multiple meals, a spa or an event center? e. Should the County continue the policy that construction of separate additional structures shall not be permitted, or could this requirement be relaxed? f. If the existing requirements are relaxed to make B&Bs more viable, should the County place a limit of the number of applications that may be approved in a given time period? NEXT STEPS: Some possible next steps could be: - Prepare a presentation for community meetings and workshops, describing the issues and seeking public input about the questions above and any other ideas or concerns the community may have. - Seek input from the Planning Commission, the Agricultural Advisory Committee, the City of Livermore, the Livermore Valley Winegrowers Association, the Tri-Valley Conservancy, Visit TriValley and others. - Assemble the information gathered at these meetings, develop draft recommendations for your Committee, the Planning Commission and Board of Supervisors to consider. Attachments: - Dean Runyan Associates, Tri-Valley, California Travel Impacts, , June CBRE Hotels, Hotel Horizons, September-November 2017 edition - STR, Inc., Tri-Valley CVB for the month of December Strategic Marketing Group[SMG], Regional Tourism Asset Assessment prepared for Visit Tri- Valley, Airsage, Airsage Visitor Analytics, Tri-Valley, December 2016 cc: County Counsel

6 AirSage Visitor Analytics Tri-Valley December 2016

7 AirSage Company Overview Patented Population Analytics 15 billion location data points per day 100 million mobile devices Consumer privacy protection

8 AirSage WiSE Platform

9 Explanation Tri-Valley Tri-Valley Attendees Devices seen in any of the 9 points of interest (POI) as defined below: 1. Vineyards 2. Fairgrounds 3. Outlets 4. Automotive Museum 5. Downtown Danville 6. Downtown Livermore 7. Downtown Pleasanton 8. Emerald Glen Park 9. Dublin Civic Center Resident is a device with a home location inside Alameda and Contra Costa Counties. Visitor is a device with a home location outside of Alameda and Contra Costa Counties. 4

10 Devices Unique Devices By POI Tri-Valley 12,000 10,000 9,692 8,000 6,000 4,000 4,474 3,918 3,034 3,152 2,564 2,776 3,774 2, , Vineyards Fairgrounds Outlets Automotive Museum Downtown Livermore 440 1,882 Downtown Danville 916 Downtown Pleasanton Emerald Glen Park 1,704 Dublin Civic Center Visitor Resident 5

11 1-Dec 2-Dec 3-Dec 4-Dec 5-Dec 6-Dec 7-Dec 8-Dec 9-Dec 10-Dec 11-Dec 12-Dec 13-Dec 14-Dec 15-Dec 16-Dec 17-Dec 18-Dec 19-Dec 20-Dec 21-Dec 22-Dec 23-Dec 24-Dec 25-Dec 26-Dec 27-Dec 28-Dec 29-Dec 30-Dec 31-Dec Unique Device Activity By Day 3000 Tri-Valley Visitor Resident 6

12 California Visitor Home Locations Tri-Valley Top Counties from California outside Study Area 1. San Joaquin, CA 2. Santa Clara, CA 3. San Francisco, CA 4. San Mateo, CA 5. Stanislaus, CA 6. Sacramento, CA 7. Los Angeles, CA 8. Orange, CA 9. El Dorado, CA 10. Placer, CA 7

13 Nationwide Visitor Home Locations Tri-Valley Top Counties outside California 1. Clark, NV 2. Washoe, NV 3. Douglas, NV 4. Maricopa, AZ 5. King, WA 6. Cook, IL 7. Fairfax, VA 8. Salt Lake, UT 9. New York, NY 10. Broward, FL 8

14 Statewide Visitor Home Locations Tri-Valley Shows the home locations aggregated by top 10 states excluding California California 14,127 devices

15 Visitor Arrivals Tri-Valley 1,200 1,

16 Devices Visitor Time Spent Tri-Valley 6,000 5,000 4,000 3,000 2,000 1, Days 11

17 Percent Total Visitor Income Distribution Tri- Valley 35.0% 30.0% 25.0% Mean Income - $92, % 15.0% 10.0% 5.0% 0.0% <$10K $10K - $15K $15K - $25K $25K - $35K $35K - $50K $50K - $75K $75K - $100K >$100K 12

18 Percent Total Resident Income Distribution Tri- Valley 75.0% 70.0% 65.0% 60.0% 55.0% 50.0% Mean Income - $124, % 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% <$10K $10K - $15K $15K - $25K $25K - $35K $35K - $50K $50K - $75K $75K - $100K >$100K 13

19 POI Travel Patterns Tri-Valley Outlets & Downtown Livermore Downtown Livermore & Downtown Pleasanton Outlets & Dublin Civic Center Automotive Museum & Downtown Danville Fairgrounds & Downtown Livermore Fairgrounds & Dublin Civic Center Vineyards & Downtown Livermore Resident Visitor * Most frequent two POI travel patterns 14

20 Unique Device Activity by Hour Tri-Valley :00 AM 2:00 AM 3:00 AM 4:00 AM 5:00 AM 6:00 AM 7:00 AM 8:00 AM 9:00 AM 10:00 AM 11:00 AM 12:00 PM 1:00 PM 2:00 PM 3:00 PM 4:00 PM 5:00 PM 6:00 PM 7:00 PM 8:00 PM 9:00 PM 10:00 PM 11:00 PM Weekday Weekend

21 Thank you!

22 VOLUME XI - ISSUE III SEPTEMBER - NOVEMBER 2017 EDITION PRICE: $545 See use and distribution restrictions on the last page of this report. Downloaded by Barbara Steinfeld, Visit TriValley OAKLAND REGIONAL ECONOMIC SUMMARY Economic activity in the Twelfth District continued to expand at a moderate pace during the reporting period of mid-may through June. Overall price inflation was flat, while upward wage pressures strengthened. Sales of retail goods REGIONAL ECONOMIC SUMMARY were modest, and growth in the consumer and business services sectors remained strong. Conditions in the manufacturing sector improved, and activity in the agriculture sector picked up to a modest pace. Contacts reported robust activity in residential real estate markets, and activity in the commercial sector picked up. Conditions in the financial services sector remained solid. Tourism demand remained strong, although contacts noted that continued uncertainty surrounding immigration policy slowed international bookings at hotels in Southern California. Restaurant sales remained sluggish, and contacts expect the sluggishness to continue through the end of the year. Real estate market activity picked up to a robust pace. Commercial construction activity was solid. Contacts reported an uptick in commercial investment aimed at remodeling and repurposing large retail spaces for healthcare and entertainment services. Financing conditions for commercial projects tightened slightly." Federal Reserve Bank Beige Book, July 2017 Oakland: Next 4 Quarters The arrows show the forecast direction of change over the next 4 quarters vs. the previous 4 quarters. Green indicates the change will be above the long run average, yellow indicates it will be the same, and orange indicates it will be below. Occupancy Occupancy will decrease to 75.0%, a decline over the past 4 quarters' rate of 77.0%, but above the long run average of 67.4% Average Daily Rate ADR growth expectations are weakening, 2.5% vs. the past 4 quarters' rate of 3.3%, and are below the long run average of 3.6% Revenue Per Available Room RevPAR change projections are falling to negative 0.2% as compared to the past 4 quarters' rate of positive 0.6%, and are lower than the long run average of positive 4.6% Supply (orange indicates above long-term average) Supply growth will stay about the same at 2.0%. This is greater than the long run average of 1.3% Demand Forecast demand change is falling, negative 0.7% vs. the past 4 quarters' rate of negative 0.6%, and is below the long run average of positive 2.1% Source: CBRE Hotels' Americas Research, Q VOLUME XI - ISSUE III HOTEL MARKET SUMMARY SEPTEMBER - NOVEMBER 2017 EDITION By year-end 2017, Oakland hotels are forecast to see a RevPAR decrease of 0.9%. This is the result of an estimated decline in occupancy of 2.4% and a 1.6% gain in average daily room rates (ADR). The 0.9% decline in Oakland RevPAR HOTEL MARKET SUMMARY is less than the national projection of a 2.8% increase. Both the upper and lower-priced segments of Oakland are expected to show negative RevPAR change by year end. Upper-priced hotels are forecast to attain a 0.6% gain in ADR, but suffer a 1.4% decrease in occupancy, resulting in a 0.8% RevPAR decline. Lower-priced hotels are projected to experience an ADR growth rate of 1.3%, along with a 3.5% loss in occupancy, resulting in a 2.2% RevPAR decline. Looking towards 2018, Oakland RevPAR is expected to grow 0.6%, reversing the downward trend of Prospects for RevPAR growth in the upper-priced segment (positive 1.1%) are better than in the lower-priced segment (negative 0.3%). Oakland market occupancy levels are expected to range from 74.2% to 75.8% during the 5-year forecast period. Oakland Forecast Forecast Summary Summary YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR % 6.2% $ % $ % % 3.3% $ % $ % % 4.3% $ % $ % % 3.1% $ % $ % % -2.1% $ % $ % 2017F 75.8% -2.4% $ % $ % 2018F 74.6% -1.6% $ % $ % 2019F 74.2% -0.6% $ % $ % 2020F 74.3% 0.1% $ % $ % 2021F 74.8% 0.6% $ % $ % Source: CBRE Hotels' Americas Research, STR, Q Long Run Averages 1988 to 2016 EXHIBIT Occupancy: 1**: Performance 67.4%, ADR Change: Grade 3.6%, vs. RevPAR Long Change: Run 4.6% Average EXHIBIT 1**: Performance Grade vs. Long Run Average 3 Number of Standard Deviations Occupancy ADR Change RevPAR Change -3 '12 '13 '14 '15 '16 '17F '18F '19F '20F '21F Source: CBRE Hotels' Americas Research, STR, Q **See Appendix for exhibit descriptions SEPTEMBER - NOVEMBER 2017 EDITION PRICE: $545

23 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Economic Summary Below are a select number of variables that drive the CBRE Hotels Americas Research econometric forecasts contained in this report. Income and employment are important barometers of economic health and are used in every Hotel Horizons forecast model. The lodging market is part of the larger economy, and the forces that affect us nationally also affect lodging, but in different magnitudes and time periods (see Exhibits 4 and 5 below). Exhibits 2-6 provide an overview of current economic history and forecast, and provide explanation of what to expect in the future, and how that affects the lodging industry. Exhibit 2*: Income Change 15.0% 10.0% 5.0% 0.0% -5.0% Real Personal Income See graph below Exhibit 3*: Employment Change -10.0% -8.0% '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19 '21 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19 '21 Source: CBRE EA, Q Source: CBRE EA, Q % 4.0% 2.0% 0.0% -2.0% -4.0% -6.0% Total Payroll Employment See graph below Exhibit 4*: Quarterly Income vs. RevPAR Change Income (Left) RevPAR (Right) Exhibit 5*: Quarterly Employment vs. Demand Change Employment (Left) Demand (Right) Source: CBRE EA, CBRE Hotels, STR, Q Source: CBRE EA, CBRE Hotels, STR, Q Exhibit 6*: Average Annual Growth Rates 4% 3% Oakland 1988 to 2016 Oakland 2017 to % 2.6% 2.8% 2.9% 2.6% 2% 1% 1.2% 0.9% 1.8% 0% Change in Total Employment Change in Consumer Price Index Change in Gross Metro Product Change in Real Personal Income Source: CBRE EA, Moody's Analytics, Q *See Appendix for exhibit descriptions P. 2 / CBRE HOTELS' AMERICAS RESEARCH

to the CAGRs for the forecast period. Exhibit 7*: Occupancy Change All U.S.")

24 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Hotel Summary The graphs on the left illustrate the magnitude of change in performance during the historical and forecasted period 2012 to Used as a relative benchmark, each market segment is plotted against a common index value of 2012 = 100. This method provides clear insight of how each market segment performed and is expected to perform in relation to others in the specified period. The charts on the right compare near-term historical compound annual growth rates (CAGR) to the CAGRs for the forecast period. Exhibit 7*: Occupancy Change All U.S. Lower-Priced Hotels Source: CBRE Hotels, STR, Q Exhibit 8*: ADR Change All U.S. Lower-Priced Hotels Source: CBRE Hotels, STR, Q Exhibit 9*: RevPAR Change All U.S. Lower-Priced Hotels Upper-Priced Hotels All Hotels Upper-Priced Hotels All Hotels Upper-Priced Hotels All Hotels Exhibit 10*: Compound Average Annual Supply Change Past 5 Years Next 5 Years 2.0% 1.4% 1.0% 0.9% 0.5% 0.0% -0.1% -0.1% -0.1% -1.0% All Hotels Upper-Priced Lower-Priced Source: CBRE Hotels, STR, Q Exhibit 11*: Compound Average Annual Demand Change Past 5 Years Next 5 Years 3.0% 2.5% 2.0% 2.0% 1.5% 1.2% 1.0% 0.6% 0.0% 0.0% -1.0% All Hotels Upper-Priced Lower-Priced Source: CBRE Hotels, STR, Q Exhibit 12*: Compound Average Annual RevPAR Change Past 5 Years Next 5 Years 14.0% 13.2% 12.0% 11.8% 10.8% 10.0% 8.0% 6.0% 4.0% 2.0% 1.5% 1.5% 1.3% 0.0% All Hotels Upper-Priced Lower-Priced Source: CBRE Hotels, STR, Q *See Appendix for exhibit descriptions Source: CBRE Hotels, STR, Q P. 3 / CBRE HOTELS' AMERICAS RESEARCH *See Appendix for exhibit descriptions

25 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Forecast - All Hotels YEAR PERIOD OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Δ SUPPLY Δ DEMAND 2012 Annual 71.5% 6.2% $ % $ % -0.2% 6.0% 2013 Annual 73.8% 3.3% $ % $ % -0.3% 3.0% % 6.0% $ % $ % 0.0% 6.0% % 3.8% $ % $ % -0.1% 3.8% % 2.7% $ % $ % 0.0% 2.7% % 5.2% $ % $ % -0.1% 5.1% 2014 Annual 77.0% 4.3% $ % $ % 0.0% 4.3% % 5.5% $ % $ % -0.1% 5.5% % 3.9% $ % $ % -0.2% 3.7% % 1.8% $ % $ % -0.9% 0.9% % 1.5% $ % $ % -1.0% 0.5% 2015 Annual 79.4% 3.1% $ % $ % -0.5% 2.6% % -0.5% $ % $ % -0.7% -1.3% % -1.3% $ % $ % -0.1% -1.3% % -3.5% $ % $ % 0.6% -2.9% % -2.9% $ % $ % 1.8% -1.1% 2016 Annual 77.7% -2.1% $ % $ % 0.4% -1.7% % -2.9% $ % $ % 2.8% -0.2% % -1.0% $ % $ % 2.9% 1.9% 2017F % -2.6% $ % $ % 3.3% 0.6% 2017F % -3.4% $ % $ % 2.6% -0.9% 2017F Annual 75.8% -2.4% $ % $ % 2.9% 0.4% 2018F Annual 74.6% -1.6% $ % $ % 0.6% -1.0% 2019F Annual 74.2% -0.6% $ % $ % 0.7% 0.1% 2020F Annual 74.3% 0.1% $ % $ % 1.1% 1.2% 2021F Annual 74.8% 0.6% $ % $ % 1.4% 2.0% Q Year to Date 77.7% -0.9% $ % $ % -0.4% -1.3% Q Year to Date 76.2% -1.9% $ % $ % 2.9% 0.9% Q Trailing 4 Qtrs 77.0% -2.6% $ % $ % 2.0% -0.6% Source: CBRE Hotels' Americas Research, STR, Q Exhibit 13*: Oakland Standardized Changes in Real RevPAR Movements Over Time Exhibit 13*: Oakland Standardized Changes in Real RevPAR Movements Over Time 3 2 U.S. Oakland Number of Standard Deviations F 2019F 2021F Source: CBRE Hotels' Americas Research, STR, Q *See Appendix for exhibit description P. 4 / CBRE HOTELS' AMERICAS RESEARCH

26 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Forecast - Upper-Priced Hotels YEAR PERIOD OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Δ SUPPLY Δ DEMAND 2012 Annual 75.2% 6.0% $ % $ % 0.0% 6.0% 2013 Annual 76.9% 2.3% $ % $ % -0.9% 1.5% % 5.1% $ % $ % -0.3% 4.8% % 1.6% $ % $ % 0.0% 1.6% % 1.7% $ % $ % 0.0% 1.7% % 3.6% $ % $ % 0.0% 3.6% 2014 Annual 79.2% 2.9% $ % $ % -0.1% 2.8% % 4.4% $ % $ % 0.0% 4.4% % 3.1% $ % $ % -0.5% 2.7% % 1.4% $ % $ % -1.4% 0.0% % 0.7% $ % $ % -1.4% -0.7% 2015 Annual 81.0% 2.4% $ % $ % -0.8% 1.5% % 0.6% $ % $ % -0.9% -0.4% % -0.6% $ % $ % 0.5% -0.1% % -2.5% $ % $ % 1.5% -1.0% % -2.1% $ % $ % 3.9% 1.7% 2016 Annual 80.1% -1.2% $ % $ % 1.3% 0.0% % -2.9% $ % $ % 6.1% 3.0% % -0.1% $ % $ % 5.1% 5.0% 2017F % -1.8% $ % $ % 5.4% 3.6% 2017F % -1.0% $ % $ % 3.8% 2.8% 2017F Annual 78.9% -1.4% $ % $ % 5.1% 3.6% 2018F Annual 78.4% -0.7% $ % $ % 0.8% 0.1% 2019F Annual 77.8% -0.7% $ % $ % 1.1% 0.3% 2020F Annual 77.9% 0.2% $ % $ % 1.8% 1.9% 2021F Annual 78.1% 0.3% $ % $ % 2.1% 2.4% Q Year to Date 79.8% 0.0% $ % $ % -0.2% -0.2% Q Year to Date 78.6% -1.5% $ % $ % 5.6% 4.0% Q Trailing 4 Qtrs 79.5% -1.9% $ % $ % 4.2% 2.1% Source: CBRE Hotels' Americas Research, STR, Q Oakland Financial Benchmarks* - Full-Service Hotels FULL-SERVICE HOTELS - PERCENT OF TOTAL REVENUE Financial Line Item Mountain / Pacific Region ADR Between $125 & $ to 300 Rooms Rooms Revenue 70.5% 70.9% 72.8% Food and Beverage Revenue 24.3% 24.9% 22.6% Total Departmental Expenses 38.8% 35.5% 37.1% Total Departmental Profit 61.2% 64.5% 62.9% Total Undistributed Expenses 23.1% 25.1% 26.1% Gross Operating Profit** 38.1% 39.4% 36.8% *Data from 2017 Trends in the Hotel Industry report Oakland Upper-Price Average ADR: $ **Before deductions for management fees and non-operating income and expenses. Oakland Upper-Price Average Size: 187 Rooms Source: CBRE Hotels' Americas Research, 2016 For a more comparable and detailed financial comparison, we recommend a Benchmarker SM report. Please contact Viet Vo at for more information. P. 5 / CBRE HOTELS' AMERICAS RESEARCH

27 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Forecast - Lower-Priced Hotels YEAR PERIOD OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Δ SUPPLY Δ DEMAND 2012 Annual 68.2% 6.3% $ % $ % -0.3% 6.0% 2013 Annual 71.1% 4.2% $ % $ % 0.2% 4.5% % 6.7% $ % $ % 0.3% 7.0% % 5.9% $ % $ % -0.1% 5.8% % 3.7% $ % $ % -0.1% 3.6% % 6.6% $ % $ % -0.1% 6.5% 2014 Annual 75.1% 5.6% $ % $ % 0.0% 5.6% % 6.6% $ % $ % -0.1% 6.4% % 4.6% $ % $ % 0.0% 4.6% % 2.1% $ % $ % -0.4% 1.7% % 2.2% $ % $ % -0.6% 1.6% 2015 Annual 78.0% 3.8% $ % $ % -0.3% 3.5% % -1.5% $ % $ % -0.6% -2.1% % -1.9% $ % $ % -0.6% -2.4% % -4.4% $ % $ % -0.2% -4.6% % -3.6% $ % $ % 0.0% -3.6% 2016 Annual 75.7% -2.9% $ % $ % -0.3% -3.2% % -3.1% $ % $ % 0.1% -3.1% % -2.0% $ % $ % 1.1% -0.9% 2017F % -3.4% $ % $ % 1.4% -2.0% 2017F % -5.7% $ % $ % 1.5% -4.3% 2017F Annual 73.1% -3.5% $ % $ % 1.0% -2.5% 2018F Annual 71.3% -2.5% $ % $ % 0.5% -2.0% 2019F Annual 70.9% -0.4% $ % $ % 0.3% -0.1% 2020F Annual 71.0% 0.0% $ % $ % 0.5% 0.5% 2021F Annual 71.6% 1.0% $ % $ % 0.7% 1.7% Q Year to Date 76.0% -1.7% $ % $ % -0.6% -2.2% Q Year to Date 74.1% -2.5% $ % $ % 0.6% -1.9% Q Trailing 4 Qtrs 74.8% -3.3% $ % $ % 0.2% -3.1% Source: CBRE Hotels' Americas Research, STR, Q Oakland Financial Benchmarks* - Limited-Service Hotels LIMITED-SERVICE HOTELS - PERCENT OF TOTAL REVENUE Financial Line Item Mountain / Pacific Region ADR Between $75 & $115 Under 100 Rooms Rooms Revenue 97.5% 98.5% 98.4% Food and Beverage Revenue 0.0% 0.0% 0.0% Total Departmental Expenses 25.5% 27.7% 26.6% Total Departmental Profit 74.5% 72.3% 73.4% Total Undistributed Expenses 26.9% 30.9% 31.0% Gross Operating Profit** 47.5% 41.4% 42.4% *Data from 2017 Trends in the Hotel Industry report Oakland Lower-Price Average ADR: $ **Before deductions for management fees and non-operating income and expenses. Oakland Lower-Price Average Size: 68 Rooms Source: CBRE Hotels' Americas Research, 2016 For a more comparable and detailed financial comparison, we recommend a Benchmarker SM report. Please contact Viet Vo at for more information. P. 6 / CBRE HOTELS' AMERICAS RESEARCH

28 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Airbnb Summary Below is an overview of Airbnb s presence in this market. The estimates of Airbnb performance come from Airdna, a firm that provides data and analytics on Airbnb rental performance for 4 million+ Airbnb listings worldwide. Figure 1 shows the total number of units available, sold and revenue generated during from July 2016 June 2017 along with the calculated Occupancy, Average Daily Rate(ADR), RevPAR, and year-over-year growth rates. Figure 2 shows the percent of units and revenue by unit type. Figure 3 shows the average daily number of active Airbnb units by month. Figure 4 lists the ADRs broken down by unit types and number of bed rooms over the past 12 months. More detailed reports on Airbnb performance in this market can be found at Figure 1: July 2016 June 2017 Airbnb Performance METRIC 2017 Y-o-Y CHANGE Occupancy 63.3% -0.9% ADR $ % RevPAR $ % Available Supply 906, % Units Sold 574, % Total Revenue $65,961, % Source: Airdna, CBRE Hotels' Americas Research, Q Figure 2: Percent of Active Units and Revenue by Listing Type 2017 TTM Active Units 2017 TTM Revenue 3.1% 1.0% 44.5% 52.5% 25.8% 73.3% Entire Home/Apt Private Room Shared Room Figure 3: July 2016 June 2017 Active Units by Month Active Units 4,000 3,500 3,000 2,500 2,000 1,500 1, JUL 2016 AUG 2016 SEP 2016 OCT 2016 NOV 2016 DEC 2016 JAN 2017 FEB 2017 MAR 2017 APR 2017 MAY 2017 JUN 2017 Figure 4: July 2016 June 2017 ADRs by Unit Type and Bedroom Count 2017 Average Daily Rate ($) Glossary Bedrooms Active Units - a unit is considered active if it had at least one night sold during the 1 $ month Average Daily Rate (ADR) - The revenue collected divided by the units sold. Bedrooms - The number of rooms that are available within each unit. 2 $ Entire home/apt Private room Shared room 3 4+ $70.12 $42.28 $ $ Unit Types: Detailed Report on Airbnb data for any U.S. Market Can be found at: Entire Home - The guest has complete and sole access to the entire Unit during the stay. Private Room - The guest has their own sleeping area, but shares access to the Unit common areas with others. Shared Room - The guest rents a common area, like an airbed in a living room. P. 7 / CBRE HOTELS' AMERICAS RESEARCH

29 HOTEL HORIZONS National Horizon Profile 2018 Average Annual Supply Change SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND This page showcases the CBRE Hotels' Americas Research Hotel Horizons forecasting universe. The map below displays average supply change for Quarterly Hotel Horizons reports are available for the nation and all the markets shown below. 2 Albany 2 Dayton 2 Milwaukee 2 Raleigh-Durham 3 Albuquerque 1 Denver 2 Minneapolis 3 Richmond 3 Anaheim 2 Detroit 1 Nashville 2 Sacramento 2 Atlanta 1 Fort Lauderdale 3 New Orleans 3 Saint Louis 1 Austin 2 Fort Worth 1 New York 3 Salt Lake City 2 Baltimore 2 Hartford 2 Newark 2 San Antonio 2 Boston 2 Houston 3 Norfolk-VA Beach 2 San Diego 1 Charleston 2 Indianapolis 3 Oahu 2 San Francisco 1 Charlotte 3 Jacksonville 3 Oakland 2 San Jose-Santa Cruz 2 Chicago 2 Kansas City 2 Omaha 1 Savannah 2 Cincinnati 2 Long Island 3 Orlando 1 Seattle 3 Cleveland 2 Los Angeles 2 Philadelphia 2 Tampa 3 Columbia 1 Louisville 2 Phoenix 3 Tucson 2 Columbus 2 Memphis 2 Pittsburgh 2 Washington DC 1 Dallas 1 Miami 1 Portland 3 West Palm Beach Less Than 2% Between 2% and 5% Greater Than 5% Source: CBRE Hotels' Americas Research, STR, Q P. 8 CBRE HOTELS' AMERICAS RESEARCH

30 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Market Profile Total Room Supply: 19,882 Oakland Top Brands UPPER-PRICED BRANDS PROPERTIES ROOMS % MARKET LOWER-PRICED BRANDS PROPERTIES ROOMS % MARKET Marriott 4 1, % Extended Stay America 10 1, % Courtyard 8 1, % Motel 6 9 1, % DoubleTree % Best Western Plus % Hilton % La Quinta Inns & Suites % Hyatt House % Holiday Inn % Source: STR, Q Oakland Supply Pipeline Upper-Priced Lower-Priced Unclassified / Independent PHASE PROPERTIES ROOMS % MARKET PROPERTIES ROOMS % MARKET PROPERTIES ROOMS % MARKET Unconfirmed % % % Planning % 10 1, % % Final Planning % % % In Construction % % % Total 13 1, % 14 1, % % Source: STR, CBRE Hotels' Americas Research, Q Pipeline Status Definitions PHASE DEFINITION Unconfirmed* Potential projects that remain unconfirmed at this time. STR is unable to verify the existence of these projects through a corporate chain feed or other verifiable source. Planning Final Planning In Construction Source: STR, Q Confirmed, under contract projects where construction will begin in more than 12 months. Confirmed, under contract projects where construction will begin within the next 12 months. Vertical construction on the physical building has begun. This does not include construction on any sub-grade structures including, but not limited to, parking garages, underground supports/footers or any other type of sub-grade construction. *Formerly Pre-Planning P. 9 / CBRE HOTELS' AMERICAS RESEARCH

31 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Oakland Submarket Map Total Room Supply: 19,882 Oakland Submarket Summary Source: CBRE EA, Q SUBMARKET UPPER-PRICED LOWER-PRICED TOTALS Properties Rooms % Market Properties Rooms % Market Properties Rooms % Market Pleasanton / Livermore 18 2, % 24 2, % 42 4, % Northeast / Concord 10 2, % 47 2, % 57 5, % Oakland / Berkeley / Hayward 22 4, % 85 5, % 107 9, % Source: STR, Q Total 50 9, % , % , % P. 10 / CBRE HOTELS' AMERICAS RESEARCH

32 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Submarket Profile - Pleasanton / Livermore Total Room Supply: 4,936 The Pleasanton / Livermore submarket includes hotels in Livermore and Pleasanton, as well as hotels in San Ramon, Dublin, and Danville. Submarket Rank* 104% Pleasanton / Livermore Submarket Inventory UPPER-PRICED PROPERTIES ROOMS %SUBMKT LOWER-PRICED PROPERTIES ROOMS %SUBMKT Inventory 18 2, % Inventory 24 2, % UPPER-PRICED BRANDS BY SHARE PROPERTIES ROOMS %SUBMKT LOWER-PRICED BRANDS BY SHARE PROPERTIES ROOMS %SUBMKT Marriott % Extended Stay America % DoubleTree % Holiday Inn % Courtyard % Motel % Pleasanton / Livermore Construction Pipeline Source: STR, Q UPPER-PRICED LOWER-PRICED UNCLASSIFIED/INDEPENDENT PHASE PROPERTIES ROOMS %SUBMKT PROPERTIES ROOMS %SUBMKT PROPERTIES ROOMS %SUBMKT Unconfirmed % % % Planning % % % Final Planning % % % In Construction % % % TOTAL % % % Source: STR, CBRE Hotels' Americas Research, Q Pleasanton / Livermore Performance - All Hotels All Hotels Penetration vs. Market Total YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR YEAR OCC ADR REVPAR % - $ $ % 97.6% 99.1% % 4.1% $ % $ % % 98.3% 100.6% % 0.2% $ % $ % % 99.9% 98.2% % 4.9% $ % $ % % 102.1% 102.0% % -1.3% $ % $ % % 103.0% 103.7% 2Q16 YTD 78.6% 1.2% $ % $ % 2Q16 YTD 101.1% 103.7% 104.9% 2Q17 YTD 74.4% -5.3% $ % $ % 2Q17 YTD 97.6% 107.2% 104.6% Pleasanton / Livermore Performance - Upper-Priced Hotels Source: STR, Q YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Upper-Priced Penetration vs. Market Total % - $ $ % 2.8% $ % $ % % 80.2% 0.5% -1.2% $ $ % 8.9% $ $ % 7.6% Q16 YTD 81.1% 79.9% 5.5% 1.6% $ $ % 11.4% $ $ % 13.2% Q17 YTD 75.7% -5.2% $ % $ % Pleasanton / Livermore Performance - Lower-Priced Hotels Market Occ ADR RevPAR YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Lower-Priced Penetration vs. Market Total % - $ $ % 76.9% 6.0% 4.0% $80.63 $ % 15.4% $59.72 $ % 20.0% % 75.7% -0.2% -1.5% $90.20 $ % 10.0% $66.68 $ % 8.4% Q16 YTD 76.8% 0.5% $ % $ % 95 2Q17 YTD 72.6% -5.5% $ % $ % Source: STR, Q Source: STR, Q Out of 3 *Based on RevPAR change over the last 4 quarters. Submarket Penetration* *Submarket RevPAR penetration expressed as a percentage of the market RevPAR for the previous 4 quarters. Direction of arrow indicates if penetration is increasing or decreasing relative to one year ago's performance. P. 11 / CBRE HOTELS' AMERICAS RESEARCH

33 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Submarket Profile - Northeast / Concord Total Room Supply: 5,082 The Oakland NE / Concord submarket includes hotels in Concord, Walnut Creek, Richmond, Antioch, Pleasant Hill, Pittsburg, Martinez, Lafayette, Brentwood, and El Cerrito. Submarket Rank* Submarket Penetration* 2 89% Northeast / Concord Submarket Inventory UPPER-PRICED PROPERTIES ROOMS %SUBMKT LOWER-PRICED PROPERTIES ROOMS %SUBMKT Inventory 10 2, % Inventory 47 2, % UPPER-PRICED BRANDS BY SHARE PROPERTIES ROOMS %SUBMKT LOWER-PRICED BRANDS BY SHARE PROPERTIES ROOMS %SUBMKT Marriott % Motel % Hilton % Extended Stay America % Crowne Plaza % Clarion % Northeast / Concord Construction Pipeline Source: STR, Q UPPER-PRICED LOWER-PRICED UNCLASSIFIED/INDEPENDENT PHASE PROPERTIES ROOMS %SUBMKT PROPERTIES ROOMS %SUBMKT PROPERTIES ROOMS %SUBMKT Unconfirmed % % % Planning % % % Final Planning % % % In Construction % % % TOTAL % % % Source: STR, CBRE Hotels' Americas Research, Q Northeast / Concord Performance - All Hotels All Hotels Penetration vs. Market Total YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR YEAR OCC ADR REVPAR % - $ $ % 96.1% 90.3% % 3.9% $ % $ % % 92.6% 87.6% % 9.1% $ % $ % % 90.7% 89.7% % 4.9% $ % $ % % 89.1% 89.6% % -2.9% $ % $ % % 88.2% 88.0% 2Q16 YTD 77.0% -0.5% $ % $ % 2Q16 YTD 99.0% 88.0% 87.1% 2Q17 YTD 77.1% 0.1% $ % $ % 2Q17 YTD 101.1% 88.1% 89.1% Northeast / Concord Performance - Upper-Priced Hotels Source: STR, Q YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Upper-Priced Penetration vs. Market Total % - $ $ % 3.1% $ % $ % % 78.2% 6.7% -3.8% $ $ % 7.1% $ $ % 3.0% Q16 YTD 81.4% 76.8% 2.7% -3.0% $ $ % 8.8% $ $ % 5.5% Q17 YTD 77.9% 1.5% $ % $ % Northeast / Concord Performance - Lower-Priced Hotels Market Occ ADR RevPAR YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Lower-Priced Penetration vs. Market Total % - $ $ % 78.8% 4.6% 6.7% $76.31 $ % 11.4% $50.78 $ % 18.8% % 77.1% 11.1% -2.2% $82.74 $ % 8.9% $61.15 $ % 6.5% Q16 YTD 77.1% 1.3% $ % $ % 80 2Q17 YTD 76.4% -0.8% $ % $ % Source: STR, Q Source: STR, Q Out of 3 *Based on RevPAR change over the last 4 quarters. *Submarket RevPAR penetration expressed as a percentage of the market RevPAR for the previous 4 quarters. Direction of arrow indicates if penetration is increasing or decreasing relative to one year ago's performance. P. 12 / CBRE HOTELS' AMERICAS RESEARCH

34 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Submarket Profile - Oakland / Berkeley / Hayward Total Room Supply: 9,864 The Oakland / Berkeley / Hayward submarket includes hotels in Oakland (primarily on MacArthur Boulevard and Hegenberger Road), hotels in Berkeley (mostly on University Avenue and near University of California Berkeley), and hotels in Hayward (mostly on A Street and Mission Boulevard). Submarket Rank* Submarket Penetration* 3 104% Oakland / Berkeley / Hayward Submarket Inventory UPPER-PRICED PROPERTIES ROOMS %SUBMKT LOWER-PRICED PROPERTIES ROOMS %SUBMKT Inventory 22 4, % Inventory 85 5, % UPPER-PRICED BRANDS BY SHARE PROPERTIES ROOMS %SUBMKT LOWER-PRICED BRANDS BY SHARE PROPERTIES ROOMS %SUBMKT Courtyard % Motel % Marriott % La Quinta Inns & Suites % Hilton Garden Inn % Extended Stay America % Oakland / Berkeley / Hayward Construction Pipeline Source: STR, Q UPPER-PRICED LOWER-PRICED UNCLASSIFIED/INDEPENDENT PHASE PROPERTIES ROOMS %SUBMKT PROPERTIES ROOMS %SUBMKT PROPERTIES ROOMS %SUBMKT Unconfirmed % % % Planning % % % Final Planning % % % In Construction % % % TOTAL 6 1, % 10 1, % % Source: STR, CBRE Hotels' Americas Research, Q Oakland / Berkeley / Hayward Performance - All Hotels All Hotels Penetration vs. Market Total YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR YEAR OCC ADR REVPAR % - $ $ % 103.1% 105.7% % 2.6% $ % $ % % 104.6% 106.5% % 4.1% $ % $ % % 104.9% 106.6% % 1.3% $ % $ % % 104.9% 104.7% % -2.0% $ % $ % % 104.7% 104.5% 2Q16 YTD 77.7% -2.1% $ % $ % 2Q16 YTD 100.0% 104.4% 104.4% 2Q17 YTD 76.7% -1.3% $ % $ % 2Q17 YTD 100.6% 102.7% 103.3% Oakland / Berkeley / Hayward Performance - Upper-Priced Hotels Source: STR, Q YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Upper-Priced Penetration vs. Market Total % - $ $ % 1.7% $ % $ % % 81.0% 2.7% 0.1% $ $ % 7.9% $ $ % 8.1% Q16 YTD 80.9% 81.3% 0.1% 0.4% $ $ % 12.4% $ $ % 12.9% Q17 YTD 80.8% -0.6% $ % $ % Oakland / Berkeley / Hayward Performance - Lower-Priced Hotels Market Occ ADR RevPAR YEAR OCC Δ OCC ADR Δ ADR REVPAR Δ REVPAR Lower-Priced Penetration vs. Market Total % - $ $ % 78.0% 3.4% 2.2% $83.89 $ % 14.9% $60.84 $ % 17.4% % 75.0% 5.2% -3.8% $92.79 $ % 7.7% $70.78 $ % 3.6% Q16 YTD 75.1% -4.1% $ % $ % 95 2Q17 YTD 73.3% -2.3% $ % $ % Source: STR, Q Source: STR, Q Out of 3 *Based on RevPAR change over the last 4 quarters. *Submarket RevPAR penetration expressed as a percentage of the market RevPAR for the previous 4 quarters. Direction of arrow indicates if penetration is increasing or decreasing relative to one year ago's performance. P. 13 / CBRE HOTELS' AMERICAS RESEARCH

35 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND MARKET SEGMENTS - REPRESENTATIVE BRANDS Upper-Priced Lower-Priced Fairmont Embassy Suites Courtyard by Marriott Best Western Plus Best Western Days Inn Four Seasons Hilton Crowne Plaza Comfort Inn Red Lion Econo Lodge Loews Hyatt Hyatt Place Hampton Inn La Quinta Extended Stay America Ritz Carlton Marriott Radisson Holiday Inn Mainstay Suites Red Roof W Hotels Westin Residence Inn TownePlace Suites Quality Inn Value Place EXHIBIT DEFINITIONS Exhibit 1 Exhibits 2-5 Exhibit 6 Exhibits 7-9 Exhibits Exhibit 13 Occupancy levels, ADR change and RevPAR change are plotted on a fixed "grade" scale. Measured as current value minus the mean, divided by the series' standard deviation. Grades: A: Very strong, greater than one standard deviation above long run average. B: Strong, within one standard deviation above long run average C: Somewhat weak, within one standard deviation below long run average. D: Weak, below one standard deviation of the long run average. Year over year change in Income, Employment, RevPAR and Demand, displayed as annual (Exhibits 2 and 3) and quarterly (Exhibits 4 and 5). Average annual Employment, Consumer Price Index, Gross Domestic Product, and Real Personal Income change for the MSA. Index based change charts with base year 2012 = 100, illustrating the magnitude of change. Compound average annual RevPAR, Demand and Supply change for Upper Priced, Lower Priced, and combined (All) hotels within the MSA. Real RevPAR change (inflation adjusted, CPI) of the current period minus the historical mean of Real RevPAR change, divided by the historical standard deviation of Real RevPAR change. FINANCIAL BENCHMARKS The financial benchmarks come from the 2017 edition (2016 data) of Trends in the Hotel Industry, CBRE Hotels Americas Research s annual analysis of hotel financial statements from thousands of properties located across the nation. To benchmark the performance of hotels in the local market, we relied on national operating data from hotels of a similar profile to the average hotel in the subject market. The average room count, occupancy, and ADR of upper-priced hotels were used to analyze the performance of full-service hotels. The average room count, occupancy, and ADR of lower-priced hotels were used to analyze the performance of limited-service hotels. For a more in-depth report with a custom comparable set designed for your individual property or the subject market, see our CBRE Hotels Benchmarker SM service. (pip.cbrehotels.com) HOW WE FORECAST CBRE Hotels' Americas Research prepares hotel market forecasts based on accepted econometric procedures and sound judgment. The two-stage process for producing the forecasts firstly involves econometric estimation of future hotel market activity and financial performance based on historical relationships between economic and hotel market variables, and secondly, a judgmental review of modeled outputs by experienced hotel market analysts. CBRE Hotels and others believe that errors in forecasting are minimized by relying on both data analytics and judgment. ECONOMETRIC MODELS Econometric forecasting represents one of the most sophisticated approaches to gaining insight into future economic activity. Unlike some forecasting methods used in business practice, the models that underlie econometric forecasts contain variables based in economic theory. The forecasts come from historical relationships, similar to statistical correlations, among hotel market measures and economic variables. The measures for the variables come from actual market transactions involving individuals and firms interacting in the economy. Positive Features of Econometric Models: The variables included in the models follow from economic theory. The relationships between variables are estimated with advanced statistical methods. The forecasts developed with econometric models are objectively determined, unlike forecasts based only on judgmental approaches. P. 14 / CBRE HOTELS' AMERICAS RESEARCH

36 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND Gaining insight into the futures of complicated economic environments requires the introduction of multi-level forecasting models. Several equations often need to be identified and estimated to model complex economic conditions such as the national economy. Multi-equation models have considerable appeal for economic forecasting because they explicitly recognize the interdependence of relationships commonly encountered in markets. Perhaps the best example of this type of model is one that involves both the demand side and the supply side of markets, in which prices of goods are set by the interaction of buyers and sellers. Thus, price appears as a variable in both the demand and supply equations. THE EQUATIONS The Hotel Horizons econometric forecasting models fall into the category of multi-equation, demand and supply models. These models have the structure defined below, but vary in their construction for particular market applications (e.g., different cities and hotel market segments). The three estimated equations are: 1. Demand for hotel rooms is primarily driven by the general level of economic activity in the nation or city, as measured by income and employment. The equation recognizes the fundamental relationship between room purchasing behavior and either growth or decline in the relevant economy. Both economic theory and historical data relationships strongly support the inclusion of ADR in the demand equation because lower ADRs motivate increases in travel and leisure spending, while higher ADRs motivate decreases. 2. Supply change - In historical lodging data, a strong relationship exists between growth in the supply of new hotel rooms and priorperiod lodging market conditions. In the equation, new hotel room growth in modeled as a function of past levels of new room growth, past ADR, and past occupancy levels. 3. ADR movements are correlated with room scarcity in the market. The equation which estimates ADR defines ADR as a function of past room rates and contemporaneous occupancy levels. The parameters (i.e., coefficients on each variable) then are used to forecast demand, supply change, and RADR by multiplying the parameters by CBRE Econometric Advisors and Moody s Analytics forecasts of the economic variables and relevant previously estimated values (lagged variables). Three additional calculations are made with these results, as follows: 1. Supply change is added to the previous-period number of available rooms to produce an available rooms level in future periods. 2. Number of rooms sold is divided by number of available rooms to obtain occupancy percent in each future period. 3. Expected inflation is added to real ADR to convert to nominal ADR. JUDGMENTAL INTERVENTION A committee of hotel experts from CBRE Hotels' Americas Research performs a thorough review of each model prediction. These assessments are made by locally-based hotel experts working in the various offices around the U.S. The quarterly forecasts for the current and forecast period years are subject to review. The committee modifies the model s market prediction when there is compelling evidence that factors have come into play that the model could not possibly foresee. A Super Bowl-type event, as an extreme example, would cause the committee s forecast to differ noticeably from the model's prediction not only in the city in which the event will occur, but also competing cities within the region. In most instances, however, the committee either defers to the model prediction or makes modest adjustments. Economic Data from July, 2017 Hotel Data from June 2017 P. 15 / CBRE HOTELS' AMERICAS RESEARCH

37 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND What Has Changed Since The Last Report? Forecasts are valuable tools for developing expectations of key variables. Changes to forecasts occur for two primary reasons. The first is adjustments to historical series made by the data provider, causing future periods to vary due to changes in their base. The second is that economic expectations tend to shift as more information becomes available, thus moving the hotel variables according to their underlying relationships. We are constantly re-evaluating the performance of our forecasts, and presented below is a view on how the world has changed since the June - August 2017 issue, presented in same period, prior year change format. All data under "This Report" are actual through 2nd Quarter Data marked as "Last Report" are actual through 1st Quarter 2017, with 2nd Quarter 2017 being the first forecast period for that report. As noted on earlier pages, all of the hotel variables below are modeled using data from Moody's Analytics. It is important to note that all historical data are subject to revision. At the beginning of each year, STR, our source for historical lodging data, repositions the chain-scale classifications for branded properties, and chain-class categories for independent hotels. The reclassifications are based on the ADR achieved the prior year. Because of these reclassifications, the historical data presented in this report may differ from the historical data presented in prior Hotel Horizons reports. Further, the reclassifications may have influenced our forecasts of future performance st Qtr 2nd Qtr 3rd Qtr F 4th Qtr F Year End Year End Year End CHANGE IN REAL PERSONAL INCOME* This Report 3.4% 3.3% 2.9% 2.8% 3.1% 2.1% 2.8% Last Report 2.7% 2.2% 2.5% 3.0% 2.6% 2.2% 2.8% CHANGE IN TOTAL PAYROLL EMPLOYMENT* This Report 2.4% 2.0% 1.6% 1.0% 1.8% 1.0% 0.1% Last Report 2.7% 2.5% 2.0% 1.6% 2.2% 1.1% 0.0% CHANGE IN SUPPLY** This Report 2.8% 2.9% 3.3% 2.6% 2.9% 0.6% 0.7% Last Report 2.8% 3.5% 4.0% 3.7% 3.5% 1.8% 1.2% CHANGE IN DEMAND** This Report -0.2% 1.9% 0.6% -0.9% 0.4% -1.0% 0.1% Last Report -0.2% 0.5% 1.9% 1.6% 1.0% -0.1% 0.0% CHANGE IN OCCUPANCY** This Report -2.9% -1.0% -2.6% -3.4% -2.4% -1.6% -0.6% Last Report -3.0% -2.9% -2.0% -2.0% -2.5% -1.9% -1.2% CHANGE IN ADR** This Report 1.8% 0.6% -0.2% 4.7% 1.6% 2.3% 1.7% Last Report 1.8% 1.9% 1.6% 6.4% 2.9% 2.6% 2.5% CHANGE IN REVPAR** This Report -1.2% -0.4% -2.7% 1.1% -0.9% 0.6% 1.2% Last Report -1.2% -1.0% -0.4% 4.3% 0.4% 0.7% 1.3% * Economic data (history and forecast) are from CBRE EA, Q ** Hotel performance data: History supplied by STR; Forecast developed by CBRE Hotels' Americas Research, Q and 2018 Year End Forecast Change in RevPAR % 0.4% 0.7% -0.9% Source: CBRE Hotels' Americas Research, Q This Report Last Report P. 16 / CBRE HOTELS' AMERICAS RESEARCH

38 HOTEL HORIZONS SEPTEMBER - NOVEMBER 2017 EDITION OAKLAND GLOSSARY OF TERMS ADR Occupancy RevPAR Supply Demand LRA Penetration Standard Deviation Average Daily Rate - rooms revenue divided by paid rooms occupied. Paid rooms occupied divided by available rooms. Revenue per Available Room - rooms revenue divided by available rooms. Average daily room nights available per quarter, represented as a change over previous year, same quarter except where noted annually. (Accommodated Demand) Average daily room nights occupied per quarter, represented as a change over previous year, same quarter except where noted annually. Long Run Average - Annual average from 1988 to last complete year end. Market area (or sub-market area) measurement as a percent of national (or market area) measurement. The plotting of a normal data series and how far each individual data point lies from the mean: 68.2% of the series will fall within 1 standard deviation, 95.4% of all data points will fall within 2 standard deviations, and 99.7% falling within 3 standard deviations of the mean. For more information about this market please contact: Chris Kraus at chris.kraus@cbre.com CBRE HOTELS CBRE HOTELS Dallas New York LEADERSHIP CONSULTING Jeff Binford Mark VanStekelenburg jeff.binford@cbre.com mark.vanstekelenburg@cbre.com Kevin Mallory National Practice Leader CBRE Hotels' Global Head Tom Huffsmith Houston Philadelphia kevin.mallory@cbre.com Senior Managing Director Randy McCaslin Tony Biddle tom.huffsmith@cbre.com randy.mccaslin@cbre.com anthony.biddle@cbre.com CBRE HOTELS Daniel C. Hanrahan II AMERICAS RESEARCH Atlanta Indianapolis daniel.hanrahan@cbre.com Scott Smith Mark Eble Mark Woodworth scott.smith@cbre.com mark.eble@cbre.com San Francisco Senior Managing Director Jill Bidwell Chris Kraus mark.woodworth@cbre.com jill.bidwell@cbre.com Jacksonville chris.kraus@cbre.com Hank Staley Jack Corgel Bozeman hank.staley@cbre.com Seattle Managing Director Chris Kraus Chris Kraus jack.corgel@cbre.com chris.kraus@cbre.com Los Angeles chris.kraus@cbre.com Bruce Baltin Jamie Lane Chicago bruce.baltin@cbre.com Washington, D.C. Senior Economist Mark Eble Jeff Lugosi Kannan Sankaran jamie.lane@cbre.com mark.eble@cbre.com jeff.lugosi@cbre.com kannan.sankaran@cbre.com For more reports visit our store at Hotel Horizons is compiled and produced by CBRE Hotels Americas Research. Readers are advised that CBRE Hotels Americas Research do not represent the data herein to be definitive, neither should the contents be construed as a recommendation on policies or actions. Quotation, reproduction or transmittal (in any form or by any means, whether electronic, photocopying, recording or otherwise) is not permitted without consent from CBRE Hotels Americas Research. Please address inquiries to Hotel Horizons, 3280 Peachtree Road NE, Suite 1400, Atlanta, GA Phone: (855) Copyright 2017 CBRE Hotels Americas Research. All rights reserved.

39 TRI VALLEY, CALIFORNIA TRAVEL IMPACTS, P JUNE 2017 Prepared for Visit Tri-Valley 5075 Hopyard Road, Suite #240 Pleasanton CA Dean Runyan Associates 833 S.W. Eleventh Avenue, Suite 920 Portland, Oregon

40 Introduction Travel and tourism are an important component of the economy in the Tri Valley Region of Alameda and Contra Costa Counties in California. This region is defined as the communities of Dublin, Livermore and Pleasanton in Alameda County and Danville in Contra Costa County. The attractive landscape, pleasant weather, established visitor services and attractive features such as gourmet wine and food bring both overnight and day visitors to the area. This research describes the economic benefits of these visitors, with primary findings covering the period 2012 through Findings include travel-generated sales, employment and payroll that these sales support, and the associated state and local tax receipts. In addition there are estimates of overnight visitor volume and the associated average spending. Methodology Overview The figures for Tri Valley are prepared from research for Alameda and Contra Costa Counties that is prepared for Visit California, augmented with the most recent data available for the Tri Valley Region. Figures representing 2016 are preliminary in that certain data involved in the analysis are not available in final form until after this report is prepared; for analysis purposes these are estimated on the basis of previous year data and trends. Overall findings typically vary little when final data are available. Region Definition and Population The Tri Valley Region consists largely of four communities, Livermore, Pleasanton and Dublin in Alameda County and Danville in Contra Costa County. The Tri Valley area represents about 13% of Alameda County and somewhat under 7% of Contra Costa County. The dominant portions of these counties abut San Francisco Bay and are very oriented to the economic activity of the East and South Bay region. Population, Alameda and Contra Costa Counties and Tri Valley Portions Population 2015 Alameda County Contra Costa County Location Number Percent Number Percent Tri Valley 217, % 75, % Remainder 1,421, % 1,047, % Total County 1,638, % 1,123, % Source: US Census 1

41 Commercial Lodging Commercial lodging is somewhat more concentrated in the Tri Valley area than is population, as appears in the table below. About 16% of commercial lodging units of the two counties are located in the Tri Valley Region. Commercial Lodging Inventory, Alameda and Contra Costa Counties, Tri Valley Region Lodging Sales Commercial Lodging Units Alameda County Contra Costa County Total Location Number Percent Number Percent Number Percent Tri Valley 3, % % 3, % Remainder 13, % 6, % 20, % Total County 17, % 6, % 23, % Source: STR, Dean Runyan Associates Lodging sales in the Region have grown substantially since 2012 but are concentrated in the Tri Valley Region in a manner very similar to lodging units, with the Region representing somewhat under 16% of all sales in the two-county area. Lodging Sales, Alameda and Contra Costa Counties, Tri Valley Region Annual Sales ($M) Location Alameda County Tri Valley Portion Percent 20.8% 20.5% 19.7% 19.8% 19.9% Contra Costa County Tri Valley Portion Percent 1.3% 1.3% 1.2% 1.1% 1.2% Total Region Tri Valley portion Percent 16.0% 15.9% 15.3% 15.5% 15.7% Source: STR, Dean Runyan Associates 2

42 Camping Campground capacity in Alameda County is concentrated in the Tri Valley Region, while most Contra Costa County camping is outside the area. Travel Spending Campground Units, Alameda and Contra Costa Counties, Tri Valley Region Campground Units Alameda County Contra Costa County Location Number Percent Number Percent Tri Valley % % Remainder % % Total County % % Source : Woodalls, Dean Runyan Associates Tri Valley travel spending has increased steadily since 2012, rising from $557 million to $646 million, an annual average increase of approximately 3.8%. Most of this growth is attributable to visitors staying in commercial lodging. Tri Valley Travel Spending, p Travel Spending ($M) Category p Commercial lodging Private home Campground Vacation home Day Total Source: Dean Runyan Associates 3

43 Travel Spending by Type of Visitor Accommodation, 2016p Commodities Purchased Travelers to the Tri Valley Region spent the most on food service and accommodations, with substantial spending on retail as well. Purchases of visitor air transportation relate to the location of the Oakland International Airport in Alameda County. Visitor Spending by Commodity Category, 2016p Employment and Earnings Total 2016 earnings in the Tri Valley Region that are attributable to visitor spending totaled $281 million, with the largest portion ($132 million) in accommodations and food service 4

44 businesses. The Other Travel category includes earnings for such things as air transportation, travel arrangement and visitor industry services for meetings and visitor bureaus. Earnings, Tri Valley Region, 2016p Visitor spending supports a total of 5,900 jobs in the travel industry and related businesses. Jobs in the Tri Valley Region, by Business Category, 2016p Tax Receipts Local 2016p tax receipts, consisting of lodging tax, plus sales, TID and property taxes, amounted to $32.8 million. State taxes were $34.2 million, totaling $67 million. 5

45 Visitor Volume and Average Expenditures Visitor volume for the Tri Valley Region rose from 1.55 million visitors (person trips) in 2014 to 1.6 million in A substantial portion of visitors stayed with friends or relatives. Average expenditures Tri Valley Visitor Volume, p Person Trips (000) Party Trips (000) Lodging Category p p Commercial lodging Private home Other Total 1,558 1,581 1, Source: Dean Runyan Associates Note: "Other" consists of camping and vacation home categories. Overall expenditures for overnight visitors averaged $95 per person per day, and $198 per party per day. Those staying in commercial lodging spent substantially more, $238 per person per day and $498 per party per day. Notes Regarding Methodology Average Daily Spending, 2016p Daily Spending per Lodging Category Person Party Commercial lodging $238 $498 Private home $37 $76 Camping $65 $196 Vacation Home $85 $183 All Overnight $95 $198 Source: Dean Runyan Associates The estimates in this report are expressed in current dollars. There is no adjustment for inflation. The economic impact measurements represent only direct economic impacts. Direct economic impacts include only the spending by travelers and the employment generated by that 6

46 spending. Secondary effects related to the additional spending of businesses and employees are not included. The employment estimates in this report are estimates of the total number of full and part-time jobs directly generated by travel spending, rather than the number of individuals employed. Payroll and self-employment are included in these estimates. 7

47

48

49

50

51

52

53

54

55 Visit Tri-Valley REGIONAL TOURISM ASSET ASSESSMENT Prepared for: Visit Tri-Valley 5075 Hopyard Rd, Suite 240 Pleasanton, CA Solutions for your competitive world.

56 Visit Tri-Valley Table of Contents Executive Summary 3 Part 1: Understanding Tourism Assets 7 Part 2: Existing Regional Assets 13 Part 3: Pipeline Projects 21 Part 4: Tri-Valley Tourism Asset Gaps 23 Part 5: Developing a Tourism Asset Strategy 44 Part 6: Summary Comments 45 Appendix 46 Appendix 1: Completed interviews 47 Appendix 2: Sources 48 Appendix 3: Project Overview 49 Appendix 4: Scope of Work 50 2 P a g e

57 Visit Tri-Valley Executive Summary The following report was developed in an effort to improve Tri-Valley s long term competitive position in the Northern California tourism market> the report sought to identify current tourism related destination assets as more importantly potential tourism asset gaps. The report also seeks to define a tourism strategy that can improve the competitive position of Tri Valley over the long term. The report identifies several key challenges including the lack of perception the region has as a destination and that it is seen by some to be a series of communities. Additionally, the areas have significant differences between them. For example, Livermore, with its downtown area and wineries, is a very different experience to San Ramon, which generates a significant level of corporate travel. Moving forward Tri-Valley needs to consider three specific steps with regard to its assets. 1. Continue to build its brand assets in order to create value for all of the areas within the region. 2. Continue to promote all of the area s assets and experiences. 3. Add both tangible and intangible assets over the long and short term. The report identifies a number of assets needs both tangible and intangible. Tangible Asset Needs 1. Develop a Broader Lodging Supply Mix One of the most frequently mentioned needs expressed by those interviewed was the need for a broader lodging supply mix to attract different visitor segments 2. Develop Additional Meeting and Convention Space The ability to attract more business travel for meetings and conferences is impacted by the lack of a significant meeting and convention facility capable of handling larger groups for corporate, association or industry gatherings as well as limited availability mid-week lodging supply given the current occupancy rates. Tri-Valley s lack of a confined city space is also a disadvantage. 3. Leverage Existing Performing Arts and Cultural Venues The desire to upwardly impact leisure visitation in the Tri-Valley region must focus on demand generators that draw visitors based upon some affinity. An additional demand generator that can be looked to is performing arts and cultural events. 3 P a g e

58 Visit Tri-Valley 4. Additional Recreation Facilities Stakeholder interviews identified the need for additional indoor and outdoor sports facilities that would both provide benefits for local residents as well as serve as a tourism trip generator to the region 5. Infrastructure Related Opportunities Transportation system(s) A number of stakeholder interviews identified transit as a significant concern, one that has a negative impact on the potential for tourism. San Ramon City Center One of the biggest potential opportunities within the region is the development of the San Ramon City Center. Signage & Wayfinding One area of need that was expressed by a number of stakeholders was the need for signage and wayfinding. 6. Cultural Assets Several interviews identified the need for additional cultural assets including museums, theaters and performing arts venues Intangible Assets Needs 1. Data and Information One of the key intangible asset needs is comprehensive tourism economic and market research. 2. Soft Tourism Infrastructure Another important intangible asset that needs to be added to Tri-Valley area is that of region wide organizations that can be a part of the tourism infrastructure. Below are the types of organizations that can be of assistance in growing tourism. Tri-Valley Regional Arts Committee A regional arts committee could provide significant support by developing programming that can be presented in a regional context. Tri- Valley Region Lodging Association A unified lodging industry association that meets periodically to discuss trends, market opportunities and market challenges while working with Visit Tri-Valley can be an important part of assisting the organization in being as effective as possible. 4 P a g e

59 Visit Tri-Valley Performing Arts Facility Association An organization that includes each of the performing arts facilities could provide an integrated calendar that could be presented region-wide and also provide a cohesive approach to entertainment within the region. Sports Commission- This organization would unify regional sports facilities in an effort to attract tournaments, swim meets track meets etc. in an effort to generate weekend occupancy. 3. Marketing Related Assets Within the conversation on tourism assets, a number of marketing related issues were identified. They include the following: Visitor information One of the opportunities to present a consolidated regional experience is to provide an integrated approach to branded visitor information. More funding for marketing Currently Visit Tri-Valley is funded by a Tourism Business Improvement District (TBID) which has become a funding mechanism for over seventy destinations throughout California. It will be important for Visit Tri-Valley s long term competitive position to also increase its available funding. Additional marketing/brand development Several stakeholders identified the need to increase the awareness and presence of the Tri-Valley brand. More diversified marketing In an effort to broaden the attraction of the Tri-Valley region to leisure visitors it s important to broaden the awareness of all of the activities available. Action step(s): 4. Process Related Assets A final area of interest expressed by stakeholders was related to the process of how things get done within Tri-Valley. Specifically it was suggested that Tri-Valley create a more collaborative mindset and improve the connectivity of the region. Developing a Tourism Asset Strategy In considering a long term tourism asset strategy one of the benefits the region has is an incredibly strong business travel segment which provides very strong mid-week occupancy for the flag properties. It is anticipated this trend will continue for the following reasons: Continued growth of the greater Bay Area economy specifically the South Bay tech industry. Favorable commercial real estate prices compared with Silicon Valley should continue to fuel commercial real estate demand The proposed San Ramon City Center. 5 P a g e

60 Visit Tri-Valley Given these strategic changes in the marketplace it is clear that the Tri-Valley region will continue to have a strong business travel segment. This anticipated strong business travel segment presents a unique opportunity for Tri-Valley to strengthen the overall tourism economy by strategically supporting assets that will also grow the leisure side of the market. This Business Travel Plus strategy provides the region a unique opportunity to grow overall tourism. 6 P a g e

61 Visit Tri-Valley Part 1: Understanding Tourism Assets Tourism assets can be defined in the following way: Any county, city, town or region that has a feature that attracts people and resulting travel spending that contributes to revenues, employment and taxes for that location. When considering tourism in general and Tri-Valley specifically, it is important to understand the elements that comprise the tourism experience. These elements/assets are outlined by McIntosh, Goeldner and Ritchie 1, and include the following: Tourism Element Characteristics 1. Natural Resources Natural assets unique to the region. 2. Infrastructure Air access, roads, utilities, etc. All elements that help support the visitor s experience. 3. Hospitality Human elements that interact and serve the visitor. 4. Visitor Services Hotels, food & beverage and retail services designed to assist the tourist. 5. Attractions Natural and built facilities, events and local residents that provide visitors with experiences. 6. Local Culture Culture is what makes the destination unique and real and provides memorable experience to visitors. 7. Organizational Organization and processes that work to attract visitors to the destination using a variety of promotional techniques. It is clear that while Tri-Valley offers a number of resources including attractions, local culture, organizational hospitality, and some infrastructure, the lack of a major natural asset (e.g. mountains, lakes, oceans), or significant natural resources and attractions, the remaining 1 McIntosh, Goeldner and Ritchie Tourism: Principles, Practices and Philosophies and the Strategic Marketing Group 7 P a g e

62 Visit Tri-Valley elements including infrastructure, hospitality, and visitor services are mixed. The area is very weak on organizational efforts and funding designed to attract visitors. In addition to the above tourism elements, it is important to recognize that these elements in and of themselves are not enough. In order to truly maximize the area s efforts, the following support is needed: A market-focused and market-driven strategy Too often organizations and regions can lose focus on marketing efforts and become concerned with political matters. A market-driven strategy can help refocus efforts. Funding In order to realize its stated goals, an organization needs to allocate the necessary funds to achieve the identified goals. Cooperation It is critical for all elements and areas of the county to work together to achieve mutual marketing objectives. Vision The tourism industry and its stakeholders need to provide a vision for the greater community. Community Benefits If all of these components work in unison, and are supplemented with the necessary resources and funding, the local community should benefit in a number of areas, including those illustrated below. Enhanced quality of life Recognition of the importance of protecting natural elements adds to visitor satisfaction as well as the local quality of life. Improved infrastructure and local services Tourism generated tax dollars can play an important role in municipal and county funding for local services. Jobs and business improvement Tourism often adds to the revenues that, in turn, increase employment and strengthen local business. Enhanced image and economic development value will help to attract and retain business entities. 8 P a g e

63 Visit Tri-Valley Positive Return on Investment (ROI) The combined benefits derived from a multi county-wide (Contra Costa and Alameda) tourism promotion effort can provide a positive ROI over the long-term for the entire community. Community Pride Pride in the community leads to reinvestment/further buy-in from the community. It is important to understand the overall regional demand drivers, namely those assets which actually drive consumer demand and visitation to the area. These demand generators include favorable climate; the wine and dining experience; special events that attract visitors and appeal to their interests; and specific niche activities that visitors engage in, ranging from golf to hiking, arts shopping and biking etc. It should also be noted that demand for the destination (specifically in the case Livermore) is also generated by two National Labs with corporate travel to the area s local governments and businesses. Business travel (specifically in San Ramon and Pleasanton) is another additional reason why people travel to Tri-Valley. In addition to the Livermore Labs, the area is home to a number of major corporations that generate travel to the area. Figure 1 Tri Valley Regional Tourism Demand Driver Assets Wine/Dining Shopping Downtowns Tri-Valley Recreation Special Events Corporate Travel Government/ Livermore Laboratory 9 P a g e