earnings of $29,000/day

|

|

|

- Patricia Howard

- 6 years ago

- Views:

Transcription

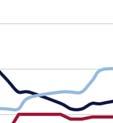

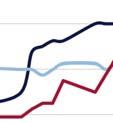

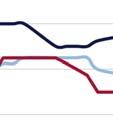

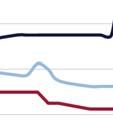

1 WHAT A WAY TO END THE YEAR 19 th December 2014 Summing up 2014 in just a few words seems like an impossible task, soo much has happened making it difficult to know where to start. Geopolitics has certainly playedd a part with disruptions in Libya, ISIS in Iraq/Syria, protracted talks over Iran the crisis in Crimea helping the oil price to peak at $116/bbl before falling to less than $60/bbl this week which is somewhat remarkable against a backdrop of such political instability. OPEC s decisionn to avoid cutting production has lent support to the tanker market despite slower oil dem growth. Whilst in the short term this is undoubtedly a positive for tankers, a persistently low oil price will discourage investmentt in higher cost fields. However, lower oil prices typically stimulate consumption subsequent tanker dem. Much was ( still is) saidd about floating storage, but the reality is that we just haven t seen a wide enough contango structure to make tanker storage profitable. However, with a surplus of crude rapidly building, floating storage could make sense later in a tantalising prospect for owners. Of course in the latter stages off this year owners have seen their earnings improve off the back off lower fuel costs. Bunker pricess peaked to averagee $591/tonne (Rotterdam HSFO) in June but December too date averaged just $342/tonne saw a strong start for the crude sector with TD3 (AG-Japan) averaging $35,000/day through January February before softening to average $18,000/da$ ay over Q2/3. However Q4 failed to disappoint with earnings averaging $50,000/day for f the period to date VLCC earnings in excess of $80,000/day at the time of writing. On the whole, VLCC owners will end 2014 much better than 2013 with earnings averagingg in the region of $29,000/day the highest annual average since Suezmaxes were able to achieve TCE T earnings of $25,500/day over the course of the year, levels not seen since 2008 promptingg much attention to the sector as can been seen from the 48 orders placed this year. Aframaxes benefitted from a volatile market subsequently earnings surged to average $24,500/ /day in part thanks to earnings of nearly $80,000/day in January. At times the product sector has been less inspiring, sentiment has shifted towards the crude sector. MRs suffered throughoutt the year as growing fleet supply continued to impact upon earnings. C2/TC14 (UK Cont-USAC/USG-UK Cont) triangulation earningss struggled to average $11,500/day in Q1-Q3. However ownerss were able to achieve triangulation earnings of $29,000/day in the final quarter. LRs took a while to get going but were not as a sluggish as the MRs. LR2s trading between the Middle East Gulf Japan earned just $11,000/day in the first half of 2014, but achieved $24,500 in the second half. The story was similar for LR1s which also achieved $11,000/day in the first half generating better returns of $19,500/day for the second half of the year. These rate improvements mean LR1s/LR2s earnings are the highest since 2008 yet many owners will still requiree higher levels to breakeven onn their investments (see our 12 th December report). Overall crude tanker supply growth slowed in 2014 with VLCC deliveries outstripping scrapping/conversionss to see year end fleet growth of 12 vessels. By comparison the Suezmax fleet grew by just 3 vessels, Aframax/LR2s contracted by 7 vessels Panamax/ LR2s by 5. Of course the story is significantly different withh MR/Hies wheree supply grew by 79 vessels a heavy orderbook set to deliver over the next 2/3 years. Tanker orders have been significantly lower at 172 units at the time off writing, down from 336 a year prior. Suezmaxes received the greatest attention with 48 units booked, VLCC ordering activity declined slightly to 38 orders. Aframax/LR2 orders declined significantly over 2013, with justt 21 orderss placed (coated/non coated) down from 63 a year earlier. It seems hard to believe that t in not one owner pulled

2 the trigger on LR1/Panamax orders is therefore little surprise to see 27 orders make the cut this year. Fortunately MR ordering has nosedived this year following the realisation that 225 orders in 2013 was more than ample, subsequently we have seen just 38 orders placed for Looking ahead the theme of compliance continues. Owners will w be faced with the challenge of complying with emission control regulations from the 1 st of o January Additionally the ballast water management convention may finally be ratified in 2015, meaning it would enter in to force 12 months later another significant cost for vessels without ballast water treatment facilities already on board. Rates VLCCC Suezmax Aframax LR2 LR1 MR (TCEs at market speed ) Middle East - Japan West Africa - UKCont North Sea - UKCont Middle East - Japan Middle East - Japan UKCont - USAC December 2013 WS TCE/day 62 $51, $45, $47, $12, $12, $10,250 December WS TCE/day WS Low WS High 69 $76, $32, $34, $27, $21, $33, Single Hull vs. Double Hull End 2014 S.Hull D.Hull VLCCC Suezmax Aframax/LR2 Panamax/LR1 Hy/MR ,7688 NB: Almost all of the remaining S/H tankers are nott actively trading in conventional tanker markets. Tanker Orderbook (25,000 dwt+) excluding options New Deliveries (25,000 dwt+ +) 61.7 M dwt (587 vsls) 20.7 M dwtt (169 vsls) 65.0 M dwt d (561) 15.8 M dwt d (157) Brent Oil Price (ICE Close) Bunkers 380cst Fujairah / Rotterdam $110.80/bbl (31 st Dec) $59.27 (18 Dec) $623 / $5933 tonne $330 / $ 308 tonne World Oil Production (November) OPEC crude production Non OPEC -inc OPEC NGL & Biofuels World Oil Dem 88.8 M b/dd (+0.8%) 29.5 M b/dd (-4.8%) 59.9 M b/dd (+3.8%) 91.7 M b/dd (+1.7%) 90.7 M b/d b (+2.1%) 30.3 M b/d b (+2.7%) 61.3 M b/d b (+2.3%) 92.4 M b/d b (+0.7%) Tankers Demolished (25,0000 dwt+) Lwt price - China / India VLCC s sold for scrap number /dwt US$: M dwtt (107) $340 / $ vessels / 6.1 M dwt $ (311 st Dec) 8.2 M dwt (74) $235 / $ vessels / 3.5 M dwt $ (18 th Dec)

3 CRUDE Middle East VLCC Charterers initially kept the party throbbing, Owners spun rates up to over wss 80 to the East, as a result. However, as December fully closed, full January programmes were awaited, the music died, some noticeable discounting quickly took over to bring levels down to around ws 70 East mid ws 30 s to the West. A last minute pre-holiday shopping spreee will be keenly hoped for by Owners to prevent more deterioration. Suezmaxes trod a steadier path. Activity simmered, rather than bubbled, but it proved sufficient to keep rates averaging in the mid ws 90 s East, low/midd ws 40 s to the West, though some very late-week action now sets a potentially steeper path over the next period. Aframaxes scratched around for most off the week rates suffered accordingly to sub 80,000 by ws 115 to Singapore with further slippage s onn the cards. West Africa Suexmaxes had a mixed bag of a week, starting slowly with rates easing gently, but from mid-week enjoying a relative fixing-fest lines, which allowed for the market to gain legs to 130,000 by ws 90+ to Europe, d ws as Charterers cleared their pre-holiday 85 to the US Gulf, though consolidation, rather than acceleration is now the watchword. VLCCs also started slowly, but the dip in the Middle East provoked more interest to the East with ws 68.5 'last done', lower levels likely to be posted within short. Mediterranean A reversal in fortunes for Aframaxes here. Last week s gains evaporated upon stagnant enquiry, cancellation of a number of Libyan stems didn t help either. Rates fell off to 80,000 by ws 97.5 X-Med, could slip a little further. Suezmaxes bumped up significantly to t 140,000 by ws 115 from the Black Sea too European destinations on solid interest, but oncee the shelves had been cleared, the market m had to exist upon crumbs, rates slipped to ws with signposts pointing strongly further South. Caribbean Aframaxes hadd high hopes of holiday shopping, but the tills stayed rather quiet rates slipped badly to 70,000 by ws upcoast it ll need a veritable fixing frenzy to clear enough availability to allow for a significant turnaround. VLCCs saw little, but it didn t need n muchh to keep Owners' plate spinning at $7.25 millionn to Singapore, $6.4 million to West Coast India, with little early change likely whilst local supply remains so limited. North Sea Healthy levels of Aframax enquiry, but a nondescript result. Rates operate with an 80,000 by ws 117.5/120 range r X-UKC, at 100,000 by ws 95/97.5 from the Baltic. Holiday plans will now be prioritised for many, d a flat period forecast. VLCCs found one o or two things to do - but not more. $5.3 million was w paid, however, for fuel oil to Singapore, d $7.175 million for Crude oil fromm Hound Point to South Korea to at least provide some talking point for f the industry chatteratti.

4 CLEAN PRODUCTS East LR1s have remained fairly tight on tonnage but volumes have been less, so rates have just drifted from the elevated level they reached the week before. 55,000 mt Naphtha AG/Japan is now at ws ,000 mt jet AG/UKC is hovering around $2.05 million. The big Christmas slow down is coming but with MRs super tight there will be enough shorthaul stems to keep the LR1s busy for now. LR2s have seen a slight resurgence this week with the first decade January Naphtha stems hitting the market ships quickly thinning out. Rates are back to last weeks levels may move a touch higher. 75,000 mt Naphtha AG/Japan is now ws ,000 mt Jet AG/UKC is upto $2.70 million again are fixing at ws 125 levels. East Africa has been in high dem, with a host of early January liftings the market has slowly firmed with ws 175 on subjects. AG to the UKC has been very busy also Owners have been pushing rates up, it has peaked at $1.7 Million, which is a rise of $225,000 over the course of the week. The shorthauls have also seen firming with X-AG close to $350,000. Next week is disjointed given the holidays, but the firmness is expected to last into the New Year. Disappointingly for shipowners, the North Asia CPP market has had a very quiet slow week with very little to talk about in terms of cargo volume. The position list has lengthened for all three sizes, Owner sentiment has been chipped away as a result. South Korea/Singapore for the MR sizes has not really been tested this week, but Nakhodka/Singapore is reported on subjects at the time of writing at $520K which, taking the mostly accepted $50-70K differential for Korea vs. Russia loading, would put South Korea/Singapore at best $470K today another $50K drop on last week s levels. LR1s LR2s have also been deadly quiet Owners will hope the fact that the AG market is picking up again can stop the rot on the backhaul. LR1s should fix at about $520K Korea/Singapore but are untested, for LR2s, last done levels were at $625K but again the route is untested next done could well be below these levels. The Singapore market has stayed firmer this week with a good amount of activity; most Owners will still prefer to fix long-haul cargoes (especially in the lead up to Christmas) so these routes have stayed steadier at 30kt x ws 180 levels or a shade below for Singapore/Australia. Short-haul routes have been more volatile X- Singapore should be back to above $150K again now. Next week is expected to be quieter though, we will probably see rates come off as a result. Mediterranean Another whopper of a week in the Mediterranean. Monday trading was fixing around 30 x ws 215, but on account of tight tonnage a glut of cargoes rates have jumped upwards the market closes 30 x ws 230+ with 30 x ws rumoured on subjects. MR rates have been softening from the UKC, but the Med market has held up better with less tonnage availability, so consider it 37 x ws 195 for Med Transatlantic 37 x ws West Africa. Heading East to the Red Sea is around the $ million level but date Owner sensitive. UK Continent A quiet start to the week saw TC2 slip slightly with rates falling to 37 x ws185. However at time of writing a few more cargoes in the market should keep rates buoyed at current levels, with 37 x ws the conference rate depending on Worldscale ECA agreements. Cont/ West Africa followed suit trades at +15 points. Hies X- Continent continue to hover around 30 x ws Flexi's 22 x ws levels. LRs have had a quieter week giving the tonnage list an opportunity to build. LR1s remain tight although a number of ballast positions between December may put downward pressure on rates, although expect more cargoes before month is out. LR2s are extremely tight until the New Year. Caribbean USG market is trending sideways this week, hovering around the 38 x ws 145 levels for TC14. Enough enquiry in the market to keep rates firm prevent them from falling, with tonnage steadily being tucked away. Caribs up to the USAC now at around 37 x ws 160 levels. LRs ex USG have also quietened off from their busy spell, with the fixing window now in the first half of January.

5

6 DIRTY PRODUCTS Hy With six days until Christmas we have witnessed slight panic in the market where Charterers are keen to shift their remaining cargo before the t end off the year Owners are keen to capitalise on thiss but also cover their fleet during the quiet holiday period. As a consequence we have seen points surge fixing dates leap into the New Year. With both markets feeding Owners with plenty of business, tonnage has naturally tightened, however the risk of forward fixing falls on both parties laps as firm itineraries are key. Well placed tonnage is ultimately in control of this firm market that said, a lot of stems have been covered already next weekk will depend on vessels schedules. Panamax Some gentle progression p on rates from f an Owner side has managed to be achieved in the Continent, albeit with some help from some last minute 2014 fixing. This being said, as we enter week 52 with a quiet week passing inn the Mediterranean Caribbean, tonnage willl start to build any opportunity to find some employment to cover the Christmas period will bee actively sought. Expect some last minute non-market rates to appear or just simply vessels falling off tonnage lists as Charterers clip vessels away under the radar. MR A slow week for the MRs has passed, with some Owners expecting the pre-christmas rush to have appeared. Unfortunately this is yet to be seen, with only a few days left of opportunity, perhapss we won t. The Continent has seen some consistent gently inquiry, market conditions remain flat. In the Mediterranean some vessels have ignoredd the tempting 30kt stems in hope of finding the illusivee full cargo, as we sit heree on Friday,, any remaining tonnage may start to be concerned; with the hope of the first half of week 52 to see a final flurry.

TD3 VLCC AG-Japan +12,500 96,500 84,000 38,000 51,500 TD20 Suezmax WAF-UKC +11,750 47,750 36,000 78,250 44,000 TD7")

7 Dirty Tanker Spot Market Developments - Spot Worldscale TD3 VLCC AG-Japan TD20 Suezmax WAF-UKC TD7 Aframax N.Sea-UKC Dirty Tanker Spot Market Developments - $/day tce (a) TD3 VLCC AG-Japan +12,500 96,500 84,000 38,000 51,500 TD20 Suezmax WAF-UKC +11,750 47,750 36,000 78,250 44,000 TD7 Aframax N.Sea-UKC +13,500 44,250 30,750 45,500 36,750 Clean Tanker Spot Market Developments - Spot Worldscale TC1 LR2 AG-Japan TC2 MR - west UKC-USAC TC5 LR1 AG-Japan TC7 MR - east Singapore-EC Aus Clean Tanker Spot Market Developments - $/day tce (a) TC1 LR2 AG-Japan +1,750 28,500 26,750 28,500 TC2 MR - west UKC-USAC -3,250 31,250 34,500 21,750 19,500 TC5 LR1 AG-Japan +4,000 25,250 21,250 20,250 21,500 TC7 MR - east Singapore-EC Aus +1,500 22,000 20,500 18,750 (a) based on round voyage economics at 'market' speed LQM Bunker Price (Rotterdam HSFO 380) LQM Bunker Price (Fujairah 380 HSFO) LQM Bunker Price (Singapore 380 HSFO) RM/JH/JD/DP/SLK Produced by Gibson Consultancy Research Visit Gibson s website at for latest market information E.A. GIBSON SHIPBROKERS LTD., AUDREY HOUSE, ELY PLACE, LONDON EC1P 1HP Switchboard Telephone: (UK) (International) tanker@eagibson.co.uktelex: GTKR G FACSIMILE No: BIMCOM This report has been produced for general information is not a replacement for specific advice. While the market information is believed to be reasonably accurate, it is by its nature subject to limited audits validations. No responsibility can be accepted for any errors or any consequences arising therefrom. No part of the report may be reproduced or circulated without our prior written approval. E.A. Gibson Shipbrokers Ltd 2014.

2013 SUPPLY SLOWDOWN, BEFORE SHOWDOWN

WEEKL LY TANKER REPORT SUPPLY SLOWDOWN, BEFORE SHOWDOWN 18 th January 2013 The total number of tankers thatt entered market in 2012 was w significantly less than in 2011, and this year total deliveries

WEEKL LY TANKER REPORT SUPPLY SLOWDOWN, BEFORE SHOWDOWN 18 th January 2013 The total number of tankers thatt entered market in 2012 was w significantly less than in 2011, and this year total deliveries

The Year of Extremes. Weekly Tanker Market Report. Week st December 2018

Week 51 21 st December 2018 The Year of Extremes Weekly Tanker Market Report 2018 has been a year of extremes. For most part, trading conditions have been very challenging amid a persistent oversupply

Week 51 21 st December 2018 The Year of Extremes Weekly Tanker Market Report 2018 has been a year of extremes. For most part, trading conditions have been very challenging amid a persistent oversupply

the problem has not gone that Iran managing to to exporting cargoes.

IRAN BUCK$ THE TREND! 16 th November 2012 While Iran has lost its prominence from front pages of our daily newspapers, problem has not gone away. In September, Iranian crude production was reported to

IRAN BUCK$ THE TREND! 16 th November 2012 While Iran has lost its prominence from front pages of our daily newspapers, problem has not gone away. In September, Iranian crude production was reported to

2 nd May new VLCC. date. As. moree. for VLCCC. when. most of the. to crude. for the currently. The to around 2% accelerate earnings.

TANKER ORDERS BACK INTO THE SPOTLIGHT 2 nd May 2014 Last year tanker industry witnessed a surge in new tonnage investment. Despite tanker returns remaining for most of 2013 at depressed levels, orderingg

TANKER ORDERS BACK INTO THE SPOTLIGHT 2 nd May 2014 Last year tanker industry witnessed a surge in new tonnage investment. Despite tanker returns remaining for most of 2013 at depressed levels, orderingg

for the rest of tonnage dominating

TD3 CHRISTMAS COMES EARLY? 23 rd November 2012 At last we have some excitement in a crude tanker segment. VLCCs have burst into life in last 10 days, offering some much needed respite for ir owners. With

TD3 CHRISTMAS COMES EARLY? 23 rd November 2012 At last we have some excitement in a crude tanker segment. VLCCs have burst into life in last 10 days, offering some much needed respite for ir owners. With

March st. earnings of. be in the West Africa. much too. is, of the fleet. let s look

SUEZMAX STACKED AGAINSTT THE ODDS Even best spin doctors would struggle to create some positivity into earnings of currently beleaguered crude tanker market. The Suezmax sector in particular has suffered

SUEZMAX STACKED AGAINSTT THE ODDS Even best spin doctors would struggle to create some positivity into earnings of currently beleaguered crude tanker market. The Suezmax sector in particular has suffered

d to commence imports for 2014.

MIXED SIGNALS FROM ASIA? 21st February 2014 The dramatic changes in US crude oil production through development of shale oil industry have already had a significant impact on VLCC market in terms of dem.

MIXED SIGNALS FROM ASIA? 21st February 2014 The dramatic changes in US crude oil production through development of shale oil industry have already had a significant impact on VLCC market in terms of dem.

Just Scraps Again For Tankers Weekly Tanker Market Report

Week 1 6 th 2017 2016 - Just Scraps Again For Tankers Weekly Tanker Market Report Without the sale of two VLCCs in the final quarter of last year, tanker deadweight recycling totals would have been only

Week 1 6 th 2017 2016 - Just Scraps Again For Tankers Weekly Tanker Market Report Without the sale of two VLCCs in the final quarter of last year, tanker deadweight recycling totals would have been only

Consolidation Club Weekly Tanker Market Report

Week 6 9 th February 2018 Consolidation Club Weekly Tanker Market Report Just before Christmas last year, the tanker market was greeted with the announcement of the proposed merger between two NYSE quoted

Week 6 9 th February 2018 Consolidation Club Weekly Tanker Market Report Just before Christmas last year, the tanker market was greeted with the announcement of the proposed merger between two NYSE quoted

Slip N Slide Weekly Tanker Market Report

Week 2 13 th Jan 2017 Slip N Slide Weekly Tanker Market Report Newbuilding delays are a common in shipping. Slippage can often be prompted by the owner who wants to delay the entry into a weak market,

Week 2 13 th Jan 2017 Slip N Slide Weekly Tanker Market Report Newbuilding delays are a common in shipping. Slippage can often be prompted by the owner who wants to delay the entry into a weak market,

SAVIOUR? Oil news has and faltering. government. Its. country s only. the. Security also. pipeline, used

IRAQ TANKERS SAVIOUR? 2 nd November 2012 Oil news has been dominated recently by the US and European Union oill embargo against Iran. With the tanker market already suffering from the effects of tonnage

IRAQ TANKERS SAVIOUR? 2 nd November 2012 Oil news has been dominated recently by the US and European Union oill embargo against Iran. With the tanker market already suffering from the effects of tonnage

A Gulf in Class? Weekly Tanker Market Report

2020 2019 Week 2 11 th January 2019 A Gulf in Class? Weekly Tanker Market Report It is fair to say the US crude exports have transformed the global oil markets since the crude export ban was lifted by

2020 2019 Week 2 11 th January 2019 A Gulf in Class? Weekly Tanker Market Report It is fair to say the US crude exports have transformed the global oil markets since the crude export ban was lifted by

VLCC Maths Weekly Tanker Market Report

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Latest Week 38 21 st September 2018 VLCC Maths Weekly Tanker Market Report

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Latest Week 38 21 st September 2018 VLCC Maths Weekly Tanker Market Report

Rhine Logjam Weekly Tanker Market Report

Week 47 23 rd November 2018 Rhine Logjam Weekly Tanker Market Report Low water levels on the Rhine have remained a persistent problem for the European commodity markets since the summer, forcing many refineries

Week 47 23 rd November 2018 Rhine Logjam Weekly Tanker Market Report Low water levels on the Rhine have remained a persistent problem for the European commodity markets since the summer, forcing many refineries

Déjà Vu Weekly Tanker Market Report

Week 17 27 th April 2018 Déjà Vu Weekly Tanker Market Report The acceleration in VLCC demolition activity this year has frequently been in the headlines of late. As more tankers head to the beaches, this

Week 17 27 th April 2018 Déjà Vu Weekly Tanker Market Report The acceleration in VLCC demolition activity this year has frequently been in the headlines of late. As more tankers head to the beaches, this

Ice Class Frozen Out! Weekly Tanker Market Report

Week 9 2 nd March 2018 Ice Class Frozen Out! Weekly Tanker Market Report This week, much of Europe has been blanketed in snow as cold weather has spread as far south as the Mediterranean coast. With temperatures

Week 9 2 nd March 2018 Ice Class Frozen Out! Weekly Tanker Market Report This week, much of Europe has been blanketed in snow as cold weather has spread as far south as the Mediterranean coast. With temperatures

Asian Products Push Weekly Tanker Market Report

Week 46 17th Nov 2017 Asian Products Push Weekly Tanker Market Report Product tankers trading in the Far East are having a better second half of 2017 relative to the first half, and on average, have outperformed

Week 46 17th Nov 2017 Asian Products Push Weekly Tanker Market Report Product tankers trading in the Far East are having a better second half of 2017 relative to the first half, and on average, have outperformed

Dry Bulk Market Weekly Highlights Week 17 - Dry Cargo Market Highlights for the period of 21-April-2011 until 28-April-2011

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Tanker Market Outlook. 12th Mare Forum Ship Finance 2012 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 2012

Tanker Market Outlook 12th Mare Forum Ship Finance 212 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 212 Tanker Market Outlook 12th Mare Forum Ship Finance 212 Disclaimer The material and

Tanker Market Outlook 12th Mare Forum Ship Finance 212 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 212 Tanker Market Outlook 12th Mare Forum Ship Finance 212 Disclaimer The material and

Ship Scrapping - Market Pressures. IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 2012

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Demand, Supply & Capacity in the Shipbuilding Industry

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

Quarterly Aviation Industry Performance

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance (March - June 17) Prepared by: Strategic Planning department 1 Quarterly

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance (March - June 17) Prepared by: Strategic Planning department 1 Quarterly

LPG & Petrochemical Shipping: Current Status & Outlook. A better market, but for how long? Nicola Williams, Clarksons March 16th 2005

LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams, Clarksons March 16th 2005 The LPG Shipping Market today The LPG freight market started to move

LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams, Clarksons March 16th 2005 The LPG Shipping Market today The LPG freight market started to move

Who is the Biggest of the Clean?

Who is the Biggest of the Clean? In our January 9, 24 opinion report, The More Things Change The More They Stay the Same, we tracked the top charterers in the spot market for dirty cargoes. But the dirty

Who is the Biggest of the Clean? In our January 9, 24 opinion report, The More Things Change The More They Stay the Same, we tracked the top charterers in the spot market for dirty cargoes. But the dirty

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 2 January 211 Braemar Seascope ket Indicator Wet 19-Jan-11 Avg Avg YTD 21 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a

Weekly Chartering Report Thursday, 2 January 211 Braemar Seascope ket Indicator Wet 19-Jan-11 Avg Avg YTD 21 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a

Weekly Dry Bulk Report

22 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: A more active market throughout the week Panamax: Front haul market saw slightly more activity, not enough

22 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: A more active market throughout the week Panamax: Front haul market saw slightly more activity, not enough

Petrofin Research Greek fleet statistics

Petrofin Research 2 nd part of Petrofin Research : Greek fleet statistics In this 2 nd part of Petrofin research, the Greek Fleet Statistics, we analyse the composition of the Greek fleet, in terms of

Petrofin Research 2 nd part of Petrofin Research : Greek fleet statistics In this 2 nd part of Petrofin research, the Greek Fleet Statistics, we analyse the composition of the Greek fleet, in terms of

Quarterly Aviation Industry Performance

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance 3Q17 (Updated November 17) Prepared by: Strategic Planning department

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance 3Q17 (Updated November 17) Prepared by: Strategic Planning department

Weekly Dry Bulk Report

Week 36 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 3th 214 HIGHLIGHTS Capesize: Generally lower rates this week Supramax/Handymax: Continued improved market for both segments

Week 36 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 3th 214 HIGHLIGHTS Capesize: Generally lower rates this week Supramax/Handymax: Continued improved market for both segments

PREMIUM TRAFFIC MONITOR JULY 2014 KEY POINTS

PREMIUM TRAFFIC MONITOR JULY 2014 KEY POINTS Growth in international air passengers was weak for a second consecutive month with a 2.6% increase in July compared to a year ago premium seat numbers rose

PREMIUM TRAFFIC MONITOR JULY 2014 KEY POINTS Growth in international air passengers was weak for a second consecutive month with a 2.6% increase in July compared to a year ago premium seat numbers rose

Braemar Seascope. Market Indicator

Weekly Chartering Report Thursday, 5 January 212 Braemar Seascope ket Indicator Wet 4-Jan-12 Avg Avg YTD 211 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a

Weekly Chartering Report Thursday, 5 January 212 Braemar Seascope ket Indicator Wet 4-Jan-12 Avg Avg YTD 211 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a

IATA ECONOMICS BRIEFING AIRLINE BUSINESS CONFIDENCE INDEX OCTOBER 2010 SURVEY

IATA ECONOMICS BRIEFING AIRLINE BUSINESS CONFIDENCE INDEX OCTOBER SURVEY KEY POINTS Results from IATA s quarterly survey conducted in October show business conditions continued to improve during the third

IATA ECONOMICS BRIEFING AIRLINE BUSINESS CONFIDENCE INDEX OCTOBER SURVEY KEY POINTS Results from IATA s quarterly survey conducted in October show business conditions continued to improve during the third

Weekly Dry Bulk Report

2-215 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 12 1 8 6 4 2 HIGHLIGHTS Capesize: Still quiet market Panamax: Continued slide in rates L&S INDEX OF DRY BULK STOCKS* Index

2-215 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 12 1 8 6 4 2 HIGHLIGHTS Capesize: Still quiet market Panamax: Continued slide in rates L&S INDEX OF DRY BULK STOCKS* Index

Index of business confidence. Monthly FTK (Billions) Aug 2013 vs. Aug 2012 YTD 2013 vs. YTD 2012 Aug 2013 vs. Jul 2013

Aug 2013 vs. Aug 2012 YTD 2013 vs. YTD 2012 Aug 2013 vs. Jul 2013") AIR PASSENGER MARKET ANALYSIS AUGUST 2013 KEY POINTS Air travel markets expanded strongly in August. Global revenue passenger kilometers were up 6.8% compared to a year ago, an improvement on July growth

AIR PASSENGER MARKET ANALYSIS AUGUST 2013 KEY POINTS Air travel markets expanded strongly in August. Global revenue passenger kilometers were up 6.8% compared to a year ago, an improvement on July growth

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 3 ch 211 Braemar Seascope ket Indicator Wet 2--11 Avg Avg YTD 21 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26, NHC

Weekly Chartering Report Thursday, 3 ch 211 Braemar Seascope ket Indicator Wet 2--11 Avg Avg YTD 21 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26, NHC

AIR PASSENGER MARKET ANALYSIS DECEMBER 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS DECEMBER 2015 KEY POINTS Global air passenger traffic grew by 6.5% in 2015 as a whole the fastest pace since the post-gfc rebound in 2010 and well above the 10-year average

AIR PASSENGER MARKET ANALYSIS DECEMBER 2015 KEY POINTS Global air passenger traffic grew by 6.5% in 2015 as a whole the fastest pace since the post-gfc rebound in 2010 and well above the 10-year average

Weekly Dry Bulk Report

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

AIR TRANSPORT MARKET ANALYSIS MAY 2011

AIR TRANSPORT MARKET ANALYSIS MAY 2011 KEY POINTS May saw a renewed expansion in both air travel and freight, after a soft patch during the previous three months. Air travel volumes were 6.8% higher than

AIR TRANSPORT MARKET ANALYSIS MAY 2011 KEY POINTS May saw a renewed expansion in both air travel and freight, after a soft patch during the previous three months. Air travel volumes were 6.8% higher than

Weekly Dry Bulk Report

44 ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Firming rates throughout the week in both basins Panamax: Another week of firming rates in all sectors CAPESIZE During an active Monday, both the

44 ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Firming rates throughout the week in both basins Panamax: Another week of firming rates in all sectors CAPESIZE During an active Monday, both the

AIR PASSENGER MARKET ANALYSIS JULY 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS JULY 2015 KEY POINTS Global air travel rose 8.2% in July compared to a year ago, partly reflecting an upward bias due to the timing of Ramadan. But even after controlling

AIR PASSENGER MARKET ANALYSIS JULY 2015 KEY POINTS Global air travel rose 8.2% in July compared to a year ago, partly reflecting an upward bias due to the timing of Ramadan. But even after controlling

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 27 tember 212 Braemar Seascope ket Indicator Wet* 26--12 Avg Avg YTD 211 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y

Weekly Chartering Report Thursday, 27 tember 212 Braemar Seascope ket Indicator Wet* 26--12 Avg Avg YTD 211 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y

AIR PASSENGER MARKET ANALYSIS MARCH 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS MARCH 2015 KEY POINTS Global air travel rose by a strong 7.4% in March compared to a year ago, an improvement on the February result of 6.4%. The acceleration in the year-on-year

AIR PASSENGER MARKET ANALYSIS MARCH 2015 KEY POINTS Global air travel rose by a strong 7.4% in March compared to a year ago, an improvement on the February result of 6.4%. The acceleration in the year-on-year

TANKER MARKET CAN A MIRACLE HAPPEN?

TEN Ltd THE TANKER MARKET CAN A MIRACLE HAPPEN? Nikolas P. Tsakos President & CEO, TEN November 19 th, 2008 1 Tanker Freight Rates Remain Healthy Charterer discrimination against single hull tonnage on

TEN Ltd THE TANKER MARKET CAN A MIRACLE HAPPEN? Nikolas P. Tsakos President & CEO, TEN November 19 th, 2008 1 Tanker Freight Rates Remain Healthy Charterer discrimination against single hull tonnage on

AIR PASSENGER MARKET ANALYSIS JUNE 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS JUNE 2015 KEY POINTS Global air travel rose 5.7% in June compared to a year ago, a slowdown on the strong May increase of 6.9%. The deceleration is due to slower growth in

AIR PASSENGER MARKET ANALYSIS JUNE 2015 KEY POINTS Global air travel rose 5.7% in June compared to a year ago, a slowdown on the strong May increase of 6.9%. The deceleration is due to slower growth in

Airlines across the world connected a record number of cities this year, with more than 20,000 city pair connections*

1 Airlines across the world connected a record number of cities this year, with more than 20,000 city pair connections*. This is a 1,351 increase over 2016 and a doubling of service since 1996, when there

1 Airlines across the world connected a record number of cities this year, with more than 20,000 city pair connections*. This is a 1,351 increase over 2016 and a doubling of service since 1996, when there

Index of business confidence. Monthly FTK (Billions) Sep 2013 vs. Sep 2012 YTD 2013 vs. YTD 2012 Sep 2013 vs. Aug 2013

Sep 2013 vs. Sep 2012 YTD 2013 vs. YTD 2012 Sep 2013 vs. Aug 2013") AIR PASSENGER MARKET ANALYSIS SEPTEMBER 2013 KEY POINTS Air travel markets expanded at a solid rate in September. Global revenue passenger kilometers were up 5.5% compared to a year ago. This is a slight

AIR PASSENGER MARKET ANALYSIS SEPTEMBER 2013 KEY POINTS Air travel markets expanded at a solid rate in September. Global revenue passenger kilometers were up 5.5% compared to a year ago. This is a slight

The World s Largest Buyer of Ships and Offshore Assets

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

Long Term Trends in Shipbuilding HVB Press Conference. 20 th September 2006 Stephen Gordon, Clarkson Research

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

WEEK 22 1 June 2018 ISSUE

WEEK 22 1 June 218 ISSUE 22 218 Spot Mar ket WS/LS TCE WS/LS TCE VLCC (13. Kts L/B) -May 1-June AG>USG 28k 18. -- 18. -- AG>SPORE 27k 47.5 $13,777 48. $13,773 AG>JPN 265k 44. $13,567 46. $15,83 AG>CHINA

WEEK 22 1 June 218 ISSUE 22 218 Spot Mar ket WS/LS TCE WS/LS TCE VLCC (13. Kts L/B) -May 1-June AG>USG 28k 18. -- 18. -- AG>SPORE 27k 47.5 $13,777 48. $13,773 AG>JPN 265k 44. $13,567 46. $15,83 AG>CHINA

AIR PASSENGER MARKET ANALYSIS

Monthly RPK (Billions) Monthly FTK (Billions) Index of business confidence % change over year AIR PASSENGER MARKET ANALYSIS APRIL 2013 KEY POINTS Global revenue passenger kilometers were up 3.2% in April

Monthly RPK (Billions) Monthly FTK (Billions) Index of business confidence % change over year AIR PASSENGER MARKET ANALYSIS APRIL 2013 KEY POINTS Global revenue passenger kilometers were up 3.2% in April

AIR PASSENGER MARKET ANALYSIS

Monthly RPK (Billions) Monthly FTK (Billions) Index of business confidence % change over year AIR PASSENGER MARKET ANALYSIS NOVEMBER 2013 KEY POINTS Air travel markets increased at a solid rate in November,

Monthly RPK (Billions) Monthly FTK (Billions) Index of business confidence % change over year AIR PASSENGER MARKET ANALYSIS NOVEMBER 2013 KEY POINTS Air travel markets increased at a solid rate in November,

Worldwide Fleet Forecast

Worldwide Fleet Forecast Presented to: Montreal June 6, 26 DAVID BECKERMAN Director, Consulting Services Agenda State of the Industry Worldwide Fleet Regional Jets Narrowbody Jets Large Widebody Jets Freighter

Worldwide Fleet Forecast Presented to: Montreal June 6, 26 DAVID BECKERMAN Director, Consulting Services Agenda State of the Industry Worldwide Fleet Regional Jets Narrowbody Jets Large Widebody Jets Freighter

GULF MARITIME SHIPBROKERS & CONSULTANTS K U W A I T beyond shipbrokers

GULF MARITIME SHIPBROKERS & CONSULTANTS K U W A I T beyond shipbrokers First Licensed Shipbroker in Kuwait 13 May 212 Dry Cargo Weekly Market Report Department Phone email General Info +965 2259 8822 general@gulf-maritime.com

GULF MARITIME SHIPBROKERS & CONSULTANTS K U W A I T beyond shipbrokers First Licensed Shipbroker in Kuwait 13 May 212 Dry Cargo Weekly Market Report Department Phone email General Info +965 2259 8822 general@gulf-maritime.com

Weekly Dry Bulk Report

5 ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Few shipments into China Panamax: Rates still declining L&S INDEX OF DRY BULK STOCKS* Index 214 Index 215 CAPESIZE PANAMAX Rates

5 ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Few shipments into China Panamax: Rates still declining L&S INDEX OF DRY BULK STOCKS* Index 214 Index 215 CAPESIZE PANAMAX Rates

AIR PASSENGER MARKET ANALYSIS SEPTEMBER 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS SEPTEMBER 2015 KEY POINTS Global air travel rose 7.3% in September compared to a year ago. The mid-year data showed some distortion from holiday impacts, but the last couple

AIR PASSENGER MARKET ANALYSIS SEPTEMBER 2015 KEY POINTS Global air travel rose 7.3% in September compared to a year ago. The mid-year data showed some distortion from holiday impacts, but the last couple

PREMIUM TRAFFIC MONITOR MARCH 2009

PREMIUM TRAFFIC MONITOR MARCH 2009 KEY POINTS The fall in passenger numbers slowed in March, to a decline of 9.3% following February s 9.6% fall. However, this slowdown was entirely due to February s fall

PREMIUM TRAFFIC MONITOR MARCH 2009 KEY POINTS The fall in passenger numbers slowed in March, to a decline of 9.3% following February s 9.6% fall. However, this slowdown was entirely due to February s fall

NBAA 2015 MARKET UPDATE

NBAA 2015 MARKET UPDATE November 2015 Forward-Looking Statements 2 This report contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. All statements,

NBAA 2015 MARKET UPDATE November 2015 Forward-Looking Statements 2 This report contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. All statements,

2015 RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF 2015 PETROFIN RESEARCH CONTENTS OF PETROFIN RESEARCH PART 2

based on data as of September RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF CONTENTS OF PART 2 RESULTS AT A GLANCE (P. 2) SECTION A: VITAL STATISTICS OF THE ENTIRE GREEK FLEET (P. 3) SECTION

based on data as of September RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF CONTENTS OF PART 2 RESULTS AT A GLANCE (P. 2) SECTION A: VITAL STATISTICS OF THE ENTIRE GREEK FLEET (P. 3) SECTION

Weekly Dry Bulk Report

9 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Boost in fixtures for C5 towards the weekend Panamax: Pacific activity slowly increasing

9 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Boost in fixtures for C5 towards the weekend Panamax: Pacific activity slowly increasing

AIR TRANSPORT MARKET ANALYSIS APRIL 2011

AIR TRANSPORT MARKET ANALYSIS APRIL 2011 KEY POINTS From this month we provide an assessment of global scheduled air transport markets, adding domestic to international, and including both IATA and non-iata

AIR TRANSPORT MARKET ANALYSIS APRIL 2011 KEY POINTS From this month we provide an assessment of global scheduled air transport markets, adding domestic to international, and including both IATA and non-iata

Update on the Constantly Changing Shipbuilding Market

. Update on the Constantly Changing Shipbuilding Market Martin Stopford, MD Clarkson Research LSE Ship Finance Conference 14 th Nov 2 Martin Stopford, H. Clarkson, Research & Publications Division 12th

. Update on the Constantly Changing Shipbuilding Market Martin Stopford, MD Clarkson Research LSE Ship Finance Conference 14 th Nov 2 Martin Stopford, H. Clarkson, Research & Publications Division 12th

WHEN IS THE NEXT SHIPPING BOOM?

WHEN IS THE NEXT SHIPPING BOOM? By Ravi K Mehrotra CBE Executive Chairman Foresight Group, London Samunder Club April & May 2012 Houston and Florida, USA 1 WHEN IS THE NEXT SHIPPING BOOM? I am not a fortune

WHEN IS THE NEXT SHIPPING BOOM? By Ravi K Mehrotra CBE Executive Chairman Foresight Group, London Samunder Club April & May 2012 Houston and Florida, USA 1 WHEN IS THE NEXT SHIPPING BOOM? I am not a fortune

NBAA 2014 Business Aviation Market Update. October 2014

NBAA 2014 Business Aviation Market Update October 2014 1 Jefferies Global Industrials Conference - August 14, 2014 Forward Looking Statements This report contains forward-looking statements within the

NBAA 2014 Business Aviation Market Update October 2014 1 Jefferies Global Industrials Conference - August 14, 2014 Forward Looking Statements This report contains forward-looking statements within the

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

AIR PASSENGER MARKET ANALYSIS JANUARY 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS JANUARY 2015 KEY POINTS Global air travel was up 4.6% in January compared to a year ago, a slower start to the year when compared to the strong 5.8% expansion in 2014 overall.

AIR PASSENGER MARKET ANALYSIS JANUARY 2015 KEY POINTS Global air travel was up 4.6% in January compared to a year ago, a slower start to the year when compared to the strong 5.8% expansion in 2014 overall.

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 7 ch 213 Braemar Seascope ket Indicator Wet* 6--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26,

Weekly Chartering Report Thursday, 7 ch 213 Braemar Seascope ket Indicator Wet* 6--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26,

Ship Recycling: The last pillar of shipping. February 22, nd Annual Capital Link Greek Shipping Forum 1

Ship Recycling: The last pillar of shipping February 22, 2011 2 nd Annual Capital Link Greek Shipping Forum 1 Where do old ships go? Indian subcontinent India, Bangladesh and Pakistan China Turkey February

Ship Recycling: The last pillar of shipping February 22, 2011 2 nd Annual Capital Link Greek Shipping Forum 1 Where do old ships go? Indian subcontinent India, Bangladesh and Pakistan China Turkey February

PREMIUM TRAFFIC MONITOR APRIL 2015 KEY POINTS

PREMIUM TRAFFIC MONITOR APRIL 2015 KEY POINTS Passenger travel on international markets rose 3.8% in April compared to a year ago, slower than the 4.6% result in March. The growth trend for international

PREMIUM TRAFFIC MONITOR APRIL 2015 KEY POINTS Passenger travel on international markets rose 3.8% in April compared to a year ago, slower than the 4.6% result in March. The growth trend for international

Weekly Dry Bulk Report

49 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 95 85 75 65 55 45 35 HIGHLIGHTS Capesize: BCI down 31% w-o-w Panamax: Slightly firming BPI L&S INDEX OF DRY BULK STOCKS*

49 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 95 85 75 65 55 45 35 HIGHLIGHTS Capesize: BCI down 31% w-o-w Panamax: Slightly firming BPI L&S INDEX OF DRY BULK STOCKS*

Index of business confidence. Monthly FTK (Billions) June 2012 vs. June 2011 YTD 2012 vs. YTD 2011 RPK ASK PLF FTK AFTK FLF RPK ASK PLF FTK AFTK FLF

June 2012 vs. June 2011 YTD 2012 vs. YTD 2011 RPK ASK PLF FTK AFTK FLF RPK ASK PLF FTK AFTK FLF") Monthly RPK (Billions) Monthly FTK (Billions) Index of business confidence % change over year AIR TRANSPORT MARKET ANALYSIS JUNE 2012 KEY POINTS Air travel markets expanded in June, but the trend in passenger

Monthly RPK (Billions) Monthly FTK (Billions) Index of business confidence % change over year AIR TRANSPORT MARKET ANALYSIS JUNE 2012 KEY POINTS Air travel markets expanded in June, but the trend in passenger

Weekly Dry Bulk Report

12 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Relatively flat in the Pacific Front haul, reasonably quiet Panamax: Firming rates for tonnage fixing

12 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Relatively flat in the Pacific Front haul, reasonably quiet Panamax: Firming rates for tonnage fixing

AIR PASSENGER MARKET ANALYSIS

AIR PASSENGER MARKET ANALYSIS OCTOBER 2014 KEY POINTS Air travel volumes were up 5.7% in October year-on-year, slightly stronger than the September rise of 5.2%, and a continuation of the positive growth

AIR PASSENGER MARKET ANALYSIS OCTOBER 2014 KEY POINTS Air travel volumes were up 5.7% in October year-on-year, slightly stronger than the September rise of 5.2%, and a continuation of the positive growth

IATA ECONOMIC BRIEFING DECEMBER 2008

ECONOMIC BRIEFING DECEMBER 28 THE IMPACT OF RECESSION ON AIR TRAFFIC VOLUMES Recession is now forecast for North America, Europe and Japan late this year and into 29. The last major downturn in air traffic,

ECONOMIC BRIEFING DECEMBER 28 THE IMPACT OF RECESSION ON AIR TRAFFIC VOLUMES Recession is now forecast for North America, Europe and Japan late this year and into 29. The last major downturn in air traffic,

AIR PASSENGER MARKET ANALYSIS MAY 2015 KEY POINTS

AIR PASSENGER MARKET ANALYSIS MAY 2015 KEY POINTS Global air travel rose by a strong 6.9% in May compared to a year ago. This was an acceleration on April year-overyear growth of 5.7%. Air travel was strong

AIR PASSENGER MARKET ANALYSIS MAY 2015 KEY POINTS Global air travel rose by a strong 6.9% in May compared to a year ago. This was an acceleration on April year-overyear growth of 5.7%. Air travel was strong

SLOW STEAMING A transientt fashion or here to stay?

SLOW STEAMING A transientt fashion or here to stay? Modern box vessels cruising slower than ships in the era of sail... Dynamar B.V. Noorderkade 1G 1823 CJ ALKMAAR The Netherlands Phone: +31 725147400

SLOW STEAMING A transientt fashion or here to stay? Modern box vessels cruising slower than ships in the era of sail... Dynamar B.V. Noorderkade 1G 1823 CJ ALKMAAR The Netherlands Phone: +31 725147400

Index of business confidence. Monthly FTK (Billions) May 2014 vs. May 2013 YTD 2014 vs. YTD 2013 May 2014 vs. Apr 2014

May 2014 vs. May 2013 YTD 2014 vs. YTD 2013 May 2014 vs. Apr 2014") AIR PASSENGER MARKET ANALYSIS MAY 2014 KEY POINTS Air travel markets rose by a strong 6.2% in May compared to a year ago. Although this is slightly down on April growth of 7.6%, April was positively biased

AIR PASSENGER MARKET ANALYSIS MAY 2014 KEY POINTS Air travel markets rose by a strong 6.2% in May compared to a year ago. Although this is slightly down on April growth of 7.6%, April was positively biased

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

IATA ECONOMIC BRIEFING FEBRUARY 2007

IATA ECONOMIC BRIEFING FEBRUARY 27 NEW AIRCRAFT ORDERS KEY POINTS New aircraft orders remained very high in 26. The total of 1,834 new orders for Boeing and Airbus commercial planes was down slightly from

IATA ECONOMIC BRIEFING FEBRUARY 27 NEW AIRCRAFT ORDERS KEY POINTS New aircraft orders remained very high in 26. The total of 1,834 new orders for Boeing and Airbus commercial planes was down slightly from

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

Greek Shipping : Greece s steaming force

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

EASYJET INTERIM MANAGEMENT STATEMENT FOR THE QUARTER ENDED 30 JUNE 2011

22 July 2011 easyjet Interim Management Statement Page 1 of 5 22 July 2011 EASYJET INTERIM MANAGEMENT STATEMENT FOR THE QUARTER ENDED 30 JUNE 2011 Highlights (figures below are for the quarter ended 30

22 July 2011 easyjet Interim Management Statement Page 1 of 5 22 July 2011 EASYJET INTERIM MANAGEMENT STATEMENT FOR THE QUARTER ENDED 30 JUNE 2011 Highlights (figures below are for the quarter ended 30

Air transport demand shows continued resilience despite geopolitical pressure as passenger and freight traffic grow

Air transport demand shows continued resilience despite geopolitical pressure as passenger and freight traffic grow Montreal, 7 August 2018 Airports Council International (ACI) World reported global passenger

Air transport demand shows continued resilience despite geopolitical pressure as passenger and freight traffic grow Montreal, 7 August 2018 Airports Council International (ACI) World reported global passenger

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 2 e 213 Braemar Seascope ket Indicator Wet* 19--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26,

Weekly Chartering Report Thursday, 2 e 213 Braemar Seascope ket Indicator Wet* 19--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26,

PREMIUM TRAFFIC MONITOR DECEMBER 2014 KEY POINTS

PREMIUM TRAFFIC MONITOR DECEMBER 2014 KEY POINTS International air travel recorded another moderate rise to end 2014, up 3.6% in December compared to a year ago. The annual expansion was in line with the

PREMIUM TRAFFIC MONITOR DECEMBER 2014 KEY POINTS International air travel recorded another moderate rise to end 2014, up 3.6% in December compared to a year ago. The annual expansion was in line with the

PREMIUM TRAFFIC MONITOR FEBRUARY 2015 KEY POINTS

PREMIUM TRAFFIC MONITOR FEBRUARY 2015 KEY POINTS Passenger travel on international markets rose 4.6% in February compared to a year ago, up on the 3.7% result in January; Economy class travel drove the

PREMIUM TRAFFIC MONITOR FEBRUARY 2015 KEY POINTS Passenger travel on international markets rose 4.6% in February compared to a year ago, up on the 3.7% result in January; Economy class travel drove the

SHIP POWER YOUR SHORTER ROUTE TO BIGGER PROFITS. JAAKKO ESKOLA Group Vice President, Ship Power

SHIP POWER YOUR SHORTER ROUTE TO BIGGER PROFITS Group Vice President, Ship Power 1 Wärtsilä 29 March 2012 Shipping has a future 90% of world trade is still done by sea NO SUPRISE it doesn t cost a thing

SHIP POWER YOUR SHORTER ROUTE TO BIGGER PROFITS Group Vice President, Ship Power 1 Wärtsilä 29 March 2012 Shipping has a future 90% of world trade is still done by sea NO SUPRISE it doesn t cost a thing

EASYJET INTERIM MANAGEMENT STATEMENT FOR THE QUARTER ENDED 31 DECEMBER 2010

20 January 2011 easyjet Interim Management Statement Page 1 of 5 20 January 2011 EASYJET INTERIM MANAGEMENT STATEMENT FOR THE QUARTER ENDED 31 DECEMBER 2010 Highlights: Total revenue up by 7.5% to 654

20 January 2011 easyjet Interim Management Statement Page 1 of 5 20 January 2011 EASYJET INTERIM MANAGEMENT STATEMENT FOR THE QUARTER ENDED 31 DECEMBER 2010 Highlights: Total revenue up by 7.5% to 654

% change vs. Dec ALL VISITS (000) 2,410 12% 7,550 5% 31,148 1% Spend ( million) 1,490 15% 4,370-1% 18,710 4%

2,410 12% 7,550 5% 31,148 1% Spend ( million) 1,490 15% 4,370-1% 18,710 4%") HEADLINES FULL YEAR 2012 (PROVISIONAL) 1 Overall visits 31.148 million visits making 2012 the best year for inbound tourism since 2008 but not a record. 1% increase in visits on 2011 (30.798 visits) slightly

HEADLINES FULL YEAR 2012 (PROVISIONAL) 1 Overall visits 31.148 million visits making 2012 the best year for inbound tourism since 2008 but not a record. 1% increase in visits on 2011 (30.798 visits) slightly

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 8 ust 213 Braemar Seascope ket Indicator Wet* 7--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26,

Weekly Chartering Report Thursday, 8 ust 213 Braemar Seascope ket Indicator Wet* 7--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26,

PACIFIC ISLAND COUNTRIES

QUARTERLY REVIEW OF TOURIST ARRIVALS IN PACIFIC ISLAND COUNTRIES QUARTER 1 218 March, 218 Report prepared by : Research & Statistics Division Contacts : Jennifer Butukoro (cbutukoro@spto.org) : Elizabeth

QUARTERLY REVIEW OF TOURIST ARRIVALS IN PACIFIC ISLAND COUNTRIES QUARTER 1 218 March, 218 Report prepared by : Research & Statistics Division Contacts : Jennifer Butukoro (cbutukoro@spto.org) : Elizabeth

PREMIUM TRAFFIC MONITOR AUGUST 2015 KEY POINTS

PREMIUM TRAFFIC MONITOR AUGUST 2015 KEY POINTS Passenger travel on international markets was up 5.4% in August year-on-year, reflecting strong growth on the Within Europe travel market. Both travel classes

PREMIUM TRAFFIC MONITOR AUGUST 2015 KEY POINTS Passenger travel on international markets was up 5.4% in August year-on-year, reflecting strong growth on the Within Europe travel market. Both travel classes

IATA ECONOMICS BRIEFING

IATA ECONOMICS BRIEFING NEW AIRCRAFT ORDERS A POSITIVE SIGN BUT WITH SOME RISKS FEBRUARY 26 KEY POINTS 25 saw a record number of new aircraft orders over 2, for Boeing and Airbus together even though the

IATA ECONOMICS BRIEFING NEW AIRCRAFT ORDERS A POSITIVE SIGN BUT WITH SOME RISKS FEBRUARY 26 KEY POINTS 25 saw a record number of new aircraft orders over 2, for Boeing and Airbus together even though the

Management Discussions and Analysis for the three-month period ended 31 March 2014 and Executive Summary

Executive Summary Overview of the global economy during the first quarter of 2015 (Q1/2015) are as following; the US economy has been in recovery mode while rapidly dollar appreciation weighs on net exports

Executive Summary Overview of the global economy during the first quarter of 2015 (Q1/2015) are as following; the US economy has been in recovery mode while rapidly dollar appreciation weighs on net exports

Royal Caribbean Cruises Ltd. Bunker World Conference May 5, 2010

Royal Caribbean Cruises Ltd. Bunker World Conference May 5, 2010 Agenda Cruise Industry Overview Success Factors Growth Opportunities Emissions Control Impact Current Issues Challenging Macro Economic

Royal Caribbean Cruises Ltd. Bunker World Conference May 5, 2010 Agenda Cruise Industry Overview Success Factors Growth Opportunities Emissions Control Impact Current Issues Challenging Macro Economic

Golden Ocean Group Limited Q results March 1, 2007

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Arab Aviation and Media Summit 2012

Arab Aviation and Media Summit 2012 Outcomes and Perspectives June 2012 Executive Summary Since Air Arabia and CNBC Arabia organised the first Arab Aviation and Media Summit in 2011, the aviation sector

Arab Aviation and Media Summit 2012 Outcomes and Perspectives June 2012 Executive Summary Since Air Arabia and CNBC Arabia organised the first Arab Aviation and Media Summit in 2011, the aviation sector

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 15 ust 213 Braemar Seascope ket Indicator Wet* 14--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

Weekly Chartering Report Thursday, 15 ust 213 Braemar Seascope ket Indicator Wet* 14--13 Avg Avg YTD 212 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

8 th City of London Biennial Meeting November 2016 International Maritime Organisation (IMO), London

, London") 8 th City of London Biennial Meeting 17-18 November 2016 International Maritime Organisation (IMO), London Drybulk Shipping in 21 st Century by Hakki Deval (MSc STF 2001) 0 China joins WTO in December

8 th City of London Biennial Meeting 17-18 November 2016 International Maritime Organisation (IMO), London Drybulk Shipping in 21 st Century by Hakki Deval (MSc STF 2001) 0 China joins WTO in December

2012 Result. Mika Vehviläinen CEO

2012 Result Mika Vehviläinen CEO 1 Agenda Market environment in Q4 Business performance and strategy execution Outlook Financials 2 Market Environment According to IATA, Global air travel continues to

2012 Result Mika Vehviläinen CEO 1 Agenda Market environment in Q4 Business performance and strategy execution Outlook Financials 2 Market Environment According to IATA, Global air travel continues to