WHEN IS THE NEXT SHIPPING BOOM?

|

|

|

- Jessica O’Brien’

- 5 years ago

- Views:

Transcription

1 WHEN IS THE NEXT SHIPPING BOOM? By Ravi K Mehrotra CBE Executive Chairman Foresight Group, London Samunder Club April & May 2012 Houston and Florida, USA 1

2 WHEN IS THE NEXT SHIPPING BOOM? I am not a fortune teller as most of the Shipping fraternity think although my group has survived the last 28 years! In reality I am a professional turned entrepreneur hence fortune telling is the last thing on my mind. To succeed in Shipping one has to be a hard-headed person used to 24 x 7 working conditions as Shipping has no time zones and therefore there is no time to indulge in the fantasy of fortune telling. Another trait of a ship owner is that they keep themselves abreast of what is happening around the world also their mental filtering system keeps on working to see if any of the world events will have an effect on shipping for example the Arab Spring of last year. Ship owners love their ships but they develop a keen sense of when to sell and when to buy. Finally, ship owners are good lovers hence generally women find them attractive. This gives them the mental balance to focus on their second love ship owning. 2

3 WHEN IS THE NEXT SHIPPING BOOM? Also Boom is a very harsh and euphoric word, it does not happen by the clap of hands. Many factors are involved and have to work in tandem. Therefore what I can do is to work with you and see where we are now and what factors, if they develop, can have a positive effect on international shipping which can provide basic parameters for a possible shipping boom as we experienced between 2005 and mid Do we agree? So let us begin by seeing what the existing world economy and seaborne trade is and the future projections of growth. Please see slides IV & V:- 3

4 WORLD GDP GROWTH PROJECTIONS Growth Percentage Years ABS Outlook Spring 2011 IV

5 WORLD TRADE VOLUME GROWTH PROJECTIONS Trade Volume Growth Years ABS Outlook Spring 2011 V

6 WHAT DO THESE TWO SLIDES TELL US? We had a financial crisis in the second half of 2008 which stopped Banking Letter of credit facilities and World Trade came suddenly from annual growth of seaborne trade of 7% to -1% in With the relaxation of Banking facilities in 2010, the seaborne trade grew more than 7% albeit from a negative position at the end of 2008 which gave a balanced outlook on Shipping in However what is more significant is that the world shipbuilding activity was unaffected by this financial crisis as most of it is concentrated in Asia and where the banking crisis had least effect so the ship building continued. World ship borne trade came down in 2008 & 2009 but new ships kept on adding in the world fleet. This created an overhang of the world ship fleet and this brought down the ship utilisation rate as well as ship values thus effecting the earnings of ship owners the results of which can be seen around us. Please see slides VII to IX:- 6

7 EXISTING WORLD MERCHANT FLEET SUPPLY, DEMAND & UTILISATION Million Compensated Gross Tonnes Years R.S. Platou, Norway VII

8 EXISTING WORLD DRY BULK FLEET SUPPLY, DEMAND & UTILISATION Million DWT Tonnage Years R.S. Platou, Norway VIII

9 EXISTING WORLD TANKER FLEET SUPPLY, DEMAND & UTILISATION Million DWT Tonnage Years R.S. Platou, Norway IX

10 WHAT DO THE LAST THREE SLIDES TELL US? As we can see from the previous three graphs, the last shipping boom was between 2005 to mid Why? The ship utilisation rate was above 90%. You can never go above 95% as all ships are not available for trade, some ships are going through repairs, surveys etc. So what do these slides teach us? Either we have to increase the world trade to absorb all shipbuilding capacity or alternatively reduce shipbuilding capacity or increase old ship scrapping. Please see slides XI, XII & XIII:- 10

11 FOR THE FUTURE OF SHIPPING EXCESS SUPPLY IS THE CHALLENGE Black bars New deliveries in million GT Red bars Scrapping in million GT ABS Outlook Spring 2011 XI

12 FOR THE FUTURE OF SHIPPING EXCESS SUPPLY IS THE CHALLENGE Million Gross Tons Years ABS Outlook Spring 2011 XII

13 FOR THE FUTURE OF SHIPPING EXCESS SUPPLY IS THE CHALLENGE seaborne imports billion tonnes Several Trade Scenarios Growth of sea trade Period %pa % % % % % % China Imports World less China 7% i 7% scenario 4% scenario 3% scenario 1% scenario World & China s seaborne imports with scenarios Reference: Clarksons, UK XIII

14 WHAT DO THE LAST THREE SLIDES TELL US? As we can see from the previous three slides, world ship scrapping has increased but not significantly; as for an experienced ship owner it is economical to run old ships where cash flow requirements are low provided charterers are happy with your operations. Most of the ship building increases were in China and with China s economical success it will be difficult to close some of these yards. The best China can do is to put a ban on opening new ones. Therefore, it is expected that the growth in the world fleet will continue for some years without significant increase in world economic growth. In other words ship owner s return on ship operations have to come down drastically. Their margins have to come from some other activities. Only very cash flow rich shipping companies, national companies and very efficient shipping companies will survive the next 3-4 years. For this see slides XV & XVI:- 14

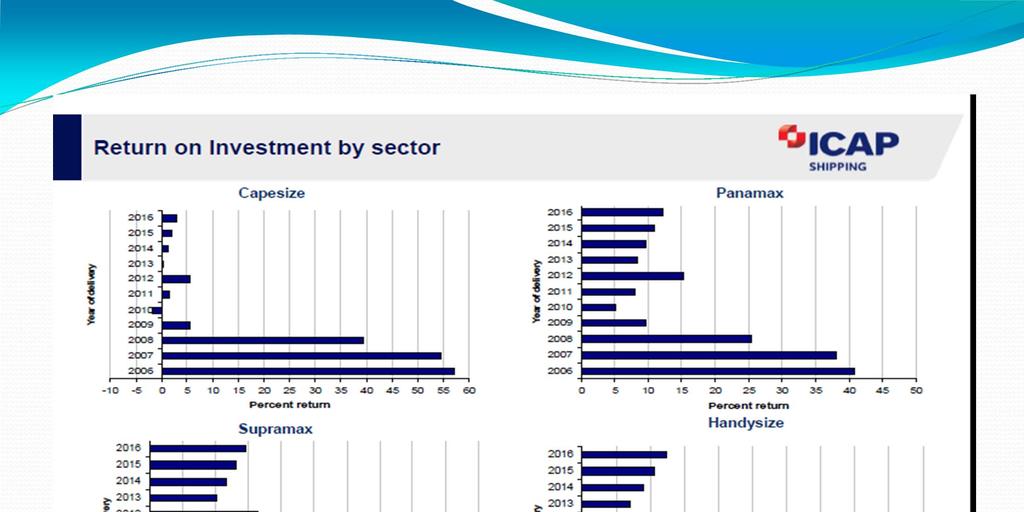

15 RETURN ON INVESTMENT: Assumptions used in the IRR model: Asset sold 5 years after delivery Return on investment by year of delivery and sector Handysize 25 years amortization costs Vessel delivered 24 months after ordering 8% financing costs 5% operational escalation rate Year of delivery Supramax Panamax Semiannual repayments Debt/Equity ratio 80/20 between Debt/Equity ratio 60/40 between Repayment done in 5 x 20% installments Earnings for the period based on both historical market performance and forward rate projections Return based on asset prices at the time of ordering (January) Scrap price assumed to average at $270 per Ldt for the period 2007 Cape Percent return Delivery year Cape Panamax Supramax Handysize XV

16 XVI

17 WHAT DO WE LEARN FROM THIS PRESENTATION UP TILL NOW? Ship owners got used to almost 50% returns on any kind of ships during 2005 to mid It gave them the best cash flows since the second world war. In other words it spoilt them and ship owners as usual became irresponsible and placed orders for new ships immediately which helped to increase shipbuilding capacity. The result of this over ordering will reduce returns on the capital employed to around 5% which is even below what nowadays banks are charging for lending money including Libor. This marginal return on capital will also disappear if the ship has a breakdown or waits idly between two charters. 17

18 SO THE QUESTION IS... Would you like to invest during 2012 in an industry where you know there are no or very little returns? Appreciation of ship values will also not be there as shipbuilding has excess capacity In my view, any person in their right mind would not undertake this investment in shipping, but we the ship owners are not right minded people We are egotistic and we are in love with our ships (after our women of course...) Each ship owner thinks he or she has the right formula for success 18

19 SO WHAT DO YOU DO WITH SUCH A BUNCH OF PEOPLE? The problem is we do not know any other business and we are intrigued by the romance of ships and the ocean, where both are unpredictable. We have learned to linger on with the hope of divine intervention which will change the economics of shipping. A recent sad example of divine intervention is the tsunami which hit Japan in March of last year. It changed the fortune of LNG ships. 19

20 So, let us examine the possibility of so called For this, I submit to you the next three slides to examine 20

21 XXI

22 OIL AND NATURAL GAS RESERVES XXII

23 XXIII

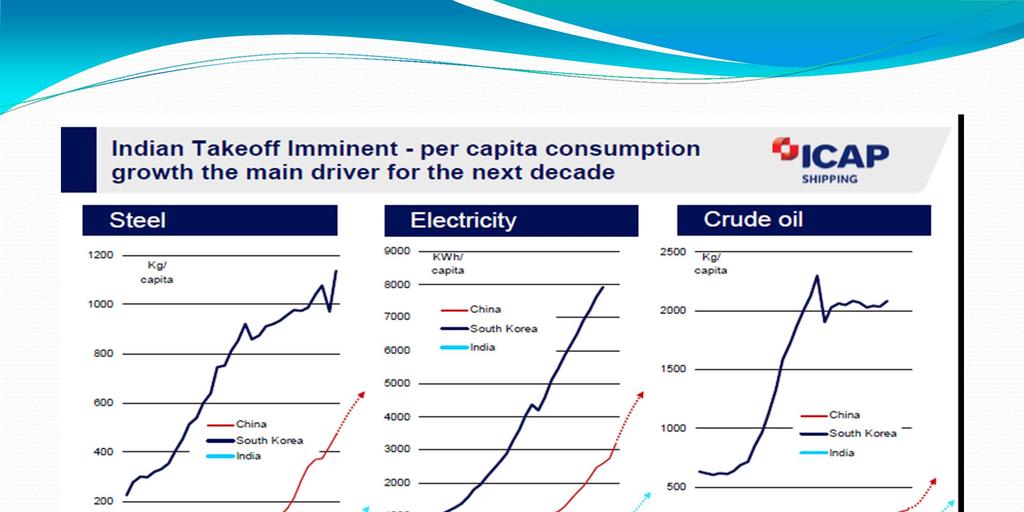

24 SUMMARY All three slides focus on the prospect of future growth of China and India. Any other country growing will have very little impact on the present day size of the world fleet due to the limited size of population in other countries. Slide XXI shows the per capita consumption of steel, electricity and oil in these two countries which are the primary indicators of growth of a country. This shows if they are to become middle level developed nations, how much they will have to grow. For this reason we have compared these two countries with South Korea. From the graph you can see that it looks like these two countries have not yet started growing, they have a long way to go. So the question is when? For this I would like to present slide XXV:- 24

25 NB: The Indian take-off could occur before the Chinese Phase II expansion has finished but not before when the Indian economy will develop critical mass of GDP above $ 3.5 Trillion per year XXV

26 CONCLUSION From this slide you can see at present that we are in an over supply position as far as shipping is concerned but come 2016 we are in for another shipping boom. This may be the grandfather of all previous booms as both China s phase II and India s phase I growth story will be unstoppable. The growth in shipbuilding will have a marginal effect when you compare 2.5 billion people trying to become consumers of the developed world s goodies. Every year China and India will be creating a new Europe of middle class income groups. Nothing will be able to slow down this boom. 26

27 So the question my Friends is not when is the next shipping boom? Given the change in consumption are we going to see a fundamental change in our ships and their trade routes? BUT Who, as a ship owner, will survive till 2016? 27

28 Do you have any suggestions? 28

29 WHEN IS THE NEXT SHIPPING BOOM? By Ravi K Mehrotra CBE Executive Chairman Foresight Group, London Samunder Club April & May 2012 Houston and Florida, USA 1

8 th City of London Biennial Meeting November 2016 International Maritime Organisation (IMO), London

, London") 8 th City of London Biennial Meeting 17-18 November 2016 International Maritime Organisation (IMO), London Drybulk Shipping in 21 st Century by Hakki Deval (MSc STF 2001) 0 China joins WTO in December

8 th City of London Biennial Meeting 17-18 November 2016 International Maritime Organisation (IMO), London Drybulk Shipping in 21 st Century by Hakki Deval (MSc STF 2001) 0 China joins WTO in December

Golden Ocean Group Limited Q results March 1, 2007

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Tanker Market Outlook. 12th Mare Forum Ship Finance 2012 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 2012

Tanker Market Outlook 12th Mare Forum Ship Finance 212 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 212 Tanker Market Outlook 12th Mare Forum Ship Finance 212 Disclaimer The material and

Tanker Market Outlook 12th Mare Forum Ship Finance 212 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 212 Tanker Market Outlook 12th Mare Forum Ship Finance 212 Disclaimer The material and

IUMI 2005 Amsterdam Facts & Figures Committee

Report on Marine Insurance Premium 23 and 24 IUMI 25 Amsterdam Facts & Figures Committee Tore Forsmo, Managing Director Astrid Seltmann, Analyst The Central Union of Marine Underwriters, Oslo, Norway Thanks

Report on Marine Insurance Premium 23 and 24 IUMI 25 Amsterdam Facts & Figures Committee Tore Forsmo, Managing Director Astrid Seltmann, Analyst The Central Union of Marine Underwriters, Oslo, Norway Thanks

Demand, Supply & Capacity in the Shipbuilding Industry

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

The World s Largest Buyer of Ships and Offshore Assets

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

Ship Scrapping - Market Pressures. IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 2012

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

PETROFIN RESEARCH Greek fleet statistics January 2018 based on data as of end December 2017

based on data as of end December RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF PETROFIN RESEARCH PETROFIN RESEARCH 2 year anniversary of Greek fleet analysis CONTENTS OF PETROFIN RESEARCH PART

based on data as of end December RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF PETROFIN RESEARCH PETROFIN RESEARCH 2 year anniversary of Greek fleet analysis CONTENTS OF PETROFIN RESEARCH PART

Long Term Trends in Shipbuilding HVB Press Conference. 20 th September 2006 Stephen Gordon, Clarkson Research

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

2015 RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF 2015 PETROFIN RESEARCH CONTENTS OF PETROFIN RESEARCH PART 2

based on data as of September RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF CONTENTS OF PART 2 RESULTS AT A GLANCE (P. 2) SECTION A: VITAL STATISTICS OF THE ENTIRE GREEK FLEET (P. 3) SECTION

based on data as of September RESEARCH AND ANALYSIS: GREEK FLEET STATISTICS 2ND PART OF CONTENTS OF PART 2 RESULTS AT A GLANCE (P. 2) SECTION A: VITAL STATISTICS OF THE ENTIRE GREEK FLEET (P. 3) SECTION

TANKER MARKET CAN A MIRACLE HAPPEN?

TEN Ltd THE TANKER MARKET CAN A MIRACLE HAPPEN? Nikolas P. Tsakos President & CEO, TEN November 19 th, 2008 1 Tanker Freight Rates Remain Healthy Charterer discrimination against single hull tonnage on

TEN Ltd THE TANKER MARKET CAN A MIRACLE HAPPEN? Nikolas P. Tsakos President & CEO, TEN November 19 th, 2008 1 Tanker Freight Rates Remain Healthy Charterer discrimination against single hull tonnage on

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

Petrofin Research Greek fleet statistics

Petrofin Research 2 nd part of Petrofin Research : Greek fleet statistics In this 2 nd part of Petrofin research, the Greek Fleet Statistics, we analyse the composition of the Greek fleet, in terms of

Petrofin Research 2 nd part of Petrofin Research : Greek fleet statistics In this 2 nd part of Petrofin research, the Greek Fleet Statistics, we analyse the composition of the Greek fleet, in terms of

ASL Marine Holdings Ltd.

ASL Marine Holdings Ltd. SHIPBUILDING SHIPREPAIR SHIPCHARTERING Pulse of Asia 2008 - Presentation 8 th July 2008 1 Presentation Outline Company Profile 9M FY2008 Financial Review Business Review - Shipbuilding

ASL Marine Holdings Ltd. SHIPBUILDING SHIPREPAIR SHIPCHARTERING Pulse of Asia 2008 - Presentation 8 th July 2008 1 Presentation Outline Company Profile 9M FY2008 Financial Review Business Review - Shipbuilding

I The shipping market contents ISL

Comment - Charts and Tables concerning The Shipping Market World Merchant Fleet Tanker Market Bulk Carrier Market Tab. 1 Additions/Reductions by Ship Types 2014-2016 and up to June 2017... III Tab. 2 Size

Comment - Charts and Tables concerning The Shipping Market World Merchant Fleet Tanker Market Bulk Carrier Market Tab. 1 Additions/Reductions by Ship Types 2014-2016 and up to June 2017... III Tab. 2 Size

GLOBAL SHIP RECYCLING MARKET OVERVIEW & June 30, rd Asia Ship Recycling & SNP Summit, China

GLOBAL SHIP RECYCLING MARKET OVERVIEW & OUTLOOK 2011 1 SHIP RECYCLING 1. Commercial influences on scrapping decision 2. The Global Ship Recycling Industry: Where it s done 3. Issues: Supply, Capacity and

GLOBAL SHIP RECYCLING MARKET OVERVIEW & OUTLOOK 2011 1 SHIP RECYCLING 1. Commercial influences on scrapping decision 2. The Global Ship Recycling Industry: Where it s done 3. Issues: Supply, Capacity and

Greek Shipping : Greece s steaming force

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

COSCO CORPORATION. (SINGAPORE) LTD FY2003 Full Year Results. Presentation

LTD FY2003 Full Year Results. Presentation") COSCO CORPORATION (SINGAPORE) LTD FY2003 Full Year Results Presentation 11 February 2004 1 Outline of Presentation 1. Background & Corporate Restructuring Exercise 2. Operations Review 3. Financial Review

COSCO CORPORATION (SINGAPORE) LTD FY2003 Full Year Results Presentation 11 February 2004 1 Outline of Presentation 1. Background & Corporate Restructuring Exercise 2. Operations Review 3. Financial Review

Management Discussions and Analysis for the three-month period ended 31 March 2014 and Executive Summary

Executive Summary Overview of the global economy during the first quarter of 2015 (Q1/2015) are as following; the US economy has been in recovery mode while rapidly dollar appreciation weighs on net exports

Executive Summary Overview of the global economy during the first quarter of 2015 (Q1/2015) are as following; the US economy has been in recovery mode while rapidly dollar appreciation weighs on net exports

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

Appendix 8: Fitted distribution parameters for ship location

Appendix 8: Fitted distribution parameters for ship location Drogden Southbound Data Fitted Average -56-56 Stdev 56 34 Ratio,4 Registrations Mixed dist Channel borders 1 9 8 7 6 5 4 3 2 1-5 -3-1 1 3 5,12,1

Appendix 8: Fitted distribution parameters for ship location Drogden Southbound Data Fitted Average -56-56 Stdev 56 34 Ratio,4 Registrations Mixed dist Channel borders 1 9 8 7 6 5 4 3 2 1-5 -3-1 1 3 5,12,1

Song Rui Tourism Research Center, Chinese Academy of Social Sciences March 7, 2018, Berlin

Report on World Tourism Economy Trends (2018) Song Rui Tourism Research Center, Chinese Academy of Social Sciences March 7, 2018, Berlin TREND I Fast and comprehensive growth of the global tourism economy

Report on World Tourism Economy Trends (2018) Song Rui Tourism Research Center, Chinese Academy of Social Sciences March 7, 2018, Berlin TREND I Fast and comprehensive growth of the global tourism economy

Danish Shipping. Facts and Figures. June 2018

Danish Shipping Facts and Figures June 2018 2 Table of Contents 1. Danish Shipping Industry 4 The Danish Merchant Fleet 4 Danish Shipping Exports 6 Employment 8 CEO Survey 10 2. Global Merchant Fleet 12

Danish Shipping Facts and Figures June 2018 2 Table of Contents 1. Danish Shipping Industry 4 The Danish Merchant Fleet 4 Danish Shipping Exports 6 Employment 8 CEO Survey 10 2. Global Merchant Fleet 12

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

Vagelis Chatzigiannis, GMS. 3rd February, 2016 International Seminar: Towards Sustainable Ship Recycling 1

Vagelis Chatzigiannis, GMS 3rd February, 2016 International Seminar: Towards Sustainable Ship Recycling 1 1.1. Issues affecting the implementation of actual Responsible Ship Recycling Practices a) Deep

Vagelis Chatzigiannis, GMS 3rd February, 2016 International Seminar: Towards Sustainable Ship Recycling 1 1.1. Issues affecting the implementation of actual Responsible Ship Recycling Practices a) Deep

Growing Horizons Global Market Forecast

Growing Horizons Global Market Forecast 2017-2036 John Leahy Chief Operating Officer, Customers Global Market Forecast 2017: Highlights World Fleet Forecast 2016 2036 RPK (trillions) 7.0 16.5 vs. GMF16

Growing Horizons Global Market Forecast 2017-2036 John Leahy Chief Operating Officer, Customers Global Market Forecast 2017: Highlights World Fleet Forecast 2016 2036 RPK (trillions) 7.0 16.5 vs. GMF16

Handelsbanken Nordic Large Cap Seminar

Handelsbanken Nordic Large Cap Seminar BJÖRN ROSENGREN, PRESIDENT AND CEO 10 SEPTEMBER 2012 Wärtsilä This is Wärtsilä POWER PLANTS SHIP POWER SERVICES 2 Wärtsilä Global net sales - top 10 countries Norway

Handelsbanken Nordic Large Cap Seminar BJÖRN ROSENGREN, PRESIDENT AND CEO 10 SEPTEMBER 2012 Wärtsilä This is Wärtsilä POWER PLANTS SHIP POWER SERVICES 2 Wärtsilä Global net sales - top 10 countries Norway

Shipbuilding, Ship Repair and Ship Breaking Sector Profile

Shipbuilding, Ship Repair and Ship Breaking Sector Profile Sector Snapshot: Shipbuilding, Ship Repair and Ship Recycling The Indian Shipbuilding and Ship Repair industry primarily comprises firms that

Shipbuilding, Ship Repair and Ship Breaking Sector Profile Sector Snapshot: Shipbuilding, Ship Repair and Ship Recycling The Indian Shipbuilding and Ship Repair industry primarily comprises firms that

KOPONEN VICE PRESIDENT, FINANCE & CONTROL, SHIP POWER

WÄRTSILÄ IN CHINA KEVA trip to Shanghai TIMO KOPONEN VICE PRESIDENT, FINANCE & CONTROL, SHIP POWER 7.11.2011 1 Wärtsilä Agenda What is Wärtsilä today? Where is ship building today? Why Wärtsilä is in China?

WÄRTSILÄ IN CHINA KEVA trip to Shanghai TIMO KOPONEN VICE PRESIDENT, FINANCE & CONTROL, SHIP POWER 7.11.2011 1 Wärtsilä Agenda What is Wärtsilä today? Where is ship building today? Why Wärtsilä is in China?

ANNUAL GENERAL MEETING 2007

ANNUAL GENERAL MEETING 2007 Ole Johansson 1 Wärtsilä Ship Power solutions Growth through new products and increasing presence in Asia Power Plant solutions Stronger position in decentralized energy 2 Wärtsilä

ANNUAL GENERAL MEETING 2007 Ole Johansson 1 Wärtsilä Ship Power solutions Growth through new products and increasing presence in Asia Power Plant solutions Stronger position in decentralized energy 2 Wärtsilä

Fourth Quarter 2015 Financial Results

Fourth Quarter 2015 Financial Results AerCap Holdings N.V. February 23, 2016 Disclaimer Incl. Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates and forecasts

Fourth Quarter 2015 Financial Results AerCap Holdings N.V. February 23, 2016 Disclaimer Incl. Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates and forecasts

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

WÄRTSILÄ CORPORATION

WÄRTSILÄ CORPORATION 26 RESULT PRESENTATION OLE JOHANSSON, PRESIDENT & CEO 6 FEBRUARY 27 1 Wärtsilä Highlights 26 Order intake +32.4% Order book +52.8% Net sales +26.6% Operating income +29.2% Profitability

WÄRTSILÄ CORPORATION 26 RESULT PRESENTATION OLE JOHANSSON, PRESIDENT & CEO 6 FEBRUARY 27 1 Wärtsilä Highlights 26 Order intake +32.4% Order book +52.8% Net sales +26.6% Operating income +29.2% Profitability

Dry Bulk Market Weekly Highlights Week 17 - Dry Cargo Market Highlights for the period of 21-April-2011 until 28-April-2011

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

2016 List of all ships scrapped worldwide - Facts and Figures

216 List of all ships scrapped worldwide - Facts and Figures RoW EU 6 22 Ships scrapped worldwide Turkey 92 China 74 Pakistan 141 Bangladesh 222 India 35 5 1 15 2 25 3 35 RoW EU Turkey 53.82 38.839 1.4.335

216 List of all ships scrapped worldwide - Facts and Figures RoW EU 6 22 Ships scrapped worldwide Turkey 92 China 74 Pakistan 141 Bangladesh 222 India 35 5 1 15 2 25 3 35 RoW EU Turkey 53.82 38.839 1.4.335

State of the Aviation Industry

State of the Aviation Industry Presentation to the ACI Airport Economics & Finance 10 th 11 th February London, United Kingdom Laurie N. Price Director of Aviation Strategy Mott MacDonald Aviation Current

State of the Aviation Industry Presentation to the ACI Airport Economics & Finance 10 th 11 th February London, United Kingdom Laurie N. Price Director of Aviation Strategy Mott MacDonald Aviation Current

Ship Recycling Trends, Developments & Outlook. October 21 st, 2010 Ship Recycling: Trends, Developments & Outlook 1

Ship Recycling Trends, Developments & Outlook October 21 st, 2010 Ship Recycling: Trends, Developments & Outlook 1 Ship-Recycling: From 2004 late 2008 Slowest periods in history of ship recycling More

Ship Recycling Trends, Developments & Outlook October 21 st, 2010 Ship Recycling: Trends, Developments & Outlook 1 Ship-Recycling: From 2004 late 2008 Slowest periods in history of ship recycling More

PETROFIN RESEARCH Greek shipping companies January 2018 based on data as of December 2017

1 2017 RESEARCH AND ANALYSIS: GREEK SHIPPING COMPANIES 1ST PART OF 2017 PETROFIN RESEARCH Petrofin Research are pleased to announce the release of the first part of their 2017 Greek Shipping research.

1 2017 RESEARCH AND ANALYSIS: GREEK SHIPPING COMPANIES 1ST PART OF 2017 PETROFIN RESEARCH Petrofin Research are pleased to announce the release of the first part of their 2017 Greek Shipping research.

Q Earnings Financial Results for the Third Quarter Ended December 31, January 29, 2015 OMRON Corporation

Q3 2014 Earnings Financial Results for the Third Quarter Ended December 31, 2014 January 29, 2015 OMRON Corporation Contents 1. Summary 2. Q1-Q3 Results P. 2 P. 4 3. Full-Year Forecast P. 13 4. Corporate

Q3 2014 Earnings Financial Results for the Third Quarter Ended December 31, 2014 January 29, 2015 OMRON Corporation Contents 1. Summary 2. Q1-Q3 Results P. 2 P. 4 3. Full-Year Forecast P. 13 4. Corporate

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007.

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007. Athens, Greece, November 15, 2007. Globus Maritime Limited (AIM: GLBS), a

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007. Athens, Greece, November 15, 2007. Globus Maritime Limited (AIM: GLBS), a

WÄRTSILÄ CORPORATION

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-JUNE 214 18 JULY 214 Björn Rosengren, President & CEO Wärtsilä Highlights Q2/214 NEW PIC Order intake EUR 1,163 million, +9% Net sales EUR 1,132 million, -2%

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-JUNE 214 18 JULY 214 Björn Rosengren, President & CEO Wärtsilä Highlights Q2/214 NEW PIC Order intake EUR 1,163 million, +9% Net sales EUR 1,132 million, -2%

Market Commentary. Greece s Shipping Sector: Overview and Outlook

Market Commentary November 10, 2010 Greece s Shipping Sector: Overview and Outlook Overview Greece is a maritime nation by tradition and is one of the world's largest shipping powers. Greek shipping is

Market Commentary November 10, 2010 Greece s Shipping Sector: Overview and Outlook Overview Greece is a maritime nation by tradition and is one of the world's largest shipping powers. Greek shipping is

Textile Per Capita Consumption

January 2018 Textile Per Capita Consumption 2005-2022 Part 2: Upper middle income countries - - CHF500.- Table of Contents Preface... 4 Sources... 5 Definitions... 6 Charts... 7 Executive Summary... 10

January 2018 Textile Per Capita Consumption 2005-2022 Part 2: Upper middle income countries - - CHF500.- Table of Contents Preface... 4 Sources... 5 Definitions... 6 Charts... 7 Executive Summary... 10

E u r o E c o n o m i c a Issue 1(37)/2018 ISSN:

/2018 ISSN:") Issue 1(37)/2018 ISSN: 1582-8859 An Overview on the Shipbuilding Market in Current Period and Forecast Carmen Gasparotti 1, Eugen Rusu 2 Abstract: The work presents the evolution of the shipbuilding market

Issue 1(37)/2018 ISSN: 1582-8859 An Overview on the Shipbuilding Market in Current Period and Forecast Carmen Gasparotti 1, Eugen Rusu 2 Abstract: The work presents the evolution of the shipbuilding market

III. TRADE IN COMMERCIAL SERVICES BY CATEGORY

. TRADE IN COMMERCIAL SERVICES BY CATEGORY The Highlights Transportation services Rising seaborne trade and air traffic contribute to the increase of transportation services trade In a context of rising

. TRADE IN COMMERCIAL SERVICES BY CATEGORY The Highlights Transportation services Rising seaborne trade and air traffic contribute to the increase of transportation services trade In a context of rising

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER October 2016 Jaakko Eskola, President & CEO. Wärtsilä PUBLIC

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER 216 25 October 216 Jaakko Eskola, President & CEO 1 Wärtsilä PUBLIC 25 October 216 Q3 result presentation Highlights Q3/216 Order intake EUR 1,139

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER 216 25 October 216 Jaakko Eskola, President & CEO 1 Wärtsilä PUBLIC 25 October 216 Q3 result presentation Highlights Q3/216 Order intake EUR 1,139

1. FORECAST VISITATION FOR GREAT OCEAN ROAD

1. FORECAST VISITATION FOR GREAT OCEAN ROAD 1.1. INTRODUCTION This section provides a 20-year forecast of visitation to the Great Ocean Road Region, modelled from Australian Tourism Forecast Committee

1. FORECAST VISITATION FOR GREAT OCEAN ROAD 1.1. INTRODUCTION This section provides a 20-year forecast of visitation to the Great Ocean Road Region, modelled from Australian Tourism Forecast Committee

Concrete Visions for a Multi-Level Governance, 7-8 December Paper for the Workshop Local Governance in a Global Era In Search of

Paper for the Workshop Local Governance in a Global Era In Search of Concrete Visions for a Multi-Level Governance, 7-8 December 2001 None of these papers should be cited without the author s permission.

Paper for the Workshop Local Governance in a Global Era In Search of Concrete Visions for a Multi-Level Governance, 7-8 December 2001 None of these papers should be cited without the author s permission.

2012 RESULT PRESENTATION

212 RESULT PRESENTATION BJÖRN ROSENGREN, PRESIDENT & CEO 25 JANUARY 213 Wärtsilä Net sales back to growth with stable profitability 212 development Order intake EUR 4,94 million, +9% Net sales EUR 4,725

212 RESULT PRESENTATION BJÖRN ROSENGREN, PRESIDENT & CEO 25 JANUARY 213 Wärtsilä Net sales back to growth with stable profitability 212 development Order intake EUR 4,94 million, +9% Net sales EUR 4,725

Weekly Dry Bulk Report

Week 36 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 3th 214 HIGHLIGHTS Capesize: Generally lower rates this week Supramax/Handymax: Continued improved market for both segments

Week 36 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 3th 214 HIGHLIGHTS Capesize: Generally lower rates this week Supramax/Handymax: Continued improved market for both segments

PRESS ANNOUNCEMENT JULY 28, 1999 For Immediate Release STAR CRUISES REPORTS RECORD SECOND QUARTER EARNINGS

PRESS ANNOUNCEMENT JULY 28, 1999 For Immediate Release STAR CRUISES REPORTS RECORD SECOND QUARTER EARNINGS STAR CRUISES PLC announced record net income of US$20.7 million (US 3.3 cents earnings per share)

PRESS ANNOUNCEMENT JULY 28, 1999 For Immediate Release STAR CRUISES REPORTS RECORD SECOND QUARTER EARNINGS STAR CRUISES PLC announced record net income of US$20.7 million (US 3.3 cents earnings per share)

SHIP MANAGEMENT SURVEY. July December 2017

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

Airbus market forecast for India. Presented by Joost van der Heijden Head of Airline Marketing India, South-East Asia, Japan & Africa

Airbus market forecast for India Presented by Joost van der Heijden Head of Airline Marketing India, South-East Asia, Japan & Africa The Airbus product line A380 Family A350 Family A330 Family A320 Family

Airbus market forecast for India Presented by Joost van der Heijden Head of Airline Marketing India, South-East Asia, Japan & Africa The Airbus product line A380 Family A350 Family A330 Family A320 Family

2017 List of all ships scrapped worldwide - Facts and Figures

217 List of all ships scrapped worldwide - Facts and Figures RoW EU 27 34 Ships scrapped worldwide Turkey 133 China Pakistan 98 17 Bangladesh 197 India 239 5 1 15 2 25 3 35 RoW 335.84 EU Turkey 65.915

217 List of all ships scrapped worldwide - Facts and Figures RoW EU 27 34 Ships scrapped worldwide Turkey 133 China Pakistan 98 17 Bangladesh 197 India 239 5 1 15 2 25 3 35 RoW 335.84 EU Turkey 65.915

Alberto Calderon Group Executive and Chief Executive Aluminium, Nickel and Corporate Development

Port Hedland, Iron Ore, Australia Alberto Calderon Group Executive and Chief Executive Aluminium, Nickel and Corporate Development Economic and Social Outlook Conference 1 November 2012 Disclaimer Forward

Port Hedland, Iron Ore, Australia Alberto Calderon Group Executive and Chief Executive Aluminium, Nickel and Corporate Development Economic and Social Outlook Conference 1 November 2012 Disclaimer Forward

GRINDROD LIMITED AUDITED RESULTS AND DIVIDEND ANNOUNCEMENT for the year ended 31 December 2016

www.grindrod.com GRINDROD LIMITED AUDITED RESULTS AND DIVIDEND ANNOUNCEMENT for the year ended 31 December 2016 Wifi access guest@sun Presentation and Announcement download www.grindrod.com > Investor

www.grindrod.com GRINDROD LIMITED AUDITED RESULTS AND DIVIDEND ANNOUNCEMENT for the year ended 31 December 2016 Wifi access guest@sun Presentation and Announcement download www.grindrod.com > Investor

Q Earnings Financial Results for the First Quarter Ended June 30, July 28, 2016 OMRON Corporation

Q1 2016 Earnings Financial Results for the First Quarter Ended June 30, 2016 July 28, 2016 OMRON Corporation Summary Q1 Results Both sales and operating income are in line with internal plan (decreased

Q1 2016 Earnings Financial Results for the First Quarter Ended June 30, 2016 July 28, 2016 OMRON Corporation Summary Q1 Results Both sales and operating income are in line with internal plan (decreased

Wärtsilä Corporation. Interim Report January-September 2006 Ole Johansson, President & CEO. 31 October Wärtsilä

Wärtsilä Corporation Interim Report January-September 26 Ole Johansson, President & CEO 31 October 26 Highlights Q3/26 Strong order intake continued (+25%) Net sales +26% Operating income +29% Strong cash

Wärtsilä Corporation Interim Report January-September 26 Ole Johansson, President & CEO 31 October 26 Highlights Q3/26 Strong order intake continued (+25%) Net sales +26% Operating income +29% Strong cash

AIR PASSENGER MARKET ANALYSIS

AIR PASSENGER MARKET ANALYSIS OCTOBER 2014 KEY POINTS Air travel volumes were up 5.7% in October year-on-year, slightly stronger than the September rise of 5.2%, and a continuation of the positive growth

AIR PASSENGER MARKET ANALYSIS OCTOBER 2014 KEY POINTS Air travel volumes were up 5.7% in October year-on-year, slightly stronger than the September rise of 5.2%, and a continuation of the positive growth

Ship Recycling: The last pillar of shipping. February 22, nd Annual Capital Link Greek Shipping Forum 1

Ship Recycling: The last pillar of shipping February 22, 2011 2 nd Annual Capital Link Greek Shipping Forum 1 Where do old ships go? Indian subcontinent India, Bangladesh and Pakistan China Turkey February

Ship Recycling: The last pillar of shipping February 22, 2011 2 nd Annual Capital Link Greek Shipping Forum 1 Where do old ships go? Indian subcontinent India, Bangladesh and Pakistan China Turkey February

WÄRTSILÄ CORPORATION RESULT PRESENTATION JANUARY Björn Rosengren, President & CEO. Wärtsilä

WÄRTSILÄ CORPORATION RESULT PRESENTATION 2014 29 JANUARY 2015 Björn Rosengren, President & CEO Wärtsilä Highlights 2014 good performance in challenging markets Order intake EUR 5,084 million, +5% Net sales

WÄRTSILÄ CORPORATION RESULT PRESENTATION 2014 29 JANUARY 2015 Björn Rosengren, President & CEO Wärtsilä Highlights 2014 good performance in challenging markets Order intake EUR 5,084 million, +5% Net sales

JET AIRWAYS (I) LTD. Presentation on Financial Results Q July 24, 2009

LTD. Presentation on Financial Results Q July 24, 2009") JET AIRWAYS (I) LTD Presentation on Financial Results Q1 2010 July 24, 2009 1 1 1 Agenda Domestic operating environment Jet Airways performance highlights JetLite performance highlights Outlook 2 2 2 Domestic

JET AIRWAYS (I) LTD Presentation on Financial Results Q1 2010 July 24, 2009 1 1 1 Agenda Domestic operating environment Jet Airways performance highlights JetLite performance highlights Outlook 2 2 2 Domestic

PRESS RELEASE November 18, 2002 STAR CRUISES GROUP ANNOUNCES IMPROVED EARNINGS FOR THIRD QUARTER AND FIRST NINE MONTHS OF 2002

PRESS RELEASE November 18, 2002 FOR IMMEDIATE RELEASE INTERNATIONAL STAR CRUISES GROUP ANNOUNCES IMPROVED EARNINGS FOR THIRD QUARTER AND FIRST NINE MONTHS OF 2002 Key points for the quarter and in comparison

PRESS RELEASE November 18, 2002 FOR IMMEDIATE RELEASE INTERNATIONAL STAR CRUISES GROUP ANNOUNCES IMPROVED EARNINGS FOR THIRD QUARTER AND FIRST NINE MONTHS OF 2002 Key points for the quarter and in comparison

Press Release. Bilfinger with dynamic start to financial year 2018

Press Release May 15, 2018 Bilfinger with dynamic start to financial year 2018 Book-to-bill ratio reaches 1.2 in the first quarter Fourth consecutive growth quarter in orders received Adjusted EBITA above

Press Release May 15, 2018 Bilfinger with dynamic start to financial year 2018 Book-to-bill ratio reaches 1.2 in the first quarter Fourth consecutive growth quarter in orders received Adjusted EBITA above

INTERIM REPORT JANUARY-JUNE 2013

INTERIM REPORT JANUARY-JUNE 213 BJÖRN ROSENGREN, PRESIDENT & CEO 18 JULY 213 Wärtsilä Highlights Q2/213 NEW PIC Order intake EUR 1,71 million, -11% Net sales EUR 1,152 million, +5% Book-to-bill.93 EBITA

INTERIM REPORT JANUARY-JUNE 213 BJÖRN ROSENGREN, PRESIDENT & CEO 18 JULY 213 Wärtsilä Highlights Q2/213 NEW PIC Order intake EUR 1,71 million, -11% Net sales EUR 1,152 million, +5% Book-to-bill.93 EBITA

Weekly Dry Bulk Report

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

III. TRADE IN COMMERCIAL SERVICES BY CATEGORY

.. TRADE IN COMMERCIAL SERVICES BY CATEGORY Transportation services China records impressive growth Exports of world transportation services reached $750 billion in 2007, an increase of 19 per cent, following

.. TRADE IN COMMERCIAL SERVICES BY CATEGORY Transportation services China records impressive growth Exports of world transportation services reached $750 billion in 2007, an increase of 19 per cent, following

Press Release. Bilfinger 2017: Stable foundation laid for the future

Press Release February 14, 2018 Bilfinger 2017: Stable foundation laid for the future Organic growth in orders received after three years of decline Trend reversal: Output volume better than expected Growth

Press Release February 14, 2018 Bilfinger 2017: Stable foundation laid for the future Organic growth in orders received after three years of decline Trend reversal: Output volume better than expected Growth

SHIPBUILDING INDUSTRY CORPORATION (SBIC) VIETNAM MARITIME INDUSTRY (Presentation at ASEF 9 th Forum)

VIETNAM MARITIME INDUSTRY (Presentation at ASEF 9 th Forum)") SHIPBUILDING INDUSTRY CORPORATION (SBIC) VIETNAM MARITIME INDUSTRY (Presentation at ASEF 9 th Forum) VIETNAM MARITIME INDUSTRY (Presentation at ASEF 9 th Forum) Contents Vietnam Overview Vietnam Maritime

SHIPBUILDING INDUSTRY CORPORATION (SBIC) VIETNAM MARITIME INDUSTRY (Presentation at ASEF 9 th Forum) VIETNAM MARITIME INDUSTRY (Presentation at ASEF 9 th Forum) Contents Vietnam Overview Vietnam Maritime

Thank you for participating in the financial results for fiscal 2014.

Thank you for participating in the financial results for fiscal 2014. ANA HOLDINGS strongly believes that safety is the most important principle of our air transportation business. The expansion of slots

Thank you for participating in the financial results for fiscal 2014. ANA HOLDINGS strongly believes that safety is the most important principle of our air transportation business. The expansion of slots

Circumnavigation HELM PwC Economy of the Sea Barometer (World)

") www.pwc.pt HELM PwC Economy of the Sea Barometer (World) In-depth HELM December 2015 Edition nº1 2 I really don't know why it is that all of us are so committed to the sea, except I think it's because

www.pwc.pt HELM PwC Economy of the Sea Barometer (World) In-depth HELM December 2015 Edition nº1 2 I really don't know why it is that all of us are so committed to the sea, except I think it's because

Wärtsilä Corporation 2005

Wärtsilä Corporation 25 Ole Johansson, President & CEO 7 February 26 Mission and Vision Mission We provide lifecycle power solutions to enhance the business of our customers, whilst creating better technologies

Wärtsilä Corporation 25 Ole Johansson, President & CEO 7 February 26 Mission and Vision Mission We provide lifecycle power solutions to enhance the business of our customers, whilst creating better technologies

Circumnavigation HELM PwC Economy of the Sea Barometer (World)

") www.pwc.pt HELM PwC Economy of the Sea Barometer (World) In-depth HELM December 2017 Edition nº3 2 One simply needs to grab an old conch shell to distinctly hear the great voice of the sea. The conch was

www.pwc.pt HELM PwC Economy of the Sea Barometer (World) In-depth HELM December 2017 Edition nº3 2 One simply needs to grab an old conch shell to distinctly hear the great voice of the sea. The conch was

Passenger traffic growth rate slowed to 3.6% in August; air freight volumes increased by 4.8%

Passenger traffic growth rate slowed to 3.6% in August; air freight volumes increased by 4.8% Montréal, 24 October Global airport passenger traffic lost momentum from a growth rate of 5.4% in July to 3.6%

Passenger traffic growth rate slowed to 3.6% in August; air freight volumes increased by 4.8% Montréal, 24 October Global airport passenger traffic lost momentum from a growth rate of 5.4% in July to 3.6%

TURKISH SHIPBUILDING/ RECYCLING INDUSTRIES AND NATIONAL POLICIES SUPPORTING GREENER SHIPPING

MINISTRY OF TRANSPORT MARITIME AFFAIRS AND COMMUNICATIONS TURKISH SHIPBUILDING/ RECYCLING INDUSTRIES AND NATIONAL POLICIES SUPPORTING GREENER SHIPPING OECD WP6 WORKSHOP ON GREEN GROWTH OF MARITIME INDUSTRIES

MINISTRY OF TRANSPORT MARITIME AFFAIRS AND COMMUNICATIONS TURKISH SHIPBUILDING/ RECYCLING INDUSTRIES AND NATIONAL POLICIES SUPPORTING GREENER SHIPPING OECD WP6 WORKSHOP ON GREEN GROWTH OF MARITIME INDUSTRIES

COMPARATIVE STUDY ON GROWTH AND FINANCIAL PERFORMANCE OF JET AIRWAYS, INDIGO AIRLINES & SPICEJET AIRLINES COMPANIES IN INDIA

Volume 2, Issue 2, November 2017, ISBR Management Journal ISSN(Online)- 2456-9062 COMPARATIVE STUDY ON GROWTH AND FINANCIAL PERFORMANCE OF JET AIRWAYS, INDIGO AIRLINES & SPICEJET AIRLINES COMPANIES IN

Volume 2, Issue 2, November 2017, ISBR Management Journal ISSN(Online)- 2456-9062 COMPARATIVE STUDY ON GROWTH AND FINANCIAL PERFORMANCE OF JET AIRWAYS, INDIGO AIRLINES & SPICEJET AIRLINES COMPANIES IN

Online Case. Practice case. Slides HTS de préparation - fev 2016_rev HC.pptx Draft for discussion only

Copyright 2016 by The Boston Co onsulting Group, Inc. All rights reserved. Online Case Practice case Slides HTS de préparation - fev 2016_rev HC.pptx Draft for discussion only 0 INSTRUCTIONS (1/3) During

Copyright 2016 by The Boston Co onsulting Group, Inc. All rights reserved. Online Case Practice case Slides HTS de préparation - fev 2016_rev HC.pptx Draft for discussion only 0 INSTRUCTIONS (1/3) During

(ships destined for scrap went for trading)

") Ship Recycling Trends, Developments & Outlook July 23, 2009 Ship Recycling: Trends, Developments & Outlook 1 Ship-Recycling: From 2004 late 2008 Slowest periods in history of ship recycling More than 5-fold

Ship Recycling Trends, Developments & Outlook July 23, 2009 Ship Recycling: Trends, Developments & Outlook 1 Ship-Recycling: From 2004 late 2008 Slowest periods in history of ship recycling More than 5-fold

Cathay Pacific Airways 2010 Annual Results 9 March 2011

Cathay Pacific Airways 2010 Annual Results 9 March 2011 1 Annual Result 2010 2009 Change Group Profit/(Loss) HK$14,048m HK$4,694m +199.3% Group Turnover HK$89,524m HK$66,978m +33.7% Profit Margin 15.7%

Cathay Pacific Airways 2010 Annual Results 9 March 2011 1 Annual Result 2010 2009 Change Group Profit/(Loss) HK$14,048m HK$4,694m +199.3% Group Turnover HK$89,524m HK$66,978m +33.7% Profit Margin 15.7%

LPG & Petrochemical Shipping: Current Status & Outlook. A better market, but for how long? Nicola Williams, Clarksons March 16th 2005

LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams, Clarksons March 16th 2005 The LPG Shipping Market today The LPG freight market started to move

LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams, Clarksons March 16th 2005 The LPG Shipping Market today The LPG freight market started to move

Index of business confidence. Monthly FTK (Billions) Aug 2013 vs. Aug 2012 YTD 2013 vs. YTD 2012 Aug 2013 vs. Jul 2013

Aug 2013 vs. Aug 2012 YTD 2013 vs. YTD 2012 Aug 2013 vs. Jul 2013") AIR PASSENGER MARKET ANALYSIS AUGUST 2013 KEY POINTS Air travel markets expanded strongly in August. Global revenue passenger kilometers were up 6.8% compared to a year ago, an improvement on July growth

AIR PASSENGER MARKET ANALYSIS AUGUST 2013 KEY POINTS Air travel markets expanded strongly in August. Global revenue passenger kilometers were up 6.8% compared to a year ago, an improvement on July growth

SHIPBUILDING INDUSTRY

0 SHIPBUILDING INDUSTRY Turkey is surrounded by sea on three sides, is a natural bridge between Asia and Europe. Turkey borders the Black Sea, the Mediterranean, the Aegean and the Sea of Marmara. The

0 SHIPBUILDING INDUSTRY Turkey is surrounded by sea on three sides, is a natural bridge between Asia and Europe. Turkey borders the Black Sea, the Mediterranean, the Aegean and the Sea of Marmara. The

USA Acquisition Summary. December 2010

USA Acquisition Summary December 2010 www.roadbearrv.com Strategic Intent 1. To leverage the existing business capabilities in a significant sized and growing tourism market with a similar customer base.

USA Acquisition Summary December 2010 www.roadbearrv.com Strategic Intent 1. To leverage the existing business capabilities in a significant sized and growing tourism market with a similar customer base.

WÄRTSILÄ CORPORATION

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER 215 22 OCTOBER 215 Björn Rosengren, President & CEO Wärtsilä Highlights Q3/215 Order intake EUR 1,86 million, -17% Net sales EUR 1,222 million, +9%

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER 215 22 OCTOBER 215 Björn Rosengren, President & CEO Wärtsilä Highlights Q3/215 Order intake EUR 1,86 million, -17% Net sales EUR 1,222 million, +9%

OFFSHORE MONTHLY MARKET OVERVIEW

OFFSHORE MONTHLY MARKET OVERVIEW 1 st 3 th November 17 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity +44 () 3 6 vesselsvalue.com OFFSHORE VALUES

OFFSHORE MONTHLY MARKET OVERVIEW 1 st 3 th November 17 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity +44 () 3 6 vesselsvalue.com OFFSHORE VALUES

KOREAN AIR 4Q17 FINANCIAL RESULTS

KOREAN AIR 4Q17 FINANCIAL RESULTS 1 Disclaimer This presentation is for informational purposes only, contains preliminary financial and other information about Korean Air Lines Co., Ltd. and is subject

KOREAN AIR 4Q17 FINANCIAL RESULTS 1 Disclaimer This presentation is for informational purposes only, contains preliminary financial and other information about Korean Air Lines Co., Ltd. and is subject

ABX. Holdings, Inc. BB&T Transportation Conference. February 2008

ABX Holdings, Inc. BB&T Transportation Conference February 2008 1 Safe Harbor Statement Except for historical information contained herein, the matters discussed in this presentation contain forward-looking

ABX Holdings, Inc. BB&T Transportation Conference February 2008 1 Safe Harbor Statement Except for historical information contained herein, the matters discussed in this presentation contain forward-looking

GOLDEN DESTINY MONTHLY NEWBUILDING REPORT

ISSUE NO.04/2013 APRIL 2013 MONTHLY NEWBUILDING REPORT ORDERING ACTIVITY (per vessel type) by Greek and Foreign Owners GOLDEN DESTINY MONTHLY NEWBUILDING REPORT highlights the volume of transactions in

ISSUE NO.04/2013 APRIL 2013 MONTHLY NEWBUILDING REPORT ORDERING ACTIVITY (per vessel type) by Greek and Foreign Owners GOLDEN DESTINY MONTHLY NEWBUILDING REPORT highlights the volume of transactions in

Alianza del Pacífico. October, Germán Ríos May 2012

Alianza del Pacífico October, 2011 Germán Ríos May 2012 Table of Contents The integration process in Latin America The future is Asia Latin America and Alianza del Pacífico The integration process in Latin

Alianza del Pacífico October, 2011 Germán Ríos May 2012 Table of Contents The integration process in Latin America The future is Asia Latin America and Alianza del Pacífico The integration process in Latin

WÄRTSILÄ CORPORATION

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER 21 OLE JOHANSSON, PRESIDENT & CEO 2 OCTOBER 21 1 Wärtsilä Q3/1 Highlights Order intake EUR 1,4 million (+38%) Net sales EUR 1,39 million (-11%) Operating

WÄRTSILÄ CORPORATION INTERIM REPORT JANUARY-SEPTEMBER 21 OLE JOHANSSON, PRESIDENT & CEO 2 OCTOBER 21 1 Wärtsilä Q3/1 Highlights Order intake EUR 1,4 million (+38%) Net sales EUR 1,39 million (-11%) Operating

Benchmarking Travel & Tourism in United Arab Emirates

Benchmarking Travel & Tourism in United Arab Emirates How does Travel & Tourism compare to other sectors? Summary of Findings, November 2013 Sponsored by: Outline Introduction... 3 UAE summary...... 8

Benchmarking Travel & Tourism in United Arab Emirates How does Travel & Tourism compare to other sectors? Summary of Findings, November 2013 Sponsored by: Outline Introduction... 3 UAE summary...... 8

SHIP RECYCLING CAPACITY DEVELOPMENT. The Ship Recycling International Symposium in Muroran June 15, 2010 Yasuo NAKAJO, Japan Marine Science Inc.

SHIP RECYCLING CAPACITY DEVELOPMENT The Ship Recycling International Symposium in Muroran June 15, 2010 Yasuo NAKAJO, Japan Marine Science Inc. ROLE OF THE SHIP RECYCLING IN THE GLOBAL MARITIME CLASTER

SHIP RECYCLING CAPACITY DEVELOPMENT The Ship Recycling International Symposium in Muroran June 15, 2010 Yasuo NAKAJO, Japan Marine Science Inc. ROLE OF THE SHIP RECYCLING IN THE GLOBAL MARITIME CLASTER

AerCap Holdings N.V. Aengus Kelly, CEO. January 2017

AerCap Holdings N.V. Aengus Kelly, CEO January 2017 Industry Update Looking Back PASSENGER TRAFFIC GROWTH Air traffic growth in 2016 remained robust, short-haul at 5.6% and long-haul at 6.4% 1 CHINA SLOWING

AerCap Holdings N.V. Aengus Kelly, CEO January 2017 Industry Update Looking Back PASSENGER TRAFFIC GROWTH Air traffic growth in 2016 remained robust, short-haul at 5.6% and long-haul at 6.4% 1 CHINA SLOWING

AerCap Holdings N.V. Keith Helming Chief Financial Officer. Wachovia Securities Equity Conference June 23, 2008

AerCap Holdings N.V. Keith Helming Chief Financial Officer Wachovia Securities Equity Conference June 23, 2008 Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates

AerCap Holdings N.V. Keith Helming Chief Financial Officer Wachovia Securities Equity Conference June 23, 2008 Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates

NORWEGIAN AIR SHUTTLE ASA QUARTERLY REPORT FIRST QUARTER 2004 [This document is a translation from the original Norwegian version]

![NORWEGIAN AIR SHUTTLE ASA QUARTERLY REPORT FIRST QUARTER 2004 [This document is a translation from the original Norwegian version]](/thumbs/87/95085804.jpg "NORWEGIAN AIR SHUTTLE ASA QUARTERLY REPORT FIRST QUARTER 2004 [This document is a translation from the original Norwegian version]") NORWEGIAN AIR SHUTTLE ASA QUARTERLY REPORT 2004 IN BRIEF At the start of 2003, Norwegian has become a pure low-fare airline. The Fokker F-50 operations have been terminated, and during the quarter the

NORWEGIAN AIR SHUTTLE ASA QUARTERLY REPORT 2004 IN BRIEF At the start of 2003, Norwegian has become a pure low-fare airline. The Fokker F-50 operations have been terminated, and during the quarter the

Challenges and Developments in Global Shipbuilding Industry

Challenges and Developments in Global Shipbuilding Industry -brief overview of the current situation- AgS Monitoring Shipbuilding Thorsten Ludwig, Heino Bade, Heiko Messerschmidt industriall Global Union

Challenges and Developments in Global Shipbuilding Industry -brief overview of the current situation- AgS Monitoring Shipbuilding Thorsten Ludwig, Heino Bade, Heiko Messerschmidt industriall Global Union

Republic of Turkey - Ministry of Economy,

Republic of Turkey - Ministry of Economy, 2012 0 SHIPBUILDING INDUSTRY Turkey is surrounded by sea on three sides, is a natural bridge between Asia and Europe. Turkey borders the Black Sea, the Mediterranean,

Republic of Turkey - Ministry of Economy, 2012 0 SHIPBUILDING INDUSTRY Turkey is surrounded by sea on three sides, is a natural bridge between Asia and Europe. Turkey borders the Black Sea, the Mediterranean,

Domestic, U.S. and Overseas Travel to Canada

Domestic, U.S. and Overseas Travel to Canada Short-Term Markets Outlook Second Quarter 2007 / Executive Summary Prepared for: The Canadian Tourism Commission (CTC) By: February 2007 www.canada.travel Background

Domestic, U.S. and Overseas Travel to Canada Short-Term Markets Outlook Second Quarter 2007 / Executive Summary Prepared for: The Canadian Tourism Commission (CTC) By: February 2007 www.canada.travel Background

Interim Report 6m 2014

August 11, 2014 Interim Report 6m 2014 Investors and Analysts Conference Call on August 11, 2014 Joachim Müller, CFO Latest ad-hoc release (August 4, 2014) Reduction of forecast, primarily due to a further

August 11, 2014 Interim Report 6m 2014 Investors and Analysts Conference Call on August 11, 2014 Joachim Müller, CFO Latest ad-hoc release (August 4, 2014) Reduction of forecast, primarily due to a further