Bombardier Business Aircraft Market Forecast leading the way

|

|

|

- Arthur Dean

- 5 years ago

- Views:

Transcription

1 Bombardier Business Aircraft Market Forecast leading the way

2 table of contents 03 Executive Summary 06 Historical Market Performance 09 Current Market Drivers 23 The Forecast 33 Conclusion 35 Sources Forward Looking Statement This presentation includes forward-looking statements. Forward-looking statements generally can be identified by the use of forwardlooking terminology such as may, will, expect, intend, estimate, anticipate, plan, foresee, believe or continue or the negatives of these terms or variations of them or similar terminology. By their nature, forwardlooking statements require Bombardier Inc. (the Corporation ) to make assumptions and are subject to important known and unknown risks and uncertainties, which may cause the Corporation s actual results in future periods to differ materially from forecasted results. While the Corporation considers its assumptions to be reasonable and appropriate based on current information available, there is a risk that they may not be accurate. For additional information with respect to the assumptions underlying the forward-looking statements made in this presentation, please refer to the respective sections of the Corporation s aerospace segment ( Aerospace ) and the Corporation s transportation segment ( Transportation ) in the F09 MD&A. Certain factors that could cause actual results to differ materially from those anticipated in the forward-looking statements, include risks associated with general economic conditions, risks associated with the Corporation s business environment (such as the financial condition of the airline industry, government policies and priorities and competition from other businesses), operational risks (such as regulatory risks and dependence on key personnel, risks associated with doing business with partners, risks involved with developing new products and services, warranty and casualty claim losses, legal risks from legal proceedings, risks relating to the Corporation s dependence on certain key customers and key suppliers, risks resulting from fixed-term commitments, human resource risk, and environmental risk), financing risks (such as risks resulting from reliance on government support, risks relating to financing support provided on behalf of certain customers, risks relating to liquidity and access to capital markets, risks relating to the terms of certain restrictive debt covenants and market risks (including currency, interest rate and commodity pricing risk). See the Risks and Uncertainties section in the F09 MD&A. Readers are cautioned that the foregoing list of factors that may affect future growth, results and performance is not exhaustive and undue reliance should not be placed on forward-looking statements. The forward-looking statements set forth herein reflect the Corporation s expectations as at the date of the F09 MD&A and are subject to change after such date. Unless otherwise required by applicable securities laws, the Corporation expressly disclaims any intention, and assumes no obligation to update or revise any forwardlooking statements, whether as a result of new information, future events or otherwise. All monetary amounts are expressed in 2009 U.S. dollars unless otherwise stated. Bombardier Business Aircraft Market Forecast

3 executive summary Bombardier Business Aircraft Market Forecast

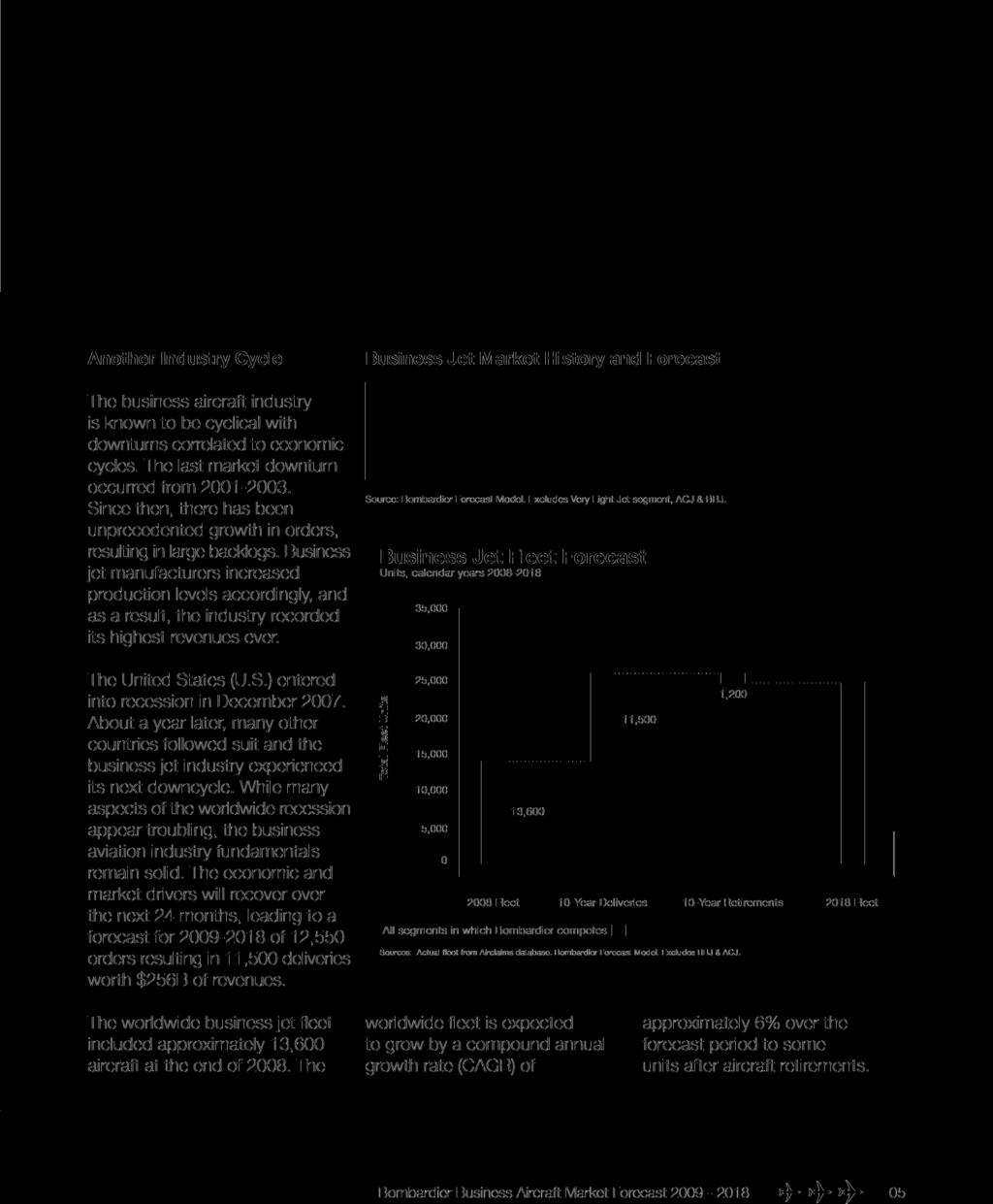

4 executive summary The Bombardier Aerospace Business Aircraft Market Forecast reflects Bombardier s view of the business jet industry s future. In the current turbulent economic times, there is significant focus on the challenges facing this industry. Bombardier remains confident that there is strong potential for the business jet industry over the next 10 years. With a strong product portfolio, dedication to customer satisfaction and product development, Bombardier is well positioned to benefit from the expected growth in the business jet industry over the next decade and to maintain and grow our leadership position. New for the 2009 Forecast The forecast focuses on the three categories in which Bombardier competes; light, midsize and large. The very light jet segment is not included unless specifically mentioned. (See new market segmentation on p.30). This year s forecast provides a detailed breakdown of the international markets and takes account of new market drivers such as innovation, as measured by the Herfindahl-Hirschman Index. Industry Orders and Delivery Units Calendar years, Order and Delivery Units 2,000 1,800 1,600 1,400 1,200 1, Total Orders Total Deliveries Sources: Actual deliveries from GAMA. Orders estimated from competitive intelligence, OEM guidance. Excludes Very Light Jet segment, ACJ and BBJ. Bombardier Business Aircraft Market Forecast

5 2 3, , 8 0 0

6 historical market performance Bombardier Business Aircraft Market Forecast

7 historical market performance Throughout history, the business jet market has proven to be highly cyclical. Over the past 40 years, the industry has been defined by multiple up and down cycles. From 1965 to 1995, the CAGR for industry deliveries was 4%, with most of the growth coming from its main market, the United States. After 1995, the business jet industry began expanding to other regions of the world, generating much higher growth, 12% on average. The following section describes the last historical business cycles since The Downturn Historical Business Jet Market Deliveries Units, calendar years CAGR = 4% CAGR = 12% Source: Actual deliveries from GAMA. Very Light Jets include CJ1+, CJ2+, Mustang, Phenom 100, Premier I and Eclipse 500. Excludes ACJ & BBJ The downturn was caused by various factors. The high percentage of aircraft for sale on the pre-owned market at the end of the 1990s was the first sign of a market slowdown. In the U.S., conjectural factors like the slowdown of the economy and the fall of corporate profits at the end of 2000 and in 2001 considerably reduced the demand for business jets. Business aviation suffered, to a lesser extent than commercial aviation, from the climate of uncertainty that followed 9/11. The reduction in the overall number of gross business jet orders, coupled with massive cancellations from both traditional and fractional jet businesses, forced Original Equipment Manufacturers (OEMs) to sharply reduce aircraft production. Bombardier Business Aircraft Market Forecast

8 historical market performance The Growth Period The U.S. economy regained its momentum and the demand for business jets significantly rose between 2004 and Young markets such as Western Europe and previously untapped markets in Eastern Europe, Asia and the Middle East began to generate substantial demand. Moreover, OEMs launched many new models during this period, pushing orders even higher. The industry s 842-unit delivery record set in 2007 was shattered in 2008, with deliveries totalling 927 units for the year. Record sales as well as a shift in consumer interest toward larger aircraft explain the 2008 peak of $19.8 billion in industry revenues. Since Q The year was a turning point for the business aircraft industry. The U.S. went into recession in December Orders in the U.S. are since down and the level of pre-owned aircraft for sale increased sharply. During the first nine months of 2008, the Historical Business Jet Market Revenues US$B, calendar years Revenue ($US Billion) Sources: Revenues estimated from GAMA and B&CA list prices. business aircraft market continued its expansion, driven by the vigour of international sales. The collapse of the financial markets in the third quarter of 2008 precipitated a sharp downturn in business aviation. Order activity stalled in the fourth quarter. The level of preowned aircraft for sale remained unusually high and residual values took a significant hit. Moreover, All segments in which Bombardier competes OEMs juggled with cancellations and deferrals. These unfavourable market conditions forced all major OEMs to decrease their production plans for 2009 and At the time of publication, order activity remained low, even though encouraging signs on the pre-owned market suggest the situation should slowly improve towards the end of Bombardier Business Aircraft Market Forecast

9 current market drivers Bombardier Business Aircraft Market Forecast

10 current market drivers The Bombardier Aerospace Business Aircraft Market Forecast is derived from an econometric model based on several market drivers. Economic Market Drivers Global Economy The state of the world economy, and that of individual countries, is a key factor in the demand for air travel. During 2008 and into 2009, the worldwide economy experienced a sharp downturn. The current recession is the result of a major financial crisis, primarily due to the collapse of mortgagebacked securities originating in the U.S. The U.S. real GDP shrank at an annual rate of over 6% in the fourth quarter of 2008 and in the first quarter of According to IHS Global Insight, world real GDP growth is forecast to shrink by 2.6% during 2009 and then resume growing by In the longer term, the world real GDP growth is expected to stabilize on average at 3.5% per year. The significant economic Prospect for World GDP Growth World real GDP growth forecast (percent change), % 4% 3% 2% 1% Actuals downturn of has resulted in a major short-term reduction in the demand for business jets. In the longer term, resumption of global economic growth will result in an expected strong recovery in the demand for business jets. The strong fundamentals of the business jet industry are expected to remain unchanged. Forecast 0% -1% -2% -3% Source: IHS Global Insight, May Bombardier Business Aircraft Market Forecast

index is an aggregate stock market index, based on representative securities listed in major financial centres around the world.")

11 economic market drivers Wealth Creation Worldwide demand for business jets is highly correlated with wealth creation which, in turn, is largely driven by economic growth. The Morgan Stanley Capital International (MSCI) index is an aggregate stock market index, based on representative securities listed in major financial centres around the world. By its nature, the MSCI index is a good estimate of wealth creation. As displayed in the following chart, world business jet orders have been highly correlated with the MSCI World index over the past 10 years. World Business Jet Orders and the MSCI World Index Orders (units), MSCI value, calendar years, ,000 2,500 Business Jet Orders 1,500 1,000 2,000 1,500 1,000 MSCI World Index U.S. Orderrs Rest of the World Orders Europe Orders MSCI World Index Sources: Orders estimated from competitive intelligence, OEM guidance. Excludes Very Light Jet segment, ACJ & BBJ. MSCI World Index from MSCI-Barra. Bombardier Business Aircraft Market Forecast

12 economic market drivers From 2002 to 2007, the MSCI World index doubled, mainly driven by the growing prices for oil, natural resources and commodities. In 2008, most of the gains of the past years were lost as the MSCI World index fell 42%. Some regions of the world experienced more acute variations; in China and India, the MSCI Index grew by a factor of 6 and 7 respectively between 2002 and 2007, before being impacted by the economic downturn. The China and India MSCI Index fell by 52% and 65% respectively from 2007 to MSCI Index Evolution by Region 2002 = 100, Calendar years, (base) (at peak) North America Europe Latin America Russia India China Rest of Asia & Oceania Middle East and Africa* World Source: MSCI World Index, MSCI-Barra. *Data from Middle East excluded as it was not available before Bombardier Business Aircraft Market Forecast

13 economic market drivers High Net Worth Individuals Last year, Merrill Lynch and Cap Gemini estimated in their 2008 World Wealth Report that the population of High Net Worth Individuals (HNWI) (i.e., people with financial assets of $1 million or more) grew by 22.7% in India to 123,000 and by 20.3% in China to 415,000 during In 2008, HNWI accounted for 10% to 20% of business aircraft sales, and are therefore a target market. At the time of publication, the 2009 Merrill Lynch and Cap Gemini report was not available. In March 2009, Forbes released its list of world billionaires. 70% of billionaires are located in North America and Europe. This study highlighted a 30% decrease in the number of world billionaires between 2008 and Number of Billionaires Unit Number of Billionaires Source: Forbes.com North America 173 Europe 74 Asia 45 Middle East & Africa 38 Russia & CIS 30 Latin America 28 China 24 India Bombardier Business Aircraft Market Forecast

14 business jet market drivers Business Jet Perceptions Business jet usage suffered from considerable negative media coverage during late 2008 and into 2009, particularly in the United States. Much of the negative media was associated with companies applying for financial assistance from the U.S. Government. The resulting high profile media coverage masked the fact that for the vast majority of owners and users, business jets are vital assets for increasing company productivity and competitiveness. Business jets are as much a productivity tool as smartphones and laptop computers. Business jets enable employees and executives to travel to remote destinations and medium size cities, while saving considerable time and improving productivity. The business aviation industry, led by the National Business Aviation Association (NBAA), the General Aviation Manufacturers Association (GAMA) and the OEMs, have responded vigorously with structured campaigns aimed at increasing the visibility of the true facts regarding business aviation. According to GAMA, in the U.S. alone, business aviation activities stimulate the economy by providing 1.2 million jobs and generating $150 billion annually. Bombardier Business Aircraft Market Forecast

15 business jet market drivers A business case created by Bombardier for a Midwestern U.S. firm showed that use of a super midsize business jet saved 20% of management s total time, when compared with the scheduled airline alternative. Business Travel Time Comparison Management, Man-hours (hrs) Man-hours (hrs) 30,000 25,000 20,000 15,000 10,000 5,000 26,000 hrs total 5,300 (20%) 4,200 (16%) 16,500 (64%) 9,500 hrs In addition to the time savings and productivity benefits of using a business jet, there are other less quantifiable but equally important benefits. These include on-demand flight schedules, the ability to conduct business Delta hours spent if traveling commercial Hours spent traveling (business jet) Regular working man-hours conversations in private during flights, access to more airports located closer to final destination, (which may not be served by a scheduled airline), and reduced stress on the company s travelers. Bombardier believes that unwarranted negative perceptions regarding business jets (in certain regions) will no longer be an issue once the market fully re-assesses the positive benefits offered by business aviation. The Forecast accounts for the impact of this short-term issue through its effect on sales of new and used aircraft throughout Management's time Source: Bombardier Analysis. Bombardier Business Aircraft Market Forecast

16 business jet market drivers Backlogs The term backlog refers to the total number of orders not yet delivered. In the business aircraft industry, the order backlog indicates potential deliveries for upcoming years. OEMs adjust their production rates based on their current backlog levels and their expectations regarding the number of net orders they can obtain in the future. Production rate changes are a costly and complex matter, due to the expenses associated with hiring or laying-off employees as well as changes to the supply chain and scheduling. Therefore, manufacturers aim to regulate their production rates to maximize deliveries while minimizing the risk of frequent production rate changes. Business Jet Orders Estimated units, calendar years Order Units 2,000 1,500 1, Sources: Orders/units prices estimated from competitive intelligence, OEM guidance. Excludes Very Light Jet segment, ACJ & BBJ. Industry Backlog Estimated units, calendar years ,000 2,500 All segments in which Bombardier competes 2,000 1,500 1, Sources: Orders estimated from competitive intelligence, OEM guidance. Excludes Very Light Jet Segment, ACJ & BBJ. Bombardier Business Aircraft Market Forecast

.")

17 business jet market drivers In terms of business jet industry orders, 2007 was a record year with close to 1,800 orders for the light, medium and large aircraft categories. The first half of 2008 remained strong as manufacturers recorded a large number of orders (1,375). However, in the second half of the year, the economic downturn led to an abrupt drop in orders and a significant number of cancellations. In general, the light aircraft category was most affected by cancellations. It is also the category that experienced the most important changes to production rates. The medium aircraft category was less affected, but still endured decreased production rates. The large aircraft category was only slightly affected. In dollar terms, the industry backlog in the first quarter of 2009 was estimated at approximately $69.7 billion, down from a peak of $77.8 billion in the third quarter of Taking into account the soft order activity experienced to date in 2009, as well as the estimated level of aircraft cancellations and deferrals, the industry backlog is expected to continue shrinking in the short term. Industry Backlog Estimated Value ($U.S. Billion) Q $69.7 B $13.0 B $16.6 B $40.1 B Large Medium Light Sources: Orders estimated from competitive intelligence, OEM guidance. List price from BC&A. Excludes Very Light Jet segment, ACJ & BBJ. Bombardier Business Aircraft Market Forecast

18 business jet market drivers The Pre-owned Market Over 60% of new business jet orders are replacement aircraft for current owners. The demand for new aircraft is stimulated by the conditions prevailing on the preowned market. The pre-owned market is considered healthy when residual values are high and when the inventory of preowned aircraft for sale is low. As of early 2008, the percentage of the overall business jet fleet for sale on the pre-owned market began to increase rapidly. Many aircraft owners either experienced difficulty or failed to sell their pre-owned aircraft, which, in turn, made them less likely to purchase replacement aircraft. The growing number of aircraft on the pre-owned market is a leading indicator of the business Pre-Owned Aircraft Inventory as a % of the Fleet %, calendar years 1999 Q aircraft market downturn that started in the fourth quarter of Between 2002 and 2007 the pre-owned aircraft inventory, as a percentage of the fleet, decreased from 15.7% to 10.4%. From early 2008 to the first quarter of 2009, the level rose from 16.1% to 17.4%. This increase was significant, especially in the second half of the year, when manufacturers new order intake levels slowed dramatically. Looking forward, Bombardier expects the level of pre-owned inventory to start declining in 2010 and return to historical levels of 10% - 13%. 12.8% 15.7% 15.7% 14.1% 13.0% 16.1% 17.4% 9.9% 10.9% 11.0% 10.4% Q1-09 Sources: Aircraft Inventory and fleet from JETNET. Excludes Very Light Jet segment. Bombardier Business Aircraft Market Forecast

19 business jet market drivers New Aircraft Programs When compared to older aircraft models, new models tend to offer more cabin volume, increased range and better performance for a comparable price. The launch of new aircraft programs reflects OEMs confidence in the market going forward as manufacturers expect sustained deliveries in the first years after entry into service. The required investments in design, development and technology as well as market timing are crucial to the success of business aircraft programs. New aircraft programs can either be derivative or clean-sheet designs. A derivative is a new aircraft based on an existing design that has been upgraded, whereas a clean-sheet design is a brand new conceptualized Entry Into Service of New Programs Entry into service by model, calendar years Falcon 2000LX Lineage 1000 Phenom CJ4 Falcon 900LX Hawker 450XP Premier II* Sources: Dates of entry from competitors' press releases and trade media coverage. *Very Light Jets. aircraft. There are significantly higher costs involved in designing, building and certifying a cleansheet design aircraft compared to modifying an existing platform. Therefore, the trend has been for manufacturers to plan aircraft families based on platforms from which derivatives of the clean-sheet design allow for a distribution of the design costs over more than one model G250 Honda Jet* G650 Global Vision Legacy Learjet 85 Legacy 450 Several clean-sheet and derivative business jet programs were launched during the last up-cycle and are now approaching entry into service. In 2009, three new aircraft programs are expected to enter into service and generate a significant number of deliveries during the next years. Bombardier Business Aircraft Market Forecast

was adapted to quantify the level of competition and innovation in the industry.")

20 business jet market drivers The number of models in service plays a role on the total market demand. The Herfindahl- Hirschman Index (HHI) was adapted to quantify the level of competition and innovation in the industry. The HHI measures competitiveness in a particular market by taking the sum of the squares of the market shares of all aircraft models, resulting in a score between 0% and 100%. A score of 0% represents a market with pure competition, while a score of 100% represents a monopolistic market. When applying the HHI to the business aircraft market, all aircraft are assumed to be competing in the same market. Over the past 40 years, the increased level of competition in the business aircraft industry led to the development of a significant number of aircraft models, driving an increasing level of orders. As a result, the HHI has been decreasing over the last 40 years. Herfindahl Hirschman Index (HHI) %, % 20% 15% 10% 5% 0% Source: Bombardier analysis Named after economists Orris C. Herfindahl and Albert O. Hirschman, HHI is an economic concept often used in competition law and antitrust proceedings. The U.S. Department of Justice uses it to evaluate competition in different markets Bombardier Business Aircraft Market Forecast

21 business jet market drivers Fractional and Branded Charter Demand Fractional ownership (where several owners own a fraction of a given aircraft) has existed since the mid-1990 s and has accounted for, on average, 14% of industry deliveries over the last 10 years. Subsequent variations include fractional card or jet card programs where customers can access on-demand use of a business jet by committing to a certain number of hours of usage per year but without the obligation to purchase shares in an aircraft. Air Travel Options Commercial-aviation offering Business jet market On-demand service Business jet ownership Full ownership Fractional ownership Jet-card programs Low cost airlines Commercial airlines First-class commercial airlines Air Taxis Branded Charters Personalized service Source: Bombardier. Bombardier Business Aircraft Market Forecast

22 business jet market drivers The emergence of charter and branded charter operators is a recent trend. These operators offer on-demand and tailored services with identifiable, competitive trip-specific pricing, and no obligation to purchase shares in an aircraft. Branded charter operators are characterized by volume purchases of a fleet of aircraft, sophisticated operations infrastructure, and a greater use of airline-style scheduling practices in order to minimize deadhead costs. In 2008, branded charter operator orders represented approximately 20% to 30% of total business jet orders. Multiple volume orders from both fractional and branded charter operators have helped increase industry orders in recent years. Over the next 10 years, the forecast projects that approximately 15% to 20% of industry orders are expected to come from fractional and branded charter operators. Delivery Units Business Jet Fractional Delivery Units Units and share (%) of total deliveries, calendar years, % % Deliveries 16% % 95 Share of Total 18% % 57 19% 93 18% 17% % 15% % 15% 10% 5% 0% Market share (%) Source: Airclaims database. Excludes Very Light Jet Segment, ACJ & BBJ. Bombardier Business Aircraft Market Forecast

23 the forecast Bombardier Business Aircraft Market Forecast

24 the forecast Orders, Deliveries and Revenues As the economy recovers from the current downturn, orders for business aircraft will increase, which should sustain deliveries of new business jets over the next 10 years. The sharp contraction of the U.S. economy and ensuing worldwide recession during is expected to cause a significant reduction in the near term demand for business jets. Many OEMs have and will likely continue to record negative orders in early 2009 due to a significant number of cancellations. Order intake is forecast to reach a low of 375 units in 2009 and is expected to improve by the end of the year, reaching 2008 levels of approximately 1,400 units per year by Business Jet Industry 10-Year Orders Outlook Orders (units), calendar years, ,500 Total excl. VLJs: 8,700 Units Total excl. VLJs: 12,550 Units 2,000 1,500 1, All segments in which Bombardier competes Very Light Jet segment Source: Bombardier Forecasting Model. Very Light Jets include CJ1+, CJ2+, Mustang, Premier I, Phenom 100 and Eclipse 500. Excludes ACJ & BBJ. Bombardier Business Aircraft Market Forecast

25 the forecast The delivery forecast shows demand for 11,500 aircraft that will generate $256 billion in total revenue in the light to large aircraft categories over the period, compared to 6,500 aircraft and $122 billion in total revenue between 1999 and Industry deliveries are expected to recover from a low of 650 deliveries per year in , gradually increasing to approximately 1,400 industry deliveries per year by the end of the forecast period in Existing backlogs heading into the downturn of will result in near term higher deliveries compared to orders. Business Jet Industry 10-Year Deliveries Outlook Deliveries (units), calendar years, ,500 Total excl. VLJs: 6,500 Units Total excl. VLJs: 11,500 Units 2,000 1,500 1, All segments in which Bombardier competes Very Light Jet segment Source: Bombardier Forecasting Model. Very Light Jets include CJ1+, CJ2+, Mustang, Premier I, Phenom 100 and Eclipse 500. Excludes ACJ & BBJ. Bombardier Business Aircraft Market Forecast

26 regional details The Forecast is grouped into three geographic regions: North America, Europe and the Rest of the World. Orders from each region are driven by the previously mentioned economic and market drivers. The North American Market (United States and Canada) Business aviation started in North America in the 1960s. The region has always been the most important in terms of business jet sales. The North American business jet installed base was 9,400 aircraft at the end of 2008, or approximately 70% of the worldwide business jet installed base. The well developed infrastructure in North America can accommodate a continuously renewing demand of business aircraft. Business aviation also has strong roots in North America, from manufacturing to servicing and maintenance. In 2008, approximately 75% of business jets delivered were assembled in North America. The recession that began in the U.S. in December 2007 has significantly affected demand. The business jet market slowdown started in early Other regions followed the downward spiral as of the fourth quarter of The negative press associated with business jet usage among U.S. corporations has also contributed to the record preowned inventory levels and the unusual number of cancellations. The U.S. is expected to be among the first of the major economies to recover from the recession, with positive economic growth expected to return in late The expected recovery will be fueled by significant fiscal and monetary stimulus measures by the U.S. Government and increasing customer confidence. This should positively impact wealth creation. Bombardier Business Aircraft Market Forecast

27 regional details As the most dynamic and diversified economy around the world, the U.S. should continue to generate wealth and sustain the development of its business aircraft industry in the long term. In May 2009, Moody s decided to maintain the credit rating of the U.S. because it has a diverse and resilient economy, strong government institutions, high per-capita income, and a central position in the global economy. While Canadian financial institutions have proven to be stable throughout the recent crisis, Canada has experienced economic decline in 2009, although to a smaller extent when compared to the U.S. According to the latest IHS Global Insight forecast published in May 2009, both countries real GDP are expected to show positive growth in the first half of North America is forecast to receive the greatest number of business jet deliveries between 2009 and 2018 with 5,400 units. The 2008 fleet of 9,400 business jets will grow to 14,100 aircraft in 2018, resulting in a CAGR of approximately 4%. Europe In recent years, Europe has emerged as a strong market for business jet orders. Buoyed by the strong Euro relative to the U.S. dollar strong economic growth generated by the expanding European Union and the emergence of branded charter business jet operators, Europe accounted for an estimated 34% of worldwide business jet orders in 2008; compared with 29% for North America. The Euro-area economy entered into recession approximately one year later than the U.S. The GDP is expected to decline by 4.3% in 2009, however orders are expected to recover once economic growth resumes, which should occur within 12 months after the U.S. The growing European business jet installed base will create a significant replacement market in coming years, ensuring that this region will continue to be a major source of demand for business aircraft. Europe will receive the second largest number of business jet deliveries with over 3,000 units in the period from 2009 to The 2008 fleet of 1,700 business jets will grow to 4,500 aircraft by 2018 with a fleet growth CAGR of approximately 10%. Bombardier Business Aircraft Market Forecast

, and Asia and Australasia. There is significant discussion regarding the potential for China and India to become larger markets in the business aircraft industry.")

28 regional details The Rest of the World The forecast region containing the Rest of the World includes Latin America, the Middle East and Africa, Russia and the Commonwealth of Independent States (CIS), and Asia and Australasia. There is significant discussion regarding the potential for China and India to become larger markets in the business aircraft industry. As a result, they have been treated separately from Asia and Australasia. Combined, the Rest of the World regions have continued to experience economic growth through the current downturn, however growth has slowed versus recent years. As discussed in the MSCI section, stock markets in regions like Russia, India or China have been tremendously devaluated in This wealth destruction will likely prevent these regions from providing significant demand for business jets in the next 24 months. However, over the next 10 years, we believe the Rest of the World business jet installed base will Business Jet 10 Year Outlook Units & %, calendar years, Source: Bombardier Forecasting Model. Excludes Very Light Jet, ACJ & BBJ. Fleet from CASE. grow by an impressive 8% per year on average. The Middle East and Africa, Latin America and Russia and the CIS will represent almost two-thirds of the deliveries to the rest of the world due to their solid interest for business jets, their aviation infrastructures and the strong potential of their oil and natural resources driven economies. To date, there have been few orders from China and India, however there is enormous Fleet Fleet Fleet CAGR Orders Deliveries (2008) (2018) ( ) ( ) ( ) North America 9,400 14, % 5,900 5,400 Europe 1,700 4, % 3,200 3,040 Latin America 1,160 1, % Middle East & Africa 530 1, % Russia & CIS % China % India % Asia & Australasia % (excl. China & India) potential for these countries once certain infrastructure and regulatory obstacles are removed. Over the 10-year period, China and India are expected to have the highest CAGR (respectively 16% and 14%) due to their relatively small current fleet and their huge potential for growth. The fleet in the Rest of the World was approximately 2,400 aircraft at the end of We forecast additional deliveries of 3,100 units over the next 10 years. Bombardier Business Aircraft Market Forecast

29 regional details Regional 10 Year Deliveries Outlook Units, calendar years, Source: Bombardier Forecasting Model. Excludes Very Light Jet, ACJ & BBJ. Bombardier Business Aircraft Market Forecast

30 segment details The following segmentation helps to differentiate the various aircraft offered on the business jet market. It is based on a combination of price and performance specifications, primarily cabin volume, speed, range and takeoff field length. Light Category The light aircraft category encompasses light to midsize aircraft segments. When compared to other business jet market categories, the light category value proposition relies on relatively low prices and low operating costs combined with sufficient range for short-haul missions. The Learjet 40 XR, the Learjet 45 XR, the Learjet 60 XR and the in-development Learjet 85 aircraft are all part of this category. The Learjet 85 aircraft has been reaching all its development milestones, and Bombardier is committed to its entry into service in Business Jet Market Segmentation Bombardier Cessna Dassault Gulfstream Hawker Beechcraft Embraer Others Very Light Jet Mustang CJ1+ CJ2+ Premier 1A/II Phenom 100 HondaJet Light Jet CJ3 CJ4 Encore+ Super Light Jet Source: Bombardier s internal research department. *Segmentation is largely determined by a combination of cabin volume, range and price. The light aircraft category is expected to take the longest time to recover after the downturn due to the large number of aircraft (18.1% of fleet) for sale in the first quarter of 2009 on the pre-owned LIGHT JETS MEDIUM JETS LARGE JETS Midsize Jet L40XR L45XR L60XR H400XP/ 450XP Phenom 300 SJ30-2 XLS+ H750 Legacy 450 L85 Sovereign Super Midsize Jet F2000DX F900DX F7X F2000EX/ F900EX/ LX LX G150 G200 G350 G450 G500 G250 G550 H850XP H900XP Legacy 500 Legacy 600 Large Jet CL-850 Super Large Jet Lineage 1000 Ultra Long-Range Jet CL-300 CL-605 G5000 GEX-XRS CX H In production 13 In development G650 market. We expect the light category to generate a total of 6,000 deliveries over the next 10 years, representing $69 billion. Bombardier Business Aircraft Market Forecast

31 segment details Midsize Category The midsize category features the super midsize and large segments. The midsize category value proposition relies on enhanced cabin comfort and superior range versus the light category. It is the category of business jets often preferred by corporations. Bombardier successfully developed the midsize category with the Challenger 600 series. Bombardier has 3 strong products in the midsize category: the Challenger 300, the Challenger 605 and the Challenger 850 jets. The midsize aircraft category is expected to recover more quickly than the light category as there are fewer pre-owned aircraft for sale (16.5% of fleet). The midsize category is expected to account for a total of 2,700 deliveries over the next 10 years, representing $67 billion in revenue. Business Jet Forecast by Segment Delivery units, avg. revenue per unit, total market revenue (US$B), constant 2008 $, calendar years Total Delivery Units 5,000 4,000 3,000 2,000 1, $38B Light/ Super Light LEARJET CHALLENGER GLOBAL $31B Midsize Super Midsize $32B $35B Large Super Large $41B Ultra Long-Range $79B Forecast Average Revenue per Unit (In Billion USD) Sources: Bombardier analysis. Revenues estimated from GAMA and B&CA list prices. Bombardier Business Aircraft Market Forecast

32 segment details Large Category The large category features the super large and ultra long-range segments. The large category aircraft offer the most capabilities in terms of range, speed, and cabin comfort. With the Global 5000 and the Global Express XRS, Bombardier has the most advanced product line in the industry for this market category. Both aircraft will feature the new Global Vision flight deck, which pairs the latest technological advancements in avionics with enhanced and synthetic vision systems to provide pilots with an unprecedented level of situational awareness. It is on schedule for first flight in summer The large category is expected to expand faster than the other categories. The recent shift in demand towards more international customers has driven sales of larger aircraft. Contrary to U.S. customers, who generally enter the market from the bottom and then trade up, most international customers purchase their first aircraft within the large category. Customers in the large aircraft category are more willing to pay for additional comfort and technology than they were in the past. Although no category will come out of the downturn unaffected, we expect deliveries in the large category to expand the most rapidly after the downturn. Total deliveries are forecast to be 2,800 units for a value of $120 billion. A Note on the Very Light Jet Segment The very light jet segment differs from the rest of business aviation in that the majority of purchasers are owner-operators. Although the very light jet segment could become the largest segment in terms of unit deliveries with an average of 320 deliveries per year forecast between 2009 and 2018, it represents a comparatively small portion of industry revenues. The very light jet segment has been significantly weakened by the economic downturn. The future of this segment will depend on the capacity of the many manufacturers entering this market to deliver on their plans as well as on the questionable success of Air Taxi business models. Bombardier Business Aircraft Market Forecast

33 conclusion Bombardier Business Aircraft Market Forecast

34 conclusion In a Few Words The cyclical nature of the business jet industry can easily lead to pessimistic views which generally subside once the market recovers. OEMs face a tough short-term period due to the lack of available credit, numerous order cancellations and reduction of production rates. However, future perspectives remain solid. We strongly believe that the current industry challenges such as negative perceptions and the high level of pre-owned aircraft inventory will fade in the shortterm. Medium to long-term growth in the industry will be fuelled by manufacturers continuing to design and market new aircraft to drive value to customers. In particular, we expect significant demand to come from U.S. customers replacing their current aircraft and international customers from regions such as the Middle East & Africa, Latin America, and Eastern Europe entering the market. Business jets will be used by corporations as globalization trends continue to increase in the future. The business jet market should continue to experience strong growth over the period, with 12,550 orders yielding deliveries of 11,500 aircraft, worth $256 billion of revenues. The large aircraft market category is expected to expand faster than the other categories. The manpower needed to manufacture these aircraft and the revenues associated with them will create significant economic value. Leading the way The business aircraft industry will likely face new challenges going forward. As fuel prices and environmental concerns rise, the green wave is expected to modify customers actions and perceptions in the future. Bombardier is being proactive to address environmental concerns through corporate social responsibility initiatives, such as being the first OEM to offer business aircraft customers a fully managed carbon-offset program to offset their aircraft s average carbon emissions. OEMs may have to contribute towards developing worldwide infrastructure to support the regional development of business aviation. Bombardier is ready to address the new challenges on the horizon so that the industry can continue to flourish in the long-run. Bombardier Business Aircraft Market Forecast

35 sources Bombardier Business Aircraft Market Forecast

36 sources Resources used in the Bombardier Aerospace Business Aircraft Market Forecast: Airclaims database Aircraft Bluebook Price Digest AMSTAT B&CA Business & Commercial Aviation Magazine Blue Chip Economic Forecast, May 2009 EIU Economist Intelligence Unit Eurocontrol Eurostat FAA ETMSC Flight International Magazine Forbes.com GAMA General Aviation Manufacturers Association IHS Global Insight JETNET database JP Morgan Business Jet Monthly, April 2009 Merrill Lynch and Cap Gemini 2008 World Wealth Report Merrill Lynch Bizjet Flight Plan, April 2009 Merrill Lynch Market Economist, April 2009 MSCI-Barra NBAA National Business Aircraft Association NBER National Bureau of Economic Research OEMs financial reports, websites and press releases UBS Business Jet Monthly, April 2009 U.S. Bureau of Economic Analysis U.S. Bureau of Labor Statistics Weekly of Business Aviation For electronic copies of the Bombardier Aerospace Business Aircraft Market Forecast visit the company s website at Bombardier Business Aircraft Market Forecast

MARKET FORECAST BOMBARDIER COMMERCIAL AIRCRAFT COMMERCIALAIRCRAFT.BOMBARDIER.COM BOMBARDIER COMMERCIAL AIRCRAFT MARKET FORECAST

MARKET FORECAST 2015-2034 BOMBARDIER COMMERCIAL AIRCRAFT COMMERCIALAIRCRAFT.BOMBARDIER.COM BOMBARDIER COMMERCIAL AIRCRAFT MARKET FORECAST 2015-2034 FORWARD-LOOKING STATEMENTS This presentation includes

MARKET FORECAST 2015-2034 BOMBARDIER COMMERCIAL AIRCRAFT COMMERCIALAIRCRAFT.BOMBARDIER.COM BOMBARDIER COMMERCIAL AIRCRAFT MARKET FORECAST 2015-2034 FORWARD-LOOKING STATEMENTS This presentation includes

BUSINESS AVIATION MARKET OUTLOOK

BUSINESS AVIATION MARKET OUTLOOK Presented by: Michael Holland Manager mholland@icfi.com Aerospace Raw Materials Conference April 24, 2012 Pittsburgh, PA 0 Agenda Trends Driving Business Aviation Production

BUSINESS AVIATION MARKET OUTLOOK Presented by: Michael Holland Manager mholland@icfi.com Aerospace Raw Materials Conference April 24, 2012 Pittsburgh, PA 0 Agenda Trends Driving Business Aviation Production

NBAA 2015 MARKET UPDATE

NBAA 2015 MARKET UPDATE November 2015 Forward-Looking Statements 2 This report contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. All statements,

NBAA 2015 MARKET UPDATE November 2015 Forward-Looking Statements 2 This report contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. All statements,

2009 Business Aviation Outlook

2009 Business Aviation Outlook 23 rd Year of Survey, 18 th consecutive public report release 1,200 Corporate flight departments from around the world Aircraft Manufacturers and other sources 5 year purchase

2009 Business Aviation Outlook 23 rd Year of Survey, 18 th consecutive public report release 1,200 Corporate flight departments from around the world Aircraft Manufacturers and other sources 5 year purchase

2009 Business Aviation Outlook

2009 Business Aviation Outlook 2009 Business Aviation Outlook 23 st Year of Survey, 18 th consecutive public report release 1,200 Corporate flight departments from around the world Aircraft Manufacturers

2009 Business Aviation Outlook 2009 Business Aviation Outlook 23 st Year of Survey, 18 th consecutive public report release 1,200 Corporate flight departments from around the world Aircraft Manufacturers

EXECUTIVE AVIATION. MICHAEL AMALFITANO Embraer Executive Jets

EXECUTIVE AVIATION MICHAEL AMALFITANO Embraer Executive Jets 1 KEY MESSAGES Signs of growth ahead Focusing on value and customer experience Executing our growth plan 2 SIGNS OF GROWTH AHEAD Velocity of

EXECUTIVE AVIATION MICHAEL AMALFITANO Embraer Executive Jets 1 KEY MESSAGES Signs of growth ahead Focusing on value and customer experience Executing our growth plan 2 SIGNS OF GROWTH AHEAD Velocity of

When is the business aviation upturn coming and what role does the Mediterranean market play?

AEROSPACE INFORMATION REDEFINED When is the business aviation upturn coming and what role does the Mediterranean market play? Mediterranean Business Aviation 13 th September 2013 Daniel Hall Ascend Advisory

AEROSPACE INFORMATION REDEFINED When is the business aviation upturn coming and what role does the Mediterranean market play? Mediterranean Business Aviation 13 th September 2013 Daniel Hall Ascend Advisory

IATA ECONOMIC BRIEFING DECEMBER 2008

ECONOMIC BRIEFING DECEMBER 28 THE IMPACT OF RECESSION ON AIR TRAFFIC VOLUMES Recession is now forecast for North America, Europe and Japan late this year and into 29. The last major downturn in air traffic,

ECONOMIC BRIEFING DECEMBER 28 THE IMPACT OF RECESSION ON AIR TRAFFIC VOLUMES Recession is now forecast for North America, Europe and Japan late this year and into 29. The last major downturn in air traffic,

NBAA 2014 Business Aviation Market Update. October 2014

NBAA 2014 Business Aviation Market Update October 2014 1 Jefferies Global Industrials Conference - August 14, 2014 Forward Looking Statements This report contains forward-looking statements within the

NBAA 2014 Business Aviation Market Update October 2014 1 Jefferies Global Industrials Conference - August 14, 2014 Forward Looking Statements This report contains forward-looking statements within the

2017 Recap. Market Temperature. Piston Singles The single engine piston

2018 Volume 1 The Quarterly Newsletter of Vref For Those Who Demand Accuracy, And Know the Difference! 2017 Recap Activity levels are up, and inventories are dropping. This is definitely a different market

2018 Volume 1 The Quarterly Newsletter of Vref For Those Who Demand Accuracy, And Know the Difference! 2017 Recap Activity levels are up, and inventories are dropping. This is definitely a different market

AIR CANADA REPORTS 2010 THIRD QUARTER RESULTS; Operating Income improved $259 million or 381 per cent from previous year s quarter

AIR CANADA REPORTS 2010 THIRD QUARTER RESULTS; Operating Income improved $259 million or 381 per cent from previous year s quarter MONTRÉAL, November 4, 2010 Air Canada today reported operating income

AIR CANADA REPORTS 2010 THIRD QUARTER RESULTS; Operating Income improved $259 million or 381 per cent from previous year s quarter MONTRÉAL, November 4, 2010 Air Canada today reported operating income

TURBULENCE AHEAD DISENGAGE THE AUTOPILOT GLOBAL FLEET & MRO MARKET FORECAST

TURBULENCE AHEAD DISENGAGE THE AUTOPILOT 2015-2025 GLOBAL FLEET & MRO MARKET FORECAST Tuesday, October 13 th 2015 Christopher Doan Vice President Oliver Wyman acquired TeamSAI and integrated the business

TURBULENCE AHEAD DISENGAGE THE AUTOPILOT 2015-2025 GLOBAL FLEET & MRO MARKET FORECAST Tuesday, October 13 th 2015 Christopher Doan Vice President Oliver Wyman acquired TeamSAI and integrated the business

IATA ECONOMIC BRIEFING FEBRUARY 2007

IATA ECONOMIC BRIEFING FEBRUARY 27 NEW AIRCRAFT ORDERS KEY POINTS New aircraft orders remained very high in 26. The total of 1,834 new orders for Boeing and Airbus commercial planes was down slightly from

IATA ECONOMIC BRIEFING FEBRUARY 27 NEW AIRCRAFT ORDERS KEY POINTS New aircraft orders remained very high in 26. The total of 1,834 new orders for Boeing and Airbus commercial planes was down slightly from

AerCap Holdings N.V. Aengus Kelly, CEO. January 2017

AerCap Holdings N.V. Aengus Kelly, CEO January 2017 Industry Update Looking Back PASSENGER TRAFFIC GROWTH Air traffic growth in 2016 remained robust, short-haul at 5.6% and long-haul at 6.4% 1 CHINA SLOWING

AerCap Holdings N.V. Aengus Kelly, CEO January 2017 Industry Update Looking Back PASSENGER TRAFFIC GROWTH Air traffic growth in 2016 remained robust, short-haul at 5.6% and long-haul at 6.4% 1 CHINA SLOWING

Dubai Airshow 2013 Business Aviation Market Update

Dubai Airshow 2013 Business Aviation Market Update Rob Wilson, President, Business & General Aviation MEBAA General Assembly November, 2013 2013 Business Aviation Outlook 27th year of survey, 22nd public

Dubai Airshow 2013 Business Aviation Market Update Rob Wilson, President, Business & General Aviation MEBAA General Assembly November, 2013 2013 Business Aviation Outlook 27th year of survey, 22nd public

AIR CANADA REPORTS THIRD QUARTER RESULTS

AIR CANADA REPORTS THIRD QUARTER RESULTS THIRD QUARTER OVERVIEW Operating income of $112 million compared to operating income of $351 million in the third quarter of 2007. Fuel expense increased 49 per

AIR CANADA REPORTS THIRD QUARTER RESULTS THIRD QUARTER OVERVIEW Operating income of $112 million compared to operating income of $351 million in the third quarter of 2007. Fuel expense increased 49 per

Joe Randell President and Chief Executive Officer Jolene Mahody Executive Vice President and Chief Financial Officer

Joe Randell President and Chief Executive Officer Jolene Mahody Executive Vice President and Chief Financial Officer Nathalie Megann Vice President, Investor Relations and Corporate Affairs December, 2015

Joe Randell President and Chief Executive Officer Jolene Mahody Executive Vice President and Chief Financial Officer Nathalie Megann Vice President, Investor Relations and Corporate Affairs December, 2015

Quarterly Aviation Industry Performance

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance (March - June 17) Prepared by: Strategic Planning department 1 Quarterly

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance (March - June 17) Prepared by: Strategic Planning department 1 Quarterly

Business Aviation Providing Tools Not Toys

Business Aviation Providing Tools Not Toys Tool or Toy? Tool or Toy? Indefensible Indispensable Personal Toy Business Tool Tool or Toy? Privileged Pragmatic Social Buyer Sophisticated Buyer Tool or Toy?

Business Aviation Providing Tools Not Toys Tool or Toy? Tool or Toy? Indefensible Indispensable Personal Toy Business Tool Tool or Toy? Privileged Pragmatic Social Buyer Sophisticated Buyer Tool or Toy?

AIR CANADA REPORTS 2010 FIRST QUARTER RESULTS Operating loss narrows; revenue and traffic growth reflect strengthening economy

AIR CANADA REPORTS 2010 FIRST QUARTER RESULTS Operating loss narrows; revenue and traffic growth reflect strengthening economy MONTRÉAL, May 6, 2010 Air Canada today reported a reduced operating loss of

AIR CANADA REPORTS 2010 FIRST QUARTER RESULTS Operating loss narrows; revenue and traffic growth reflect strengthening economy MONTRÉAL, May 6, 2010 Air Canada today reported a reduced operating loss of

Airbus. Tom Enders Airbus. 15 & 16 December 2011

Airbus Tom Enders Airbus Global Investor Forum Global Investor Forum 15 & 16 December 2011 Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates,

Airbus Tom Enders Airbus Global Investor Forum Global Investor Forum 15 & 16 December 2011 Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates,

HONEYWELL AEROSPACE BUSINESS AVIATION OUTLOOK FORECASTS NEXT PERIOD OF INDUSTRY EXPANSION TO BEGIN BY 2012

News Release Media Contacts: Bill Reavis Perri Coyne 602-365-2055 602-436-5312 bill.reavis@honeywell.com perri.coyne@honeywell.com Honeywell Aerospace Media Center twitter.com/hon_perric HONEYWELL AEROSPACE

News Release Media Contacts: Bill Reavis Perri Coyne 602-365-2055 602-436-5312 bill.reavis@honeywell.com perri.coyne@honeywell.com Honeywell Aerospace Media Center twitter.com/hon_perric HONEYWELL AEROSPACE

CONTACT: Investor Relations Corporate Communications

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces Fourth Quarter 2017

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces Fourth Quarter 2017

CONTACT: Investor Relations Corporate Communications

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces Second Quarter 2017

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces Second Quarter 2017

AIR CANADA REPORTS FIRST QUARTER RESULTS

AIR CANADA REPORTS FIRST QUARTER RESULTS As a result of the deconsolidation of Jazz effective May 24, 2007, Air Canada s consolidated results for the first quarter of 2008 are not directly comparable to

AIR CANADA REPORTS FIRST QUARTER RESULTS As a result of the deconsolidation of Jazz effective May 24, 2007, Air Canada s consolidated results for the first quarter of 2008 are not directly comparable to

Industry Update. ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL

Industry Update ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL U.S. & Canadian GDP 8% 6% 4% U.S.* Canada** Estimate by BEA as of 02/11/16 2% 0% -2% -4% -6% -8% -10% The U.S. economy

Industry Update ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL U.S. & Canadian GDP 8% 6% 4% U.S.* Canada** Estimate by BEA as of 02/11/16 2% 0% -2% -4% -6% -8% -10% The U.S. economy

Thank you for participating in the financial results for fiscal 2014.

Thank you for participating in the financial results for fiscal 2014. ANA HOLDINGS strongly believes that safety is the most important principle of our air transportation business. The expansion of slots

Thank you for participating in the financial results for fiscal 2014. ANA HOLDINGS strongly believes that safety is the most important principle of our air transportation business. The expansion of slots

Examining the pre-owned large cabin business jet market in 2015

Examining the pre-owned large cabin business jet market in 2015 An insight for European financiers Report by: Jean Sémiramoth, Founding Partner, The Sharpwings jean.semiramoth@thesharpwings.com A contrasting

Examining the pre-owned large cabin business jet market in 2015 An insight for European financiers Report by: Jean Sémiramoth, Founding Partner, The Sharpwings jean.semiramoth@thesharpwings.com A contrasting

3. Aviation Activity Forecasts

3. Aviation Activity Forecasts This section presents forecasts of aviation activity for the Airport through 2029. Forecasts were developed for enplaned passengers, air carrier and regional/commuter airline

3. Aviation Activity Forecasts This section presents forecasts of aviation activity for the Airport through 2029. Forecasts were developed for enplaned passengers, air carrier and regional/commuter airline

CONTACT: Investor Relations Corporate Communications

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces Second Quarter 2016

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces Second Quarter 2016

Meeting the Demand The Battle for Asia Pacific s Airspace

Meeting the Demand The Battle for Asia Pacific s Airspace The statements contained herein are based on good faith assumptions and are to be used for general information purposes only. These statements

Meeting the Demand The Battle for Asia Pacific s Airspace The statements contained herein are based on good faith assumptions and are to be used for general information purposes only. These statements

VLJs Panel: What is the European Business Model?

VLJs Panel: What is the European Business Model? Phenom 100 and the European market May 24 th, 2007 Marco Túlio Pellegrini VP, Market Intelligence Forward Looking Statement This presentation includes forward-looking

VLJs Panel: What is the European Business Model? Phenom 100 and the European market May 24 th, 2007 Marco Túlio Pellegrini VP, Market Intelligence Forward Looking Statement This presentation includes forward-looking

Outlook and Opportunities in Corporate Aircraft

Outlook and Opportunities in Corporate Aircraft Don Gies Vice President & Group Manager Business Aviation Finance Presented to the ELA Large Ticket Conference April 25, 2006 Outlook and Opportunities in

Outlook and Opportunities in Corporate Aircraft Don Gies Vice President & Group Manager Business Aviation Finance Presented to the ELA Large Ticket Conference April 25, 2006 Outlook and Opportunities in

Airlines across the world connected a record number of cities this year, with more than 20,000 city pair connections*

1 Airlines across the world connected a record number of cities this year, with more than 20,000 city pair connections*. This is a 1,351 increase over 2016 and a doubling of service since 1996, when there

1 Airlines across the world connected a record number of cities this year, with more than 20,000 city pair connections*. This is a 1,351 increase over 2016 and a doubling of service since 1996, when there

IATA ECONOMICS BRIEFING

IATA ECONOMICS BRIEFING NEW AIRCRAFT ORDERS A POSITIVE SIGN BUT WITH SOME RISKS FEBRUARY 26 KEY POINTS 25 saw a record number of new aircraft orders over 2, for Boeing and Airbus together even though the

IATA ECONOMICS BRIEFING NEW AIRCRAFT ORDERS A POSITIVE SIGN BUT WITH SOME RISKS FEBRUARY 26 KEY POINTS 25 saw a record number of new aircraft orders over 2, for Boeing and Airbus together even though the

Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes July 2010

CURRENT MARKET OUTLOOK Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes July 2010 BOEING is a trademark of Boeing Management Company. Copyright 2010 Boeing. All rights reserved. The

CURRENT MARKET OUTLOOK Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes July 2010 BOEING is a trademark of Boeing Management Company. Copyright 2010 Boeing. All rights reserved. The

Investor Update September 2017 PARTNER OF CHOICE EMPLOYER OF CHOICE INVESTMENT OF CHOICE

Investor Update September 2017 PARTNER OF CHOICE EMPLOYER OF CHOICE INVESTMENT OF CHOICE 1 Forward Looking Statements In addition to historical information, this presentation contains forward-looking statements

Investor Update September 2017 PARTNER OF CHOICE EMPLOYER OF CHOICE INVESTMENT OF CHOICE 1 Forward Looking Statements In addition to historical information, this presentation contains forward-looking statements

Oct-17 Nov-17. Sep-17. Travel is expected to grow over the coming 6 months; at a slightly faster rate

Analysis provided by TRAVEL TRENDS INDEX SEPTEMBER 2018 CTI reading of.8 in September 2018 indicates that travel to or within the U.S. grew 1.6% in September 2018 compared to September 2017. LTI predicts

Analysis provided by TRAVEL TRENDS INDEX SEPTEMBER 2018 CTI reading of.8 in September 2018 indicates that travel to or within the U.S. grew 1.6% in September 2018 compared to September 2017. LTI predicts

SkyWest, Inc. Announces First Quarter 2018 Profit

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces First Quarter 2018

NEWS RELEASE CONTACT: Investor Relations Corporate Communications 435.634.3200 435.634.3553 Investor.relations@skywest.com corporate.communications@skywest.com SkyWest, Inc. Announces First Quarter 2018

Managing through disruption

28 July 2016 Third quarter results for the three months ended 30 June 2016 Managing through disruption 3 months ended Like-for-like (ii) m (unless otherwise stated) Change 30 June 2016 30 June 2015 change

28 July 2016 Third quarter results for the three months ended 30 June 2016 Managing through disruption 3 months ended Like-for-like (ii) m (unless otherwise stated) Change 30 June 2016 30 June 2015 change

December December 2013 BUSINESS AVIATION MONITOR. WINGX Advance is a proud member of: Source: Fotolia

December 2013 December 2013 BUSINESS AVIATION MONITOR WINGX Advance is a proud member of: Source: Fotolia Year to Date analysis of departures With the slight growth in December, the overall decline in

December 2013 December 2013 BUSINESS AVIATION MONITOR WINGX Advance is a proud member of: Source: Fotolia Year to Date analysis of departures With the slight growth in December, the overall decline in

AerCap Holdings N.V. April 11, 2015

AerCap Holdings N.V. April 11, 2015 Disclaimer Incl. Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates and forecasts with respect to future performance and

AerCap Holdings N.V. April 11, 2015 Disclaimer Incl. Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates and forecasts with respect to future performance and

Adjusted net income of $115 million versus an adjusted net loss of $7 million in the second quarter of 2012, an improvement of $122 million

Air Canada Reports Record Second Quarter 2013 Results Highest Adjusted Net Income, Operating Income and EBITDAR Results for Second Quarter in Air Canada s History Adjusted net income of $115 million versus

Air Canada Reports Record Second Quarter 2013 Results Highest Adjusted Net Income, Operating Income and EBITDAR Results for Second Quarter in Air Canada s History Adjusted net income of $115 million versus

Hans-Peter Ring EADS Chief Financial Officer. Cowen Conference February 8 th 2012

Hans-Peter Ring EADS Chief Financial Officer Cowen Conference February 8 th 2012 Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes,

Hans-Peter Ring EADS Chief Financial Officer Cowen Conference February 8 th 2012 Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes,

Steve Hahn. Current Market Outlook. Director, Japan Enterprise Technology Programs. Boeing Commercial Airplanes July 2014.

Current Market Outlook 2015 Boeing Commercial Airplanes July 2014 The statements contained herein are based on good faith assumptions and are to be used for general information purposes only. These statements

Current Market Outlook 2015 Boeing Commercial Airplanes July 2014 The statements contained herein are based on good faith assumptions and are to be used for general information purposes only. These statements

PREMIUM TRAFFIC MONITOR JULY 2014 KEY POINTS

PREMIUM TRAFFIC MONITOR JULY 2014 KEY POINTS Growth in international air passengers was weak for a second consecutive month with a 2.6% increase in July compared to a year ago premium seat numbers rose

PREMIUM TRAFFIC MONITOR JULY 2014 KEY POINTS Growth in international air passengers was weak for a second consecutive month with a 2.6% increase in July compared to a year ago premium seat numbers rose

current market outlook

current market outlook Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes June 2011 The statements contained herein are based on good faith assumptions and provided for general information

current market outlook Randy Tinseth Vice President, Marketing Boeing Commercial Airplanes June 2011 The statements contained herein are based on good faith assumptions and provided for general information

Global Business Jet Market: Industry Analysis & Outlook ( )

") Industry Research by Koncept Analytics Global Business Jet Market: Industry Analysis & Outlook ----------------------------------------- (2018- April 2018 1 Executive Summary A business jet or a private

Industry Research by Koncept Analytics Global Business Jet Market: Industry Analysis & Outlook ----------------------------------------- (2018- April 2018 1 Executive Summary A business jet or a private

OPERATING AND FINANCIAL HIGHLIGHTS. Subsequent Events

Copa Holdings Reports Net Income of $103.8 million and EPS of $2.45 for the Third Quarter of 2017 Excluding special items, adjusted net income came in at $100.8 million, or EPS of $2.38 per share Panama

Copa Holdings Reports Net Income of $103.8 million and EPS of $2.45 for the Third Quarter of 2017 Excluding special items, adjusted net income came in at $100.8 million, or EPS of $2.38 per share Panama

Happy Jetting. A Conversation With Dave Barger, President And Chief Executive Officer, JetBlue Airways, Page 14.

A MAGAZINE FOR AIRLINE EXECUTIVES 2009 Issue No. 2 Taking your airline to new heights Happy Jetting A Conversation With Dave Barger, President And Chief Executive Officer, JetBlue Airways, Page 14. 11

A MAGAZINE FOR AIRLINE EXECUTIVES 2009 Issue No. 2 Taking your airline to new heights Happy Jetting A Conversation With Dave Barger, President And Chief Executive Officer, JetBlue Airways, Page 14. 11

AerCap Holdings N.V. Keith Helming Chief Financial Officer. Wachovia Securities Equity Conference June 23, 2008

AerCap Holdings N.V. Keith Helming Chief Financial Officer Wachovia Securities Equity Conference June 23, 2008 Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates

AerCap Holdings N.V. Keith Helming Chief Financial Officer Wachovia Securities Equity Conference June 23, 2008 Forward Looking Statements & Safe Harbor This presentation contains certain statements, estimates

AIRBUS H Roadshow Presentation. New York July 31 st, 2017

AIRBUS H1 2017 Roadshow Presentation New York July 31 st, 2017 H1 2017 HIGHLIGHTS 2 Healthy commercial aircraft environment; robust backlog of 6,771 a/c supports ramp-up plans H1 financials reflect delivery

AIRBUS H1 2017 Roadshow Presentation New York July 31 st, 2017 H1 2017 HIGHLIGHTS 2 Healthy commercial aircraft environment; robust backlog of 6,771 a/c supports ramp-up plans H1 financials reflect delivery

OPERATING AND FINANCIAL HIGHLIGHTS SUBSEQUENT EVENTS

Copa Holdings Reports Net Income of US$6.2 Million and EPS of US$0.14 for the Third Quarter of 2015 Excluding special items, adjusted net income came in at $37.4 million, or EPS of $0.85 per share Panama

Copa Holdings Reports Net Income of US$6.2 Million and EPS of US$0.14 for the Third Quarter of 2015 Excluding special items, adjusted net income came in at $37.4 million, or EPS of $0.85 per share Panama

2010 Global Transportation Conference

Air Canada's Executive Vice President & CFO Michael Rousseau presents at 2010 Global Transportation Conference New York June 16, 2010 Agenda Air Canada leading carrier in all markets Managing through challenging

Air Canada's Executive Vice President & CFO Michael Rousseau presents at 2010 Global Transportation Conference New York June 16, 2010 Agenda Air Canada leading carrier in all markets Managing through challenging

Global Transportation Conference. New York June 18, 2008

Global Transportation Conference New York June 18, 2008 1 It s Different Up Here Diversified network New revenue model Canada a growth market New efficient fleet New onboard product Well hedged fuel Strong

Global Transportation Conference New York June 18, 2008 1 It s Different Up Here Diversified network New revenue model Canada a growth market New efficient fleet New onboard product Well hedged fuel Strong

IATA ECONOMICS BRIEFING AIRLINE BUSINESS CONFIDENCE INDEX OCTOBER 2010 SURVEY

IATA ECONOMICS BRIEFING AIRLINE BUSINESS CONFIDENCE INDEX OCTOBER SURVEY KEY POINTS Results from IATA s quarterly survey conducted in October show business conditions continued to improve during the third

IATA ECONOMICS BRIEFING AIRLINE BUSINESS CONFIDENCE INDEX OCTOBER SURVEY KEY POINTS Results from IATA s quarterly survey conducted in October show business conditions continued to improve during the third

AIR CANADA REPORTS SECOND QUARTER RESULTS

AIR CANADA REPORTS SECOND QUARTER RESULTS SECOND QUARTER OVERVIEW Passenger revenue increased 5 per cent to $2.5 billion, due to growth in traffic and yield. Excluding fuel expense, unit cost declined

AIR CANADA REPORTS SECOND QUARTER RESULTS SECOND QUARTER OVERVIEW Passenger revenue increased 5 per cent to $2.5 billion, due to growth in traffic and yield. Excluding fuel expense, unit cost declined

SKYWEST, INC. ANNOUNCES THIRD QUARTER 2014 RESULTS

NEWS RELEASE For Further Information Contact: Investor Relations Telephone: (435) 634-3203 Fax: (435) 634-3205 FOR IMMEDIATE RELEASE: October 29, 2014 SKYWEST, INC. ANNOUNCES THIRD QUARTER 2014 RESULTS

NEWS RELEASE For Further Information Contact: Investor Relations Telephone: (435) 634-3203 Fax: (435) 634-3205 FOR IMMEDIATE RELEASE: October 29, 2014 SKYWEST, INC. ANNOUNCES THIRD QUARTER 2014 RESULTS

Press Release. Bilfinger with dynamic start to financial year 2018

Press Release May 15, 2018 Bilfinger with dynamic start to financial year 2018 Book-to-bill ratio reaches 1.2 in the first quarter Fourth consecutive growth quarter in orders received Adjusted EBITA above

Press Release May 15, 2018 Bilfinger with dynamic start to financial year 2018 Book-to-bill ratio reaches 1.2 in the first quarter Fourth consecutive growth quarter in orders received Adjusted EBITA above

Retirements and Inductions How are Fleet Demographics Changing?

Retirements and Inductions How are Fleet Demographics Changing? Aviation Week Network: Aero-Engines Americas February 1, 218: Fort Lauderdale, USA TODAY S AGENDA Historic Commercial Air Transport Fleet

Retirements and Inductions How are Fleet Demographics Changing? Aviation Week Network: Aero-Engines Americas February 1, 218: Fort Lauderdale, USA TODAY S AGENDA Historic Commercial Air Transport Fleet

Parques Reunidos Corporate Presentation March 2016

Parques Reunidos Corporate Presentation March 216 Disclaimer The information contained in this presentation (the Presentation ), including but not limited to forward-looking statements, is provided as

Parques Reunidos Corporate Presentation March 216 Disclaimer The information contained in this presentation (the Presentation ), including but not limited to forward-looking statements, is provided as

AIR CANADA REPORTS FULL YEAR AND FOURTH QUARTER 2010 RESULTS

AIR CANADA REPORTS FULL YEAR AND FOURTH QUARTER 2010 RESULTS Record annual EBITDAR of $1.386 billion, 104 per cent improvement Operating income improvement of $677 million Employees to receive special

AIR CANADA REPORTS FULL YEAR AND FOURTH QUARTER 2010 RESULTS Record annual EBITDAR of $1.386 billion, 104 per cent improvement Operating income improvement of $677 million Employees to receive special

QANTAS HALF YEAR 2015 FINANCIAL RESULTS 1

QANTAS HALF YEAR 2015 FINANCIAL RESULTS 1 Key points: Underlying Profit Before Tax: $367 million Statutory Profit After Tax: $206 million Transformation benefits: $374 million Comparable unit cost reduction:

QANTAS HALF YEAR 2015 FINANCIAL RESULTS 1 Key points: Underlying Profit Before Tax: $367 million Statutory Profit After Tax: $206 million Transformation benefits: $374 million Comparable unit cost reduction:

Thales on the Civil Aerospace market

thalesgroup.com Innovation - Civil Aerospace - Defence Aerospace - Transportation - Defence - Security Thales on the Civil Aerospace market AT A GLANCE World n 1 in ATM, covering 40% of world s surface

thalesgroup.com Innovation - Civil Aerospace - Defence Aerospace - Transportation - Defence - Security Thales on the Civil Aerospace market AT A GLANCE World n 1 in ATM, covering 40% of world s surface

JETNET iq Releases Highlights From NBAA 2012 State of the Market Briefing

PRESS RELEASE Date: For Immediate Release JETNET iq Releases Highlights From NBAA 2012 State of the Market Briefing UTICA, NY Today JETNET LLC, the world leader in aviation market intelligence, presented

PRESS RELEASE Date: For Immediate Release JETNET iq Releases Highlights From NBAA 2012 State of the Market Briefing UTICA, NY Today JETNET LLC, the world leader in aviation market intelligence, presented

Mar-16. Apr-16. Travel is expected to grow over the coming 6 months; at a slower rate

Analysis provided by TRAVEL TRENDS INDE MARCH 2017 CTI reading of.8 in March 2017 shows that travel to and within the U.S. grew by 3.6% from March 2016 to March 2017. LTI predicts overall positive travel

Analysis provided by TRAVEL TRENDS INDE MARCH 2017 CTI reading of.8 in March 2017 shows that travel to and within the U.S. grew by 3.6% from March 2016 to March 2017. LTI predicts overall positive travel

Third Quarter November 7, 2008

Third Quarter 8 November 7, 8 Table of Contents Operating Statistics Revenue Highlights Expense Highlights 3 rd Quarter EBITDAR of $355 mln (millions) Q3 8 Q3 7 Change Fav./(Unfav.) Oper. Revenue $ 3,75

Third Quarter 8 November 7, 8 Table of Contents Operating Statistics Revenue Highlights Expense Highlights 3 rd Quarter EBITDAR of $355 mln (millions) Q3 8 Q3 7 Change Fav./(Unfav.) Oper. Revenue $ 3,75

MRO Market Update & Industry Trends

January 25-26, 2017 Cancun, Mexico Presented by: Jonathan M. Berger Vice President ICF jberger@icf.com MRO Market Update & Industry Trends 0 Today s Agenda Fleet & MRO Forecast 2016: What a long strange

January 25-26, 2017 Cancun, Mexico Presented by: Jonathan M. Berger Vice President ICF jberger@icf.com MRO Market Update & Industry Trends 0 Today s Agenda Fleet & MRO Forecast 2016: What a long strange

Technical Memorandum. Synopsis. Steve Carrillo, PE. Bryan Oscarson/Carmen Au Lindgren, PE. April 3, 2018 (Revised)

") Appendix D Orange County/John Wayne Airport (JWA) General Aviation Improvement Program (GAIP) Based Aircraft Parking Capacity Analysis and General Aviation Constrained Forecasts Technical Memorandum To:

Appendix D Orange County/John Wayne Airport (JWA) General Aviation Improvement Program (GAIP) Based Aircraft Parking Capacity Analysis and General Aviation Constrained Forecasts Technical Memorandum To:

Quarterly Aviation Industry Performance

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance 3Q17 (Updated November 17) Prepared by: Strategic Planning department

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance 3Q17 (Updated November 17) Prepared by: Strategic Planning department

Market Reports First Quarter 2016

Reports First Quarter 2016 Challenger 300/604/605 Hawker 800XP/850XP/900XP Phenom 100/300 Citation Mustang/CJ1/CJ1+/CJ2/CJ2+/CJ3/CJ4 Lear 45/45XR/60/60XR Beechjet 400A Hawker 400XP 1 WHO WE ARE Elliott

Reports First Quarter 2016 Challenger 300/604/605 Hawker 800XP/850XP/900XP Phenom 100/300 Citation Mustang/CJ1/CJ1+/CJ2/CJ2+/CJ3/CJ4 Lear 45/45XR/60/60XR Beechjet 400A Hawker 400XP 1 WHO WE ARE Elliott

Copa Holdings Reports Net Income of $49.9 million and EPS of $1.18 for the Second Quarter of 2018

Copa Holdings Reports Net Income of $49.9 million and EPS of $1.18 for the Second Quarter of 2018 Panama City, Panama --- Aug 8, 2018. Copa Holdings, S.A. (NYSE: CPA), today announced financial results

Copa Holdings Reports Net Income of $49.9 million and EPS of $1.18 for the Second Quarter of 2018 Panama City, Panama --- Aug 8, 2018. Copa Holdings, S.A. (NYSE: CPA), today announced financial results

Forward-looking Statements

March 23, 2011 Forward-looking Statements This presentation contains certain forward-looking statements with respect to the Corporation. These forward-looking statements, by their nature, necessarily involve

March 23, 2011 Forward-looking Statements This presentation contains certain forward-looking statements with respect to the Corporation. These forward-looking statements, by their nature, necessarily involve

Oct-17 Nov-17. Travel is expected to grow over the coming 6 months; at a slower rate

Analysis provided by TRAVEL TRENDS INDEX OCTOBER 2018 CTI reading of 51.6 in October 2018 indicates that travel to or within the U.S. grew 3.2% in October 2018 compared to October 2017. LTI predicts travel

Analysis provided by TRAVEL TRENDS INDEX OCTOBER 2018 CTI reading of 51.6 in October 2018 indicates that travel to or within the U.S. grew 3.2% in October 2018 compared to October 2017. LTI predicts travel

JAL Group Announces its FY Medium-Term Business Plan

JAL Group Announces its FY2006-2010 Medium-Term Business Plan -Mobilize the Group s Strengths to Regain Trust - Tokyo, Thursday March 2, 2006: The JAL Group today announced its medium-term business plan

JAL Group Announces its FY2006-2010 Medium-Term Business Plan -Mobilize the Group s Strengths to Regain Trust - Tokyo, Thursday March 2, 2006: The JAL Group today announced its medium-term business plan

executive summary The global commercial aircraft fleet in service is expected to increase by 80% to 45,600 aircraft in 2033 including 37,900

executive summary The 2014 Flightglobal Fleet Forecast estimates that 36,820 new commercial jet and turboprop aircraft will be delivered into passenger and freighter airline service between 2014 and 2033.

executive summary The 2014 Flightglobal Fleet Forecast estimates that 36,820 new commercial jet and turboprop aircraft will be delivered into passenger and freighter airline service between 2014 and 2033.

GERMAN EQUITY FORUM 2016

Extend Your Expectations GERMAN EQUITY FORUM 2016 NOVEMBER 21, 2016 This document contains information which is proprietary to FACC or other companies. Any reproduction, disclosure or use of this information