Weekly Market Report

|

|

|

- Sandra Mills

- 5 years ago

- Views:

Transcription

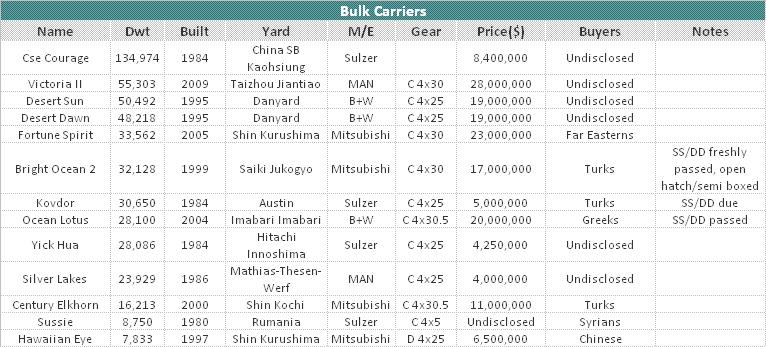

1 Week 31 Tuesday 4th August 9 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News China's economy should grow by 8% this year and next, but significant risks remain. The Economist Intelligence Unit has revised its economic forecasts for China in 9-1, and now believes that the country will achieve 8% GDP growth in both years. With real GDP growth having reached 7.9% year on year in the second quarter of 9, China already appears on course to achieve the government's aim of 8% average growth this year. However, growth in 1 remains subject to significant upside and downside risks. The outlook is obscured by the dominant role that government policy is set to play next year, and by the high degree of uncertainty with regard to the outlook for the global economy. Our forecast for next year reflects an assumption that the government will tighten credit and fiscal policy moderately. Such an approach would be likely to have negative side-effects. Assetprice inflation will be stimulated by a credit and fiscal policy stance that will be kept loose to offset the effects of the weak global economy on the export sector. (Economist) Energy & Commodities Commodities prices hit their highest level for the year on Monday, with European s oil benchmark Brent trading above $73.5 a barrel, buoyed by positive economic data and a sharp weakening of the US dollar. Other raw materials that hit a 9 peak included heating oil, copper, aluminum, zinc, lead, nickel, rice, sugar, rubber and iron ore. In addition, agricultural commodities such as corn, wheat and soyabeans rallied. White sugar in London soared to its highest price since July The commodities rally came as manufacturing data from China to the US showed a marked improvement in July, suggesting that raw materials demand from industrial consumers will perk up. (Financial Times) Shipping News A scrapping surge and only a trickle of newbuilding deliveries restricted containership fleet growth to its lowest level in at least a decade in July, new figures show. Total deployed capacity rose by only 7,-teu last month, AXS Alphaliner says, the worst month on month figure since it began tracking liner fleet growth 1 years ago. It said: The cellular fleet itself has increased by only, teu in July, with 15 cellular ships totalling 73, teu completed, while the cellular tonnage reaching scrapping spots surged to 34 ships for 54, teu within the space of one month. Just over container ships were sent to the breakers in June. Alphaliner added: The cellular fleet currently stands at 4,69 ships totalling million teu (of which 1.3% are currently lying idle or laid up). As at 3 August, the idle fleet stands at 1.31 million teu, compared to 1. million teu a month ago as a number of ships are taken out of service as they end their rotations on services that have been halted or suspended. Non-operating owners share of the idle fleet has reached 1,-teu, which at 4.7% of the global total is a new record, Alphaliner s latest report says. Claus-Peter Offen s 5,77-teu OOCL Korea (also known as the Santa Victoria, built 1) has become the first NOO vessel over 5,-teu to be idled after finishing an eight year spell with OOCL. Carriers have 713,-teu of capacity in lay-up, equal to 5.6% of the global fleet. (Tradewinds) Chartering (Wet: Stable / Dry: Stable) For the past week, on the Dry market, the BDI was on Friday (31/7/9) 3,35, +5 points up from end of previous week s levels. On the Wet market, the BDTI on Friday (31/7/9) was 474, -3 points down and the BCTI at 465, +21 points up from end of previous week s levels. Sale & Purchase (Wet: Stable- / Dry: Stable+) The tanker S&P market has some interesting aframax sales to show for this week, the DH aframax Patriot Spirit (96,9 dwt built 1992) was sold to Indonesian interests at $16,4m and the DS aframax New Ambition (88,761 dwt built 1987) was sold at $6,2m. On the dry tonnage, there have been a satisfactory number of deals to report: indicatively, the supramax Victoria II (55,33 dwt built 9) was sold for $28m, the handymaxes Desert Sun (5,492 dwt built 1995) and Desert Dawn (48,218 dwt built 1995) fetched $19m each and Greeks have acquired the handysize Ocean Lotus (28, dwt built 4) for $m with SS/DDD just passed. Newbuilding (Wet: Weaker / Dry: Weaker) This week Crystal Maritime ordered 2 Capesize bulkers of 1,dwt each from Daehan Shipyard, with delivery 11 for region 7$m each. After a torrid first half 9, there are now encouraging signs that a positive contracting environment is not far away. Demolition (Wet: Stable+ / Dry: Stable+ ) The demolition market continues to be firm. This week Indian breakers have acquired the LNG Margaret Hill (87,3cbm-23,ldt-built 1974) for 365$/ldt, asis Southampton, the tween decker Jumana (12,67dwt-4,9ldt-built 1977) for 1$/ldt, asis Suez. Pakistani breakers have purchased the MR tanker Palenque (37,574dwt- 8,379ldt-built 1987) for 31$/ldt and the tween decker Salina (12,7dwt-6,5ldt-built 1981) for 234/ldt. Chinese ship breakers have acquired the container Gem (2,728teu-14,342ldt-built 1983) for 27$/ldt. Intermodal Research 1 4/8/9

2 Wet Market $m VLCC Suez max Dirty Clean Aframax Vessel VLCC Suez max Aframax Panamax MR Handy size Jan-8 1-Feb-8 Routes Week 31 Week 3 2q9 2q8 ±% WS points Spot Rates WS points 265k AG-JAPAN 35 16, ,39 17% 22, ,795 2k AG-USG 28 12, ,919 1% 13,375 94,41 2k WAF-USG 38 23, ,284 25% 34, ,76 13k MED-MED 48 6, ,714-5% 27,36 115,885 13k WAF-USAC 45 8, ,77 6% 22,381 84,295 13k AG-CHINA 5 12, ,55-9% 21,754 68,825 k AG-EAST 7 1, ,625 % 11,9 42,69 k MED-MED 5, , -4% 17,189 69,37 k UKC-UKC ,957-16% 12,814 96,3 7k CARIBS-USG 68 5,615 2,949 13% 1,539 44,766 75k AG-JAPAN 83 13, ,493 1% 8,363 29,73 55k AG-JAPAN 12, ,9 21% 6,577 26,219 37K UKC-USAC 115 9, ,479 1% 8,931 33,563 3K MED-MED 5, ,797-9% 6,839 5,244 55K UKC-USG 7 5, ,9 % 13,57 48,955 55K MED-USG 7 3, ,873 % 12,176 45,438 5k CARIBS-USAC 65 1, ,115-7% 11,16 42,548 TC Rates Week 31 Week 3 ±% k 1yr TC 36,25 36,25.% 44,58 73,798 55,798 3k 3yr TC 36, 36,.%,813 58,844 48,585 15k 1yr TC 27,75 27,75.% 34,75 47,442 44,72 15k 3yr TC 26,7 26,7.% 32,87 41,123 38,777 15k 1yr TC 18,25 18,25.% 21,863 36,43 33,394 15k 3yr TC 19, 19,.% 22,79 3,7 29,83 7k 1yr TC 17,75 18,75-5.3% 21,72 29,471 29,567 7k 3yr TC 18,7 19, -2.6% 21,635 26,686 27,113 45k 1yr TC 13,25 14,25-7.% 17,315 23,731 26,154 45k 3yr TC 14,7 15, -3.3% 17,547 22,527 23,488 36k 1yr TC 11,25 13, % 16,89 22,2 23,519 36k 3yr TC 12, 13, -7.6% 15,974,585 21,517 Tankers SH Values (5yrs) VLCC Suezmax Aframax Panamax MR 1-Mar-8 1-Apr-8 1-May-8 1-Jun-8 1-Jul-8 1-Aug-8 1-Sep-8 1-Oct-8 1-Nov-8 1-Dec-8 1-Jan-9 1-Feb-9 1-Mar-9 1-Apr-9 1-May-9 1-Jun-9 1-Jul-9 The Tankers Sale and Purchase activity remains at low levels. Most interested parties have adopted a wait and see attitude, as second hand values continue to follow a downward trend. The double hull Patriot Spirit (96,9 dwt built 1992) was sold to Indonesian interests at $16,4m. By way of comparison, in October 8, Cardiff Marine sold Tigani (97,114 dwt built 1991) to Oceanfreight for $m. It is also worth noting that last month, the one year younger Chemtrans Lyra (97,97 dwt built 1993) also double hulled, was close to being committed for $16,5m, again to Indonesian based buyers but the deal never materialised. The double sided but single bottom aframax New Ambition (88,761 dwt built 1987) was sold to undisclosed at $6,2m. DIRTY - WS RATES Furthermore, in the small tankers section, the double bottom IMO II/III Kinugawa (24,743dwt-built 1984) was purchased by an undisclosed buyer for 3.5$m, the very modern double hull Southern York (6,5dwt-built 3) was acquired by Japanese for 15$m and finally the similar size but older DH IMO II/III Golden Chemical (6,62dwt-built 1991) was sold to Singaporeans for 4.2$m. WS points WS points Jan-7 2-Mar Jan-7 2-Mar-7, 9,, 7,, 5,, 3,, 1, 5-Jan-7, 7,, 5,, 3,, 1, 5-Apr-7 5-Jan-7 5-Mar-7 TD3 TD5 TD8 TD4 5-Jul-7 2-May-7 2-Jul-7 2-Sep-7 2-Nov-7 2-Jan-8 2-Mar-8 2-May-8 2-Jul-8 TC2 TC4 TC6 TC1 2-Sep-8 2-Nov-8 2-Jan-9 2-Mar-9 2-May-9 2-Jul-9 2-May-7 2-Jul-7 2-Sep-7 2-Nov-7 2-Jan-8 2-Mar-8 2-May-8 2-Jul-8 2-Sep-8 2-Nov-8 2-Jan-9 2-Mar-9 2-May-9 CLEAN - WS RATES 2-Jul-9 Tankers 1YR TC RATES VLCC Suezmax Aframax Panamax MR 5-Oct-7 5-Jan-8 5-Apr-8 5-Jul-8 5-Oct-8 5-Jan-9 5-Apr-9 5-Jul-9 Tankers 3YR TC RATES VLCC Suezmax Aframax Panamax MR 5-May-7 5-Jul-7 5-Sep-7 5-Nov-7 5-Jan-8 5-Mar-8 5-May-8 5-Jul-8 5-Sep-8 5-Nov-8 5-Jan-9 5-Mar-9 5-May-9 5-Jul-9 Intermodal Research 2 4/8/9

3 Dry Market $m Capesize Panamax Supramax Handymax Handysize Baltic Indices Week 31 Week 3 31/7/9 24/7/9 ±% Index Index Index Index Index BDI 3,35 3,345 % 2,571 6,663 7,321 BCI 5,385 71,188 5,17 79,45 4% 1,624 9,577 1,172 BPI 3,183 24,34 3,524 22,632-1% 79 6,342 7,283 BSI 2,81 18,64 2,91 18,234 % 661 4,225 4,788 BHSI 887 1, ,54 1% 529 2,257 2, Jan-8 1-Feb-8 Period Week Week 31 3 ±% K 6mnt TC 5,25 52,25-4% 37,3 117,43 118,6 17K 1yr TC 41, 39,45 4% 31, ,729 17,118 17K 3yr TC 33,25 33,25 % 26,452 82,429 76,58 7K 6mnt TC 28,45 28,95-2% 18,712 57,623 58,996 7K 1yr TC 22, 22,5-2% 16,476 55,887 52,567 7K 3yr TC 15,7 15,7 % 14,934 44,556 39,974 52K 6mnt TC,75,75 % 14,984 47,159 48,822 52K 1yr TC 16,7 16,95-1% 13,329 45,71 45,92 52K 3yr TC 14,25 14,75-3% 13,94 34,38 34, 45k 6mnt TC 18, 18, % 12,869 41,681 43,639 45k 1yr TC 14,5 14,75-2% 11,5 38,923, 45k 3yr TC 12,95 13, -2% 11,535 28,431 29,63 3K 6mnt TC 13, 12,25 6% 1,315 3,547 31,596 3K 1yr TC 11,45 11,45 % 9,853 29,686 28,3 3K 3yr TC 11,5 11,5 % 1,376 22,87 22,113 Bulk Carriers SH Values (5yrs) Capesize Panamax Handymax Handysize 1-Mar-8 1-Apr-8 1-May-8 1-Jun-8 1-Jul-8 1-Aug-8 1-Sep-8 1-Oct-8 1-Nov-8 1-Dec-8 1-Jan-9 1-Feb-9 1-Mar-9 1-Apr-9 1-May-9 1-Jun-9 1-Jul-9 It has been another very busy week in the dry S&P market with some interesting sales across the sectors, mainly for modern units. In the supramax sector, undisclosed buyers bought the China-built Victoria II (55,33 dwt built 9) for $28m. In the end of June, we reported the resale of the China-built supramax Nantong Cosco Khi 66 (55, dwt ) with delivery December 9 for a firm $33m! Undisclosed buyers acquired the handymaxes Desert Sun (5,492 dwt built 1995) and Desert Dawn (48,218 dwt built 1995) for $19m each. Bulkers of this tonnage/age are very popular in beg of May, East-Med owned Sea Luck (45,429 dwt built 1995) was reported sold to Chinese for $15,5m. In the handysize sector, the open hatch/semi boxed Bright Ocean 2 (32,128 dwt built 1999) was sold to Turkish buyers for $17m with SS/DD freshly passed.. Furthermore, Greeks acquired the Ocean Lotus (28, dwt built 4) for $m with SS/DDD just passed. No similar tonnage has been sold recently thus no comparison is available Turkish were also the buyers of the older Kovdor (3,65 dwt built 1984) at $5m with SS/DD due. About a month ago, in July 9, we reported the sale of Pontoporos (29,155 dwt built 1984) to undisclosed buyers at he same price of $5m with SS/DD due. 22,, 18, 16, 14, 12, 1, 8, 6, 4, 2, One deal worth mentioning,is the sale of Century Elkhorn (16,113 dwt built 1996) for $11m to Turkish buyers. Index 2, 21, 1, 15,, 9,, 3, 2-Jan-6 2-Apr-6 2-Jul-6 2-Jan-6 2-Apr-6 2-Jul-6 2-Oct-6 2-Jan-7 2-Apr-7 2-Jul-7 2-Oct-7 2-Jan-8 2-Apr-8 2-Jul-8 2-Oct-8 Baltic Indices BCI BPI BSI BHSI BDI AVR 4TC BCI AVR 5TC BSI 2-Oct-6 2-Jan-7 2-Jan-9 2-Apr-9 2-Jul-9 Average T/C Rates for Baltic Indices AVR 4TC BPI AVR 6TC BHSI 2-Apr-7 2-Jul-7 2-Oct-7 2-Jan-8 2-Apr-8 2-Jul-8 2-Oct-8 2-Jan-9 2-Apr-9 2-Jul-9 Dry Bulkers 1 Year Period Rates Capesize Panamax Handymax Supramax Handysize 21, 1, 15,, 9,, 3, 5-Jan-7 5-Mar-7 5-May-7 5-Jul-7 5-Sep-7 5-Nov-7 5-Jan-8 5-Mar-8 5-May-8 5-Jul-8 5-Sep-8 5-Nov-8 5-Jan-9 5-Mar-9 5-May-9 5-Jul-9 Dry Bulkers 3 Year Period Rates Capesize Panamax Handymax Supramax Handysize,,,,,, 5-Jan-7 5-Mar-7 5-May-7 5-Jul-7 5-Sep-7 5-Nov-7 5-Jan-8 5-Mar-8 5-May-8 5-Jul-8 5-Sep-8 5-Nov-8 5-Jan-9 5-Mar-9 5-May-9 5-Jul-9 Intermodal Research 3 4/8/9

4 Secondhand Sales Intermodal Research 4 4/8/9

5 New Building Market million $ Apr-6 7-Jul-6 Bulkers Tankers Gas Tankers NB Prices (m$) VLCC Suezmax Aframax LR1 MR 7-Oct-6 7-Jan-7 7-Apr-7 7-Jul-7 7-Oct-7 7-Jan-8 7-Apr-8 7-Jul-8 7-Oct-8 7-Jan-9 7-Apr-9 7-Jul-9 Indicative Newbuilding Prices (million$) Vessel Week Week 3 29 ±% Capesize 17k % Panamax 75k % Supramax 57k % Handysize 3k % VLCC 3k % Suezmax 15k % Aframax 11k % LR1 7k % MR 47k % LPG M3 k % LPG M3 52k % LPG M3 23k % Please note that due to the lack of new newbuilding orders in most of the above sectors, the prices are estimates. million $ 7-Apr-6 7-Jul-6 Bulk Carriers NB Prices (m$) Capesi ze Panamax Supramax Handys ize 7-Oct-6 7-Jan-7 7-Apr-7 7-Jul-7 7-Oct-7 7-Jan-8 7-Apr-8 7-Jul-8 7-Oct-8 7-Jan-9 7-Apr-9 7-Jul-9 The newbuilding market continues to show further signs of activity. Shipyards are starting to show interest on discussing prices at more competitive levels. This week Crystal Maritime ordered 2 Capesize bulkers of 1,dwt each from Daehan Shipyard, with delivery 11 for region 7$m each. Intermodal Research 5 4/8/9

6 Demolition Market The demolition market has seen a pretty stable environment for the last couple of weeks. Prices present firm and activity remains on normal levels. There is a reason for optimism with the supply plentiful and demand still there. In Bangladesh demolition prices have held up for tankers at around 3$/ldt with larger containers and bulkers seeing region 2$/ldt. Indicative Demolition Prices ($/ldt) Markets Week Week 31 3 ±% Bangladesh % India % Pakistan % China 2 2.% Bangladesh % India % Pakistan % China 2 2.% India has been the busiest market this week. Indian breakers have acquired the LNG Margaret Hill (87,3cbm-23,ldt-built 1974) for 365$/ldt, asis Southampton, the tween decker Jumana (12,67dwt- 4,9ldt-built 1977) for 1$/ldt, asis Suez and the 2 reefers Crystal Lily (487,276cuft-6,674ldt-built 1979) and Crystal orchid (482,2cuft-6,57ldt-built 1979) for an undisclosed price. Activity in Pakistan seems to be picking up, with demolition prices ranging between 35$/ldt for wet and 265$/ldt for dry tonnage. This week Pakistani breakers have purchased the MR tanker Palenque (37,574dwt-8,379ldt-built 1987) for 31$/ldt and the tween decker Salina (12,7dwt-6,5ldt-built 1981) for 234/ldt. China remains firm, offering around 2$/ldt for wet and 2$/ldt for dry tonnage. This week, Chinese ship breakers have acquired the container Gem (2,728teu-14,342ldt-built 1983) for 27$/ldt. As far as containers are concerned, China has become the primary market for Far East tonnage. Wet Dry $/ldt Wet Demolition Prices Bangladesh India Pakis tan China $/ldt Dry Demolition Prices Banglades h India Pakistan China 7-Jan-5 7-Jul-5 7-Jan-6 7-Jul-6 7-Jan-7 7-Jul-7 7-Jan-8 7-Jul-8 7-Jan-9 7-Jul-9 7-Jan-5 7-Jul-5 7-Jan-6 7-Jul-6 7-Jan-7 7-Jul-7 7-Jan-8 7-Jul-8 7-Jan-9 7-Jul-9 Intermodal Research 6 4/8/9

7 Stock Exchange Data Currencies Commoditites Market Data 3-Aug-9 31-Jul-9 3-Jul-9 29-Jul-9 28-Jul-9 W-O-W Change % Dow Jones 9, , , ,7.7 9, % Nasdaq 2,9 1,979 1,984 1,968 1, % S&P 5 1, % FTSEurofirst % DJ Euro Stoxx 5 2,674 2,638 2,655 2, 2, % FTSE 4,682 4,8 4,632 4,548 4, % FTSE All-Share UK 2,392 2,353 2,361 2,318 2,38 2.3% CAC 3,478 3,426 3,435 3,366 3, % Xetra Dax 5,427 5,332 5,361 5,27 5, % Nikkei 1,352 1,357 1,165 1,113 1,87 2.6% Hang Seng,7,573,234,136, % FTSE All World $ % / $ % / $ % / $ % $ / % / % $ INDEX % / SFr % Oil Brent $ % Oil WTI $ % Gold $ % Company Maritime Stock Data oil Stock W-O-W Curr. 3-Aug-9 31-Jul-9 3-Jul-9 29-Jul-9 28-Jul-9 27-Jul-9 Exchange Commodities & Financial Market Basic Commodities Weekly Summary Oil Brent $ Oil WTI $ Gold $ Change % gold Max 52wk Min 52wk AEGEAN MARINE PETROL NYSE USD % ARIES MARITIME TRANSPORT NASDAQ USD % CAPITAL PRODUCT PARTNERS L.P. NASDAQ USD % DANAOS CORP NYSE USD % DIANA SHIPPING NASDAQ USD % DRYSHIPS INC(IPO) NASDAQ USD % EUROSEAS LTD NASDAQ USD % EXCEL MARITIME CARRIERS NYSE USD % FREESEAS INC NASDAQ USD % GENCO SHIPPING NYSE USD % GENERAL MARITIME NYSE USD % GLOBUS MARITIME LTD LONDON GBX % HELLENIC CARRIERS LTD LONDON GBX % NAVIOS MARITIME CORP NYSE USD % OCEANFREIGHT INC NASDAQ USD %..82 OMEGA NAVIGATION ENTERPRISES INC NASDAQ USD % PARAGON SHIPPING INC NASDAQ USD % STEALTHGAS INC NASDAQ USD % TOP SHIPS INC NASDAQ USD % TSAKOS ENERGY NAVIGATION INC NYSE USD % MDO 3cst 1cst Bunker Prices W-O-W 31-Jul-9 24-Jul-9 Change % Rotterdam % Houston % Singapore % Rotterdam % Houston % Singapore % Rotterdam % Houston % Singapore % For any further queries please do not hesitate to contact our Research Department. The information contained in this report has been obtained from various sources, as reported in the market. Intermodal Shipbrokers Co. believes such information to be factual and reliable without making guarantees regarding its accuracy or completeness. Whilst every care has been taken in the production of the above review, no liability can be accepted for any loss or damage incurred in any way whatsoever by any person who may seek to rely on the information and views contained in this material. This report is being produced for the internal use of the intended recipients only and no re-producing is allowed, without the prior written authorization of Intermodal Shipbrokers Co. Intermodal Shipbrokers Co. 17th km Ethniki Odos Athens-Lamia & 3 Agrambelis Street, N. Kifisia, Athens - Greece Tel: Fax: Compiled by: Intermodal Research Department Ms. Mariana Skiadopoulou research@intermodal.gr On behalf of: Intermodal Sale & Purchase and Newbuilding Departments Mr. K. Dermatis, Mr D. Evdemon, Mr. C. Goudis, Mr. A. Poulopoulos, Mr. T. Ntalakos, Ms. N. Anomitri, Mr. G. Dermatis, Mr. T. Papadopoulos, Mr. P. Manesis snp@intermodal.gr Intermodal Research 7 4/8/9

Weekly Market Report

Week 18 Tuesday 5th May 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News US bank shares surged on Monday as investors bet that some of the country

Week 18 Tuesday 5th May 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News US bank shares surged on Monday as investors bet that some of the country

Weekly Market Report

Week 7 Tuesday 17th February 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News President Barack Obama today signs into law one of the largest pieces

Week 7 Tuesday 17th February 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News President Barack Obama today signs into law one of the largest pieces

Weekly Market Report

Week 2 Tuesday 13th January 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News The risk of serious fiscal crises in developed countries has doubled

Week 2 Tuesday 13th January 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News The risk of serious fiscal crises in developed countries has doubled

Weekly Market Report

Week 46 Tuesday 17th November 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News Japan announced Monday its best economic growth in more than two years

Week 46 Tuesday 17th November 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News Japan announced Monday its best economic growth in more than two years

Weekly Market Report

Week 15&16 Tuesday 21st April 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News Worldwide losses tied to rotten loans and securitized assets may reach

Week 15&16 Tuesday 21st April 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News Worldwide losses tied to rotten loans and securitized assets may reach

Weekly Market Report

Week 22 Tuesday 2nd June 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News The euro weakened from an 8 month high against the yen, commodities dropped

Week 22 Tuesday 2nd June 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News The euro weakened from an 8 month high against the yen, commodities dropped

Dry Bulk Market Weekly Highlights Week 17 - Dry Cargo Market Highlights for the period of 21-April-2011 until 28-April-2011

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

WEEKLY SHIPPING MARKET REPORT

WEEKLY SHIPPING MARKET REPORT WEEK 42 (10 rd October to 16 th October 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

WEEKLY SHIPPING MARKET REPORT WEEK 42 (10 rd October to 16 th October 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

WEEKLY MARKET REPORT January 27th, 2012 / Week 4

WEEKLY MARKET REPORT January 27th, 2012 / Week 4 Whilst the capesize losses were just below 6% all other segments continue to suffer double digit losses with the panamaxes leading the way. The BPI lost

WEEKLY MARKET REPORT January 27th, 2012 / Week 4 Whilst the capesize losses were just below 6% all other segments continue to suffer double digit losses with the panamaxes leading the way. The BPI lost

WEEKLY MARKET REPORT July 16th, 2010 / Week 28

LY MARKET REPORT July 16th, 21 / Week 28 All indices have continued their downward trend for another week, as the capesize rates continued their downward spiral. Very poor demand for iron ore has put pressure

LY MARKET REPORT July 16th, 21 / Week 28 All indices have continued their downward trend for another week, as the capesize rates continued their downward spiral. Very poor demand for iron ore has put pressure

Monday, August 30, Week 35 The Week at a Glance

Monday, August 3, 21 - Week 35 The Week at a Glance Hunting Season? Vacations season is almost over and decision makers are getting back in to their usual schedules. Let s see whether September will be

Monday, August 3, 21 - Week 35 The Week at a Glance Hunting Season? Vacations season is almost over and decision makers are getting back in to their usual schedules. Let s see whether September will be

WEEKLY MARKET REPORT April 20th, 2012 / Week 16

WEEKLY MARKET REPORT April 2th, 212 / Week 16 For a second consecutive week the BDI continued to increase, ending the week above the 1, benchmark (1,67 points / +9.77%) for the first time since 16th January

WEEKLY MARKET REPORT April 2th, 212 / Week 16 For a second consecutive week the BDI continued to increase, ending the week above the 1, benchmark (1,67 points / +9.77%) for the first time since 16th January

WEEKLY MARKET REPORT October 12th, 2012 / Week 41

LY MARKET REPORT October 12th, 212 / Week 41 A huge increase in the panamax market with the BPI gaining just over 45% for the week. Panamax charter rates increased significantly as fixing was strengthened

LY MARKET REPORT October 12th, 212 / Week 41 A huge increase in the panamax market with the BPI gaining just over 45% for the week. Panamax charter rates increased significantly as fixing was strengthened

Monday, September 6, Week 36 The Week at a Glance

Monday, September 6, 21 - Week 36 The Week at a Glance "Lesson learned? Guess not." Baltic Dry Indices* Last Fridays Closing Weekly Difference Baltic Dry Index 2876 164 Baltic Cape index 3937 488 Baltic

Monday, September 6, 21 - Week 36 The Week at a Glance "Lesson learned? Guess not." Baltic Dry Indices* Last Fridays Closing Weekly Difference Baltic Dry Index 2876 164 Baltic Cape index 3937 488 Baltic

WEEKLY MARKET REPORT December 16th, 2011 / Week 50

LY MARKET REPORT December 16th, 211 / Week 5 The market saw a correction this week on weaker demand for the capesize sector. After a positive end on Monday both the BDI and BCI fell for the remainder of

LY MARKET REPORT December 16th, 211 / Week 5 The market saw a correction this week on weaker demand for the capesize sector. After a positive end on Monday both the BDI and BCI fell for the remainder of

Monday, July 25, Week 30 The Week at a Glance

Baltic Dry Indices* Last Fridays Closing Weekly Difference Monday, July 25, 211 - Week 3 The Week at a Glance Butterfly effect..." Officials of the Euro-zone have come into agreement to assist Greece with

Baltic Dry Indices* Last Fridays Closing Weekly Difference Monday, July 25, 211 - Week 3 The Week at a Glance Butterfly effect..." Officials of the Euro-zone have come into agreement to assist Greece with

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 11th October, 21 Volume 326 Week 41 Sale & Purchase Activity Week 41 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 11th October, 21 Volume 326 Week 41 Sale & Purchase Activity Week 41 SECOND HAND SALES DRY TONNAGE

WEEKLY MARKET REPORT March 9th, 2012 / Week 10

WEEKLY MARKET REPORT March 9th, 2012 / Week 10 Yet another week with the smaller sizes outperforming the others. The BSI and BHSI ended nearly 16% and over 7% higher respectively. Whilst the BCI ended

WEEKLY MARKET REPORT March 9th, 2012 / Week 10 Yet another week with the smaller sizes outperforming the others. The BSI and BHSI ended nearly 16% and over 7% higher respectively. Whilst the BCI ended

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 2th June, 211 Volume 362 Week 25 Sale & Purchase Activity Week 25 SECOND HAND SALES DRY TONNAGE Type

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 2th June, 211 Volume 362 Week 25 Sale & Purchase Activity Week 25 SECOND HAND SALES DRY TONNAGE Type

WEEKLY MARKET REPORT November 19th, 2010 / Week 46

WEEKLY MARKET REPORT November 19th, 2010 / Week 46 A difficult week for the panamax market with the BPI losing 327 points representing a loss of almost 14%. The BDI fell nearly 7% mostly due to the sharp

WEEKLY MARKET REPORT November 19th, 2010 / Week 46 A difficult week for the panamax market with the BPI losing 327 points representing a loss of almost 14%. The BDI fell nearly 7% mostly due to the sharp

WEEKLY MARKET REPORT September 27th, 2013 / Week 39

LY MARKET REPORT September 27th, 2013 / Week 39 During the last two days of the week the BCI made a u-turn eroding all of the gains made until Wednesday and ended the week 51 points in the red. The momentum

LY MARKET REPORT September 27th, 2013 / Week 39 During the last two days of the week the BCI made a u-turn eroding all of the gains made until Wednesday and ended the week 51 points in the red. The momentum

WEEKLY MARKET REPORT December 9th, 2011 / Week 49

LY MARKET REPORT December 9th, 211 / Week 49 Lower iron ore prices have increased demand and helped raise freight rates in the capesize sector with the BCI ending nearly 8.5% higher. The panamax sector

LY MARKET REPORT December 9th, 211 / Week 49 Lower iron ore prices have increased demand and helped raise freight rates in the capesize sector with the BCI ending nearly 8.5% higher. The panamax sector

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

WEEKLY MARKET REPORT February 13th, 2015 / Week 07

LY MARKET REPORT February 13th, 2015 / Week 07 The only positive note in the depressed freight market is the panamax index which gained 69 points, an increase of approximately 16%. All other indices remain

LY MARKET REPORT February 13th, 2015 / Week 07 The only positive note in the depressed freight market is the panamax index which gained 69 points, an increase of approximately 16%. All other indices remain

Weekly Dry Bulk Report

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

Weekly Market Report. Issue: Week 18 Wednesday 6 th May Market insight

Weekly Market Report Issue: Week 18 Wednesday 6 th May 2014 Market insight By John N. Cotzias SnP Broker A bit more favorable wind is forecasted for 2014 for the Greek Passenger Shipping Companies. Most

Weekly Market Report Issue: Week 18 Wednesday 6 th May 2014 Market insight By John N. Cotzias SnP Broker A bit more favorable wind is forecasted for 2014 for the Greek Passenger Shipping Companies. Most

WEEKLY MARKET REPORT October 8th, 2010 / Week 40

LY MARKET REPORT October 8th, 2010 / Week 40 Surprisingly, even though China is still on holiday, the spot capesize rates have shot up to US$ 40,000 per day and as a result charterers are coming out for

LY MARKET REPORT October 8th, 2010 / Week 40 Surprisingly, even though China is still on holiday, the spot capesize rates have shot up to US$ 40,000 per day and as a result charterers are coming out for

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st July 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH JULY 217

MONTHLY MARKET OVERVIEW 1st 31st July 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH JULY 217

OFFSHORE MONTHLY MARKET OVERVIEW

OFFSHORE MONTHLY MARKET OVERVIEW 1 st 3 th November 17 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity +44 () 3 6 vesselsvalue.com OFFSHORE VALUES

OFFSHORE MONTHLY MARKET OVERVIEW 1 st 3 th November 17 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity +44 () 3 6 vesselsvalue.com OFFSHORE VALUES

WEEKLY MARKET REPORT March 2nd, 2012 / Week 9

WEEKLY MARKET REPORT March 2nd, 2012 / Week 9 Whilst the BCI and BPI made small improvements this week, it was the smaller sectors that made the difference pushing the overall BDI to a 7% increase. The

WEEKLY MARKET REPORT March 2nd, 2012 / Week 9 Whilst the BCI and BPI made small improvements this week, it was the smaller sectors that made the difference pushing the overall BDI to a 7% increase. The

WEEKLY MARKET REPORT October 17th, 2008 / Week 42

LY MARKET REPORT October 17th, 28 / Week 42 With all the indices in the red for the entire week and with the BDI down to levels last seen early in November 22 there is certainly no change in the mood for

LY MARKET REPORT October 17th, 28 / Week 42 With all the indices in the red for the entire week and with the BDI down to levels last seen early in November 22 there is certainly no change in the mood for

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st July 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JULY 218

MONTHLY MARKET OVERVIEW 1 st 31 st July 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JULY 218

WEEKLY MARKET REPORT February 15th, 2013 / Week 7

LY MARKET REPORT February 15th, 2013 / Week 7 Whilst most indices remained flat or lost some ground this week, the Panamax segment managed to maintain its momentum from last week and posted a significant

LY MARKET REPORT February 15th, 2013 / Week 7 Whilst most indices remained flat or lost some ground this week, the Panamax segment managed to maintain its momentum from last week and posted a significant

WEEKLY MARKET REPORT August 31st, 2012 / Week 35

LY MARKET REPORT August 31st, 2012 / Week 35 The news of the week is the deal involving the sale of Vales' 10 VLOCs which we had sold to them back in 2009-2010 as VLCCs from Vela and were subsequently

LY MARKET REPORT August 31st, 2012 / Week 35 The news of the week is the deal involving the sale of Vales' 10 VLOCs which we had sold to them back in 2009-2010 as VLCCs from Vela and were subsequently

WEEKLY MARKET REPORT June 6th, 2008 / Week 23

LY MARKET REPORT June 6th, 2008 / Week 23 This year's Posidonia was bigger than ever, proving one more time the importance of Greece and Piraeus in particular as one of the largest shipping centers in

LY MARKET REPORT June 6th, 2008 / Week 23 This year's Posidonia was bigger than ever, proving one more time the importance of Greece and Piraeus in particular as one of the largest shipping centers in

WEEKLY MARKET REPORT September 30th, 2011 / Week 39

LY MARKET REPORT September 30th, 2011 / Week 39 The capesize market started to decline early in the week, dragging the general index with it. They both ended the week in the red with the BCI down nearly

LY MARKET REPORT September 30th, 2011 / Week 39 The capesize market started to decline early in the week, dragging the general index with it. They both ended the week in the red with the BCI down nearly

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 28 th February 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW 1 st 28 th February 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

WEEKLY MARKET REPORT April 23rd, 2010 / Week 16

LY MARKET REPORT April 23rd, 21 / Week 16 The BDI remained practically unchanged being pushed upwards by the BCI and at the same time being dragged downwards by the BPI. The capesize market is showing

LY MARKET REPORT April 23rd, 21 / Week 16 The BDI remained practically unchanged being pushed upwards by the BCI and at the same time being dragged downwards by the BPI. The capesize market is showing

WEEKLY MARKET REPORT February 18th, 2011 / Week 7

LY MARKET REPORT February 18th, 2011 / Week 7 The market remained positive for this week as well even though the BCI ended marginally lower. The winners this week were the BCI and BSI which marked an increase

LY MARKET REPORT February 18th, 2011 / Week 7 The market remained positive for this week as well even though the BCI ended marginally lower. The winners this week were the BCI and BSI which marked an increase

WEEKLY MARKET REPORT January 7th, 2011 / Week 1

WEEKLY MARKET REPORT January 7th, 2011 / Week 1 The last time we published the market indices was just before Christmas and up to today we are seeing a continued correction in the capesize market with

WEEKLY MARKET REPORT January 7th, 2011 / Week 1 The last time we published the market indices was just before Christmas and up to today we are seeing a continued correction in the capesize market with

WEEKLY MARKET REPORT March 29th, 2013 / Week 13

LY MARKET REPORT March 29th, 2013 / Week 13 This week, all indices with the exemption of BHSI lost some ground. BSI decreased by 3.48%, while BDI, BCI and BPI lost 2.47%, 2.73% and 2.65% respectively.

LY MARKET REPORT March 29th, 2013 / Week 13 This week, all indices with the exemption of BHSI lost some ground. BSI decreased by 3.48%, while BDI, BCI and BPI lost 2.47%, 2.73% and 2.65% respectively.

WEEKLY MARKET REPORT May 16th, 2014 / Week 20

LY MARKET REPORT May 16th, 2014 / Week 20 The BDI finished positively at 1027 points, up by 30 points even though it started the week with a loss. The panamax segment improved significantly gaining 143

LY MARKET REPORT May 16th, 2014 / Week 20 The BDI finished positively at 1027 points, up by 30 points even though it started the week with a loss. The panamax segment improved significantly gaining 143

WEEKLY MARKET REPORT December 12th, 2014 / Week 50

LY MARKET REPORT December 12th, 2014 / Week 50 The capesize index continued to fall heavily this week posting a loss of just over 40%, dragging the overall index to a weekly loss of just over 12%. The

LY MARKET REPORT December 12th, 2014 / Week 50 The capesize index continued to fall heavily this week posting a loss of just over 40%, dragging the overall index to a weekly loss of just over 12%. The

WEEKLY MARKET REPORT December 5th, 2014 / Week 49

LY MARKET REPORT December 5th, 2014 / Week 49 The freight market continued to soften throughout this week with the BDI concluding at 982 points, down by almost 15%. The index for capesize sector seems

LY MARKET REPORT December 5th, 2014 / Week 49 The freight market continued to soften throughout this week with the BDI concluding at 982 points, down by almost 15%. The index for capesize sector seems

WEEKLY MARKET REPORT September 12th, 2014 / Week 37

LY MARKET REPORT September 12th, 2014 / Week 37 The freight market saw encouraging signs for most of the week and ended up with a 2.25% increase of the BDI at 1181 points. BCI and BHSI had also positive

LY MARKET REPORT September 12th, 2014 / Week 37 The freight market saw encouraging signs for most of the week and ended up with a 2.25% increase of the BDI at 1181 points. BCI and BHSI had also positive

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 35 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 2 nd SEPTEMBER 2011.

MARKET REPORT WEEK 35 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 2 nd SEPTEMBER 2011. The BDI moved up by nearly 13% last week mainly because the BCI enjoyed a fantastic week increasing

MARKET REPORT WEEK 35 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 2 nd SEPTEMBER 2011. The BDI moved up by nearly 13% last week mainly because the BCI enjoyed a fantastic week increasing

WEEKLY MARKET REPORT June 28th, 2013 / Week 26

LY MARKET REPORT June 28th, 2013 / Week 26 The behavior of the market indices were practically a repeat of last week, with the BCI and the BPI increasing nearly 19% and 9% followed by the BSI and BHSI

LY MARKET REPORT June 28th, 2013 / Week 26 The behavior of the market indices were practically a repeat of last week, with the BCI and the BPI increasing nearly 19% and 9% followed by the BSI and BHSI

WEEKLY MARKET REPORT October 5th, 2012 / Week 40

LY MARKET REPORT October 5th, 2012 / Week 40 Despite China being on holiday this week the market was positive in the large sectors (capes and panamaxes) where strong gains were posted. This week's winner

LY MARKET REPORT October 5th, 2012 / Week 40 Despite China being on holiday this week the market was positive in the large sectors (capes and panamaxes) where strong gains were posted. This week's winner

Monday, December 12, Week 50 The Week at a Glance

Baltic Dry Indices* Monday, December 12, 211 - Week 5 The Week at a Glance 'China to the rescue?' Last Fridays Closing Weekly Difference Baltic Dry Index 1922 56 Baltic Cape index 3697 288 Baltic Panamax

Baltic Dry Indices* Monday, December 12, 211 - Week 5 The Week at a Glance 'China to the rescue?' Last Fridays Closing Weekly Difference Baltic Dry Index 1922 56 Baltic Cape index 3697 288 Baltic Panamax

WEEKLY MARKET REPORT February 19th, 2010 / Week 7

LY MARKET REPORT February 19th, 2010 / Week 7 As expected, we have had a relatively quiet week due to the Chinese New Year with the local buyers almost absent from the market. Surprisingly however, the

LY MARKET REPORT February 19th, 2010 / Week 7 As expected, we have had a relatively quiet week due to the Chinese New Year with the local buyers almost absent from the market. Surprisingly however, the

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 14th March, 211 Volume 348 Week 11 Sale & Purchase Activity Week 11 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 14th March, 211 Volume 348 Week 11 Sale & Purchase Activity Week 11 SECOND HAND SALES DRY TONNAGE

WEEKLY MARKET REPORT October 11th, 2013 / Week 41

LY MARKET REPORT October 11th, 2013 / Week 41 The market remained volatile this week for the capesize segment. Whilst the BCI increased early in the week it turned sharply downwards on Wednesday and eventually

LY MARKET REPORT October 11th, 2013 / Week 41 The market remained volatile this week for the capesize segment. Whilst the BCI increased early in the week it turned sharply downwards on Wednesday and eventually

WEEKLY MARKET REPORT January 9th, 2015 / Week 01

LY MARKET REPORT January 9th, 2015 / Week 01 WISHING YOU A HEALTHY, HAPPY AND PROSPEROUS 2015. Like the previous week, all of the indices were in the red throughout this week. The BCI suffered another

LY MARKET REPORT January 9th, 2015 / Week 01 WISHING YOU A HEALTHY, HAPPY AND PROSPEROUS 2015. Like the previous week, all of the indices were in the red throughout this week. The BCI suffered another

Ship Scrapping - Market Pressures. IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 2012

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

MARKET REPORT WEEK 39

MARKET REPORT WEEK 39 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 1 ST OCTOBER 2010. The freight market made no really definitive moves last week whereby the BDI ended practically unchanged.

MARKET REPORT WEEK 39 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 1 ST OCTOBER 2010. The freight market made no really definitive moves last week whereby the BDI ended practically unchanged.

WEEKLY MARKET REPORT November 12th, 2010 / Week 45

WEEKLY MARKET REPORT November 12th, 2010 / Week 45 Another week in the red with the capesize market dragging the BDI to the 2,300 point mark. The BDI lost over 7% whilst the capesize was down almost 10%.

WEEKLY MARKET REPORT November 12th, 2010 / Week 45 Another week in the red with the capesize market dragging the BDI to the 2,300 point mark. The BDI lost over 7% whilst the capesize was down almost 10%.

Monday, September 3, Week 36 The Week at a Glance

Monday, September 3, 212 - Week 36 The Week at a Glance Surprise!! Despite rumors that Russia, due to this year s prolonged drought, were out of the export market, they are in fact competing head to head

Monday, September 3, 212 - Week 36 The Week at a Glance Surprise!! Despite rumors that Russia, due to this year s prolonged drought, were out of the export market, they are in fact competing head to head

WEEKLY SHIPPING MARKET REPORT

WEEKLY SHIPPING MARKET REPORT WEEK 10 (28 th February to 6 th March 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

WEEKLY SHIPPING MARKET REPORT WEEK 10 (28 th February to 6 th March 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

WEEKLY SHIPPING MARKET REPORT WEEK 6

WEEKLY SHIPPING MARKET REPORT WEEK 6 WEEK 6 (6 th February to 12 th February 2016) Market Overview Bulkers For one more week Dry Bulk market follow the negative trend of the last months. Situation has

WEEKLY SHIPPING MARKET REPORT WEEK 6 WEEK 6 (6 th February to 12 th February 2016) Market Overview Bulkers For one more week Dry Bulk market follow the negative trend of the last months. Situation has

WEEKLY SHIPPING MARKET REPORT WEEK 2

Advanced Shipping & Trading S.A 1 st Floor, 168 Vouliagmenis Avenue 16674 Glyfada, Greece Contact Details: Tel: +30 210 3003000 snp@advanced-ship.gr chartering@advanced-ship.gr finance@advanced-ship.gr

Advanced Shipping & Trading S.A 1 st Floor, 168 Vouliagmenis Avenue 16674 Glyfada, Greece Contact Details: Tel: +30 210 3003000 snp@advanced-ship.gr chartering@advanced-ship.gr finance@advanced-ship.gr

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 30 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 29 th JULY 2011.

MARKET REPORT WEEK 30 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 29 th JULY 2011. The dry freight market continues to fall with the BCI losing another -5% w-o-w, the BPI -1.5%, the BSI -1%

MARKET REPORT WEEK 30 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 29 th JULY 2011. The dry freight market continues to fall with the BCI losing another -5% w-o-w, the BPI -1.5%, the BSI -1%

WEEKLY SHIPPING MARKET REPORT

WEEKLY SHIPPING MARKET REPORT WEEK 45 (31 st October to 6 th November 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

WEEKLY SHIPPING MARKET REPORT WEEK 45 (31 st October to 6 th November 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st October 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH OCTOBER

MONTHLY MARKET OVERVIEW 1 st 31 st October 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH OCTOBER

WEEKLY MARKET REPORT June 10th, 2011 / Week 23

LY MARKET REPORT June 10th, 2011 / Week 23 With capesizes once again on the decline (BCI down over 10% for the week) the BDI lost nearly 5% to close just over 1400 points. The gain of the BPI which climbed

LY MARKET REPORT June 10th, 2011 / Week 23 With capesizes once again on the decline (BCI down over 10% for the week) the BDI lost nearly 5% to close just over 1400 points. The gain of the BPI which climbed

ATHENIAN SHIPBROKERS S.A.

17-19, Vas. Pavlou Str., GR 166 73, Voula, Athens, Greece Tel: 21 96597 - Fax: 21 89964 - Tlx: 22626 ATH GR Internet Mail athenian@atheniansa.gr Monthly Report November 28 PRICES TANKERS ($ MIO) 24 25

17-19, Vas. Pavlou Str., GR 166 73, Voula, Athens, Greece Tel: 21 96597 - Fax: 21 89964 - Tlx: 22626 ATH GR Internet Mail athenian@atheniansa.gr Monthly Report November 28 PRICES TANKERS ($ MIO) 24 25

WEEKLY MARKET REPORT February 5th, 2010 / Week 5

LY MARKET REPORT February 5th, 2010 / Week 5 Another negative week as far the indices are concerned but not reflected in the Sale & Purchase market which has had another very active week. The indices started

LY MARKET REPORT February 5th, 2010 / Week 5 Another negative week as far the indices are concerned but not reflected in the Sale & Purchase market which has had another very active week. The indices started

Weekly Market Report Sale & Purchase Newbuilding Secondhand Demoli on Chartering Week 02 Tuesday 18th January 2010

Weekly Market Report Sale & Purchase Newbuilding Secondhand Demoli on Chartering Week 02 Tuesday 18th January 2010 by Yannis Olziersky Broker s insight The Bal c Index has tumbled to its lowest point in

Weekly Market Report Sale & Purchase Newbuilding Secondhand Demoli on Chartering Week 02 Tuesday 18th January 2010 by Yannis Olziersky Broker s insight The Bal c Index has tumbled to its lowest point in

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011.

MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011. Whilst world financial markets continue to concern, and the gold price continues to rise (being seen as

MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011. Whilst world financial markets continue to concern, and the gold price continues to rise (being seen as

MARKET REPORT WEEK 05

MARKET REPORT WEEK 05 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th FEBRUARY 2011 Last week was a predictably quieter one on the shipping markets due to the Chinese New Year Holidays ushering

MARKET REPORT WEEK 05 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th FEBRUARY 2011 Last week was a predictably quieter one on the shipping markets due to the Chinese New Year Holidays ushering

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 38 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 23 rd SEPTEMBER 2011.

MARKET REPORT WEEK 38 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 23 rd SEPTEMBER 2011. Further good volumes of Capesize fixing lifted the BCI another 6% w-o-w now making the average rate

MARKET REPORT WEEK 38 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 23 rd SEPTEMBER 2011. Further good volumes of Capesize fixing lifted the BCI another 6% w-o-w now making the average rate

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 18th October, 21 Volume 327 Week 42 Sale & Purchase Activity Week 42 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 18th October, 21 Volume 327 Week 42 Sale & Purchase Activity Week 42 SECOND HAND SALES DRY TONNAGE

Weekly Market Report. Broker s insight. Chartering (Wet: So er- / Dry: Firm+ ) By Panos Makrinos, SnP Broker

By Panos Makrinos, SnP Broker") Weekly Market Report Issue: Week 33 Tuesday 20 th August 2013 By Panos Makrinos, SnP Broker Broker s insight As everyone in the shipping industry pre y much expected, this was another summer that would

Weekly Market Report Issue: Week 33 Tuesday 20 th August 2013 By Panos Makrinos, SnP Broker Broker s insight As everyone in the shipping industry pre y much expected, this was another summer that would

Weekly Market Report. Broker s insight by John N. Cotzias. Chartering (Wet: Stable+ / Dry: Stable- ) Sale & Purchase (Wet: Stable- / Dry: Stable- )

Sale & Purchase (Wet: Stable- / Dry: Stable- )") Weekly Market Report Week 45 Tuesday 13th November 2012 Broker s insight by John N. Cotzias This year s demoli on sta s cal figures ll end of October show that we are experiencing another superb and never

Weekly Market Report Week 45 Tuesday 13th November 2012 Broker s insight by John N. Cotzias This year s demoli on sta s cal figures ll end of October show that we are experiencing another superb and never

WEEKLY MARKET REPORT

WEEKLY MARKET REPORT Week Ending: 4 th December 2009 (Week 49, Report No: 49/09) (Given in good faith but without guarantee) SUMMARY OF SALES VESSEL TYPE NEW BUILDINGS SEC O ND HAND DEMO LITIO N DEMO LITIO

WEEKLY MARKET REPORT Week Ending: 4 th December 2009 (Week 49, Report No: 49/09) (Given in good faith but without guarantee) SUMMARY OF SALES VESSEL TYPE NEW BUILDINGS SEC O ND HAND DEMO LITIO N DEMO LITIO

Golden Ocean Group Limited Q results March 1, 2007

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st March 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MARCH 217

MONTHLY MARKET OVERVIEW 1st 31st March 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MARCH 217

Monday, July 19, Week 29 The Week at a Glance

Monday, July 19, 21 - Week 29 The Week at a Glance No more bets please We have read that Goldman Sachs has to pay a fine of USD 55 million for the settlement of the well known case. Some players were expecting

Monday, July 19, 21 - Week 29 The Week at a Glance No more bets please We have read that Goldman Sachs has to pay a fine of USD 55 million for the settlement of the well known case. Some players were expecting

Monday, January 25, Week 4 The Week at a Glance

Monday, January 25, 21 - Week 4 The Week at a Glance Baltic Dry Indices* Last Fridays Closing Weekly Difference A Book s cover We thought of being a little philosophical this week! Well, it s an old saying

Monday, January 25, 21 - Week 4 The Week at a Glance Baltic Dry Indices* Last Fridays Closing Weekly Difference A Book s cover We thought of being a little philosophical this week! Well, it s an old saying

WEEKLY MARKET REPORT October 25th, 2013 / Week 43

LY MARKET REPORT October 25th, 2013 / Week 43 The negative momentum in the capesize and panamax market continued throughout the week both losing 17.8% and 7.6% respectively. At the same time, the smaller

LY MARKET REPORT October 25th, 2013 / Week 43 The negative momentum in the capesize and panamax market continued throughout the week both losing 17.8% and 7.6% respectively. At the same time, the smaller

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

WEEKLY MARKET REPORT January 21st, 2011 / Week 3

WEEKLY MARKET REPORT January 21st, 2011 / Week 3 What is happening now in the market is certainly affected by the extraordinary events that have taken place in Australia with the worst flooding in five

WEEKLY MARKET REPORT January 21st, 2011 / Week 3 What is happening now in the market is certainly affected by the extraordinary events that have taken place in Australia with the worst flooding in five

Long Term Trends in Shipbuilding HVB Press Conference. 20 th September 2006 Stephen Gordon, Clarkson Research

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

The World s Largest Buyer of Ships and Offshore Assets

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

Weekly Market Report. Broker s insight

Weekly Market Report Week 43 Tuesday 30th October 2012 by Nikos Papantonopoulos From Green Fields to Green Ships Broker s insight The market for MR vessels has nothing exci ng for one more week. The Atlan

Weekly Market Report Week 43 Tuesday 30th October 2012 by Nikos Papantonopoulos From Green Fields to Green Ships Broker s insight The market for MR vessels has nothing exci ng for one more week. The Atlan

WEEKLY MARKET REPORT May 31st, 2013 / Week 22

LY MARKET REPORT May 31st, 2013 / Week 22 Apart from the supramax sector which rose marginally (BSI up 1.63%) all other segments lost ground for yet another week. Worst affected was the panamax which lost

LY MARKET REPORT May 31st, 2013 / Week 22 Apart from the supramax sector which rose marginally (BSI up 1.63%) all other segments lost ground for yet another week. Worst affected was the panamax which lost

MARKET REPORT WEEK 12

MARKET REPORT WEEK 12 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 25 th MARCH 2011 The Baltic Freight Indices only moved within small bands w-o-w with the Capes being the biggest mover, reversing

MARKET REPORT WEEK 12 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 25 th MARCH 2011 The Baltic Freight Indices only moved within small bands w-o-w with the Capes being the biggest mover, reversing

S&P Market Trends during December: Secondhand Newbuilding Demolition

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 13 th December 2013 (Week 50, Report No: 50/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 13 th December 2013 (Week 50, Report No: 50/13) (Given in good faith but without guarantee)

Monday, November 8, Week 45 The Week at a Glance

Monday, November 8, 21 - Week 45 The Week at a Glance Injection! Fed decided last week to inject about USD 6, billion in treasury bonds (USD 75, billion per month) which led in market reacting positively

Monday, November 8, 21 - Week 45 The Week at a Glance Injection! Fed decided last week to inject about USD 6, billion in treasury bonds (USD 75, billion per month) which led in market reacting positively

MARKET REPORT WEEK 45

MARKET REPORT WEEK 45 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 12 th NOVEMBER 2010 At face value we have just endured another fairly dreary week in the shipping markets with the dry freight

MARKET REPORT WEEK 45 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 12 th NOVEMBER 2010 At face value we have just endured another fairly dreary week in the shipping markets with the dry freight

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st May 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH MAY 217 BULKERS

MONTHLY MARKET OVERVIEW 1st 31st May 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH MAY 217 BULKERS

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 30 th November 2018 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 (0) 203 026 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW 1 st 30 th November 2018 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 (0) 203 026 5555 vesselsvalue.com

MARKET REPORT WEEK 09

MARKET REPORT WEEK 09 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th MARCH 2011 Whilst the BDI improved slightly in all sectors last week we suspect it is far from a being a definite /

MARKET REPORT WEEK 09 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th MARCH 2011 Whilst the BDI improved slightly in all sectors last week we suspect it is far from a being a definite /

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW August SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH AUGUST BULKERS

MONTHLY MARKET OVERVIEW August SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH AUGUST BULKERS

WEEKLY MARKET REPORT March 28th, 2014 / Week 13

LY MARKET REPORT March 28th, 2014 / Week 13 Baltic rates in all dry segments experienced a downturn this week. Major losses in the capesize and panamax sector forced the overall BDI in a 14% decrease compared

LY MARKET REPORT March 28th, 2014 / Week 13 Baltic rates in all dry segments experienced a downturn this week. Major losses in the capesize and panamax sector forced the overall BDI in a 14% decrease compared

WEEKLY SHIPPING MARKET REPORT WEEK 7

WEEKLY SHIPPING MARKET REPORT WEEK 7 WEEK 7 (13 th February to 19 th February 2016) Market Overview Bulkers Chinese New Year celebrations ended affecting the BDI with just a small increase. It would be

WEEKLY SHIPPING MARKET REPORT WEEK 7 WEEK 7 (13 th February to 19 th February 2016) Market Overview Bulkers Chinese New Year celebrations ended affecting the BDI with just a small increase. It would be

Final Results 31 December 2013

Final Results 31 December 2013 Clarkson PLC 10 March 2014 www.clarksons.com Agenda Headline results Divisional performance Business Model & Strategy The market Outlook 10 March 2014 Final Results www.clarksons.com

Final Results 31 December 2013 Clarkson PLC 10 March 2014 www.clarksons.com Agenda Headline results Divisional performance Business Model & Strategy The market Outlook 10 March 2014 Final Results www.clarksons.com