Weekly Market Insight Friday, 20th July 2018

|

|

|

- Regina Chandler

- 5 years ago

- Views:

Transcription

1 Weekly Market Insight Amid fresh escalation in trade tension between the US and China, commodity prices followed a downward path during the last period. Concerns that the tit-for-tat tariff war could derail the global economy had a negative bearing to market sentiment. Additionally, recent data from Beijing indicating a rather softer tone in Chinese growth has influenced commodity investor outlook. Bit further back the upsurge in commodity prices since early 2016 whetted commodity producers appetite for increased production volumes. Indicatively, the Russian energy minister announced last Friday that oil production could be increased more sharply than what had been agreed in Vienna. This announcement came in a period when there were rumours in the market that Washington is considering releasing some of its emergency oil reserves ahead of the November midterm to counteract the higher prices that Americans have been seeing at the pumps. In this context, after touching a three-year high in early July, Brent the international oil benchmark dropped to low $70s per barrel this week. On a very similar tone, iron ore producers ramped up their production. In its full-year operational review, BHP says it produced Mt for the year above its April guidance after rising to 72 Mt during the June quarter. In sync, Vale achieved a new record quarterly production of 96.8 Mt of iron ore, despite the nationwide truck drivers strike in May. Rio Tinto expected iron ore shipments for the year to be at the upper end of its range of 330 Mt to 340 Mt, driven by productivity improvements and fewer weather-related disruptions. Under these circumstances, iron ore price drifted lower to mid $60s pmt. Contents Spot Market...2 FFA Market..5 Bunker Market..8 S&P Market.9 Distant Past Market.12 Oddly, whilst miners and oil producers have seen a window of opportunity to increase their production levels for enhancing their revenues, investors in the dry bulk sector managed, in the most, to stay away from the yards. In contrast to 2014, the current upswing in the freight rates has had a minor impact on dry bulk s orderbook. Standing at a tad above 80 million, on DWT terms, sector s orderbook hovered very close to its lowest levels in the last twelve years. In fact, one should go back to early 2006 in order to find similar levels to this. Obviously, the uncertainty surrounding the new regulations, the limited access to traditional financing and the attractive secondhand prices have in combine played a major role in the calmer tone of the newbuilding market. Doric Shipbrokers S.A. Tel: Fax: drycargo@doric.gr Inquiries about the content of this report Michalis Voutsinas research@doric.gr Adding up to the aforementioned, the moderate level of vessel deliveries during the current trading year and the positive news from the demand end have enabled the dry bulk sector to steer the ship carefully and hopefully avoid the trade war reef which has reared its head. Freight market 120yrs ago (page 12): Although comparatively little chartering has been effected during the week, the markets are firmer and especially for forward loading, indicating that the worst for this year has been seen Doric Shipbrokers, Research Page 1

2 Dry Cargo Spot Market The general index touched new 2018 record high levels of 1721 on Tuesday, but it finished the week 32 points lower than that. Capesizes started the week strong, pushing the BCI above the 3335 points on Tuesday. However, the rest of the week was not so hot for the largest bulkers. For the third week in a row Panamaxes reported gains, concluding at 1557 points, last seen in end March. After a period of downward movement, geared bulkers turned positive. Having spent seven trading days in the three-digit territory, BSI ended at 1023 points this Friday. Reporting marginal gains, BHSI balanced at 560 points at this week closing. At the box office, Capesize ROCE continued outperforming all other segments, hovering at double-digit percentages of 10.87%. Being just few basis points apart, Panamax ROCE and Supramax ROCE lay at 5.71% and 5.43% respectively. Handy returns moved up at last, yet remaining less than two cents in every dollar invested. Baltic Freight Indices Date BDI BCI 5TC BPI - TCA BSI - TCA BHSI - TCA 16-Jul $24,987 $12,244 $10,951 $8, Jul $25,580 $12,254 $11,007 $8, Jul $24,710 $12,246 $11,061 $8, Jul $23,827 $12,307 $11,155 $8, Jul $24,446 $12,457 $11,232 $8, month High 1743 $30,475 $13,740 $12,356 $10, month Low 933 $7,051 $8,765 $8,486 $6, month Avg 1306 $17,145 $11,153 $10,603 $8,557 Avg. Cal $15,129 $9,766 $9,168 $7,636 Avg. Cal $7,388 $5,562 $6,236 $5,214 *Return on Capital Employed (ROCE) is the ratio of net operating profit of an investment to its capital employed. It measures the profitability of an investment by expressing its operating profit as a percentage of its capital employed. In other words, ROCE assesses how much profit an investment earns on every dollar employed. Doric Shipbrokers, Research Page 2

3 Capesizes trended sideways during the 29th week of the current trading year, concluding at BCI TC levels of $24,446 daily. In a week that all major miners reported strong increases in their production output, the largest bulkers reported 1.6% weekly gains, with all but transatlantic indices pointing up. In the commodity spectrum of the Pacific, BHP s metallurgical coal production for the 2018 financial year increased by seven per cent to a record 43 Mt. Production is expected to increase to between 43 and 46 Mt in the 2019 financial year, according to the company s operational review for the year ended on 30 June Additionally, energy coal production for the 2018 financial year was flat at 29 Mt. Output is expected to remain broadly unchanged at approximately 28 to 29 Mt in the 2019 financial year. In reference to the freight market, the Baltic C5 index reported a marginal increase of 0.6% on a weekly basis, concluding at $8.95 pmt. RGL booked the 'Ocean Road' (179,147 dwt, 2009) at $8.50 if Port Hedland load or $8.60 if Dampier. The 'Anangel Grace' (180,391 dwt, 2010) was reported fixed with prompt delivery Dalian for a trip via Australia and redelivery Singapore-Japan at $25,400 daily. The Baltic transpacific index (C10_14) ended higher at $21,508 daily, or 3.4% W-o-W. For a NoPac round, the 'Genco Commodus' (169,098 dwt, 2009) concluded at $19,000 daily, basis delivery Hadong and redelivery South Korea. In the Atlantic basin, Vale achieved record sales volumes of iron ore and pellets totaled 86.5 Mt in Q2 18, or some 4.8 Mt higher than in Q2 17. The record was achieved despite the increase of offshore stocks to support the ongoing blending activities. Furthermore, Anglo American said inspection work on a pipeline that carries iron ore from its Minas Rio mine in Brazil to a port would be completed by the end of the year. As far as the freight market is concerned, the Baltic C3 index concluded marginally up at $ pmt. On such a run, Cargill fixed the 'Maria Maria' (177,878 dwt, 2014) for a 1-10 August cargo from Tubarao to Qingdao at $ The fronthaul index (C9_14) concluded at $42,750 daily whereas the Transatlantic index (C8_14) balanced at $29,075 daily, or higher by 1.6% and slightly lower by 2% W-o-W respectively. Jera allegedly took the 'Winning Nature' (181,387 dwt, 2014) from Gibraltar 26 July for a trip via Drummond to Icdas, Turkey at $30,000 daily. There was no period activity reported this week. Representative Capesize Fixtures Vessel DWT Built Delivery Date Re-del Rate Charterers Comment Genco Commodus 169, Hadong 23-Jul South Korea approx $19,000 Panocean in d/c via NoPac Anangel Grace 180, Dalian 22/25 Jul Singapore-Japan $25,400 cnr via Australia Brave Sailor 176, Pyeongtaek prompt Singapore-Japan $22,000 Hyundai Glovis via Australia in d/c Lowlands Longevity 173, Liuheng end July Singapore-Japan $21,500 cnr via Australia or NoPac The Panamax market was affected by a low-paying pacific, which forbade the TC Average index from picking up more than 1.8% w-o-w. In the Atlantic, almost 20 fixtures surfaced out of ECSA, solidifying optimism among Owners. The pacific market was slightly busier this week but rates moved sideways. Limited fresh enquiry out of major load ports has put further pressure to spot-prompt tonnage. Australian coal exports headlined again this week, but rates did not show any excitement, following last week s trend. 'Semiramis' (82,301 dwt, 2013) fixed an uninspiring $11,000 for a coal trip with July, delivery Ube to China. On the smaller size, 'Coral Diamond' (76,596 dwt, 2007) opted for a reposition to India, closer to a seemingly healthier and promising ECSA forward market. She was concluded at $10,000 daily for an East Australian coal trip to India. Indonesian coal activity was weak, with deflated rates across the board, paying on and off $10,000 daily for South China delivery on LMEs. It was reported that Cape Race (81,400 dwt, 2012) was done at $11,500 daily with deliver at HK, to India. No noteworthy movement out of NoPac, this week as well. 'Star Laura' (82,209 dwt, 2006) rumored fixed at $12,300 daily with delivery at Ulsan for one round trip, loading at Prince Rupert. The Atlantic basin was fairly positive this week with the majority of trades concluding slightly over the last done. The Baltic market has produced quite strong fixtures. 'Key Opus' (81,863 dwt, 2015) managed $18,000 with prompt delivery Ghent via Murmansk to Turkey, with redelivery Cape Passero. There were talks of an improving Black sea grain market, with strong offers from owners side, but no actual fixtures emerged to support this argument. Across the pond, the North has absorbed a great deal of tonnage. 'Sinochart Beijing' (81,664 dwt, 2012) fixed at $16,500 daily with prompt delivery Belfast for a mineral round trip via US East Coast back to ARA range. Out of the US Gulf, 'BTG Olympos' (80,800 dwt, 2015) fixed at $22,000 daily with delivery July Hamburg via USG to Indonesia and routing via Cape of Good Hope. Further South, 'Wookie' (81,755 dwt, 2012) fixed at circa $16,500 daily plus $650,000 GBB for a front-haul grain trip via Itaqui to China. North Brazil was more active on the iron ore trade as well, following the rumors of last week, on Capesize stem splits. The busy North has brought further improvement to July slots out of ECSA market, with offers rising up to high $16,000 plus high $600,000 gbb. August loading at ECSA seems to be slightly softer, with recent fixtures, ranging circa $13,000 daily levels ex ECI on kamsarmax and slightly less on Panamax. Modigliani' (81,767 dwt, 2013) reported agreeing at $13,000 with retro sailing delivery Ennore. TA activity out of Brazil has also picked up this week, with rates ranging between $19-22,000 depending on size, dates and redelivery. Late in the week the 'Taho Europe' (84,549 dwt, 2018) fixture emerged at $15,750 with July cancelling and delivery at Yeosu for 1 year (plus the option of another) suggesting a strong premium over the spot market. Representative Panamax Fixtures Vessel DWT Built Delivery Date Re-del Rate Charterers Comment Semiramis 82, Ube 22/26 July China $11,000 Dreyfus via Eaus Coral Diamond 76, Ube prompt India $10,000 Sinoeast via Eaus Star Laura 82, Ulsan 22/23 July Singapore-Japan $12,300 MOL via P.Rupert Cape Race 81, Hong Kong 19/20 July India $11,500 cnr via Indo Modigliani 81, retro Ennore 13 July Singapore-Japan $13,000 Caravel via ECSA Wookie 81, Itaqui 30 July China $16, k Cargill Sinochart Beijing 81, Belfast prompt ARA $16,500 Bunge via USEC Key Opus 81, Ghent prompt Cape Passero $18,000 Klaveness via Baltic/Turkey BTG Olympos 80, Hamburg 23/25 July Indonesia $22,000 Omegra via USG/COGH Taho Europe 84, Yeosu 28/30 July worldwide $15,750 WW Bulk 1 + 1yr Doric Shipbrokers, Research Page 3

4 With a 2.8% weekly increase, Supramaxes have seen the BSI TCA moving higher to $11,232 daily. The market in the Pacific returned to positive territory at least in terms of index levels as the overall trading remained suppressed. The average of the Pacific routes climbed a slight 2.8 percent w-o-w which was strongly supported by the presence of fresh activity in the Indonesian coal front. For such a run, "Trenta" (56,838 dwt, 2010) was done at $10,250 basis delivery Singapore for a trip via Indo to South China. In the north, market was slack but the "Cos Prosperity" (55,676dwt, 2006) stood out as she was able to secure $9,000 with delivery Dalian for a trip to Vietnam The level of the fixture points out to CIS trading being involved. On backhaul runs, rumours had a 63k dwt open at Cjk fixing a trip to the Mediterranean at $8,000 for the first 60 days and $13,000 therafter but no further details surfaced. Out of South Africa much improved rates were noticed. The "Alis" (58,000dwt, 2013) was fixed basis delivery Port Elizabeth for a run to Singapore/Japan range at $13,000 plus $325,000 ballast bonus, which was around $125,000 better than last done. In the Atlantic, rates stayed in the green for the third consecutive week. From the USG, there was information that a couple of small Ultramax Units were fixed for trips to the Mediterranean at mid $18,000 levels. The Bulk Peru (57,937 dwt, 2011) secured $23,000 daily basis delivery SW Pass, for a trip to WCSA. ECSA hovered close to last week s levels, with transatlantic trips to the Mediterranean paying close to $16,000 levels on Supramax units, basis delivery South Brazil or Argentina. It was heard that Silver Lady (50,329 dwt, 2003) fetched $13,250 daily plus $325,000 ballast bonus for a trip via ECSA to Australia with grains. Across the pond, the SSI Formidable (63,510 dwt, 2017) achieved a healthy $19,900 daily for a grain cargo from the Continent to Singapore-Japan range. Scrap cargoes to the Eastern Mediterranean were trading at discounted rates, mainly due to Owners expectations that the Black Sea will remain firm for the weeks to come, thus being considered as a favourable repositioning area. On this route, the Kestrel I (50,351 dwt, 2004) was fixed at $11,500 daily, basis delivery Sauda. The Black Sea solidified the strength it gained last week, without further bursts though. The Ever Progress (56,592 dwt, 2012) was linked to a charter from Samsun to PG at $20,000 daily. Period-wise, the Darya Jaya (63,584 dwt, 2017) was fixed for 2/3 laden legs, basis delivery Mississippi and redelivery Singapore-Japan range at $14,000 daily plus $400,000 ballast bonus. Representative Supramax Fixtures Vessel DWT Built Delivery Date Re-del Rate Charterers Comment Cos Prosperity 55, Dalian 25 Jul Vietnam $9,000 cnr Trenta 56, Singapore Jul South China $10,350 Ausca Shipping trip via Indonesia Alis 58, Port Elizabeth prompt Singapore-Japan range $12,800 +$280K bb Oldendorff Bulk Peru 57, SW Pass prompt WCSA $23,000 cnr Silver Lady 50, ECSA prompt Australia $13,250 +$325K bb cnr SSI Formidable 60, ECSA prompt Singapore-Japan range $15,250 +$525K bb ADMI Spar Libra 53, Belfast prompt Turkey $11,500 EMR intention scrap Ever Progress 56, Samsun prompt PG $20,000 cnr Darya Jaya 63, Mississippi prompt Singapore-Japan range $14,000 +$400K cnr for 2/3 ll Signs of improvement in the Far East moderate optimism in the Atlantic on the Handysize. Week 29 ends today and the market sentiment from the East is positive for the Handies. After several weeks of decline, rates are improving both North of Taiwan but also in South East Asia. Indicatively Pan Amber (38,000 dwt, 2012) open at Makassar on the 15th of July fixed at $9,250 dop for grains via Australia to Singapore/Japan. Another example of the improved levels we witnessed is the fixture of Majesty (34,000 dwt, 2012). The ship was open at Cigading on the 22nd of July, and achieved $10,750 basis dop for alumina via Australia to the Persian Gulf. One could argue that redelivery in Persian Gulf would deserve a premium hire but on the other hand there are rumours being heard of ships fixing around $10-11,000 for trips from PG back to Singapore Japan. Up in the north, Gloria Island (28,400 dwt, 2012) open at Moji on the 20th of July managed $9500 dop for a trip with steels via Japan to Thailand. In the Atlantic basin, Black Sea and ECSA kept the good vibes going whereas the USG moderated the optimism. In the Mediterranean / Black Sea region, 'Marina R' (37,785 dwt, 2010) was reported fixed at $9,500 for an inter-med trip with grains, basis delivery Canakkale and redelivery Egypt. Rumors surfaced of a similar vessel with same delivery concluding at $10,500 for a trip to Israel with Grain. The Continent remained relatively stable during the week, with the 'SFL Medway' (34,000 dwt, 2012) securing a basic $8,000 for a demanding timber trade trip via Finland to Egypt with Skaw delivery. However some grain parcels out of France seem to willing close to the low teens region for W. Africa trades. In ECSA, the situation is improving but far from great with Integrity bulk rating a modern eco 37K bulker at $13,000 for TCT with grains to Venezuela, basis APS Imbituba. Additionally, the 'Almirante Storni' (31,797 dwt, 2012) open Aratu prompt dates fixed at $12,000 for a coastal trip. Finally in USG, the positive momentum in the market of the largest bulkers didn t pass through to the Handysize segment, with not so much fixtures reported. We have heard J Lauritzen fixed a 39,000 dwat vessel at $8,500 basis delivery aps USEC to full Brazil redelivery. On the period desk, consensus seems to be that levels are in low $10Ks for larger Handies showing signs of optimism. Representative Handysize Fixtures Vessel DWT Built Delivery Date Re-del Rate Charterers Comment Pan Amber 38, Makassar Prompt Spore - Japan $9,250 cnr grains via Australia Majesty 34, Cigading Prompt Persian Gulf $10,750 cnr alumina via Australia Gloria Island 28, Moji Prompt Thailand $9,500 cnr SFL Medway 34, Skaw Prompt Egypt $8,000 cnr via Finaland Almirante Storni 31, Aratu Prompt Brazil $12,000 cnr Marina R 37, Canakkale Prompt Egypt $9,500 cnr inter-med grains Doric Shipbrokers, Research Page 4

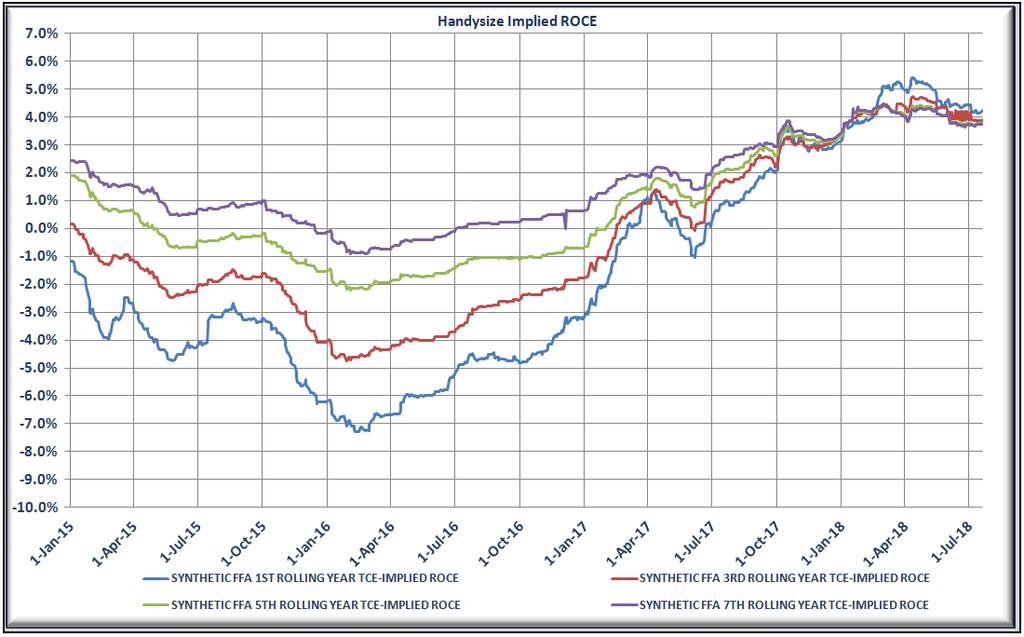

5 FFA Market In a lukewarm week for the FFA market, forward curves remained virtually unchanged. Despite the negative tone on Cape paper on the early side of the week, prompt months closed substantially higher, with August balancing at $22,140 daily and September at $23,090 daily. The short end of the Panamax curve concluded marginally above last Friday s levels, with both August and September finishing higher at $12,360 and $12,540 respectively. In the opposite direction from their spot market, the Supramax forward market moved down, with September balancing at $12,320 and October at $12,320. The prompt Handysize contracts reported marginal gains to August levels of $9,288. The back ends of all segments remained at previous levels without significant changes. Capesize first rolling year implied ROCE moved up to 6.2% this week, while at the same time the returns of Panamax followed closely to 5.4%. Geared segments implied ROCEs remained unchanged, with Supramax concluding at 6.5% and Handy at 4.2%. Doric Shipbrokers, Research Page 5

6 Doric Shipbrokers, Research Page 6

7 BFA Cape 5TC Date July (18) Aug (18) Sept (18) Q3 (18) Q4 (18) Q1 (19) Cal 19 Cal 24 Cal Jul-18 $23,140 $21,070 $22,060 $22,090 $23,650 $14,110 $19,173 $15,480 $15, Jul-18 $22,840 $20,540 $21,590 $21,657 $23,360 $13,870 $18,968 $15,410 $15, Jul-18 $22,700 $20,240 $21,430 $21,457 $23,420 $13,840 $18,940 $15,370 $15, Jul-18 $23,055 $20,960 $22,095 $22,037 $23,730 $13,960 $19,050 $15,370 $15, Jul-18 $23,660 $22,140 $23,090 $22,963 $24,305 $14,170 $19,250 $15,410 $15,410 Week High $23,660 $22,140 $23,090 $22,963 $24,305 $14,170 $19,250 $15,480 $15,480 Week Low $22,700 $20,240 $21,430 $21,457 $23,360 $13,840 $18,940 $15,370 $15,370 Week Avg $23,079 $20,990 $22,053 $22,041 $23,693 $13,990 $19,076 $15,408 $15,410 BFA Panamax 4TC Date July (18) Aug (18) Sept (18) Q3 (18) Q4 (18) Q1 (19) Cal 19 Cal 24 Cal Jul-18 $11,725 $12,070 $12,235 $12,010 $12,330 $11,130 $12,165 $9,740 $9, Jul-18 $11,640 $11,930 $12,055 $11,875 $12,160 $11,060 $12,063 $9,730 $9, Jul-18 $11,595 $11,940 $12,075 $11,870 $12,200 $11,120 $12,090 $9,730 $9, Jul-18 $11,765 $12,070 $12,200 $12,012 $12,330 $11,210 $12,195 $9,730 $9, Jul-18 $11,810 $12,360 $12,540 $12,237 $12,550 $11,470 $12,360 $9,760 $9,730 Week High $11,810 $12,360 $12,540 $12,237 $12,550 $11,470 $12,360 $9,760 $9,730 Week Low $11,595 $11,930 $12,055 $11,870 $12,160 $11,060 $12,063 $9,730 $9,705 Week Avg $11,707 $12,074 $12,221 $12,001 $12,314 $11,198 $12,175 $9,738 $9,714 BFA Supra 5TC Date July (18) Aug (18) Sept (18) Q3 (18) Q4 (18) Q1 (19) Cal 19 Cal 24 Cal Jul-18 $11,165 $11,825 $12,310 $11,767 $12,555 $11,150 $12,140 $10,020 $10, Jul-18 $11,070 $11,715 $12,152 $11,646 $12,485 $11,110 $12,120 $9,990 $9, Jul-18 $11,054 $11,694 $12,159 $11,635 $12,469 $11,115 $12,160 $10,000 $10, Jul-18 $11,030 $11,720 $12,149 $11,633 $12,479 $11,100 $12,160 $10,020 $10, Jul-18 $11,100 $11,930 $12,320 $11,783 $12,540 $11,140 $12,180 $10,040 $10,050 Week High $11,165 $11,930 $12,320 $11,783 $12,555 $11,150 $12,180 $10,040 $10,050 Week Low $11,030 $11,694 $12,149 $11,633 $12,469 $11,100 $12,120 $9,990 $9,990 Week Avg $11,084 $11,777 $12,218 $11,693 $12,506 $11,123 $12,152 $10,014 $10,016 BFA Handysize TC Date July (18) Aug (18) Sept (18) Q3 (18) Q4 (18) Q1 (19) Cal 19 Cal 24 Cal Jul-18 $8,313 $9,238 $9,650 $9,067 $9,850 $8,938 $9,213 $9,125 $9, Jul-18 $8,288 $9,163 $9,650 $9,033 $9,838 $8,938 $9,219 $9,125 $9, Jul-18 $8,275 $9,225 $9,663 $9,054 $9,863 $8,950 $9,225 $9,138 $9, Jul-18 $8,275 $9,263 $9,688 $9,075 $9,875 $8,975 $9,225 $9,138 $9, Jul-18 $8,275 $9,288 $9,713 $9,092 $9,888 $8,988 $9,250 $9,150 $9,138 Week High $8,313 $9,288 $9,713 $9,092 $9,888 $8,988 $9,250 $9,150 $9,138 Week Low $8,275 $9,163 $9,650 $9,033 $9,838 $8,938 $9,213 $9,125 $9,125 Week Avg $8,285 $9,235 $9,673 $9,064 $9,863 $8,958 $9,226 $9,135 $9,128 Doric Shipbrokers, Research Page 7

8 Bunker Market Rotterdam Singapore Fujairah Gibraltar Houston Date ($/mt) IFO 380 MGO IFO 380 MGO IFO 380 MGO IFO 380 MGO IFO 380 MGO 16-Jul-18 $429 $624 $462 $648 $451 $691 $450 $669 $439 $ Jul-18 $420 $623 $456 $643 $444 $702 $444 $662 $428 $ Jul-18 $414 $618 $450 $641 $450 $705 $440 $656 $438 $ Jul-18 $416 $617 $454 $640 $442 $705 $442 $664 $446 $ Jul-18 $418 $618 $455 $642 $452 $715 $444 $665 $447 $ month High $446 $665 $478 $701 $476 $739 $477 $738 $462 $ month Low $287 $438 $301 $461 $301 $540 $308 $484 $290 $ month Avg $362 $562 $384 $584 $382 $641 $382 $610 $363 $597 Singapore 20-Jul-18 Week max Week low Week Avg RTDM Jul-18 Week max Week low Week Avg Aug-18 $437.7 $437.7 $423.0 $429.3 Aug-18 $414.7 $414.7 $402.3 $407.9 Sep-18 $428.2 $428.2 $416.0 $421.5 Sep-18 $408.4 $408.4 $396.8 $402.3 Oct-18 $422.4 $422.4 $411.5 $416.6 Oct-18 $403.9 $403.9 $392.5 $398.0 Nov-18 $418.7 $418.7 $408.3 $413.1 Nov-18 $399.9 $399.9 $388.5 $394.1 Dec-18 $415.2 $415.2 $405.0 $409.9 Dec-18 $396.4 $396.4 $385.0 $390.7 Jan-19 $411.7 $411.7 $402.8 $406.9 Jan-19 $393.9 $393.9 $382.8 $388.4 Q4-18 $418.8 $418.8 $408.3 $413.2 Q4-18 $400.1 $400.1 $388.7 $394.3 Q1-19 $408.9 $408.9 $399.8 $404.1 Q1-19 $391.3 $391.3 $379.7 $385.5 Q2-19 $398.9 $398.9 $389.8 $394.3 Q2-19 $380.8 $380.8 $368.9 $375.0 Q3-19 $377.9 $377.9 $363.0 $368.9 Q3-19 $355.6 $355.6 $341.9 $348.6 CAL19 $377.1 $377.9 $370.5 $374.4 CAL19 $355.3 $355.4 $348.7 $352.2 CAL20 $305.1 $305.1 $297.5 $301.8 CAL20 $292.6 $292.6 $281.7 $288.6 CAL21 $322.3 $322.4 $310.7 $318.2 CAL21 $306.6 $306.6 $294.2 $302.3 CAL22 $340.3 $343.0 $335.2 $339.1 CAL22 $322.6 $322.6 $310.2 $318.3 Doric Shipbrokers, Research Page 8

9 Dry Bulk S&P Market Just one month after the acquisition of four secondhand bulkers, the New-York-listed Genco made headlines once again, with the purchase of two secondhand Capesizes. According to company s announcement, Genco has entered into an agreement to acquire two 2016 South Korean built 180,000 dwt Capesize vessels for an en bloc purchase price of approximately $98 million. Furthermore, the company announced this week that it has sold two of its older Handysize vessels, the Genco Explorer (29,952 dwt, 1999) and the Genco Progress (29,952 dwt, 1999), as part of its fleet renewal program. The aggregate sale price for the two vessels is approximately $11.2 million. Given that the largest bulkers tend to outperform during strong freight rate environment, Genco s investment rotation can be seen as a vote of confidence in the current rally. In our secondhand to age-adjusted newbuilding comparison, the market for ten-year-old Capesizes and same-aged Panamaxes hovered at just 12% and 2% off their adjusted newbuilding prices respectively. Ten-year-old Supramaxes are on the market at just 6% less than their newbulding price, if we compare them on the same age basis, whereas same-aged Handies at a larger discount of 14%. Indicative Ten-Year-Old Prices Date/$ mil. Capesize 180K DWT Panamax 75K DWT Handymax 56k DWT Handysize 32K DWT 13-Jul Jul Jul Δ% Υ-ο-Υ 30.0% 22.2% 20.8% 46.9% Δ% % 63.0% 50.0% 62.5% Reported Recent S&P Activity Vessel Name DWT Built Yard/Country Price $Mil. Buyer Comments Malena 180, Hanjin HI/S.Korea 49 Genco part of en bloc NSS Fortune 184, Mitsui/Japan mid 15 Undisclosed Hanton Trader VI 81, Jiangsu New Hantong/China 24.3 Undisclosed Key Mission 82, Tsuneishi/Japan 22 Undisclosed Rena 81, STX/S. Korea mid-high 18 Undisclosed auction sale BBG Ambition 82, Tsuneishi Zhoushan/China Greek Buyers F.D.Vittorio Raiola 76, Shin Kasado/Japan mid-high 17 Undisclosed Toro 76, Imabari/Japan low 15 Undisclosed Poseidon 75, HHI/S.Korea 9.5 Undisclosed DD due Energy Prosperity 77, Sasebo/Japan 7.8 Undisclosed SBI Echo 61, Imabari/Japan 19 Undisclosed Incl. 5-yr BBB Bao Tong 63, Chengxi/China 21.3 Undisclosed C 4x36 Geraldine Manx 58, Tsuneishi Zhoushan/China 15.5 Undisclosed C 4x30 Ocean Skipper 56, Xingang/China low 11 Undisclosed C 4x30 Bulk Power 57, Zhoushan/China 11.5 Chinese Buyers C 4x30 Navios Armonia 55, Kawasaki/Japan 14.2 Greek Buyers C 4x30 Anna 52, Sanoyas/Japan 9 Chinese Buyers C 4x30 Christina 50, Jiangnan/China 8 Chinese Buyers C 4x30 Tamarita 52, Tsuneishi Cebu/Philippines 8.5 Chinese Buyers C 4x30 Paraskevi 45, China Shipbuilding/Taiwan 4.8 Undisclosed C 4x30 Nord Auckland 36, Hyundai-Vinashin/Vietnam 13.3 Undisclosed C 4x30 Maple Glory 32, Taizhou Maple/China 10 Undisclosed C 4x30.5 Tequila Sunrise 31, Saiki/Japan mid 11 Undisclosed C 4x30 Sider Dream 33, Hakodate/Japan 9.5 Undisclosed C 4x30 Oriente Shine 31, Hakodate/Japan 7.2 Chinese Buyers C 4x30 Global Standard 28, Shimanami Zosen/Japan 10 Undisclosed C 4x30.5 Genco Progress 29, Oshima/Japan 5.6 Undisclosed C 4x30 Chikusa 17, Kurinoura/Japan 6.5 Undisclosed C 3x25 Tobin's Q* Capesize-Panamax Date Capesize 5yrs Capesize 10yrs Capesize 15yrs Panamax 5yrs Panamax 10yrs Panamax 15yrs Current ratio 94% 88% 79% 86% 98% 90% 12months High 98% 88% 81% 95% 102% 102% 12months Low 87% 74% 65% 86% 87% 75% 12months Avg 93% 82% 75% 90% 95% 93% Tobin's Q* Supramax-Handysize Date Supramax 5yrs Supramax 10yrs Supramax 15yrs Handysize 5yrs Handysize 10yrs Handysize 15yrs Current ratio 87% 94% 98% 90% 86% 72% 12months High 91% 98% 107% 91% 87% 76% 12months Low 84% 85% 79% 81% 64% 59% 12months Avg 89% 94% 98% 86% 79% 69% Doric Shipbrokers, Research Page 9

10 Doric Shipbrokers, Research Page 10

11 Doric Shipbrokers, Research Page 11

12 Market Insight 120 years ago By: Michalis Voutsinas, Doric Shipbrokers S.A. and Angela Papanastasatou, Tufton Oceanic Ltd. Weekly Spot Market Current week Previous week Jun-98 May-98 Apr-98 Implied Spot Roce 7.7% 4.8% 9.5% 23.6% 14.5% Global Spot TCE BlackSea Round East Round Med Round US Round River Plate Round S&P Market (5,000dwt) Current week Previous week Jun-98 May-98 Apr-98 NB 36,104 36,104 35,167 33,892 33,317 SH 5yrs old 27,034 27,034 27,962 26,587 26,677 SH 10yrs old 20,727 20,727 21,630 20,376 20,476 SH 15yrs old 15,562 15,562 16,558 15,275 15,400 Doric Shipbrokers, Research Page 12

13 History does not repeat itself but it does rhyme We have warned owners against fixing ahead for autumn loading from the Black Sea direction, as there is later on bound to be a big demand for tonnage, corresponding to the enormous crops, a large percentage of which must be shipped over August, September and October. This accounts for the feverish anxiety of the speculators and chartering agents to secure tonnage forward, knowing that the prospects of their making a profit of probably even shillings per unit will be if they are successful in obtaining tonnage all in their favour. In this context, the average returns on capital employed in shipping during this week (21-July-1898) reported gains, concluding at 7.7%. We understand that several boats have again been secured from the Danube for September and October loading for Antwerp or Rotterdam on the berth terms contracts, but at an advance on the rates recently paid. For obvious reasons the charterers are making it a sine qua non with the owners and brokers that these fixtures shall be kept secret, for their game is to have as much cheap tonnage up their sleeves as they can get to deal with later on; and probably in the interests of the non-fixers ahead it is best that these fixtures should not leak out, as it would be to the advantage of the bona fide merchants to know that ultimately the speculative charterers will be bound to play their trump cards by taking tonnage at much higher rates, with a view of forcing the markets up to such a level that will enable them to re-let their pocket fixtures at substantial profits. If owners who indiscreetly contemplate operating ahead were to demand charter terms and a declaration of shippers or merchants names, then they would probably find that the negotiations would be abruptly broken off. Plenty of firms would take cheap tonnage ahead, knowing they would have all to gain and in case of disaster nothing to lose. It is not a great while ago that a certain Danube firm, now defunct, when the crisis came had not got 200 to pay differences and yet notwithstanding such a warning there are still plenty of owners who will commit their tonnage months ahead to chartering firms without making the slightest inquiry into their financial standing. As we said last week in regard to the berth rates, they will accept what amounts to the speculators verbal promise to load if convenient. The cotton charterers are mostly skirmishing, hoping to capture a few cheap boats to set the ball rolling; but we cannot hear of any success. The longer they wait the better for shipowners, as in September and October they will have to compete for tonnage with very different markets to what we have at present. In the meantime, they are apparently trying to cover themselves to an infinitesimal extent by taking tonnage up on the so-called net grain charter. These charters permit the shipment of any lawful merchandise, therefore having chartered a boat on the open charter basis they can ship a cargo of cotton or part cotton to any port between Bordeaux and Hamburg inclusive. These net charters are favoured by a great many owners who have insufficient experience of general charters; the probable profits are easily calculated, but these owners apparently lose sight of the contingency of being ordered to Hamburg, Bordeaux, etc. and having to make a voyage back to the UK on their own account. Surely the equivalent on the n.r.t. basis, or even the lb. basis for cotton to Liverpool must be better than going to the Elbe or Weser on the net charter. In the spot arena, the Black Sea market is considerably firmer, with berth rates from Odessa for L.H.A.R. being 9s 1.5d and for later loading 9s 7d. From Nicolaieff cargo can be engaged ahead 1s per unit over the Odessa rates. Danube rates are hardening, with berth rates for July loading to Antwerp-Rotterdam range being 11s 9d, for August 12s 9d and September/October 14s 9d. Mediterranean rates are generally better. From Alexandria business has been done to UK on the basis 11s orders or 10s direct, which can be repeated and probably improved upon. From Smyrna, one or two fixtures have been effected to the EC UK ports at about 9s 9d on the deadweight. Not much ore chartering has been done, but rates are harder and the next fixtures reported should indicate an advance. There is not much to report in the American market. From the Northern range, berth grain rates to UK/Cont. for July loading are 2s 3d per quarter and for August 2s 8d. Rather more business has been doing for phosphate, one or two boats having been fixed from Pensacola to Genoa for July/August loading at 19s 2d. From British North America, there is a large and increasing demand for tonnage, as the shippers and charterers now know from last year s experience that if they do not get August tonnage they will have to pay enormous rates to obtain even a few boats for September loading, resulting, if they cannot pay those rates, in their having to stock their deals on the other side for the winter. Eastern business has been quiet, only one or two fixtures being reported. There is no change to report in the River Plate market. In the miscellaneous markets, there appears to be rather more demand for tonnage, especially for time-charter for US account at rates varying from 7s 3d to 7s 9d for periods ranging from three to nine months. On the S&P front, both the newbulding and the secondhand market remained stable at previously reported levels. A typical newbuilding 5,000dwt British-build steamer is currently at the market for 36,100, or up 20.8% on a yearly basis, whereas a ten-year old of the same dwt and specification at 20,700, or 21.8% Y-o-Y. Doric Shipbrokers, Research Page 13

Weekly Dry Bulk Report

2-215 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 12 1 8 6 4 2 HIGHLIGHTS Capesize: Still quiet market Panamax: Continued slide in rates L&S INDEX OF DRY BULK STOCKS* Index

2-215 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 12 1 8 6 4 2 HIGHLIGHTS Capesize: Still quiet market Panamax: Continued slide in rates L&S INDEX OF DRY BULK STOCKS* Index

GULF MARITIME SHIPBROKERS & CONSULTANTS K U W A I T beyond shipbrokers

GULF MARITIME SHIPBROKERS & CONSULTANTS K U W A I T beyond shipbrokers First Licensed Shipbroker in Kuwait 13 May 212 Dry Cargo Weekly Market Report Department Phone email General Info +965 2259 8822 general@gulf-maritime.com

GULF MARITIME SHIPBROKERS & CONSULTANTS K U W A I T beyond shipbrokers First Licensed Shipbroker in Kuwait 13 May 212 Dry Cargo Weekly Market Report Department Phone email General Info +965 2259 8822 general@gulf-maritime.com

Dry Bulk Market Weekly Highlights Week 17 - Dry Cargo Market Highlights for the period of 21-April-2011 until 28-April-2011

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Weekly Dry Bulk Report

44 ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Firming rates throughout the week in both basins Panamax: Another week of firming rates in all sectors CAPESIZE During an active Monday, both the

44 ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Firming rates throughout the week in both basins Panamax: Another week of firming rates in all sectors CAPESIZE During an active Monday, both the

Weekly Dry Bulk Report

5 ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Few shipments into China Panamax: Rates still declining L&S INDEX OF DRY BULK STOCKS* Index 214 Index 215 CAPESIZE PANAMAX Rates

5 ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Few shipments into China Panamax: Rates still declining L&S INDEX OF DRY BULK STOCKS* Index 214 Index 215 CAPESIZE PANAMAX Rates

Weekly Dry Bulk Report

9 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Boost in fixtures for C5 towards the weekend Panamax: Pacific activity slowly increasing

9 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 85 65 45 25 HIGHLIGHTS Capesize: Boost in fixtures for C5 towards the weekend Panamax: Pacific activity slowly increasing

Weekly Dry Bulk Report

12 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Relatively flat in the Pacific Front haul, reasonably quiet Panamax: Firming rates for tonnage fixing

12 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: Relatively flat in the Pacific Front haul, reasonably quiet Panamax: Firming rates for tonnage fixing

Weekly Dry Bulk Report

49 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 95 85 75 65 55 45 35 HIGHLIGHTS Capesize: BCI down 31% w-o-w Panamax: Slightly firming BPI L&S INDEX OF DRY BULK STOCKS*

49 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 15 95 85 75 65 55 45 35 HIGHLIGHTS Capesize: BCI down 31% w-o-w Panamax: Slightly firming BPI L&S INDEX OF DRY BULK STOCKS*

Weekly Dry Bulk Report

Week 36 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 3th 214 HIGHLIGHTS Capesize: Generally lower rates this week Supramax/Handymax: Continued improved market for both segments

Week 36 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 3th 214 HIGHLIGHTS Capesize: Generally lower rates this week Supramax/Handymax: Continued improved market for both segments

Weekly Dry Bulk Report

22 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: A more active market throughout the week Panamax: Front haul market saw slightly more activity, not enough

22 -Shipbrokers and consultants since 1919- ly Dry Bulk Report 22 May 3th 214 HIGHLIGHTS Capesize: A more active market throughout the week Panamax: Front haul market saw slightly more activity, not enough

Weekly Dry Bulk Report

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

Week 46 -Shipbrokers and consultants since 1919- Weekly Dry Bulk Report Week 22 May 30th 2014 Capesize: Market continues to fall Panamax: BPI-TCA falling 9 per cent from last Friday CAPESIZE The Capesize

Weekly Market Insight Friday, 22nd June 2018

Weekly Market Insight While forecasts remain positive for the short-term prospects of the sector and many market participants have taken long positions in the period market, spot market seems directionless

Weekly Market Insight While forecasts remain positive for the short-term prospects of the sector and many market participants have taken long positions in the period market, spot market seems directionless

Weekly Market Insight Friday, 25th January 2019

Weekly Market Insight With such a discouraging week start, it would have been of a great surprise to see things progressing on a merry tone. China s economic growth dropped to its slowest annual rate in

Weekly Market Insight With such a discouraging week start, it would have been of a great surprise to see things progressing on a merry tone. China s economic growth dropped to its slowest annual rate in

Weekly Market Insight Friday, 19th October 2018

Weekly Market Insight Fuelled by an upward trending freight market, asset prices in the secondhand market started off the current trading year on the right foot. After the typically weakest month of the

Weekly Market Insight Fuelled by an upward trending freight market, asset prices in the secondhand market started off the current trading year on the right foot. After the typically weakest month of the

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

Golden Ocean Group Limited Q results March 1, 2007

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Weekly Market Insight Friday, 14th September 2018

Weekly Market Insight Although sentiment and analysts projections remain bullish for the rest of the trading year, the BDI decided to ruin the party moving further south this week balancing below 1400

Weekly Market Insight Although sentiment and analysts projections remain bullish for the rest of the trading year, the BDI decided to ruin the party moving further south this week balancing below 1400

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 30 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 29 th JULY 2011.

MARKET REPORT WEEK 30 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 29 th JULY 2011. The dry freight market continues to fall with the BCI losing another -5% w-o-w, the BPI -1.5%, the BSI -1%

MARKET REPORT WEEK 30 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 29 th JULY 2011. The dry freight market continues to fall with the BCI losing another -5% w-o-w, the BPI -1.5%, the BSI -1%

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA - WEEKLY October 3rd, 2008 OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings BULK CARRIERS 'Marigold' 46,745tdw Blt 04/82 Korea, Krs M/E Sulzer Cr 3x20t,

OPTIMA - WEEKLY October 3rd, 2008 OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings BULK CARRIERS 'Marigold' 46,745tdw Blt 04/82 Korea, Krs M/E Sulzer Cr 3x20t,

Dry Bulk Insight. Market firm but volatile. Our view. contents Summary 01

Dry Bulk Insight Monthly Analysis of the Dry Bulk ket issue 49 april 8 Radarwatch Farmers strike in Argentina hits Panamax and Handy rates in the Atlantic Australian miners and Chinese steelmakers still

Dry Bulk Insight Monthly Analysis of the Dry Bulk ket issue 49 april 8 Radarwatch Farmers strike in Argentina hits Panamax and Handy rates in the Atlantic Australian miners and Chinese steelmakers still

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

Dry Bulk Insight. Some term comfort. Our view. contents Summary 01

Dry Bulk Insight Monthly Analysis of the Dry Bulk Market issue 59 Radarwatch Argentina is facing worst drought in a decade thus curtailing its grain trade Pessimism continues to loom in newbuild market

Dry Bulk Insight Monthly Analysis of the Dry Bulk Market issue 59 Radarwatch Argentina is facing worst drought in a decade thus curtailing its grain trade Pessimism continues to loom in newbuild market

Dry Bulk Insight. Prices and rates fall as suppliers fight. contents Summary 01

Dry Bulk Insight Monthly Analysis of the Dry Bulk Market issue 61 april 9 Radarwatch The prolonged ore negotiations pulled the market down as rates declined despite increase in chartering volumes Bangladeshi

Dry Bulk Insight Monthly Analysis of the Dry Bulk Market issue 61 april 9 Radarwatch The prolonged ore negotiations pulled the market down as rates declined despite increase in chartering volumes Bangladeshi

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

Weekly Market Insight Friday, 16th November 2018

Weekly Market Insight Shortly before it collided with the 1000-point wall, Baltic Dry Index managed to hit the brakes, avoiding the crash on the last moment. Whilst the major threes of the dry bulk spectrum,

Weekly Market Insight Shortly before it collided with the 1000-point wall, Baltic Dry Index managed to hit the brakes, avoiding the crash on the last moment. Whilst the major threes of the dry bulk spectrum,

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 35 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 2 nd SEPTEMBER 2011.

MARKET REPORT WEEK 35 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 2 nd SEPTEMBER 2011. The BDI moved up by nearly 13% last week mainly because the BCI enjoyed a fantastic week increasing

MARKET REPORT WEEK 35 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 2 nd SEPTEMBER 2011. The BDI moved up by nearly 13% last week mainly because the BCI enjoyed a fantastic week increasing

COSCO CORPORATION. (SINGAPORE) LTD FY2003 Full Year Results. Presentation

LTD FY2003 Full Year Results. Presentation") COSCO CORPORATION (SINGAPORE) LTD FY2003 Full Year Results Presentation 11 February 2004 1 Outline of Presentation 1. Background & Corporate Restructuring Exercise 2. Operations Review 3. Financial Review

COSCO CORPORATION (SINGAPORE) LTD FY2003 Full Year Results Presentation 11 February 2004 1 Outline of Presentation 1. Background & Corporate Restructuring Exercise 2. Operations Review 3. Financial Review

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st July 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JULY 218

MONTHLY MARKET OVERVIEW 1 st 31 st July 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JULY 218

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011.

MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011. Whilst world financial markets continue to concern, and the gold price continues to rise (being seen as

MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011. Whilst world financial markets continue to concern, and the gold price continues to rise (being seen as

WEEKLY SHIPPING MARKET REPORT WEEK 6

WEEKLY SHIPPING MARKET REPORT WEEK 6 WEEK 6 (6 th February to 12 th February 2016) Market Overview Bulkers For one more week Dry Bulk market follow the negative trend of the last months. Situation has

WEEKLY SHIPPING MARKET REPORT WEEK 6 WEEK 6 (6 th February to 12 th February 2016) Market Overview Bulkers For one more week Dry Bulk market follow the negative trend of the last months. Situation has

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

MARKET REPORT WEEK 05

MARKET REPORT WEEK 05 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th FEBRUARY 2011 Last week was a predictably quieter one on the shipping markets due to the Chinese New Year Holidays ushering

MARKET REPORT WEEK 05 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th FEBRUARY 2011 Last week was a predictably quieter one on the shipping markets due to the Chinese New Year Holidays ushering

MARKET REPORT WEEK 39

MARKET REPORT WEEK 39 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 1 ST OCTOBER 2010. The freight market made no really definitive moves last week whereby the BDI ended practically unchanged.

MARKET REPORT WEEK 39 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 1 ST OCTOBER 2010. The freight market made no really definitive moves last week whereby the BDI ended practically unchanged.

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

I The shipping market contents ISL

Comment - Charts and Tables concerning The Shipping Market World Merchant Fleet Tanker Market Bulk Carrier Market Tab. 1 Additions/Reductions by Ship Types 2014-2016 and up to June 2017... III Tab. 2 Size

Comment - Charts and Tables concerning The Shipping Market World Merchant Fleet Tanker Market Bulk Carrier Market Tab. 1 Additions/Reductions by Ship Types 2014-2016 and up to June 2017... III Tab. 2 Size

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 28 th February 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW 1 st 28 th February 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

WEEKLY SHIPPING MARKET REPORT WEEK 7

WEEKLY SHIPPING MARKET REPORT WEEK 7 WEEK 7 (13 th February to 19 th February 2016) Market Overview Bulkers Chinese New Year celebrations ended affecting the BDI with just a small increase. It would be

WEEKLY SHIPPING MARKET REPORT WEEK 7 WEEK 7 (13 th February to 19 th February 2016) Market Overview Bulkers Chinese New Year celebrations ended affecting the BDI with just a small increase. It would be

LPG & Petrochemical Shipping: Current Status & Outlook. A better market, but for how long? Nicola Williams, Clarksons March 16th 2005

LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams, Clarksons March 16th 2005 The LPG Shipping Market today The LPG freight market started to move

LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams, Clarksons March 16th 2005 The LPG Shipping Market today The LPG freight market started to move

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st July 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH JULY 217

MONTHLY MARKET OVERVIEW 1st 31st July 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH JULY 217

WEEKLY SHIPPING MARKET REPORT WEEK 25

WEEKLY SHIPPING MARKET REPORT WEEK 25 WEEK 25 (17 th Jun to 24 th Jun 2016) Market Overview During this week BDI closed at 609 and returned back to levels of 2 weeks before, having an increase of 22 points

WEEKLY SHIPPING MARKET REPORT WEEK 25 WEEK 25 (17 th Jun to 24 th Jun 2016) Market Overview During this week BDI closed at 609 and returned back to levels of 2 weeks before, having an increase of 22 points

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 11th October, 21 Volume 326 Week 41 Sale & Purchase Activity Week 41 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 11th October, 21 Volume 326 Week 41 Sale & Purchase Activity Week 41 SECOND HAND SALES DRY TONNAGE

Demand, Supply & Capacity in the Shipbuilding Industry

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 14th March, 211 Volume 348 Week 11 Sale & Purchase Activity Week 11 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 14th March, 211 Volume 348 Week 11 Sale & Purchase Activity Week 11 SECOND HAND SALES DRY TONNAGE

Baltic Exchange Indices Calculation methods and upcoming regulation International Maritime Statistics Forum April 2013

Baltic Exchange Indices Calculation methods and upcoming regulation International Maritime Statistics Forum April 2013 Robin King Head of Marketing History 1700 1744 Virginia and Baltick Coffee House 1800

Baltic Exchange Indices Calculation methods and upcoming regulation International Maritime Statistics Forum April 2013 Robin King Head of Marketing History 1700 1744 Virginia and Baltick Coffee House 1800

Final Results 31 December 2013

Final Results 31 December 2013 Clarkson PLC 10 March 2014 www.clarksons.com Agenda Headline results Divisional performance Business Model & Strategy The market Outlook 10 March 2014 Final Results www.clarksons.com

Final Results 31 December 2013 Clarkson PLC 10 March 2014 www.clarksons.com Agenda Headline results Divisional performance Business Model & Strategy The market Outlook 10 March 2014 Final Results www.clarksons.com

WEEKLY SHIPPING MARKET REPORT

WEEKLY SHIPPING MARKET REPORT WEEK 42 (10 rd October to 16 th October 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

WEEKLY SHIPPING MARKET REPORT WEEK 42 (10 rd October to 16 th October 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA - WEEKLY January 11th, 2008 WEEKLY REPORT OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings BULK CARRIERS 'Golden Sentosa' 170,500tdw Blt 08/08 Daehan,

OPTIMA - WEEKLY January 11th, 2008 WEEKLY REPORT OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings BULK CARRIERS 'Golden Sentosa' 170,500tdw Blt 08/08 Daehan,

MARKET REPORT WEEK 12

MARKET REPORT WEEK 12 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 25 th MARCH 2011 The Baltic Freight Indices only moved within small bands w-o-w with the Capes being the biggest mover, reversing

MARKET REPORT WEEK 12 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 25 th MARCH 2011 The Baltic Freight Indices only moved within small bands w-o-w with the Capes being the biggest mover, reversing

S&P Market Trends during December: Secondhand Newbuilding Demolition

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 13 th December 2013 (Week 50, Report No: 50/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 13 th December 2013 (Week 50, Report No: 50/13) (Given in good faith but without guarantee)

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007.

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007. Athens, Greece, November 15, 2007. Globus Maritime Limited (AIM: GLBS), a

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007. Athens, Greece, November 15, 2007. Globus Maritime Limited (AIM: GLBS), a

Danish Shipping. Facts and Figures. June 2018

Danish Shipping Facts and Figures June 2018 2 Table of Contents 1. Danish Shipping Industry 4 The Danish Merchant Fleet 4 Danish Shipping Exports 6 Employment 8 CEO Survey 10 2. Global Merchant Fleet 12

Danish Shipping Facts and Figures June 2018 2 Table of Contents 1. Danish Shipping Industry 4 The Danish Merchant Fleet 4 Danish Shipping Exports 6 Employment 8 CEO Survey 10 2. Global Merchant Fleet 12

WEEKLY SHIPPING MARKET REPORT WEEK 28

WEEKLY SHIPPING MARKET REPORT WEEK 28 WEEK 28 (8 th Jul to 15 th Jul 2016) Market Overview During this week BDI, improved day by day, having a weekly closing at 745 points with an increase of 42 points

WEEKLY SHIPPING MARKET REPORT WEEK 28 WEEK 28 (8 th Jul to 15 th Jul 2016) Market Overview During this week BDI, improved day by day, having a weekly closing at 745 points with an increase of 42 points

Long Term Trends in Shipbuilding HVB Press Conference. 20 th September 2006 Stephen Gordon, Clarkson Research

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 2th June, 211 Volume 362 Week 25 Sale & Purchase Activity Week 25 SECOND HAND SALES DRY TONNAGE Type

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 2th June, 211 Volume 362 Week 25 Sale & Purchase Activity Week 25 SECOND HAND SALES DRY TONNAGE Type

Panamax & Post-Pmx Market Outlook

Panamax & Post-Pmx Market Outlook (an analysis of the fleet profile, trade prospects, and rates) Aug 2018 bancosta blue studies volume DRY 2018/#10 research www.bancosta.com ; research@bancosta.com Aug

Panamax & Post-Pmx Market Outlook (an analysis of the fleet profile, trade prospects, and rates) Aug 2018 bancosta blue studies volume DRY 2018/#10 research www.bancosta.com ; research@bancosta.com Aug

MARKET REPORT WEEK 09

MARKET REPORT WEEK 09 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th MARCH 2011 Whilst the BDI improved slightly in all sectors last week we suspect it is far from a being a definite /

MARKET REPORT WEEK 09 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th MARCH 2011 Whilst the BDI improved slightly in all sectors last week we suspect it is far from a being a definite /

Information meeting. Third quarter results. March 2011

Information meeting Third quarter 2010-11 results 1 March 2011 Agenda 2010-11: recovery in activity and return to profitability Current issues Air France-KLM ambitions for the next three years 2 All businesses

Information meeting Third quarter 2010-11 results 1 March 2011 Agenda 2010-11: recovery in activity and return to profitability Current issues Air France-KLM ambitions for the next three years 2 All businesses

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st October 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH OCTOBER

MONTHLY MARKET OVERVIEW 1 st 31 st October 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH OCTOBER

MARKET REPORT WEEK 45

MARKET REPORT WEEK 45 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 12 th NOVEMBER 2010 At face value we have just endured another fairly dreary week in the shipping markets with the dry freight

MARKET REPORT WEEK 45 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 12 th NOVEMBER 2010 At face value we have just endured another fairly dreary week in the shipping markets with the dry freight

Ship Scrapping - Market Pressures. IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 2012

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Index of business confidence. Monthly FTK (Billions) Aug 2013 vs. Aug 2012 YTD 2013 vs. YTD 2012 Aug 2013 vs. Jul 2013

Aug 2013 vs. Aug 2012 YTD 2013 vs. YTD 2012 Aug 2013 vs. Jul 2013") AIR PASSENGER MARKET ANALYSIS AUGUST 2013 KEY POINTS Air travel markets expanded strongly in August. Global revenue passenger kilometers were up 6.8% compared to a year ago, an improvement on July growth

AIR PASSENGER MARKET ANALYSIS AUGUST 2013 KEY POINTS Air travel markets expanded strongly in August. Global revenue passenger kilometers were up 6.8% compared to a year ago, an improvement on July growth

WEEKLY MARKET REPORT December 16th, 2011 / Week 50

LY MARKET REPORT December 16th, 211 / Week 5 The market saw a correction this week on weaker demand for the capesize sector. After a positive end on Monday both the BDI and BCI fell for the remainder of

LY MARKET REPORT December 16th, 211 / Week 5 The market saw a correction this week on weaker demand for the capesize sector. After a positive end on Monday both the BDI and BCI fell for the remainder of

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 19

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 19 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 11 th May 2012. There is not much excitement to write about this Monday as last week was fairly

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 19 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 11 th May 2012. There is not much excitement to write about this Monday as last week was fairly

Industry Update. ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL

Industry Update ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL U.S. & Canadian GDP 8% 6% 4% U.S.* Canada** Estimate by BEA as of 02/11/16 2% 0% -2% -4% -6% -8% -10% The U.S. economy

Industry Update ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL U.S. & Canadian GDP 8% 6% 4% U.S.* Canada** Estimate by BEA as of 02/11/16 2% 0% -2% -4% -6% -8% -10% The U.S. economy

REPORT. VisitEngland Business Confidence Monitor Wave 5 Autumn

REPORT VisitEngland Business Confidence Monitor 2011 5-7 Museum Place Cardiff, Wales CF10 3BD Tel: ++44 (0)29 2030 3100 Fax: ++44 (0)29 2023 6556 www.strategic-marketing.co.uk Page 2 of 31 Contents Page

REPORT VisitEngland Business Confidence Monitor 2011 5-7 Museum Place Cardiff, Wales CF10 3BD Tel: ++44 (0)29 2030 3100 Fax: ++44 (0)29 2023 6556 www.strategic-marketing.co.uk Page 2 of 31 Contents Page

Tourism Snapshot. A focus on the markets in which the CTC and its partners are active. February 2015 Volume 11, Issue 2.

Tourism Snapshot Tourism Whistler/Mike Crane A focus on the markets in which the CTC and its partners are active www.canada.travel/corporate February Volume 11, Issue 2 Key highlights The strong beginning

Tourism Snapshot Tourism Whistler/Mike Crane A focus on the markets in which the CTC and its partners are active www.canada.travel/corporate February Volume 11, Issue 2 Key highlights The strong beginning

WEEKLY SHIPPING MARKET REPORT WEEK 20

WEEKLY SHIPPING MARKET REPORT WEEK 20 WEEK 20 (13 th May to 20 th May 2016) Market Overview One step closer to the end of the first half of the year and BDI trying hard to give us a sentiment of amelioration.

WEEKLY SHIPPING MARKET REPORT WEEK 20 WEEK 20 (13 th May to 20 th May 2016) Market Overview One step closer to the end of the first half of the year and BDI trying hard to give us a sentiment of amelioration.

The World s Largest Buyer of Ships and Offshore Assets

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

Tourism Snapshot. June 2015 Volume 11, Issue 6. A focus on the markets in which Destination Canada (DC) and its partners are active.

and its partners are active.") Tourism Snapshot Tourism PEI / Paul Baglole A focus on the markets in which Destination Canada (DC) and its partners are active. www.destinationcanada.com June Volume 11, Issue 6 Key highlights Over the

Tourism Snapshot Tourism PEI / Paul Baglole A focus on the markets in which Destination Canada (DC) and its partners are active. www.destinationcanada.com June Volume 11, Issue 6 Key highlights Over the

MARKET REPORT WEEK 27 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 9 th JULY 2010.

MARKET REPORT WEEK 27 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 9 th JULY 2010. The BDI collectively and individually fell for a 6th straight week which means that between cob Fri 28th

MARKET REPORT WEEK 27 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 9 th JULY 2010. The BDI collectively and individually fell for a 6th straight week which means that between cob Fri 28th

WEEKLY MARKET REPORT July 16th, 2010 / Week 28

LY MARKET REPORT July 16th, 21 / Week 28 All indices have continued their downward trend for another week, as the capesize rates continued their downward spiral. Very poor demand for iron ore has put pressure

LY MARKET REPORT July 16th, 21 / Week 28 All indices have continued their downward trend for another week, as the capesize rates continued their downward spiral. Very poor demand for iron ore has put pressure

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 3th June 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JUNE 217 BULKERS

MONTHLY MARKET OVERVIEW 1st 3th June 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JUNE 217 BULKERS

A History of the Baltic indices:

A History of the Baltic indices: All amendments and changes contained within this document are highlighted in bold italic, 1985 4 January 1985 - The Baltic Exchange commences publication of a daily freight

A History of the Baltic indices: All amendments and changes contained within this document are highlighted in bold italic, 1985 4 January 1985 - The Baltic Exchange commences publication of a daily freight

Monday, September 6, Week 36 The Week at a Glance

Monday, September 6, 21 - Week 36 The Week at a Glance "Lesson learned? Guess not." Baltic Dry Indices* Last Fridays Closing Weekly Difference Baltic Dry Index 2876 164 Baltic Cape index 3937 488 Baltic

Monday, September 6, 21 - Week 36 The Week at a Glance "Lesson learned? Guess not." Baltic Dry Indices* Last Fridays Closing Weekly Difference Baltic Dry Index 2876 164 Baltic Cape index 3937 488 Baltic

WEEKLY SHIPPING MARKET REPORT WEEK 2

Advanced Shipping & Trading S.A 1 st Floor, 168 Vouliagmenis Avenue 16674 Glyfada, Greece Contact Details: Tel: +30 210 3003000 snp@advanced-ship.gr chartering@advanced-ship.gr finance@advanced-ship.gr

Advanced Shipping & Trading S.A 1 st Floor, 168 Vouliagmenis Avenue 16674 Glyfada, Greece Contact Details: Tel: +30 210 3003000 snp@advanced-ship.gr chartering@advanced-ship.gr finance@advanced-ship.gr

MARKET REPORT WEEK 13

MARKET REPORT WEEK 13 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 1 st APRIL 2011 Last week ended up a disappointment on the freight side with only the BHSI making any gain albeit less than

MARKET REPORT WEEK 13 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 1 st APRIL 2011 Last week ended up a disappointment on the freight side with only the BHSI making any gain albeit less than

Braemar Seascope. Market Indicator. TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )

TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y )") Weekly Chartering Report Thursday, 3 ch 211 Braemar Seascope ket Indicator Wet 2--11 Avg Avg YTD 21 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26, NHC

Weekly Chartering Report Thursday, 3 ch 211 Braemar Seascope ket Indicator Wet 2--11 Avg Avg YTD 21 Avg TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) TC E ( U S $ / D a y ) 26, NHC

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

WEEKLY SHIPPING MARKET. REPORT WEEK 34 WEEK 34 (22 th Aug to 26 th Aug 2016) Market Overview. Bulkers. Tankers. Demolition

Market Overview. Bulkers. Tankers. Demolition") WEEKLY SHIPPING MARKET WEEKLY REPORT SHIPPING WEEK MARKET 20 REPORT WEEK 34 WEEK 34 (22 th Aug to 26 th Aug 2016) Market Overview One step closer to the end of the summer and BDI is staying in a continuous

WEEKLY SHIPPING MARKET WEEKLY REPORT SHIPPING WEEK MARKET 20 REPORT WEEK 34 WEEK 34 (22 th Aug to 26 th Aug 2016) Market Overview One step closer to the end of the summer and BDI is staying in a continuous

2012 RESULT PRESENTATION

212 RESULT PRESENTATION BJÖRN ROSENGREN, PRESIDENT & CEO 25 JANUARY 213 Wärtsilä Net sales back to growth with stable profitability 212 development Order intake EUR 4,94 million, +9% Net sales EUR 4,725

212 RESULT PRESENTATION BJÖRN ROSENGREN, PRESIDENT & CEO 25 JANUARY 213 Wärtsilä Net sales back to growth with stable profitability 212 development Order intake EUR 4,94 million, +9% Net sales EUR 4,725

Monthly Traffic Results Frankfurt Airport

with 9M-Report 1 January 2 February 3 March 4 April 5 May 6 June 7 July 8 August 9 September 10 October 11 November 12 December Traffic category Passengers (arr.+dep.+transit) Airfreight (metric tons)

with 9M-Report 1 January 2 February 3 March 4 April 5 May 6 June 7 July 8 August 9 September 10 October 11 November 12 December Traffic category Passengers (arr.+dep.+transit) Airfreight (metric tons)

PETROFIN RESEARCH Greek shipping companies January 2018 based on data as of December 2017

1 2017 RESEARCH AND ANALYSIS: GREEK SHIPPING COMPANIES 1ST PART OF 2017 PETROFIN RESEARCH Petrofin Research are pleased to announce the release of the first part of their 2017 Greek Shipping research.

1 2017 RESEARCH AND ANALYSIS: GREEK SHIPPING COMPANIES 1ST PART OF 2017 PETROFIN RESEARCH Petrofin Research are pleased to announce the release of the first part of their 2017 Greek Shipping research.

WEEKLY MARKET REPORT October 12th, 2012 / Week 41

LY MARKET REPORT October 12th, 212 / Week 41 A huge increase in the panamax market with the BPI gaining just over 45% for the week. Panamax charter rates increased significantly as fixing was strengthened

LY MARKET REPORT October 12th, 212 / Week 41 A huge increase in the panamax market with the BPI gaining just over 45% for the week. Panamax charter rates increased significantly as fixing was strengthened

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 38 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 23 rd SEPTEMBER 2011.

MARKET REPORT WEEK 38 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 23 rd SEPTEMBER 2011. Further good volumes of Capesize fixing lifted the BCI another 6% w-o-w now making the average rate

MARKET REPORT WEEK 38 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 23 rd SEPTEMBER 2011. Further good volumes of Capesize fixing lifted the BCI another 6% w-o-w now making the average rate

Greek Shipping : Greece s steaming force

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

Tourism Snapshot A Monthly Monitor of the Performance of Canada s Tourism Industry

Tourism Snapshot A Monthly Monitor of the Performance of Canada s Tourism Industry December 2015 Volume 11, Issue 12 www.destinationcanada.com Tourism Snapshot December 2015 1 2 Tourism Snapshot December

Tourism Snapshot A Monthly Monitor of the Performance of Canada s Tourism Industry December 2015 Volume 11, Issue 12 www.destinationcanada.com Tourism Snapshot December 2015 1 2 Tourism Snapshot December

Tourism Snapshot A focus on the markets in which the CTC and its partners are active

Tourism Snapshot A focus on the markets in which the CTC and its partners are active www.canada.travel/corporate January 214 Volume 1, Issue 1 Key highlights Total arrivals from CTC s international markets

Tourism Snapshot A focus on the markets in which the CTC and its partners are active www.canada.travel/corporate January 214 Volume 1, Issue 1 Key highlights Total arrivals from CTC s international markets

WEEKLY SHIPPING MARKET REPORT WEEK 12

WEEKLY SHIPPING MARKET REPORT WEEK 12 WEEK 12 (18 th March to 24 th March 2016) Market Overview Bulkers In the middle of grain season and in the begging of the catholic easter holidays,another week comes

WEEKLY SHIPPING MARKET REPORT WEEK 12 WEEK 12 (18 th March to 24 th March 2016) Market Overview Bulkers In the middle of grain season and in the begging of the catholic easter holidays,another week comes

WEEKLY MARKET REPORT January 27th, 2012 / Week 4

WEEKLY MARKET REPORT January 27th, 2012 / Week 4 Whilst the capesize losses were just below 6% all other segments continue to suffer double digit losses with the panamaxes leading the way. The BPI lost

WEEKLY MARKET REPORT January 27th, 2012 / Week 4 Whilst the capesize losses were just below 6% all other segments continue to suffer double digit losses with the panamaxes leading the way. The BPI lost

MARKET REPORT WEEK 49 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th DECEMBER 2009

MARKET REPORT WEEK 49 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th DECEMBER 2009 Nilimar's SNP market overview Seems that while last week did not produce many concluded deals the market

MARKET REPORT WEEK 49 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th DECEMBER 2009 Nilimar's SNP market overview Seems that while last week did not produce many concluded deals the market

Finding Rationality in an Irrational World: The Economics of Successful Hotel Negotiations

Finding Rationality in an Irrational World: The Economics of Successful Hotel Negotiations Isaac Collazo, Vice President, Performance Strategy & Planning, InterContinental Hotels Group (IHG) Maria Lowry,

Finding Rationality in an Irrational World: The Economics of Successful Hotel Negotiations Isaac Collazo, Vice President, Performance Strategy & Planning, InterContinental Hotels Group (IHG) Maria Lowry,

Monday, August 30, Week 35 The Week at a Glance

Monday, August 3, 21 - Week 35 The Week at a Glance Hunting Season? Vacations season is almost over and decision makers are getting back in to their usual schedules. Let s see whether September will be

Monday, August 3, 21 - Week 35 The Week at a Glance Hunting Season? Vacations season is almost over and decision makers are getting back in to their usual schedules. Let s see whether September will be

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st March 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MARCH 217

MONTHLY MARKET OVERVIEW 1st 31st March 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MARCH 217

Weekly Market Report

Week 46 Tuesday 17th November 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News Japan announced Monday its best economic growth in more than two years