CRETE PROPERTY MARKET. 2 nd Semester 2014

|

|

|

- Rudolph Wells

- 6 years ago

- Views:

Transcription

1 1 CRETE PROPERTY MARKET 2 nd Semester 2014

2 2 Table of Contents 1. Economic Overview & Indices Office Market Residential Market Retail Market Logistics & Industrial Market Hotel and Tourism... 20

3 3 1. Economic Overview & Indices The substantial progress that Greece has made during 2013 and 2014 has been evident with the return of the Greek state and systemic banks to the international markets in 2014, as well as the successful completion of stress tests conducted by the ECB. The EU contribution in the funding for Greece s second program run out at the end of 2014, while IMF s funding continues until the end of the first quarter of Additionally, on the back of the successful outcome of the stress tests and the new political situation in Greece the government is now in a better position to start negotiations with the Institutions, leading to the disbursement of the next loan installment. Consequently, the recent agreement and extension of the program gives time to Greece to negotiate the form and structure of the future international aid either as a 3 rd program or an emergency facility line. This process is still ongoing and any prediction on the form of the outcome is very hard. Due to the political situation in Q4 of 2014 the positive sign of GDP growth rate for Q is not expected to hold, and deflationary pressures remain. Exports are expected to surge in 2015 due to the competitiveness gain and depreciation of the euro. Overall, Greece s remarkable adjustment in the last four and a half years has led to rebalancing of the economy. This was made possible through fiscal consolidation, mainly by reducing spending and expanding the tax base on a permanent basis. Moreover, substantial productivity-enhancing and employment increasing structural reforms (especially, in the labor and product markets) were implemented successfully, boosting Greece s international competitiveness, as well as net exports, business and consumer sentiment.

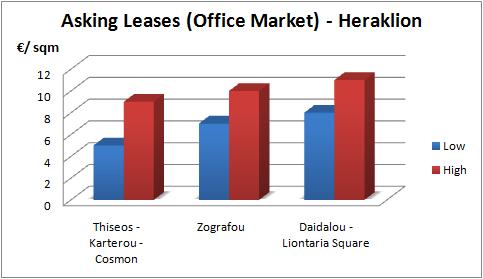

4 4 2. Office Market During the 2 nd semester of 2014, office market and rental values in Crete remained almost stable relatively to the 1 st semester of 2014, while in comparison with 2013 prices were decreased up to 5-10%. Despite the fact that prices are nowadays at sensible levels, asking prices are still negotiable and can be decreased up to 10%, at similar levels comparing to the previous semester. Demand remains at low levels as supply is being further increased. Companies have decreased their profits due to the economical situation and some of them did not manage to stay active, which led to more unoccupied office space. It is worth mentioning that there is no interest from businesses and freelancers to move out of the CBD, where there are much more spacious buildings with office use. Due to the passing economic recession, bigger office blocks have remained empty for more than two years and it is likely to remain at the same situation for the next year. Nevertheless, in rare cases freelancers have leased small offices outside the CBD, but only next to hospitals or public services buildings. In Chania, rental values around the Dikastirion Square are higher relatively to the city center due to the privileged location of the square, which is close to the building of the Regional Union of Chania, the Court House and the Town Planning Directorate, while the higher market values can be found at the city center (Skalidi & Giannari Streets). In Boniali Centre and Plaza Building (Pireos Street), asking leases vary from 4 6 /sqm/month and asking prices from /sqm. In Megaro Pantheon, leases vary from 3,5 5 /sqm/month and prices from /sqm, while around Dikastirion Square leases vary from 5 8 /sqm/month and prices from /sqm and can go up to 10 /sqm/month and /sqm respectively in cases of relatively new and small office spaces. In Skalidi & Giannari Streets, asking leases vary from 4,5 7,5 /sqm/month and prices from /sqm. In Heraklion, the vast majority of office spaces supply and demand is congregated around the Center Business District and especially at Zografou Street, Daidalou Street and Liontaria Square, where lawyers, doctors and accountants are highly interested due to the proximity to the CBD. Asking leases and prices vary from 5-9 /sqm/month and from /sqm respectively at Thiseos, Karterou & Cosmon Streets, from 7-10 /sqm/month and from

5 /sqm at Zografou Street and from 8 11 /sqm/month and from /sqm at Daidalou Street and Liontaria Square. In Rethymno, the main office market is situated around the Center Business District, the Old City and Iroon Polytechniou Square, close to the main retail market and the public services buildings, while relatively new office spaces can be found at the main streets that lead to the CBD, i.e. Igoumenou Gavriil Avenue and Portaliou Avenue. Asking leases and prices vary from 7 9 /sqm/month and from /sqm respectively at main streets and from 5 7 /sqm/month and from /sqm at secondary streets in the Old City, from 8 10 /sqm/month and from /sqm at the main street (Kountouriotou Avenue) and from 5-7 /sqm/month and from /sqm at secondary streets (Moatsou, Dimitrakaki) in the CBD and from 4 7 /sqm/month and from 1, /sqm around Iroon Polytechniou Square, Igoumenou Gavriil Avenue and Portaliou Avenue. In Lasithi, due to the small size of the cities of Agios Nikolaos, Ierapetra and Sitia, office spaces are congregated only in the center of the cities. Asking leases and prices vary from 4-7 /sqm/month and from /sqm respectively in Agios Nikolaos, from 6 8 /sqm/month and from /sqm in Ierapetra and from 4 6 /sqm/month and from /sqm in Sitia. Picture: Trianon Center in Chania,

6 6

7 7

8 8 * Leases and prices depend on the age, the condition and the location of the buildings.

9 9 3. Residential Market During the 2 nd semester of 2014, the residential market remained almost stable in comparison with the 1 st semester of 2014 and 2013, while in comparison with 2012 prices have decreased up to 10%. Due to the continuous exacerbating economic climate, the demand side tries to exploit this circumstance and asks for properties with exclusive characteristics at very low prices. However, this demand cannot be matched from the potential sellers, but after negotiations the admittedly high asking prices can be reduced to an extent of 15-20% in order to reach an agreement. In many cases, house owners are not in an urgent need of cash yet, so the levels of asking prices are still at relatively high levels. The demand for new structures remains at very low levels, since the potential buyers show preference to old residences with the future prospect of renovation. In Chania, around CBD, the vast majority of residences are at least year old and the price range is from /sqm, depending on the exact location, age and level of maintenance, while new structures prices vary from /sqm. The prices regarding new conventional structures in popular residential areas near the CBD vary from /sqm in Chalepa, from /sqm in Lentariana & Aberia and from /sqm in Nea Chora. Exceptions in prices range do exist and depend on the location and offering view of the asset and the quality of the construction. Rental prices remained almost stable relatively with 2013, with a reduction of almost 10% in comparison to In Chalepa, rental prices for conventional residences vary from 3,5 5 /sqm, around Court Area from 4 6 /sqm/month, in Koumpes from 3 4 /sqm/month, in Nea Chora from 3,5 5 /sqm/month and in Lentariana & Aberia from 3,5 4,5 /sqm/month. In Heraklion, around CBD, the vast majority of residences are at least 25 years old homes whose price range is from /sqm, mainly depending on the level of maintenance and the parking availability around the property. The price range, for recently built residences in popular areas near the CBD, such as Analispi and Mastampas, is from /sqm, depending on the location, the floor level, the construction quality, the view and the overall size of the property. Rental prices remained almost stable relatively with the previous year. Rental prices vary from 4 5,5 /sqm/month in popular areas near the CBD and up to 6,5 /sqm/month around CBD. The upper levels of the aforementioned ranges represent small new houses, with one or two bedrooms and size between 35 sqm and 60 sqm.

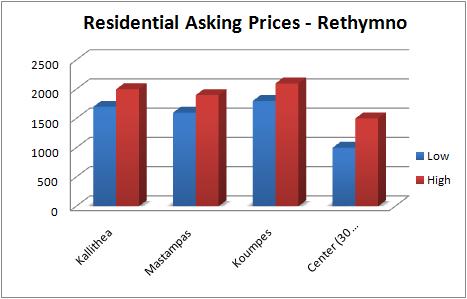

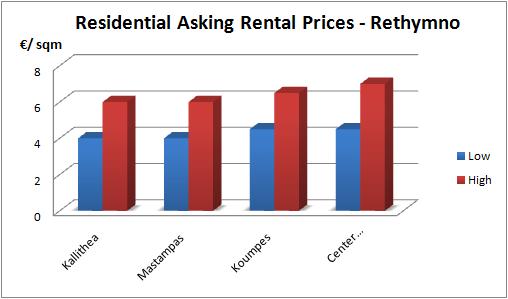

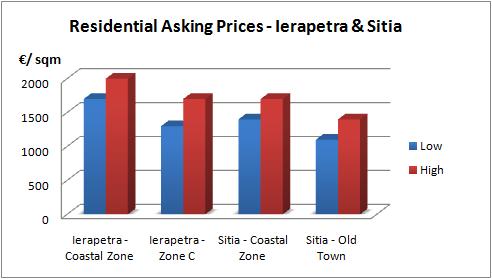

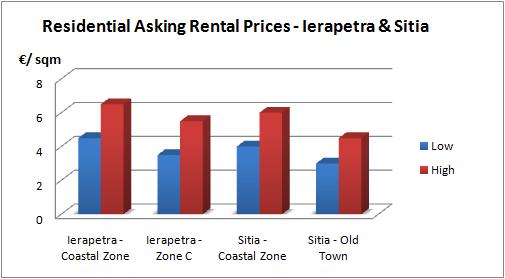

10 10 In Rethymno, the vast majority of residences in the Old City are old structures whose price range is from /sqm, mainly depending on the level of maintenance. The price range, for new conventional residences in areas near the CBD, such as Kallithea, Mastampas and Koumpes, is from /sqm, depending on the specific characteristics of the property, such as location, floor level, view and size. Rental prices remained almost stable relatively with 2013, with a reduction of 10% in comparison to In the Old City, rental prices vary from 4,5 7 /sqm/month, in Kallithea and Mastampas from 4 6 /sqm and in Koumpes from 4,5 6,5 /sqm/month. In Lasithi, in Agios Nikolaos, the price range for new residences is from /sqm in the coastal zone and from /sqm in the new city sections (Stavros, Kopranes, Amoudi), while the range for relatively new residences (10 years old) in the Old Town is from /sqm. In Ierapetra, residences prices in the coastal zone vary from /sqm and in the new city section (zone C) from /sqm, while in Sitia, the price range is from /sqm in the coastal zone and the new city sections (Kserokamares, Kokkina) and from /sqm in the Old Town (older structures). Rental prices remained almost stable relatively with the previous year. In Agios Nikolaos, rental prices vary from 3 5 /sqm/month in the Old Town and in the new city sections and up to 6,5 /sqm/month in the coastal zone, in Ierapetra rental prices vary from 3,5 5,5 /sqm/month in Zone C and up to 6,5 /sqm/month in the coastal zone, while in Sitia rental prices vary from 4 6 /sqm/month in the coastal zone and the new city sections and from 3 4,5 /sqm/month in the Old Town. Pictures: New Apartment Complexes in Heraklion and Rethymno, Source: www. zoipreari.drupalgardens.com

11 11

12 12

13 13

14 14 4. Retail Market During 2014, salaries and pensions were diminished, so retail business profits were seriously decreased and many businesses did not manage to stay in market. Banks recapitalizations have been successfully completed but money has not passed to the real economy. For this reason, an extension of the business hours has been decided but only a few retailers and local businessmen have implemented the decision. The local market had relied on the speculation of a good tourism season, but despite the notable increase at the arrivals, revenues remained at low levels. During the 2 nd semester of 2014, private consumption was stabilized and some activity took place. Big retail brands seam to take advantage of the historical low prices in the major retail streets. Recent encouraging developments in the labor market and a relative relaxation in fiscal adjustment effort imply that household spending will pick up further in the coming months. Overall prices have been stabilized, vacancy has dropped and absorption has increased. Facts of 2 nd semester 2014: 6 out of 10 small or medium sized businesses with bank loans, cannot afford paying the monthly payment because of their diminished revenue. There is a high rate of refusing decisions to operate the retail shops on Sundays. This rate reached the level of 65 % in Heraklion and Rethymno and of 75 % in Chania. There is a high promotional activity of new business incentive programs such as agricultural entrepreneurship, youth entrepreneurship, female entrepreneurship and other small and medium sized business programs which have leaded to slight counter urbanization and to fewer unoccupied retail stores. Many international and national retail enterprises are in search of retail properties in Crete (especially Heraklion and Chania), as they are willing to expand their chain stores due to the forthcoming economic recovery. These enterprises have business in sectors like IT, young fashion, beauty products and clothing. During the last semester, the expensive fashion retailers have not been affected as much as most people have imagined, as a straight result of the continuous salary cutbacks during the last three years. Tourists have enhanced this result and especially the Russian and Chinese ones.

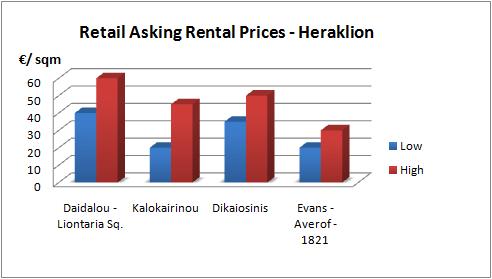

15 15 In the large cities of Crete, due to the fact that the prices are not formed based on objective factors but are driven by each landlord s personal will, cities retail property market is quite unstable as far as prices is concerned and display unexpected differences on similar kind of properties. During 2014, the rental renegotiations have been depleted, many local retailers have moved to nearby properties, perhaps in better location and surely with comparably better rental price. This trend was also mentioned for the previous semester and still happens because business owners have the opportunity to decrease their fixed expenditure and simultaneously move either to better shopping streets or to more spacious retail properties. According to our recent research of the retail market in Crete, there are some main streets around CBD and towards the suburbs of the cities that used to be of high commercial importance, but due to the economic recession, we can nowadays typify them as streets with steady or low commercial interest. This happened because many businesses have seized their operation and many retail properties have been empty for a long period. It is worth mentioning that for the aforementioned two categories, the level of unoccupied retail properties have lessened relatively to 2013, especially at the streets with steady commercial interest. Moreover, unoccupied retail shops have been dramatically decreasing, in streets between the prime commercial streets of CBD, because of small and medium sized business incentive programs that have been launched by the government. In Chania, rental prices at the old port vary from /sqm/month and from /sqm/month at the area of Koum Kapi, in Chalidon, Chatzimichali Giannari and Skalidi Streets (main area of retail market) from /sqm/month, in the area of Stivanadika from /sqm/month, in Tzanakaki and Papandreou Streets from /sqm/month, in Kidonias and Apokoronou Streets from /sqm/month and in secondary streets of the city centre (Peridou, Sfakion, Karaiskaki, Plastira) from 8-12 /sqm/month. On the other hand, in low commercial interest streets prices vary from 5-8 /sqm/month (Kissamou, Mpotsari, Gogoni Streets) and from 4-6 /sqm/month regarding the city entrance roads (K. Karamanli & Kazantzaki Avenues). In Heraklion, within CBD, asking rental prices vary from /sqm/month in primary streets (Daidalou, Liontaria Square, Dikaiosinis, Kalokarinou Avenue east part) and from /sqm/month in secondary streets (Kalokairinou Avenue west part, Evans, Averof. 1821), as depicted below.

and from 10 15 /sqm/month in secondary streets (Gerakari, Ethnikis")

16 16 Streets with steady commercial interest are 62 Martyron Avenue, Knossou Avenue and Dimokratias Avenue where leases vary from 9-15 /sqm/month. On the other hand, the streets with low commercial interest are Ethnikis Antistaseos Avenue, Ikarou Avenue and EOK Avenue where leases vary from 5-8 /sqm/month and the empty retail properties are much more in comparison with the steady commercial interest streets. In Rethymno, within the Old Town, rental prices vary from /sqm/month in Arkadiou Street ( prices at the north part) and from /sqm/month in secondary streets (Gerakari, Ethnikis Antistaseos), in the coastal zone, from /sqm/month in El. Benizelou Street and from /sqm/month in Sof. Benizelou Street, within the CBD, from /sqm/month in Kountouriotou Avenue and from 8 12 /sqm/month in secondary streets (Moatsou, Zimvrakaki), while in the city entrance roads, rental prices vary from 8 15 /sqm/month in Stamathioudaki and Ig. Gavriil Avenues (west entrance) and from /sqm/month in Portaliou Avenue (east entrance). In Lasithi, commercial activity is being found only in the cities center. Rental prices in Agios Nikolaos vary from /sqm/month within the CBD and from 7 15 /sqm/month in the coastal zone, in Ierapetra (center) from 7 15 /sqm/month and in Sitia (center) from 5 13 /sqm/month. Picture: Shopping Center Olea in Platanias (source: Picture: Shopping Center Talos Plaza in Heraklion (source:

17 17

18 18

19 19 5. Logistics & Industrial Market In Crete, no interest is observed in logistics and industrial market; therefore during the 2 nd semester of 2014 market has remained stable. The divestment of Makro s Greek cashand-carry operations to the local retail group Sklavenitis has brought no change in the operation of the two wholesale stores in Heraklion and Chania. On the other hand, the German hypermarket chain Praktiker showed interest in opening a new store in Chania during 2014; however, plans were put on hold due to the unsteady political and economical conditions in Greece. Source:

20 20 6. Hotel and Tourism Tourism is one of the few sectors of the Greek national economy that is competitive at a global level. Despite the lingering economic challenges, tourism sector has shown a remarkable strength in 2014, a record year in tourism. Greece s unique geographical characteristics, in combination with its highly developed and still fast developing transportation infrastructure and also the development and modernization of more specific tourist facilities, are expected to contribute to its development as a major tourist destination in Europe and as an international transportation hub of European proportions. Picture: Caramel Boutique Resort in Rethymno, Source: On the real estate side of the Tourism sector there is strong interest from private equity funds and world calibre operators to expand in the Greek market, enhance infrastructure and attract even more tourists, mainly of a higher level of income. As a result, there is a strong demand for big and medium size hotels or large land plots by the sea. More specifically, the ITANOS GAIA investment of more than 250 mn by the British company Loyalward Ltd, affiliate of Minoan Group Plc, intends to develop a total area of 25 hectares in Cavo Sidero, Lasithi. Based on the initial concept of the project, the hotel complex which will consist of five hotels with beds, a golf court and other sport facilities, will be mainly intended for luxury tourists. The hotel complex is expected to operate in 2017, creating approximately job vacancies and arising noticeably the touristic profile of Crete.

21 21 In addition, DCI s (Dolphin Capital Investors) investment portfolio includes three major projects in Sitia, Plaka and Triopetra. DCI has already reached an agreement for the construction at Sitia, eastern Crete, of a Waldorf Astoria hotel, which constitutes the highest quality hotel chain of the group of Hilton Hotels and Resorts. The complex will be situated on a land plot of 280 hectares with 2.5km of seafront and consists of over 80,000m2 of buildable residential units, a 200 room luxury hotel, a convention centre, an 18-hole golf course and clubhouse, a 32 berth marina, a beach & country club and other leisure facilities. The Plaka Bay Resort in Lasithi will be developed on a land plot of 440 hectares with 7km of seafront and consists of a residential development of over 100,000m2 buildable area, one or more five-star hotels, other supporting recreational facilities and potentially an 18-hole golf course. Finally, the Triopetra project in south Rethymno will be developed on a seafront plot of more than 11 hectares and will consist of a 63 room luxury hotel with 2,500m2 public areas and a 600m2 spa and fitness club, as well as 82 residential units with a total 8,870m2 buildable area. Also, the international chain Carlson Rezidor Group has signed a franchise contract with the owner company of the hotel Minos Imperial Luxury Beach Resort and Spa in the region of Milatos, Lasithi. The hotel will be renamed into Radisson Blue Beach Resort in Finally, the American colossus Diamond Resorts International, a leader in hospitality and vacation ownership, has bought 4 hotels in Heraklion and Rethymno. Picture: Sitia Bay Golf Resort, Source:

22 22 According to the most recent data published by the World Tourism Organization (WTO), in 2013 Greece was in 16 th position as regards the number of international tourist arrivals (17.9 mn), with the expectation of better rankings in 2014 and 2015 (stats for 2014 have not yet officially announced). Furthermore, according to the World Economic Forum (WEF), in 2013, Greece took the 32 nd place among 140 countries regarding the Travel & Tourism Competitiveness Index and the 91 st place regarding the overall Competitiveness Index (stats for 2014 have not yet officially announced). Tourism arrivals (not including cruises) exceeded expectations in 2014 and grew by almost 23%, reaching a record 22 mn arrivals. As a result, tourism receipts were also increased remarkably by almost 13% in 2014 to 13.2 bn, compared to bn in Both economic figures are new records for incoming tourism in Greece. The decision of Ryan Air, the largest low-cost airline in Europe, to create a base in Chania in 2013 and a new base in Athens in 2014, has brought significant benefits in terms of tourism for the entire Crete. The international arrivals for 2014 in Chania airport have reached the number of 950,316 with an increase of 11.8% in comparison with 2013 (849,667 arrivals). This increase is mainly due to Ryan Air and has speed up the project of the expansion of the airport Ioannis Daskalogiannis, which is expected to finish at the end of At the same time, in Heraklion airport, arrivals in 2014 reached the number of 2,606,472 with an increase of 5.4% compared to 2013 (2,472,082 arrivals). As far as the cruise sector, Greece is the 3 rd most popular tourist destination in Europe, following Spain and Italy. Despite the initial predictions of zero increase relatively to 2013, during 2014, 2.5 mn passengers arrived at the Greek ports, relatively to 2.2 mn passengers during Due to the lack of infrastructure and the abandoned ships at the docks, Souda Port did not manage to benefit from the overall raise in the cruise sector. According to the official statistics of Souda Port, 39 cruise ships visited the port during 2014 relatively to 47 cruise ships in This decrease was mainly due to the decision of the group Royal Caribbean International to withdraw the cruise ship Navigator of the Sea from Souda Port. However, predictions for 2015 are very promising, since 3 new cruise companies are expected to drop anchor in Souda Port. The scheduled cruise arrivals for 2015 reach the number of 68 so far, with a total capacity of 88,022 passengers.

23 23 On the other hand, in 2014, 339,512 passengers (on the basis of the tonnage of ships) chose Heraklion port as transit or homeport. According to local authorities, the growth for 2014 was up to 20% compared with 2013, despite the competition from other countries in the region, such as Turkey. During the 1 st semester of 2014, 70 cruise ships visited the Heraklion Port, while 92 cruise ships dropped anchor during the 2 nd semester of During the 1 st and 2 nd semester of 2015, 61 and 79 cruise ships are expected to visit the Heraklion Port respectively. The significant increase regarding the cruise arrivals in Heraklion Port has lead to the decision of constructing a cruise terminal at the national airport of Heraklion. Picture: New Cruise Terminal in Kazantzakis airport, Source:

24 24 GREECE Athens 15 Vouliagmenis Ave., Τel.: Fax: office@danos.gr Thessaloniki 4 Ionos Dragoumi Str., Τel.: Fax: info.thes@danos.gr Crete - Chania 3 Iroon Polytechniou Str., Τel. : Fax: info.crete@danos-melakis.gr Crete - Heraklion 38 Aretousas Str., Tel.: Fax: info.crete@danos-melakis.gr CYPRUS Nicosia 35 I. Hatziiosif Ave., 2027 Strovolos Τel.: Fax: danosa@spidernet.com.cy Limassol 69 Gladstonos Str., 3040 Acropolis Centre, Shop 10 Τel.: Fax: danosa@cytanet.com.cy SERBIA Belgrade 3 Spanskih Βoraca Str New Belgrade Tel.: Fax: office@danos.rs

25 25 DISCLAIMER This report is published for general information only. Although high standards have been used in the preparation of the information, analysis, view, and projections presented in this report, no legal responsibility can be accepted by DANOS or BNP PARIBAS RE for any loss or damage resultant from the contents of this document. As a general report this material does not necessarily represent the view of DANOS or BNP PARIBAS RE in relation to particular properties or projects. Reproduction of this report in whole or in part is allowed with proper reference to DANOS Research.

CRETE PROPERTY MARKET 2 nd Semester 2013

1 CRETE PROPERTY MARKET 2 nd Semester 213 2 Table of Contents 1. Office Market... 3 2. Residential Market... 6 3. Retail Market... 9 4. Logistics & Industrial Market... 13 5. Hotel and Tourism... 13 3

1 CRETE PROPERTY MARKET 2 nd Semester 213 2 Table of Contents 1. Office Market... 3 2. Residential Market... 6 3. Retail Market... 9 4. Logistics & Industrial Market... 13 5. Hotel and Tourism... 13 3

THESSALONIKI PROPERTY MARKET. 2nd Semester 2014

THESSALONIKI PROPERTY MARKET 2nd Semester 2014 1. Economic Overview & Indices The substantial progress that Greece has made during 2013 and 2014 has been evident with the return of the Greek state and

THESSALONIKI PROPERTY MARKET 2nd Semester 2014 1. Economic Overview & Indices The substantial progress that Greece has made during 2013 and 2014 has been evident with the return of the Greek state and

CRETE PROPERTY MARKET. 2nd Semester 2016

CRETE PROPERTY MARKET 2nd Semester 2016 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market... 18 6. Tourism...

CRETE PROPERTY MARKET 2nd Semester 2016 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market... 18 6. Tourism...

CRETE PROPERTY MARKET. 2 nd Semester 2015

1 CRETE PROPERTY MARKET 2 nd Semester 2015 2 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market... 19 6.

1 CRETE PROPERTY MARKET 2 nd Semester 2015 2 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market... 19 6.

THESSALONIKI PROPERTY MARKET. 1st Semester 2016

THESSALONIKI PROPERTY MARKET 1st Semester 2016 Economic Overview & Indices The outcome of the referendum in the United Kingdom in support of the exit from the European Union creates an unstable European

THESSALONIKI PROPERTY MARKET 1st Semester 2016 Economic Overview & Indices The outcome of the referendum in the United Kingdom in support of the exit from the European Union creates an unstable European

CRETE PROPERTY MARKET. 1st Semester 2018

CRETE PROPERTY MARKET 1st Semester 2018 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 10 4. Retail Market... 16 5. Logistics & Industrial Market... 20 6. Tourism...

CRETE PROPERTY MARKET 1st Semester 2018 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 10 4. Retail Market... 16 5. Logistics & Industrial Market... 20 6. Tourism...

THESSALONIKI PROPERTY MARKET. 2nd Semester 2015

THESSALONIKI PROPERTY MARKET 2nd Semester 2015 Economic Overview & Indices 2015 was crucial for Greece due to the progress of negotiations with its international creditors. As a result, the signs of improvement

THESSALONIKI PROPERTY MARKET 2nd Semester 2015 Economic Overview & Indices 2015 was crucial for Greece due to the progress of negotiations with its international creditors. As a result, the signs of improvement

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 2 nd Semester 2017 Economic Overview & Indices Real GDP growth (Annual percent change) The completion of the second EU program review in June 2017 buoyed confidence, supporting

THESSALONIKI PROPERTY MARKET 2 nd Semester 2017 Economic Overview & Indices Real GDP growth (Annual percent change) The completion of the second EU program review in June 2017 buoyed confidence, supporting

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 1 st Semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on

THESSALONIKI PROPERTY MARKET 1 st Semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 2nd Semester 2016 Economic Overview Greek economy is gradually returning to positive development rates. The GDP was increased by +1,8% in the third quarter of 2016 on annual

THESSALONIKI PROPERTY MARKET 2nd Semester 2016 Economic Overview Greek economy is gradually returning to positive development rates. The GDP was increased by +1,8% in the third quarter of 2016 on annual

How does my local economy function? What would the economic consequences of a project or action be?

June 5th,2012 Client: City of Cortez Shane Hale Report Prepared for SBDC Ft. Lewis Report Prepared by Donna K. Graves Information Services Executive Summary - At the request of Joe Keck at the Small Business

June 5th,2012 Client: City of Cortez Shane Hale Report Prepared for SBDC Ft. Lewis Report Prepared by Donna K. Graves Information Services Executive Summary - At the request of Joe Keck at the Small Business

1.2% 3.5% 13.2% Inflation May 2017 y-o-y. Retail Sales, May 2017 y-o-y

City Report Q2 2017 1.2% 3.5% 13.2% GDP Growth Q1 2017 y-o-y Inflation May 2017 y-o-y Unemployment rate Q1 2017, Belgrade 489 11.1% 6.2% Net Salary May 2017, Belgrade Retail Sales, May 2017 y-o-y Industrial

City Report Q2 2017 1.2% 3.5% 13.2% GDP Growth Q1 2017 y-o-y Inflation May 2017 y-o-y Unemployment rate Q1 2017, Belgrade 489 11.1% 6.2% Net Salary May 2017, Belgrade Retail Sales, May 2017 y-o-y Industrial

Serbia Key Facts. Serbia in Europe. Belgrade s urban municipalities

Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 1 and N 7, on the way from Europe to Asia. The Republic

Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 1 and N 7, on the way from Europe to Asia. The Republic

Shopping Mall Business in Japan

Overview of Business Operations (Fiscal year ending February 20, 2011) Shopping Mall Business in Japan ÆON Mall is pressing ahead in creating shopping malls that answer customer needs and are the most

Overview of Business Operations (Fiscal year ending February 20, 2011) Shopping Mall Business in Japan ÆON Mall is pressing ahead in creating shopping malls that answer customer needs and are the most

1. Serbia Key Facts. Picture: Belgrade s municipalities. Picture: Knez Mihailova Street

1. Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 10 and N 7, on the way from Europe to Asia. The

1. Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 10 and N 7, on the way from Europe to Asia. The

PROPERTY MARKET ATHENS 1 st semester 2017

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

The challenge of competitiveness for the Greek Tourism Industry

The challenge of competitiveness for the Greek Tourism Industry George Drakopoulos Director General Deree Business Week Annual Forum, 18 th March 2010 About SETE SETE is a non-governmental, non-profit

The challenge of competitiveness for the Greek Tourism Industry George Drakopoulos Director General Deree Business Week Annual Forum, 18 th March 2010 About SETE SETE is a non-governmental, non-profit

2nd International Rhodes Tourism Forum November 2006

2nd International Rhodes Tourism Forum 10 11 November 2006 Eleni Desylla Tourism Sector Manager HELLENIC CENTER FOR INVESTMENT 1 THE GREEK INVESTMENT INSTITUTIONAL FRAMEWORK AND THE EXISTING AND FUTURE

2nd International Rhodes Tourism Forum 10 11 November 2006 Eleni Desylla Tourism Sector Manager HELLENIC CENTER FOR INVESTMENT 1 THE GREEK INVESTMENT INSTITUTIONAL FRAMEWORK AND THE EXISTING AND FUTURE

PROPERTY MARKET ATHENS 2 nd semester 2017

PROPERTY MARKET ATHENS 2 nd semester 2017 Economic Overview & Indices The completion of the second EU program review in June 2017 buoyed confidence, supporting activity. Employment growth is buttressing

PROPERTY MARKET ATHENS 2 nd semester 2017 Economic Overview & Indices The completion of the second EU program review in June 2017 buoyed confidence, supporting activity. Employment growth is buttressing

Tourism Dynamics Issue 1

October 2014 Tourism Dynamics Issue 1 At a Glance In this issue Tourist arrivals 3 Arrivals of tourists per 3 country Opportunities ahead 4 Income from tourism 4 key GDP component Income by country 5 New

October 2014 Tourism Dynamics Issue 1 At a Glance In this issue Tourist arrivals 3 Arrivals of tourists per 3 country Opportunities ahead 4 Income from tourism 4 key GDP component Income by country 5 New

RETAIL MARKET REPORT RESEARCH Q Moscow HIGHLIGHTS

Q1 2018 RETAIL MARKET REPORT Moscow HIGHLIGHTS A slight increase of the new supply was recorded at the level of 18,700 sq m (GLA) at the Moscow retail real estate market in Q1 2018. The stable dynamics

Q1 2018 RETAIL MARKET REPORT Moscow HIGHLIGHTS A slight increase of the new supply was recorded at the level of 18,700 sq m (GLA) at the Moscow retail real estate market in Q1 2018. The stable dynamics

Main Points in the Results for FY2015

0 1 2 Main Points in the Results for FY2015 Operating profit increased to 75.4 billion yen, exceeding the goal of 75.0 billion yen for the final year of the medium-term management plan in the first year

0 1 2 Main Points in the Results for FY2015 Operating profit increased to 75.4 billion yen, exceeding the goal of 75.0 billion yen for the final year of the medium-term management plan in the first year

Cairo, May 21, TMG Holding reports EGP BN consolidated revenue, EGP 161 MN consolidated net profit

First Quarter ending Earning Release Cairo, May 21, - reports EGP 1.139 BN consolidated revenue, EGP 161 MN consolidated net profit after minority and EGP 2.2 BN of new sales value for the first quarter

First Quarter ending Earning Release Cairo, May 21, - reports EGP 1.139 BN consolidated revenue, EGP 161 MN consolidated net profit after minority and EGP 2.2 BN of new sales value for the first quarter

Acceleration of tourism

Belgrade 217 Tourism & Hotel Outlook Regulated by RICS Tourism & Hotel Market Outlook 217 LeRoy Realty Consultants 1 The growth of travel & tourism industry considerably outperforms that of the local economy

Belgrade 217 Tourism & Hotel Outlook Regulated by RICS Tourism & Hotel Market Outlook 217 LeRoy Realty Consultants 1 The growth of travel & tourism industry considerably outperforms that of the local economy

Tourism Development in Greece Background facts & current policy issues

Tourism Development in Greece Background facts & current policy issues Georgios Drakopoulos Director General, SETE & Chairman, UNWTO Business Council Meeting with the French Counselors for Foreign Trade

Tourism Development in Greece Background facts & current policy issues Georgios Drakopoulos Director General, SETE & Chairman, UNWTO Business Council Meeting with the French Counselors for Foreign Trade

MARKETBEAT. Queenstown Regional. Residential

Winter 2016 MARKETBEAT RESEARCH NEWSLETTER Queenstown Regional Queenstown is booming. A surging tourism sector drawing in more workers, coupled with an increasing wave of lifestylers and rising investor

Winter 2016 MARKETBEAT RESEARCH NEWSLETTER Queenstown Regional Queenstown is booming. A surging tourism sector drawing in more workers, coupled with an increasing wave of lifestylers and rising investor

Press Release For Immediate Release

Press Release For Immediate Release FRANSHION PROPERTIES (CHINA) LIMITED Announces 2008 Interim Results Revenue Surged by 797% to HK$870.3 million Profit Attributable to Equity Holders Grew by a Substantial

Press Release For Immediate Release FRANSHION PROPERTIES (CHINA) LIMITED Announces 2008 Interim Results Revenue Surged by 797% to HK$870.3 million Profit Attributable to Equity Holders Grew by a Substantial

Economic Impact of Tourism in Hillsborough County September 2016

Economic Impact of Tourism in Hillsborough County - 2015 September 2016 Key findings for 2015 Almost 22 million people visited Hillsborough County in 2015. Visits to Hillsborough County increased 4.5%

Economic Impact of Tourism in Hillsborough County - 2015 September 2016 Key findings for 2015 Almost 22 million people visited Hillsborough County in 2015. Visits to Hillsborough County increased 4.5%

RESEARCH INDUSTRIAL SNAPSHOT

RESEARCH INDUSTRIAL SNAPSHOT GREATER LONDON AND WESTERN HOME COUNTIES H2 2017 GREATER LONDON & WESTERN HOME COUNTIES LOGISTICS & INDUSTRIAL RESEARCH Introduction As the UK economy continues to grow so

RESEARCH INDUSTRIAL SNAPSHOT GREATER LONDON AND WESTERN HOME COUNTIES H2 2017 GREATER LONDON & WESTERN HOME COUNTIES LOGISTICS & INDUSTRIAL RESEARCH Introduction As the UK economy continues to grow so

PROPERTY MARKET ATHENS 1 st semester 2017

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

ERW. 022/ ACC003/ th February Subject: Management's Discussion and Analysis period ending 31 st December 2012

ERW. 022/ ACC003/56 26 th February 2013 Subject: Management's Discussion and Analysis period ending 31 st December 2012 Attention: The President, The Stock Exchange of Thailand Dear Sir, The Erawan Group

ERW. 022/ ACC003/56 26 th February 2013 Subject: Management's Discussion and Analysis period ending 31 st December 2012 Attention: The President, The Stock Exchange of Thailand Dear Sir, The Erawan Group

Belgrade City Report Q City Reports

Belgrade City Report Q2 2016 City Reports GDP Growth Q1 (y-o-y) Net Salary May Economy & Investment Economics 3.5% Inflation May y-o-y 0.7% 452 Unemployment Rate Q1 19% Retail Sales Index April y-o-y 7.4%

Belgrade City Report Q2 2016 City Reports GDP Growth Q1 (y-o-y) Net Salary May Economy & Investment Economics 3.5% Inflation May y-o-y 0.7% 452 Unemployment Rate Q1 19% Retail Sales Index April y-o-y 7.4%

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER. March Palmos Analysis. March 11

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER March 2011 Palmos Analysis March 11 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER March 2011 Palmos Analysis March 11 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its

The Economic Impact of Tourism in Maryland. Tourism Satellite Account Calendar Year 2015

The Economic Impact of Tourism in Maryland Tourism Satellite Account Calendar Year 2015 MD tourism economy reaches new peaks The Maryland visitor economy continued to grow in 2015; tourism industry sales

The Economic Impact of Tourism in Maryland Tourism Satellite Account Calendar Year 2015 MD tourism economy reaches new peaks The Maryland visitor economy continued to grow in 2015; tourism industry sales

Hospitality Market Snapshot Nairobi & Its Suburbs. June 2016

Hospitality Market Snapshot Nairobi & Its Suburbs June 2016 Kenya Nairobi In this issue 3 Nairobi Economic Overview Current Room Supply & Outlook 3 4 4 4 5 CBD 6 Westlands & Surrounds & Surrounds 7 Upper

Hospitality Market Snapshot Nairobi & Its Suburbs June 2016 Kenya Nairobi In this issue 3 Nairobi Economic Overview Current Room Supply & Outlook 3 4 4 4 5 CBD 6 Westlands & Surrounds & Surrounds 7 Upper

The business. Business opportunities throughout the value chain

The business Business opportunities throughout the value chain 36 Pandox Annual Report 2017 Pandox is an active hotel property owner with a business model based on long revenue-based leases with the best

The business Business opportunities throughout the value chain 36 Pandox Annual Report 2017 Pandox is an active hotel property owner with a business model based on long revenue-based leases with the best

PRESS RELEASE SURVEY ON QUALITATIVE CHARACTERISTICS OF RESIDENT TOURISTS: 2016 (provisional data)

") Thousands HELLENIC REPUBLIC HELLENIC STATISTICAL AUTHORITY Piraeus, 8 September 217 PRESS RELEASE SURVEY ON QUALITATIVE CHARACTERISTICS OF RESIDENT TOURISTS: 216 (provisional data) The Hellenic Statistical

Thousands HELLENIC REPUBLIC HELLENIC STATISTICAL AUTHORITY Piraeus, 8 September 217 PRESS RELEASE SURVEY ON QUALITATIVE CHARACTERISTICS OF RESIDENT TOURISTS: 216 (provisional data) The Hellenic Statistical

The Economic Impact of Tourism in North Carolina. Tourism Satellite Account Calendar Year 2013

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2013 Key results 2 Total tourism demand tallied $26 billion in 2013, expanding 3.9%. This marks another new high

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2013 Key results 2 Total tourism demand tallied $26 billion in 2013, expanding 3.9%. This marks another new high

The contribution of Tourism to the Greek economy in 2017

The contribution of Tourism to the Greek economy in 2017 1 st edition (provisional data) May 2018 Dr. Aris Ikkos, ISHC Research Director Serafim Koutsos Analyst INSETE Republishing is permitted provided

The contribution of Tourism to the Greek economy in 2017 1 st edition (provisional data) May 2018 Dr. Aris Ikkos, ISHC Research Director Serafim Koutsos Analyst INSETE Republishing is permitted provided

The Economic Impact of Tourism in North Carolina. Tourism Satellite Account Calendar Year 2015

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2015 Key results 2 Total tourism demand tallied $28.3 billion in 2015, expanding 3.6%. This marks another new high

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2015 Key results 2 Total tourism demand tallied $28.3 billion in 2015, expanding 3.6%. This marks another new high

Cairo, November 15, 2016 TMG holding reports EGP 3.9 BN consolidated revenues, EGP 616 MN consolidated net profit

Nine Months and Third Quarter ending September 30, Earning Release Cairo, November 15, TMG holding reports EGP 3.9 BN consolidated revenues, EGP 616 MN consolidated net profit after minority and EGP 5.5

Nine Months and Third Quarter ending September 30, Earning Release Cairo, November 15, TMG holding reports EGP 3.9 BN consolidated revenues, EGP 616 MN consolidated net profit after minority and EGP 5.5

JUNE18 NEWSLETTER GREECE IN NUMBERS RENEWABLE ENERGY SOURCES GREEK F&B EXPORTS

GREEK F&B EXPORTS RENEWABLE ENERGY SOURCES GREECE IN NUMBERS The newsletter is a monthly publication of Enterprise Greece, the national investment and trade promotion agency. Greek F&B Industry Enters

GREEK F&B EXPORTS RENEWABLE ENERGY SOURCES GREECE IN NUMBERS The newsletter is a monthly publication of Enterprise Greece, the national investment and trade promotion agency. Greek F&B Industry Enters

DUBAI HOTEL INVESTMENT REPORT PUBLISHED BY THE FIRST GROUP.

DUBAI HOTEL INVESTMENT REPORT PUBLISHED BY THE FIRST GROUP www.thefirstgroup.com WHY DUBAI? Dubai population 2015: 2.2 million 2020: 3.4 million (predicted) Source: Dubai Municipality AIRPORT CAPACITY

DUBAI HOTEL INVESTMENT REPORT PUBLISHED BY THE FIRST GROUP www.thefirstgroup.com WHY DUBAI? Dubai population 2015: 2.2 million 2020: 3.4 million (predicted) Source: Dubai Municipality AIRPORT CAPACITY

1.0% 3.6% 15.9% Inflation March 2017 y-o-y. Retail Sales,

City Report Q1 2017 1.0% 3.6% 15.9% GDP Growth Q1 2017 Inflation March 2017 y-o-y Unemployment rate 2016, Belgrade 495 11.4% 0.9% Salary March 2017, Belgrade Retail Sales, March 2017 y-o-y, Serbia Industrial

City Report Q1 2017 1.0% 3.6% 15.9% GDP Growth Q1 2017 Inflation March 2017 y-o-y Unemployment rate 2016, Belgrade 495 11.4% 0.9% Salary March 2017, Belgrade Retail Sales, March 2017 y-o-y, Serbia Industrial

QUARTERLY UPDATE 31 MARCH 2017

AUSTRALIAN PROPERTY OPPORTUNITIES FUND QUARTERLY UPDATE 31 MARCH 2017 The Australian Property Opportunities Fund (APOF I or the Fund) is pleased to provide this update for the March quarter 2017 (Q1 2017)

AUSTRALIAN PROPERTY OPPORTUNITIES FUND QUARTERLY UPDATE 31 MARCH 2017 The Australian Property Opportunities Fund (APOF I or the Fund) is pleased to provide this update for the March quarter 2017 (Q1 2017)

OCTOBER17 NEWSLETTER FOREIGNERS BUYING GREEK PROPERTY ECONOMY GROWS FURTHER FOOD EXPORTS GROWING GERMAN TOUR GROUP INVESTS IN GREECE

FOOD EXPORTS GROWING FOREIGNERS BUYING GREEK PROPERTY ECONOMY GROWS FURTHER GERMAN TOUR GROUP INVESTS IN GREECE The newsletter is a monthly publication of the Enterprise Greece, the national trade and

FOOD EXPORTS GROWING FOREIGNERS BUYING GREEK PROPERTY ECONOMY GROWS FURTHER GERMAN TOUR GROUP INVESTS IN GREECE The newsletter is a monthly publication of the Enterprise Greece, the national trade and

2.1% 3.0% 12.9% Inflation December 2017 y-o-y. Retail Sales, November 2017 y-o-y

City Report Q4 2017 2.1% 3.0% 12.9% GDP Growth Q3 2017 y-o-y Inflation December 2017 y-o-y Unemployment rate Q3 2017, Belgrade 495 6.6% 5.5% Net Salary November 2017, Belgrade Retail Sales, November 2017

City Report Q4 2017 2.1% 3.0% 12.9% GDP Growth Q3 2017 y-o-y Inflation December 2017 y-o-y Unemployment rate Q3 2017, Belgrade 495 6.6% 5.5% Net Salary November 2017, Belgrade Retail Sales, November 2017

AEROFLOT ANNOUNCES FY 2017 IFRS FINANCIAL RESULTS

AEROFLOT ANNOUNCES FY 2017 IFRS FINANCIAL RESULTS Moscow, 1 March 2018 Aeroflot Group ( the Group, Moscow Exchange ticker: AFLT) today publishes its audited financial statements in accordance with International

AEROFLOT ANNOUNCES FY 2017 IFRS FINANCIAL RESULTS Moscow, 1 March 2018 Aeroflot Group ( the Group, Moscow Exchange ticker: AFLT) today publishes its audited financial statements in accordance with International

Investor Briefings First-Half FY2016 Financial Results

Cedar Woods Properties Limited Investor Briefings First-Half FY2016 Financial Results 26 February 2016 Cedar Woods Presentation 2 Snapshot of Achievements in FY2016 Extensive portfolio of residential estates

Cedar Woods Properties Limited Investor Briefings First-Half FY2016 Financial Results 26 February 2016 Cedar Woods Presentation 2 Snapshot of Achievements in FY2016 Extensive portfolio of residential estates

MARKETBEAT RETAIL SNAPSHOT

Bil US$ MARKETBEAT RETAIL SNAPSHOT LAS VEGAS, NV A Cushman & Wakefield Research Publication Q4 2014 NATIONAL ECONOMIC OVERVIEW Like Floyd Mayweather in the final round of a championship match, the U.S

Bil US$ MARKETBEAT RETAIL SNAPSHOT LAS VEGAS, NV A Cushman & Wakefield Research Publication Q4 2014 NATIONAL ECONOMIC OVERVIEW Like Floyd Mayweather in the final round of a championship match, the U.S

Israel. Tourism in the economy. Tourism governance and funding

Israel Tourism in the economy Tourism accounts directly for 2.8% of Israel s GDP and about 3.5% of total employment. The combined total of direct and indirect tourism jobs is estimated at 230 000, representing

Israel Tourism in the economy Tourism accounts directly for 2.8% of Israel s GDP and about 3.5% of total employment. The combined total of direct and indirect tourism jobs is estimated at 230 000, representing

Management Discussions and Analysis for the three-month period ended 31 March 2014 and Executive Summary

Executive Summary Overview of the global economy during the first quarter of 2015 (Q1/2015) are as following; the US economy has been in recovery mode while rapidly dollar appreciation weighs on net exports

Executive Summary Overview of the global economy during the first quarter of 2015 (Q1/2015) are as following; the US economy has been in recovery mode while rapidly dollar appreciation weighs on net exports

Netherlands. Tourism in the economy. Tourism governance and funding

Netherlands Tourism in the economy The importance of domestic and inbound tourism for the Dutch economy is increasing, with tourism growth exceeding the growth of the total economy in the last five years.

Netherlands Tourism in the economy The importance of domestic and inbound tourism for the Dutch economy is increasing, with tourism growth exceeding the growth of the total economy in the last five years.

FAR EAST H-TRUST POSTS 2Q 2014 INCOME AVAILABLE FOR DISTRIBUTION OF $22.1 MILLION

Highlights: FAR EAST H-TRUST POSTS 2Q 2014 INCOME AVAILABLE FOR DISTRIBUTION OF $22.1 MILLION Gross revenue of $29.6 million in 2Q 2014 amidst challenging operating environment Net property income of $26.6

Highlights: FAR EAST H-TRUST POSTS 2Q 2014 INCOME AVAILABLE FOR DISTRIBUTION OF $22.1 MILLION Gross revenue of $29.6 million in 2Q 2014 amidst challenging operating environment Net property income of $26.6

Sweden. Tourism in the economy. Tourism governance and funding

Sweden Tourism in the economy In 2014 Sweden s GDP was SEK 3 907 billion. Tourism s share of GDP is 2.8%, and has been growing steadily for the last ten years and is an important contributor to the economy

Sweden Tourism in the economy In 2014 Sweden s GDP was SEK 3 907 billion. Tourism s share of GDP is 2.8%, and has been growing steadily for the last ten years and is an important contributor to the economy

Summary o f Results for the First Half of FY2018

Summary o f Results for the First Half of FY2018 November 9, 2018 (9005) https://www.tokyu.co.jp/ Contents Ⅰ.Executive Summary 2 Ⅱ.Conditions in Each Business 6 Ⅲ.Details of Financial Results for the 13

Summary o f Results for the First Half of FY2018 November 9, 2018 (9005) https://www.tokyu.co.jp/ Contents Ⅰ.Executive Summary 2 Ⅱ.Conditions in Each Business 6 Ⅲ.Details of Financial Results for the 13

Upgrading Budget Hotels in The Gambia Project Profile

Upgrading Budget Hotels in The Gambia Project Profile April 20 Why The Gambia? Situated on the Atlantic coast and with a navigable river that flows more than,00km inland, The Gambia is the ideal, convenient

Upgrading Budget Hotels in The Gambia Project Profile April 20 Why The Gambia? Situated on the Atlantic coast and with a navigable river that flows more than,00km inland, The Gambia is the ideal, convenient

Minor International Public Company Limited

Minor International Public Company Limited Management Discussion & Analysis MINT s financial performance as of 30th June 2008 Summary of Key Financial Performance 2Q08 Performance Minor International Public

Minor International Public Company Limited Management Discussion & Analysis MINT s financial performance as of 30th June 2008 Summary of Key Financial Performance 2Q08 Performance Minor International Public

MENA HOTEL MARKET REVIEW MUSCAT OMAN 2018

MENA HOTEL MARKET REVIEW MUSCAT OMAN 2018 www.trimideast.com 1 OMR (billion) MENA HOTEL MARKET REVIEW MUSCAT OMAN 2018 OMAN ECONOMIC OVERVIEW Oman s economy continues to be heavily reliant on hydrocarbons,

MENA HOTEL MARKET REVIEW MUSCAT OMAN 2018 www.trimideast.com 1 OMR (billion) MENA HOTEL MARKET REVIEW MUSCAT OMAN 2018 OMAN ECONOMIC OVERVIEW Oman s economy continues to be heavily reliant on hydrocarbons,

DEXUS Property Group (ASX: DXS) ASX release

ASX release") 6 May 2013 DEXUS and DWPF to acquire strategic office investment in Perth DEXUS Property Group (DEXUS or DXS) and DEXUS Wholesale Property Fund (DWPF) today announced the joint acquisition of a strategic

6 May 2013 DEXUS and DWPF to acquire strategic office investment in Perth DEXUS Property Group (DEXUS or DXS) and DEXUS Wholesale Property Fund (DWPF) today announced the joint acquisition of a strategic

The Economic Impact of Tourism in Hillsborough County. July 2017

The Economic Impact of Tourism in Hillsborough County July 2017 Table of contents 1) Key Findings for 2016 3 2) Local Tourism Trends 7 3) Trends in Visits and Spending 12 4) The Domestic Market 19 5) The

The Economic Impact of Tourism in Hillsborough County July 2017 Table of contents 1) Key Findings for 2016 3 2) Local Tourism Trends 7 3) Trends in Visits and Spending 12 4) The Domestic Market 19 5) The

TUI GROUP INVESTOR PRESENTATION

TUI GROUP INVESTOR PRESENTATION German Investment Conference UniCredit / Kepler Munich, 26-27 September 2012 Future-related statements This presentation contains a number of statements related to the future

TUI GROUP INVESTOR PRESENTATION German Investment Conference UniCredit / Kepler Munich, 26-27 September 2012 Future-related statements This presentation contains a number of statements related to the future

GBR HOSPITALITY QUARTERLY NEWSLETTER. on the Greek Hospitality Industry 2012 Q4

GBR HOSPITALITY QUARTERLY NEWSLETTER on the Greek Hospitality Industry 2012 Q4 Introduction This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader

GBR HOSPITALITY QUARTERLY NEWSLETTER on the Greek Hospitality Industry 2012 Q4 Introduction This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader

SHIP MANAGEMENT SURVEY. July December 2017

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

GOING PLACES MACARTHURCOOK OFFICE PROPERTY TRUST

GOING PLACES MACARTHURCOOK OFFICE PROPERTY TRUST ANNUAL REPORT 2006 1 2 3 4 1 2 181 Miller Street, North Sydney, NSW 150 170 Leichhardt Street, Spring Hill, Brisbane, QLD 3 4 38 Akuna Street, Canberra,

GOING PLACES MACARTHURCOOK OFFICE PROPERTY TRUST ANNUAL REPORT 2006 1 2 3 4 1 2 181 Miller Street, North Sydney, NSW 150 170 Leichhardt Street, Spring Hill, Brisbane, QLD 3 4 38 Akuna Street, Canberra,

BANYAN TREE HOLDINGS LIMITED (Company Registration Number: H) COMPANY CONTINUES ITS ASSET REBALANCING STRATEGY.

COMPANY CONTINUES ITS ASSET REBALANCING STRATEGY.") BANYAN TREE HOLDINGS LIMITED (Company Registration Number: 200003108H) COMPANY CONTINUES ITS ASSET REBALANCING STRATEGY. Highlights: 4Q11: - Revenue flat at S$85.4 million. - Operating Profit dropped to

BANYAN TREE HOLDINGS LIMITED (Company Registration Number: 200003108H) COMPANY CONTINUES ITS ASSET REBALANCING STRATEGY. Highlights: 4Q11: - Revenue flat at S$85.4 million. - Operating Profit dropped to

S$ million 2Q2012 2Q2011 Change 1H2012 1H2011 Change Revenue % % Gross Profit % % Gross Profit Margin

Roxy-Pacific Holdings Limited NEWS RELEASE ROXY-PACIFIC ACHIEVES 8% INCREASE IN NET PROFIT TO S$17.7 MILLION IN 2Q2012 - Revenue rises 13% to S$52.7 million - 18% surge in revenue from Property Development

Roxy-Pacific Holdings Limited NEWS RELEASE ROXY-PACIFIC ACHIEVES 8% INCREASE IN NET PROFIT TO S$17.7 MILLION IN 2Q2012 - Revenue rises 13% to S$52.7 million - 18% surge in revenue from Property Development

BEACHSIDE ON THE PARK

Built better. BEACHSIDE ON THE PARK Due Diligence Project Report (07) 5370 1800 info@builtbetter.com.au builtbetter.com.au 1 builtbetter.com.au WELCOME TO BEACHSIDE Beachside on the park has been Constructed

Built better. BEACHSIDE ON THE PARK Due Diligence Project Report (07) 5370 1800 info@builtbetter.com.au builtbetter.com.au 1 builtbetter.com.au WELCOME TO BEACHSIDE Beachside on the park has been Constructed

OPERATING AND FINANCIAL HIGHLIGHTS

Copa Holdings Reports Net Income of US$32.0 Million and EPS of US$0.72 for the Second Quarter of 2012 Excluding special items, adjusted net income came in at $58.6 million, or EPS of $1.32 per share Panama

Copa Holdings Reports Net Income of US$32.0 Million and EPS of US$0.72 for the Second Quarter of 2012 Excluding special items, adjusted net income came in at $58.6 million, or EPS of $1.32 per share Panama

The Economic Impact of Tourism in Maryland. Tourism Satellite Account Calendar Year 2016

The Economic Impact of Tourism in Maryland Tourism Satellite Account Calendar Year 2016 County Results Washington County, Visitors Washington County Visitors (thousands) Year Overnight Day Total Growth

The Economic Impact of Tourism in Maryland Tourism Satellite Account Calendar Year 2016 County Results Washington County, Visitors Washington County Visitors (thousands) Year Overnight Day Total Growth

BANYAN TREE HOLDINGS LIMITED (Company Registration Number: H) 1H07 Results Snapshot (in S$million) : 2Q07 Results Snapshot (in S$million) :

1H07 Results Snapshot (in S$million) : 2Q07 Results Snapshot (in S$million) :") BANYAN TREE HOLDINGS LIMITED (Company Registration Number: 200003108H) BANYAN TREE S HALF YEAR PROFITS UP 55% ON 23% REVENUE GAIN. Highlights: - 1H07 Revenue increased by 23% to S$187.9 million - 1H07

BANYAN TREE HOLDINGS LIMITED (Company Registration Number: 200003108H) BANYAN TREE S HALF YEAR PROFITS UP 55% ON 23% REVENUE GAIN. Highlights: - 1H07 Revenue increased by 23% to S$187.9 million - 1H07

30 degrees in the shade Ideal Conditions For Growth. Corporate Brochure

30 degrees in the shade Ideal Conditions For Growth Corporate Brochure Our Vision......is to fill the gap in the North Cyprus hotel market, by making it accessible to multigenerational visitors desiring

30 degrees in the shade Ideal Conditions For Growth Corporate Brochure Our Vision......is to fill the gap in the North Cyprus hotel market, by making it accessible to multigenerational visitors desiring

MANAGEMENT DISCUSSION AND ANALYSIS

MANAGEMENT DISCUSSION AND ANALYSIS COMPANY AND SUBSIDIARIES FINANCIAL STATUS AND PERFORMANCE MINOR INTERNATIOANL PUBLIC COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 2006 1.) Overview In

MANAGEMENT DISCUSSION AND ANALYSIS COMPANY AND SUBSIDIARIES FINANCIAL STATUS AND PERFORMANCE MINOR INTERNATIOANL PUBLIC COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 2006 1.) Overview In

Chiwayland announces 2Q2016 results, with sights set on international markets and other growth engines

Chiwayland announces 2Q2016 results, with sights set on international markets and other growth engines On track for the delivery of two major property developments by 4Q2016 Barring unforeseen circumstances,

Chiwayland announces 2Q2016 results, with sights set on international markets and other growth engines On track for the delivery of two major property developments by 4Q2016 Barring unforeseen circumstances,

MARKET AND OPERATIONS STUDY OF THE FOUR SEASONS BARBADOS HOTEL PROJECT

MARKET AND OPERATIONS STUDY OF THE FOUR SEASONS BARBADOS HOTEL PROJECT FRESHWATER BAY, BARBADOS Prepared For: INTER-AMERICAN DEVELOPMENT BANK November 4, 2011 Prepared by: Jones Lang LaSalle Hotels 2333

MARKET AND OPERATIONS STUDY OF THE FOUR SEASONS BARBADOS HOTEL PROJECT FRESHWATER BAY, BARBADOS Prepared For: INTER-AMERICAN DEVELOPMENT BANK November 4, 2011 Prepared by: Jones Lang LaSalle Hotels 2333

Yields Report 2018: High End Holiday Homes in the Mediterranean

Yields Report 018: Yields Report 018: It has become clear that the holiday home market is the most evolving branch of the real estate market in the Mediterranean. Having identified the market s dynamics,

Yields Report 018: Yields Report 018: It has become clear that the holiday home market is the most evolving branch of the real estate market in the Mediterranean. Having identified the market s dynamics,

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER. Palmos Analysis Ltd.

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER Palmos Analysis Ltd. March 2014 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its efforts

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER Palmos Analysis Ltd. March 2014 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its efforts

Tourism Snapshot Year-in-review. Facts & Figures 5th edition.

Tourism Snapshot 2010 Year-in-review Facts & Figures 5th edition www.canada.travel/corporate Tourism highlights In 2010, international visitors made15.9 million overnight trips to Canada, up 1.8% compared

Tourism Snapshot 2010 Year-in-review Facts & Figures 5th edition www.canada.travel/corporate Tourism highlights In 2010, international visitors made15.9 million overnight trips to Canada, up 1.8% compared

Dominican Republic. Broker/Owner, Global Properties Realty & Investments, LLC

Dominican Republic Broker/Owner, Global Properties Realty & Investments, LLC National Association of REALTORS Chair CIPS Advisory Board, 2018 NAR President Liaison to the Dominican Republic, 2013 / 2018

Dominican Republic Broker/Owner, Global Properties Realty & Investments, LLC National Association of REALTORS Chair CIPS Advisory Board, 2018 NAR President Liaison to the Dominican Republic, 2013 / 2018

State of the Shared Vacation Ownership Industry. ARDA International Foundation (AIF)

") State of the Shared Vacation Ownership Industry ARDA International Foundation (AIF) This paper includes a high-level overview of the timeshare industry with a core focus on financial growth, owner demographics

State of the Shared Vacation Ownership Industry ARDA International Foundation (AIF) This paper includes a high-level overview of the timeshare industry with a core focus on financial growth, owner demographics

Tourist Traffic in the City of Rijeka For the Period Between 2004 and 2014

Tourist Traffic in the City of Rijeka For the Period Between 2004 and 2014 Rijeka, February 2015. Table of Contents Pg No. 1. Introduction 3 2. Physical indicators on an annual level 4 2.1. Structure and

Tourist Traffic in the City of Rijeka For the Period Between 2004 and 2014 Rijeka, February 2015. Table of Contents Pg No. 1. Introduction 3 2. Physical indicators on an annual level 4 2.1. Structure and

Flughafen Wien Group Continues on Success Path in the First Quarter of 2016

Flughafen Wien Group Continues on Success Path in the First Quarter of 2016 Upward revaluation of stake in Malta Airport and good business development lead to strong increase in the net profit for the

Flughafen Wien Group Continues on Success Path in the First Quarter of 2016 Upward revaluation of stake in Malta Airport and good business development lead to strong increase in the net profit for the

ERW. 083/ ACC012/ th November Subject: Management's Discussion and Analysis period ending 30 th September 2012

ERW. 083/ ACC012/55 12 th November 2012 Subject: Management's Discussion and Analysis period ending 30 th September 2012 Attention: The President, The Stock Exchange of Thailand Dear Sir, The Erawan Group

ERW. 083/ ACC012/55 12 th November 2012 Subject: Management's Discussion and Analysis period ending 30 th September 2012 Attention: The President, The Stock Exchange of Thailand Dear Sir, The Erawan Group

2005 INTERIM ANNOUNCEMENT

(Stock Code: 78) 2005 INTERIM ANNOUNCEMENT FINANCIAL HIGHLIGHTS Six months ended 30th June, 2005 (Unaudited) HK$ M Six months ended 30th June, 2004 (Unaudited and restated) HK$ M % Change Turnover 542.4

(Stock Code: 78) 2005 INTERIM ANNOUNCEMENT FINANCIAL HIGHLIGHTS Six months ended 30th June, 2005 (Unaudited) HK$ M Six months ended 30th June, 2004 (Unaudited and restated) HK$ M % Change Turnover 542.4

El Al Israel Airlines announced today its financial results for the year 2016 and the fourth quarter of the year:

El Al Israel Airlines announced today its financial results for the year 2016 and the fourth quarter of the year: The Company's revenues in 2016 amounted to approx. USD 2,038 million, compared to approx.

El Al Israel Airlines announced today its financial results for the year 2016 and the fourth quarter of the year: The Company's revenues in 2016 amounted to approx. USD 2,038 million, compared to approx.

2011 Hotel investment strategy :

2011 Hotel investment strategy : What every developer should know New World Hotel 27 Sept, 2011 Presented by: Robert McIntosh, Executive Director, CBRE Hotels, Asia Pacific. SUMMARY Hotel Performance Hotel

2011 Hotel investment strategy : What every developer should know New World Hotel 27 Sept, 2011 Presented by: Robert McIntosh, Executive Director, CBRE Hotels, Asia Pacific. SUMMARY Hotel Performance Hotel

OPERATING AND FINANCIAL HIGHLIGHTS

Copa Holdings Reports Net Income of US$18.6 Million and EPS of US$0.42 for the Second Quarter of 2010 Excluding special items, adjusted net income came in at $26.3 million, or $0.60 per share Panama City,

Copa Holdings Reports Net Income of US$18.6 Million and EPS of US$0.42 for the Second Quarter of 2010 Excluding special items, adjusted net income came in at $26.3 million, or $0.60 per share Panama City,

Tourism Investment Potential

Prodexpo October 2016 October 2016 Tourism Investment Potential 1 International Tourist Arrivals & Receipts Greek Tourism continues its positive trend in spite of negative internal and external factors

Prodexpo October 2016 October 2016 Tourism Investment Potential 1 International Tourist Arrivals & Receipts Greek Tourism continues its positive trend in spite of negative internal and external factors

Hong Kong Tourism Industry

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com April 11 Hong Kong Tourism Industry Tourism industry is important Tourism is the fastest growing of the

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com April 11 Hong Kong Tourism Industry Tourism industry is important Tourism is the fastest growing of the

From: OECD Tourism Trends and Policies Access the complete publication at: Chile

From: OECD Tourism Trends and Policies 2014 Access the complete publication at: http://dx.doi.org/10.1787/tour-2014-en Chile Please cite this chapter as: OECD (2014), Chile, in OECD Tourism Trends and

From: OECD Tourism Trends and Policies 2014 Access the complete publication at: http://dx.doi.org/10.1787/tour-2014-en Chile Please cite this chapter as: OECD (2014), Chile, in OECD Tourism Trends and

U.S. HOTEL SUPPLY GROWTH STILL IN CHECK WITH DEMAND

MAY 2015 U.S. HOTEL SUPPLY GROWTH STILL IN CHECK WITH DEMAND Susan Furbay Vice President of Business Development HVS 369 Willis Avenue, Mineola, NY 11501, USA Years of rising average daily rates and demand,

MAY 2015 U.S. HOTEL SUPPLY GROWTH STILL IN CHECK WITH DEMAND Susan Furbay Vice President of Business Development HVS 369 Willis Avenue, Mineola, NY 11501, USA Years of rising average daily rates and demand,

From: OECD Tourism Trends and Policies Access the complete publication at: Mexico

From: OECD Tourism Trends and Policies 2014 Access the complete publication at: http://dx.doi.org/10.1787/tour-2014-en Mexico Please cite this chapter as: OECD (2014), Mexico, in OECD Tourism Trends and

From: OECD Tourism Trends and Policies 2014 Access the complete publication at: http://dx.doi.org/10.1787/tour-2014-en Mexico Please cite this chapter as: OECD (2014), Mexico, in OECD Tourism Trends and

Australia s. The Northern Territory is experiencing solid growth in visitor numbers driven by a strong economy. Northern Territory

Australia s Northern Territory Australia s Northern Territory is a strategic market for tourism investment, with its well established reputation as an iconic tourism destination located on the doorstep

Australia s Northern Territory Australia s Northern Territory is a strategic market for tourism investment, with its well established reputation as an iconic tourism destination located on the doorstep

Alfonso Cardenas Cua Intal Madelar Lubaton Veracruz Alfonso Cardenas Cua Intal Madelar Lubaton Veracruz

Alfonso Cardenas Cua Intal Madelar Lubaton Veracruz Alfonso Cardenas Cua Intal Madelar Lubaton Veracruz 3 Vision-Mission Vision : To become the leading provider and facilitator of value-based luxury, leisure

Alfonso Cardenas Cua Intal Madelar Lubaton Veracruz Alfonso Cardenas Cua Intal Madelar Lubaton Veracruz 3 Vision-Mission Vision : To become the leading provider and facilitator of value-based luxury, leisure

Czech Republic. Tourism in the economy. Tourism governance and funding

Czech Republic Tourism in the economy Tourism s share of GDP in the Czech Republic has been increasing over the last two years from 2.7% in 2012 to 2.9 % in 2013. The number of people employed in tourism

Czech Republic Tourism in the economy Tourism s share of GDP in the Czech Republic has been increasing over the last two years from 2.7% in 2012 to 2.9 % in 2013. The number of people employed in tourism

The Economic Impact of Tourism on Galveston Island, Texas

The Economic Impact of Tourism on Galveston Island, Texas 2017 Analysis Prepared for: Headline Results Headline results Tourism is an integral part of the Galveston Island economy and continues to be a

The Economic Impact of Tourism on Galveston Island, Texas 2017 Analysis Prepared for: Headline Results Headline results Tourism is an integral part of the Galveston Island economy and continues to be a

Sofia City Report H City Reports

Sofia City Report H1 2016 City Reports Gross Salary Q1 Economy & Investment GDP growth Q1 y-o-y 2.9% 650 Inflation May y-o-y - 2.0% Unemployment Rate Q1 8.6% Source: National Statistical Institute of Republic

Sofia City Report H1 2016 City Reports Gross Salary Q1 Economy & Investment GDP growth Q1 y-o-y 2.9% 650 Inflation May y-o-y - 2.0% Unemployment Rate Q1 8.6% Source: National Statistical Institute of Republic

Quarterly Report Egypt Hotels Q Egypt Quarterly Review & Forecast 4 Key Cities

Quarterly Report Egypt Hotels Q1 2016 Egypt Quarterly Review & Forecast 4 Key Cities Contents Cairo... 3 Sharm El Sheikh... 4 Hurghada... 5 Alexandria... 6 2 Cairo SUPPLY Forthcoming pipeline in Cairo

Quarterly Report Egypt Hotels Q1 2016 Egypt Quarterly Review & Forecast 4 Key Cities Contents Cairo... 3 Sharm El Sheikh... 4 Hurghada... 5 Alexandria... 6 2 Cairo SUPPLY Forthcoming pipeline in Cairo