CRETE PROPERTY MARKET. 2nd Semester 2016

|

|

|

- Beverly Mason

- 6 years ago

- Views:

Transcription

1 CRETE PROPERTY MARKET 2nd Semester 2016

2 Table of Contents 1. Economic Overview Office Market Residential Market Retail Market Logistics & Industrial Market Tourism... 19

3 1. Economic Overview Greek economy is gradually returning to positive development rates. The GDP was increased by +1,8% in the third quarter of 2016 on annual base (over +1,5% according to the initial valuations of ELSTAT), primarily due to the increase of private consumption by +5,1% (over -4,1% decrease in the third quarter of 2015), which was supported by the rise of salaries in the economy overall (+2,1% in real terms in the 3 rd quarter of 2016). At the same time, activity in most of the sectors and specifically the industrial, retail and tourism is increased as Greek exportations seem to retrieve the dynamic they used to have in More specifically within the positive progressions are included: - The boost of industrial production in processing except oil products in October 2016 (+6,7% over -1,2% reduction in October 2015), for 5 months in row (+3,6% for the period January October 2016), as well as in most of the industrial sectors (+8,9% in oil products, +8,9% in electricity, +2,6% in water provision). - The rise in sales in processing except oil products for 4 months in row in September 2016 (+1,4% over -1,7% in September 2015), which resulted to the supplementation of large part of the losses of the first five months of 2016 (-0,7% overall for the period January September 2016). - The continuation of the increase of the exportable commodities apart from fuels in October 2016 (+2,6% in value and +4,6% in volume) for 4 months in row (+1,2% in value and +4,8% in volume for the period January October 2016), especially food products and various industrial products (+10,5% and +7,3% respectively for the period Jan Oct 2016). - The boost of turnovers in most of the sectors during the third quarter of 2016, especially in wholesale (+3,2% after 7 continuous quarters of downward trend), tourism (+2,6% after decrease in the past 3 quarters and additional increase +4,8% in the third quarter of 2015), land and air transportations (+3,3% and +7,4% respectively) and the car sector (+18,6%). - The improved conditions in services and retail in November 2016, with business expectations being on a positive track. - The stable even though slow, decrease of the unemployment rate (23,1% in September 2016, from 23,3% of the previous month and 24,7% in September 2015). It is noted that the increase of the number of the registered unemployed by 12,3 thousand in October 2016, over 8,4 thousand who had been added in October 2015, is relevant to the end of the tourist period and the great number of recruitments made primarily by hotels and restaurants, the period prior to summer.

4 On the other hand, there are still recorded trends which show that economy is still facing difficulties such as: - The decrease of consumptive trust to -66,9 units in November 2016, after a rise that took place the previous two months, as a result of the deterioration of the consumers predictions regarding their economic situation and the country s situation as a whole the next 12 month period, apparently influenced by the impending over-taxation in 2017 and the new measures which are about to be implemented for the second assessment of the program. - The deterioration of the entrepreneurial expectations in industry in November 2016, with the predictions about the production levels, the new orders and exportations slightly falling and the predictions regarding the employment progression being less promising. At the same time the PMI index in processing was formed to 48,3 units from 48,6 units the previous month, showing a relevant image regarding the production levels and new orders whereas the variation of job vacancies remained on positive track. - The triple cost of businesses lending in comparison to the European average and the non-performing bank loans of ~107 billion. Apart from the above issues, the country is implementing a strict fiscal policy which according to the Eurogroup s decision of the 5/12/2016 will be preserved even after 2018, creating concerns in the market for further increase of the over-taxation and attenuation of the developing dynamic which is formed. Definitely the achievement of the program s targets is necessary for the restoration of the credibility of the economic policy. Conclusion The austerity measures implementation process that Greece adopted since the signature of the first Memorandum is highly demanding. Having achieved a considerable decrease of the General Government Spending to 55.7 billion euros from 2008 till now (-30%) on one hand and an impressive shrinkage of the General Government Balance to 4.6% of GDP (from 15.4% in 2008) on the other hand, Greece still faces problems however, since GDP (175.6 billion euros) is consistently shrinking.

5 2. Office Market Office market in Crete remained almost stable during H2 of 2016, while relative to 2014, market and rental values were decreased up to 5-10%. Despite the fact that asking prices are nowadays at quite low levels, asking prices are still negotiable and can be decreased up to 10-15%. Prime yields have seen a slight compression during the past semester, since the effects of the capital controls were not as severe as originally predicted and investors have been actively looking for opportunities. In Chania, rental values around the Court Square are higher relatively to the city center, due to the privileged location of the square, which is close to the building of the Regional Union of Chania and the Court House, while the higher market values can be found at the city center (Skalidi & Giannari Streets, 1866 Square). Trianon Center in Court Area, Chania In Heraklion, the vast majority of office spaces are congregated around the city center (Zografou St, Daidalou St, Dimokratias St, Dikaiosinis St, 25 th August St, Evans St, Kalokairinou St, Averof St, Liontaria Square), where freelances and businesses are highly interested due to the proximity to public services. On the other hand, there is no interest for offices spaces outside the city center and in low commercial streets. In Rethymnon, the main office market is around the CBD, the Old City and Iroon Polytechniou Square, close to the main retail market and public services buildings, while relatively new office spaces can be found at the main streets that lead to the CBD, i.e. Igoumenou Gavriil Avenue (west entrance) and Portaliou Avenue (east entrance).

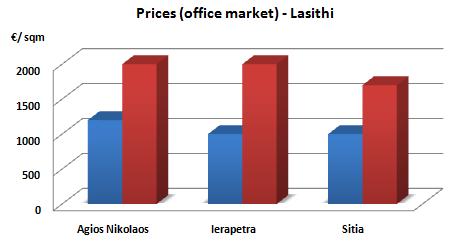

6 Finally, in Lasithi, due to the small size of the cities of Agios Nikolaos, Ierapetra and Sitia, office spaces are congregated only in the center of the cities. Source: Danos Melakis Ltd

7 Source: Danos Melakis Ltd

8 Source: Danos Melakis Ltd Source: Danos Melakis Ltd

9 * Leases and prices depend on the age, the condition and the location of the buildings. 3. Residential Market After the announcement of the national elections in January 2015, there was a significant increase in the demand for small apartments mainly, since many people decided to withdraw their deposits and invest them in old and economical apartments. The recent activity in the real estate market showed that residences turned into a safe investment for many people with anxiety and economic insecurity. However, this small activity did not manage to reverse the negative climate in real estate market and was sharply interrupted by the introduction of capital controls, while the main reasons that the market hasn t picked up yet are the lack of new bank loans and no recovery of the mortgage market. The residential market is still a deep sleeper with minimum transactions with prices decreased slightly in most areas, with only a few prime areas showing signs of stability. There was a pickup in rental activity with high demand for medium size and good quality homes. It is worth mentioning that asking prices have decreased up to 10% in comparison with 2014, while negotiations usually result in a price cut over 10-15%. As for the holiday residence sector, many investment opportunities can be found, due to the significant price decreases during the past years. Almost 5,000 holiday residences in Crete are for sale, a number that remained almost stable during the last five years, since construction activity has stopped and investing interest still remains at low levels. At the same time, market values have decreased up to 40% and sometimes even more relative to the period before crisis. In general, it is believed that residential market has bottomed out during H2 of 2015 and has entered into a recovery path since the beginning of 2016, as the economy stabilizes, helping to reinforce the recovery of the economy as a whole. In Chania, around CBD, the vast majority of residences are at least year old and the price range is from /sqm, depending on the exact location, age and level of maintenance, while new structures prices vary from /sqm. The prices regarding new conventional structures in popular residential areas near CBD vary from /sqm in Chalepa, from /sqm in Lentariana & Aberia and from /sqm in Nea Chora. As for rental prices, they remained almost stable relative to 2015.

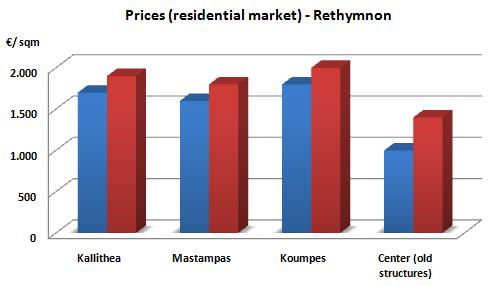

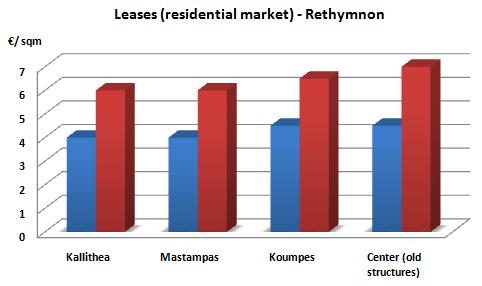

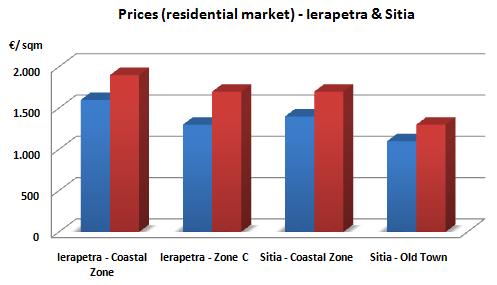

10 In Heraklion, around CBD, the vast majority of residences are at least 25 years old, whose price range is from /sqm, depending on the level of maintenance and the parking availability. The price range for new residences in popular areas near the CBD, such as Analispi, Mastampas and Therissos, is from /sqm. The same price range stands also in the suburb of Agios Ioannis. Regarding the rest suburbs (Deilina, Koroni Magara, Mesampelies, Pateles, Poros, Katsampas and Mpenntevi), the price range is from /sqm. As for rental prices, they remained almost stable relative and vary from 4 6 /sqm, with the upper levels representing residences in the CBD or popular suburbs, such as Agios Ioannis. In Rethymnon, the vast majority of residences in the Old City are old structures whose price range is from /sqm, mainly depending on the level of maintenance. The price range for new conventional residences in areas near CBD, such as Kallithea, Mastampas and Koumpes, is from /sqm, depending on the characteristics of the property, such as location, floor level, view and size. As for rental prices, they remained almost stable relative to 2015, with a reduction of almost 10% since New Apartment Complexes in Heraklion and Rethymno Finally, in Lasithi, the highest market values can be found at the coastal zone as well as the new suburbs of Agios Nikolaos, Ierapetra and Sitia, due to the most recent structures that can be found there, while market values at the old sections of the cities are slightly smaller. Rental prices remained almost stable relative to 2015.

11 Source: Danos Melakis Ltd

12 Source: Danos Melakis Ltd

13 Source: Danos Melakis Ltd

14 4. Retail Market Source: Danos Melakis Ltd In Chania, the most commercial area is the Old Port, where rental values vary from /sqm and from /sqm at Koum Kapi, while the most commercial roads are Chalidon, Chatzimichali Giannari and Skalidi Streets (main area of retail market), where rental values vary from /sqm. The new H&M store at Tzanakaki Street and the pedestrianisation of Potie area have led to higher rental values and increased absorption in these two areas. In Heraklion, there is a high interest for retail stores within the old walls and especially the CBD. The most commercial areas are Daidalou Street, 1866 Street and Liontaria Square, where rental values vary from /sqm. Shopping Center Olea in Platanias Shopping Center Talos Plaza in Heraklion

and from 10 15 /sqm in secondary streets (Gerakari, Ethnikis Antistaseos).")

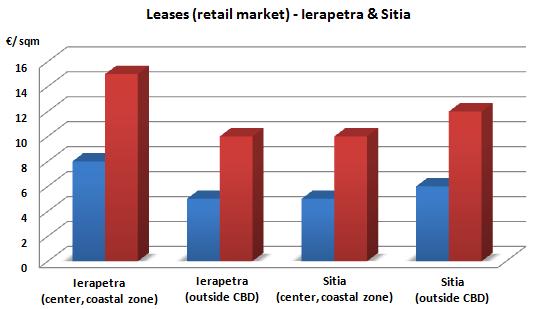

15 In Rethymnon, within the Old Town, rental values vary from /sqm in Arkadiou Street ( prices at the north part) and from /sqm in secondary streets (Gerakari, Ethnikis Antistaseos). Finally, in Lasithi, commercial activity is found only in the cities center and the coastal zones. The relatively small offer of retail stores has led to very high market and rental values in some cases. Source: Danos Melakis Ltd

16 Source: Danos Melakis Ltd

17 Source: Danos Melakis Ltd

18 5. Logistics & Industrial Market In Crete, no interest is observed in logistics and industrial market; therefore market has remained stable during H Large storage units can be mainly found in Heraklion and Chania, due to the presence of industrial parks, airports and large commercial ports in the two cities. Rental values vary from 2-4 /sqm in Heraklion and from /sqm in Chania. As for the regional units of Rethymnon and Lasithi, there is no formed real estate market in this sector, since the few large storage units are constructed upon request and based on the customer s needs. Finally as far as the industrial park of Rethimno in the area of Agia Triada is concerned, the total number of plots have been available since 2010 and there have been constructed complete infrastructure networks as well as public installations, however only one business has been installed until today, which is a sign of the big crisis that the sector is facing nowadays.

19 6. Tourism Tourism is one of the few sectors of the Greek national economy that is competitive at a global level. Despite the lingering economic challenges and the slow down due to the major politic developments, tourism sector showed remarkable strength and 2015 was a record year. The unique geographical characteristics, in combination with the highly developed and still fast developing transportation infrastructure, the development and modernization of more specific tourist facilities, are expected to contribute to the development of Greece as a major tourist destination in Europe and as an international transportation hub of European proportions. Airports Arrivals As far as the city of Chania is concerned, during 2016, passengers were transported within the country ( arrivals, departures), according to official data of the airport of Chania passengers were transported by Ryanair, passengers by Aegean (Aegean and Olympic Air) and passengers by other air companies. It is observed increase in the number of all the main nationalities who visit western Crete except Danish, the arrivals of whom have been reduced by 4%. On the contrary the greatest rise is recorded by British with 34%, getting the 3 rd place from Danish and as a result they win one of the first places as far as the total number of arrivals is concerned. As a matter of fact, the last 6 years has been recorded continuous rise by British, almost quadrupling their arrivals at Chania airport. Half foreigner tourists who visit Chania airport come from non-scandinavian countries confirming also this year the continuous increase of these nationalities. The upward trend which is observed since 2010 is mainly attributed to the dynamic presence of the low cost airline company Ryanair which occupies almost 30% of the total arrivals, 9 out of ten passengers of which come from non-scandinavian countries, alternating the mixture of tourists who choose Chania airport as final destination. Increase in the total number of foreigner tourists arrivals is also observed at Heraklion airport, where 65% consists of German, British, French and Russians. The positive change is contributed to the increase of all the main nationalities who prefer Heraklion airport and specifically Russian tourists, who increase their arrivals by 42% in comparison to the high reduction of the former two years.

20 It is worth noticing, that as it is mentioned by executives of the Service of Civil Aviation, according to statistical data of the last year, the airport which recorded the highest percentage of increase of passengers transportation, (within the category of airports with passenger activity over 4 million), is the Heraklion airport with a rise of 13,3%. Based on statistical data about December2016, its results that the rise in inbound passengers was 10,5% and 19,1% for outbound passengers. Overall, at the airports of Athens, Thessaloniki, Heraklio, Chania and Rhodes, is recorded the greatest passenger activity for December Based on temporary data of SETE, the monthly international arrivals for 2016 at the airports of Heraklion and Chania are as follows: INTERNATIONAL ARRIVALS 2016 Herakleion Chania January 0 2,258 February 185 2,213 March 10,225 9,548 April 120,125 53,909 May 343, ,349 June 456, ,017 July 608, ,817 August 604, ,922 September 479, ,259 Οctober 258,064 91,012 Νovember 3,028 3,310 December 1,007 2,258 Total 2,885,154 1,048,872 Sete.gr

21 Ports - Arrivals As far as the cruises are concerned, 2016 was a successful year for the city of Chania as there were conducted almost 100 cruise arrivals at the two ports (Souda port and the Venetian port). As a matter of fact, Chania is in the 8 th place among the most popular cruise destinations in Greece while the arrival of more than passengers by cruises in 2016 is a high record for the city. As far as the rest of Crete is concerned, in 2016, 165 ships with passengers arrived. In Agios Nikolaos 49 ships with passengers arrived and in Rethimno were conducted 3 cruise arrivals with 400 passengers. Investments There is strong interest from private equity funds and investors and international firms along with world calibre operators to expand in the Greek market, enhance infrastructure and attract more tourists, mainly of a higher level of income. The investment interest includes existing tourist hotel units of medium or large size, large seaside plots as well as small private islands. As for Crete, there is interest for large seaside plots mainly in Eastern Crete, while since the last two years there has been strong interest for small boutique hotels in the Venetian Port of Chania. Within the second semester of 2016, the hotel Olive Green Hotel operated in the city centre of Heraklion. It was first built in 1960 and was then reconstructed by the Hotel Group Karataraki to the first eco and smart hotel in Crete, 100% environmentally friendly. The hotel includes 48 rooms while the biggest part of the energy requirements is covered by solar panels and other innovative systems.

22 Olive green hotel Heraklion It has been also initiated the construction of a new 5* hotel unit of 240 beds of Karantzis Group, in the area of Chersonisos. The hotel unit is being constructed on a seaside plot of 32 hectares. The investment which has been subsumed into the Investment Law is a 14,55 million budget with a financing rate of 30%. At the same time the affiliated company of the Group Stell Polaris Creta is planning the construction of a new 5* hotel unit and of 597 beds in Agios Ioannis region in Ierapetra, an investment for which the Building License has been already issued. As far as the area of Lasithi is concerned, the investment by the joint venture MIRUM HELLAS is under consideration. The investment is of a budget of 400 million which includes the plan Elounda Hills in Agios Nikolaos and is about the construction of residences, hotels and other infrastructures. As for Chania, in 2016 there were added two investments in the luxury resorts category. The one is the Domez Noruz Chania Autograph Collection which has been offering unique services since July, having a merchant corporation with the Mariott Group. The other one is the new five-star hotel Anemos Luxury Grand at Georgioupolis coast. The hotel consists of 240 luxury rooms, 4 shared pools, 60 private pools, 3 restaurants, 4 bars, conference rooms and a spa center.

23 At the same time the Mathioulakis Group has initiated a new five star hotel unit at the north coast of Chania. It consists of 300 beds while in the area is expected to be added another resort of half capacity but of equivalent category. Anemos Luxury Grand Resort, Georgioupolis, Chania.

24 GREECE Athens 15 Vouliagmenis Ave., Τel.: Fax: office@danos.gr Thessaloniki 4 Ionos Dragoumi Str., Τel.: Fax: info.thes@danos.gr Crete - Chania 3 Iroon Polytechniou Str., Τel.: Fax: info.crete@danos-melakis.gr Crete - Heraklion 7 Doukos Beaufort Str., Tel.: Fax: info.crete@danos-melakis.gr CYPRUS Nicosia 35 I. Hatziiosif Ave., 2027 Strovolos Τel.: Fax: sales@danos.com.cy Limassol 69 Gladstonos Str., 3040 Acropolis Centre, Shop 10 Τel.: Fax: limassoldanos@danos.com.cy SERBIA Belgrade 3 Spanskih Βoraca Str , New Belgrade Tel.: Fax: office@danos.rs

25 DISCLAIMER This report is published for general information only. Although high standards have been used in the preparation of the information, analysis, view and projections presented in this report, no legal responsibility can be accepted by DANOS or BNP PARIBAS RE for any loss or damage resultant from the contents of this document. As a general report this material does not necessarily represent the view of DANOS or BNP PARIBAS RE in relation to particular properties or projects. Reproduction of this report in whole or in part is allowed with proper reference to DANOS Research.

CRETE PROPERTY MARKET. 2 nd Semester 2015

1 CRETE PROPERTY MARKET 2 nd Semester 2015 2 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market... 19 6.

1 CRETE PROPERTY MARKET 2 nd Semester 2015 2 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market... 19 6.

CRETE PROPERTY MARKET 2 nd Semester 2013

1 CRETE PROPERTY MARKET 2 nd Semester 213 2 Table of Contents 1. Office Market... 3 2. Residential Market... 6 3. Retail Market... 9 4. Logistics & Industrial Market... 13 5. Hotel and Tourism... 13 3

1 CRETE PROPERTY MARKET 2 nd Semester 213 2 Table of Contents 1. Office Market... 3 2. Residential Market... 6 3. Retail Market... 9 4. Logistics & Industrial Market... 13 5. Hotel and Tourism... 13 3

THESSALONIKI PROPERTY MARKET. 2nd Semester 2014

THESSALONIKI PROPERTY MARKET 2nd Semester 2014 1. Economic Overview & Indices The substantial progress that Greece has made during 2013 and 2014 has been evident with the return of the Greek state and

THESSALONIKI PROPERTY MARKET 2nd Semester 2014 1. Economic Overview & Indices The substantial progress that Greece has made during 2013 and 2014 has been evident with the return of the Greek state and

CRETE PROPERTY MARKET. 1st Semester 2018

CRETE PROPERTY MARKET 1st Semester 2018 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 10 4. Retail Market... 16 5. Logistics & Industrial Market... 20 6. Tourism...

CRETE PROPERTY MARKET 1st Semester 2018 Table of Contents 1. Economic Overview... 3 2. Office Market... 5 3. Residential Market... 10 4. Retail Market... 16 5. Logistics & Industrial Market... 20 6. Tourism...

CRETE PROPERTY MARKET. 2 nd Semester 2014

1 CRETE PROPERTY MARKET 2 nd Semester 2014 2 Table of Contents 1. Economic Overview & Indices... 3 2. Office Market... 4 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market...

1 CRETE PROPERTY MARKET 2 nd Semester 2014 2 Table of Contents 1. Economic Overview & Indices... 3 2. Office Market... 4 3. Residential Market... 9 4. Retail Market... 14 5. Logistics & Industrial Market...

THESSALONIKI PROPERTY MARKET. 1st Semester 2016

THESSALONIKI PROPERTY MARKET 1st Semester 2016 Economic Overview & Indices The outcome of the referendum in the United Kingdom in support of the exit from the European Union creates an unstable European

THESSALONIKI PROPERTY MARKET 1st Semester 2016 Economic Overview & Indices The outcome of the referendum in the United Kingdom in support of the exit from the European Union creates an unstable European

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 2nd Semester 2016 Economic Overview Greek economy is gradually returning to positive development rates. The GDP was increased by +1,8% in the third quarter of 2016 on annual

THESSALONIKI PROPERTY MARKET 2nd Semester 2016 Economic Overview Greek economy is gradually returning to positive development rates. The GDP was increased by +1,8% in the third quarter of 2016 on annual

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET. 2nd Semester 2015

THESSALONIKI PROPERTY MARKET 2nd Semester 2015 Economic Overview & Indices 2015 was crucial for Greece due to the progress of negotiations with its international creditors. As a result, the signs of improvement

THESSALONIKI PROPERTY MARKET 2nd Semester 2015 Economic Overview & Indices 2015 was crucial for Greece due to the progress of negotiations with its international creditors. As a result, the signs of improvement

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET 1 st Semester 2018 Economic Overview The upward trend of the economy continued for the fifth consecutive quarter. Specifically, in the first quarter of 2018 real GDP grew by

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 2 nd Semester 2017 Economic Overview & Indices Real GDP growth (Annual percent change) The completion of the second EU program review in June 2017 buoyed confidence, supporting

THESSALONIKI PROPERTY MARKET 2 nd Semester 2017 Economic Overview & Indices Real GDP growth (Annual percent change) The completion of the second EU program review in June 2017 buoyed confidence, supporting

THESSALONIKI PROPERTY MARKET

THESSALONIKI PROPERTY MARKET 1 st Semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on

THESSALONIKI PROPERTY MARKET 1 st Semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on

PROPERTY MARKET ATHENS 1 st semester 2017

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

PROPERTY MARKET ATHENS 1 st semester 2017

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

PROPERTY MARKET ATHENS 1 st semester 2017 Economic Overview According to the data of the Greek Statistical Authority (provisional data, 1 st quarter of 2017), Gross Domestic Product (GDP) based on seasonally

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER. March Palmos Analysis. March 11

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER March 2011 Palmos Analysis March 11 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER March 2011 Palmos Analysis March 11 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its

PROPERTY MARKET ATHENS 2 nd semester 2017

PROPERTY MARKET ATHENS 2 nd semester 2017 Economic Overview & Indices The completion of the second EU program review in June 2017 buoyed confidence, supporting activity. Employment growth is buttressing

PROPERTY MARKET ATHENS 2 nd semester 2017 Economic Overview & Indices The completion of the second EU program review in June 2017 buoyed confidence, supporting activity. Employment growth is buttressing

The contribution of Tourism to the Greek economy in 2017

The contribution of Tourism to the Greek economy in 2017 1 st edition (provisional data) May 2018 Dr. Aris Ikkos, ISHC Research Director Serafim Koutsos Analyst INSETE Republishing is permitted provided

The contribution of Tourism to the Greek economy in 2017 1 st edition (provisional data) May 2018 Dr. Aris Ikkos, ISHC Research Director Serafim Koutsos Analyst INSETE Republishing is permitted provided

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER. Palmos Analysis Ltd.

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER Palmos Analysis Ltd. March 2014 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its efforts

Thessaloniki Chamber of Commerce & Industry TCCI BAROMETER Palmos Analysis Ltd. March 2014 TCCI BAROMETER (Executive Summary) Thessaloniki Chamber of Commerce and Industry (TCCI), consistent to its efforts

RESEARCH INDUSTRIAL SNAPSHOT

RESEARCH INDUSTRIAL SNAPSHOT GREATER LONDON AND WESTERN HOME COUNTIES H2 2017 GREATER LONDON & WESTERN HOME COUNTIES LOGISTICS & INDUSTRIAL RESEARCH Introduction As the UK economy continues to grow so

RESEARCH INDUSTRIAL SNAPSHOT GREATER LONDON AND WESTERN HOME COUNTIES H2 2017 GREATER LONDON & WESTERN HOME COUNTIES LOGISTICS & INDUSTRIAL RESEARCH Introduction As the UK economy continues to grow so

1. Serbia Key Facts. Picture: Belgrade s municipalities. Picture: Knez Mihailova Street

1. Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 10 and N 7, on the way from Europe to Asia. The

1. Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 10 and N 7, on the way from Europe to Asia. The

Serbia Key Facts. Serbia in Europe. Belgrade s urban municipalities

Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 1 and N 7, on the way from Europe to Asia. The Republic

Serbia Key Facts Located in Southeast Europe, Serbia represents central part of the Balkan Peninsula, at the intersection of Pan European Corridors N 1 and N 7, on the way from Europe to Asia. The Republic

Tourism Investment Potential

Prodexpo October 2016 October 2016 Tourism Investment Potential 1 International Tourist Arrivals & Receipts Greek Tourism continues its positive trend in spite of negative internal and external factors

Prodexpo October 2016 October 2016 Tourism Investment Potential 1 International Tourist Arrivals & Receipts Greek Tourism continues its positive trend in spite of negative internal and external factors

South Aegan Region (Greece)

") South Aegan Region (Greece) South Aegan Region 1. Introduction The South Aegean Region is situated in the south-eastern border of Greece and constitutes at the same time, along with Cyprus, the south-eastern

South Aegan Region (Greece) South Aegan Region 1. Introduction The South Aegean Region is situated in the south-eastern border of Greece and constitutes at the same time, along with Cyprus, the south-eastern

Israel. Tourism in the economy. Tourism governance and funding

Israel Tourism in the economy Tourism accounts directly for 2.8% of Israel s GDP and about 3.5% of total employment. The combined total of direct and indirect tourism jobs is estimated at 230 000, representing

Israel Tourism in the economy Tourism accounts directly for 2.8% of Israel s GDP and about 3.5% of total employment. The combined total of direct and indirect tourism jobs is estimated at 230 000, representing

MARKETBEAT RETAIL SNAPSHOT

Bil US$ MARKETBEAT RETAIL SNAPSHOT LAS VEGAS, NV A Cushman & Wakefield Research Publication Q4 2014 NATIONAL ECONOMIC OVERVIEW Like Floyd Mayweather in the final round of a championship match, the U.S

Bil US$ MARKETBEAT RETAIL SNAPSHOT LAS VEGAS, NV A Cushman & Wakefield Research Publication Q4 2014 NATIONAL ECONOMIC OVERVIEW Like Floyd Mayweather in the final round of a championship match, the U.S

JUNE18 NEWSLETTER GREECE IN NUMBERS RENEWABLE ENERGY SOURCES GREEK F&B EXPORTS

GREEK F&B EXPORTS RENEWABLE ENERGY SOURCES GREECE IN NUMBERS The newsletter is a monthly publication of Enterprise Greece, the national investment and trade promotion agency. Greek F&B Industry Enters

GREEK F&B EXPORTS RENEWABLE ENERGY SOURCES GREECE IN NUMBERS The newsletter is a monthly publication of Enterprise Greece, the national investment and trade promotion agency. Greek F&B Industry Enters

Tourism Dynamics Issue 1

October 2014 Tourism Dynamics Issue 1 At a Glance In this issue Tourist arrivals 3 Arrivals of tourists per 3 country Opportunities ahead 4 Income from tourism 4 key GDP component Income by country 5 New

October 2014 Tourism Dynamics Issue 1 At a Glance In this issue Tourist arrivals 3 Arrivals of tourists per 3 country Opportunities ahead 4 Income from tourism 4 key GDP component Income by country 5 New

Tourism in numbers

Tourism in numbers 2013-2014 Glenda Varlack Introduction Tourism is a social, cultural and economic experience which involves the movement of people to countries or places outside their usual environment

Tourism in numbers 2013-2014 Glenda Varlack Introduction Tourism is a social, cultural and economic experience which involves the movement of people to countries or places outside their usual environment

The Economic Impact of Tourism in North Carolina. Tourism Satellite Account Calendar Year 2013

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2013 Key results 2 Total tourism demand tallied $26 billion in 2013, expanding 3.9%. This marks another new high

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2013 Key results 2 Total tourism demand tallied $26 billion in 2013, expanding 3.9%. This marks another new high

GBR HOSPITALITY QUARTERLY NEWSLETTER. on the Greek Hospitality Industry 2012 Q4

GBR HOSPITALITY QUARTERLY NEWSLETTER on the Greek Hospitality Industry 2012 Q4 Introduction This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader

GBR HOSPITALITY QUARTERLY NEWSLETTER on the Greek Hospitality Industry 2012 Q4 Introduction This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader

The Economic Impact of Tourism in North Carolina. Tourism Satellite Account Calendar Year 2015

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2015 Key results 2 Total tourism demand tallied $28.3 billion in 2015, expanding 3.6%. This marks another new high

The Economic Impact of Tourism in North Carolina Tourism Satellite Account Calendar Year 2015 Key results 2 Total tourism demand tallied $28.3 billion in 2015, expanding 3.6%. This marks another new high

ANA HOLDINGS Financial Results for the Three Months Ended June 30, 2018

ANA HOLDINGS NEWS ANA HOLDINGS Financial Results for the Three Months Ended June 30, 2018 TOKYO, July 31, 2018 ANA HOLDINGS INC. (hereinafter ANA HD ) today reports its financial results for the three

ANA HOLDINGS NEWS ANA HOLDINGS Financial Results for the Three Months Ended June 30, 2018 TOKYO, July 31, 2018 ANA HOLDINGS INC. (hereinafter ANA HD ) today reports its financial results for the three

Tourism Development in Greece Background facts & current policy issues

Tourism Development in Greece Background facts & current policy issues Georgios Drakopoulos Director General, SETE & Chairman, UNWTO Business Council Meeting with the French Counselors for Foreign Trade

Tourism Development in Greece Background facts & current policy issues Georgios Drakopoulos Director General, SETE & Chairman, UNWTO Business Council Meeting with the French Counselors for Foreign Trade

Czech Republic. Tourism in the economy. Tourism governance and funding

Czech Republic Tourism in the economy Tourism s share of GDP in the Czech Republic has been increasing over the last two years from 2.7% in 2012 to 2.9 % in 2013. The number of people employed in tourism

Czech Republic Tourism in the economy Tourism s share of GDP in the Czech Republic has been increasing over the last two years from 2.7% in 2012 to 2.9 % in 2013. The number of people employed in tourism

Tourism Satellite Account Calendar Year 2010

The Economic Impact of Tourism in Georgia Tourism Satellite Account Calendar Year 2010 Highlights The Georgia visitor economy rebounded in 2010, recovering 98% of the losses experienced during the recession

The Economic Impact of Tourism in Georgia Tourism Satellite Account Calendar Year 2010 Highlights The Georgia visitor economy rebounded in 2010, recovering 98% of the losses experienced during the recession

OCTOBER17 NEWSLETTER FOREIGNERS BUYING GREEK PROPERTY ECONOMY GROWS FURTHER FOOD EXPORTS GROWING GERMAN TOUR GROUP INVESTS IN GREECE

FOOD EXPORTS GROWING FOREIGNERS BUYING GREEK PROPERTY ECONOMY GROWS FURTHER GERMAN TOUR GROUP INVESTS IN GREECE The newsletter is a monthly publication of the Enterprise Greece, the national trade and

FOOD EXPORTS GROWING FOREIGNERS BUYING GREEK PROPERTY ECONOMY GROWS FURTHER GERMAN TOUR GROUP INVESTS IN GREECE The newsletter is a monthly publication of the Enterprise Greece, the national trade and

Nairobi Hospitality Report 2017, & Cytonn Monthly November 2017

Nairobi Hospitality Report 2017, & Cytonn Monthly November 2017 Focus of the Week In October 2016, we released Kenya s-hospitality-sector-report dubbed Sailing Through The Storm. According to the report,

Nairobi Hospitality Report 2017, & Cytonn Monthly November 2017 Focus of the Week In October 2016, we released Kenya s-hospitality-sector-report dubbed Sailing Through The Storm. According to the report,

1.2% 3.5% 13.2% Inflation May 2017 y-o-y. Retail Sales, May 2017 y-o-y

City Report Q2 2017 1.2% 3.5% 13.2% GDP Growth Q1 2017 y-o-y Inflation May 2017 y-o-y Unemployment rate Q1 2017, Belgrade 489 11.1% 6.2% Net Salary May 2017, Belgrade Retail Sales, May 2017 y-o-y Industrial

City Report Q2 2017 1.2% 3.5% 13.2% GDP Growth Q1 2017 y-o-y Inflation May 2017 y-o-y Unemployment rate Q1 2017, Belgrade 489 11.1% 6.2% Net Salary May 2017, Belgrade Retail Sales, May 2017 y-o-y Industrial

Yields Report 2018: High End Holiday Homes in the Mediterranean

Yields Report 018: Yields Report 018: It has become clear that the holiday home market is the most evolving branch of the real estate market in the Mediterranean. Having identified the market s dynamics,

Yields Report 018: Yields Report 018: It has become clear that the holiday home market is the most evolving branch of the real estate market in the Mediterranean. Having identified the market s dynamics,

SHIP MANAGEMENT SURVEY* July December 2015

SHIP MANAGEMENT SURVEY* July December 2015 1. SHIP MANAGEMENT REVENUES FROM NON- RESIDENTS Ship management revenues dropped marginally to 462 million, following a decline in global shipping markets. Germany

SHIP MANAGEMENT SURVEY* July December 2015 1. SHIP MANAGEMENT REVENUES FROM NON- RESIDENTS Ship management revenues dropped marginally to 462 million, following a decline in global shipping markets. Germany

SERBIAN MARKET OVERVIEW 1st semester 2017

SERBIAN MARKET OVERVIEW 1 st semester 2017 Economic Overview Serbia economic activity has marked continual positive trends during 2017, recording modest GDP growth of 1% in line with the projections at

SERBIAN MARKET OVERVIEW 1 st semester 2017 Economic Overview Serbia economic activity has marked continual positive trends during 2017, recording modest GDP growth of 1% in line with the projections at

I ll give you an overview of financial results for the first half of fiscal year 2017 and topics of each business, mainly Shopping Complex Business.

I ll give you an overview of financial results for the first half of fiscal year 2017 and topics of each business, mainly Shopping Complex Business. Page 2 shows a summary. Let me begin with consolidated

I ll give you an overview of financial results for the first half of fiscal year 2017 and topics of each business, mainly Shopping Complex Business. Page 2 shows a summary. Let me begin with consolidated

PRESS RELEASE Financial Results. Rising passenger traffic at 12.5m Exceeding 1bn in consolidated revenue

PRESS RELEASE 2016 Financial Results Rising passenger traffic at 12.5m Exceeding 1bn in consolidated revenue Kifissia, 23 March 2017 AEGEAN reports full year 2016 results with consolidated revenue at 1,020m,

PRESS RELEASE 2016 Financial Results Rising passenger traffic at 12.5m Exceeding 1bn in consolidated revenue Kifissia, 23 March 2017 AEGEAN reports full year 2016 results with consolidated revenue at 1,020m,

48 Oct-15. Nov-15. Travel is expected to grow over the coming 6 months; at a slower rate

Analysis provided by TRAVEL TRENDS INDE OCTOBER 2016 CTI shows travel grew in October 2016. LTI predicts easing travel growth through the first four months of 2017, with some momentum sustained by domestic

Analysis provided by TRAVEL TRENDS INDE OCTOBER 2016 CTI shows travel grew in October 2016. LTI predicts easing travel growth through the first four months of 2017, with some momentum sustained by domestic

The Economic Impact of Tourism in Buncombe County, North Carolina

The Economic Impact of Tourism in Buncombe County, North Carolina 2017 Analysis September 2018 Introduction and definitions This study measures the economic impact of tourism in Buncombe County, North

The Economic Impact of Tourism in Buncombe County, North Carolina 2017 Analysis September 2018 Introduction and definitions This study measures the economic impact of tourism in Buncombe County, North

Industry Update. ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL

Industry Update ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL U.S. & Canadian GDP 8% 6% 4% U.S.* Canada** Estimate by BEA as of 02/11/16 2% 0% -2% -4% -6% -8% -10% The U.S. economy

Industry Update ACI-NA Winter Board of Directors Meeting February 3, 2016 Orlando, FL U.S. & Canadian GDP 8% 6% 4% U.S.* Canada** Estimate by BEA as of 02/11/16 2% 0% -2% -4% -6% -8% -10% The U.S. economy

The Civil Aviation Sector as a Driver for Economic Growth in Egypt

The Civil Aviation Sector as a Driver for Economic Growth in Egypt EDSCA Conference Cairo, November 10, 2013 Agenda 1. Facts and figures 2. Socio-economic impact of the civil aviation sector 3. Options

The Civil Aviation Sector as a Driver for Economic Growth in Egypt EDSCA Conference Cairo, November 10, 2013 Agenda 1. Facts and figures 2. Socio-economic impact of the civil aviation sector 3. Options

UNITED KINGDOM LEEDS OFFICES QUARTER

UNITED KINGDOM LEEDS OFFICES QUARTER 3 2018 2 528,654 SQ FT YTD INVESTMENT 335m 2018 Leeds city centre saw strong levels of demand in Q3 2018, with take-up at 191,464 sq ft. Similar levels of take-up were

UNITED KINGDOM LEEDS OFFICES QUARTER 3 2018 2 528,654 SQ FT YTD INVESTMENT 335m 2018 Leeds city centre saw strong levels of demand in Q3 2018, with take-up at 191,464 sq ft. Similar levels of take-up were

Online Case. Practice case. Slides HTS de préparation - fev 2016_rev HC.pptx Draft for discussion only

Copyright 2016 by The Boston Co onsulting Group, Inc. All rights reserved. Online Case Practice case Slides HTS de préparation - fev 2016_rev HC.pptx Draft for discussion only 0 INSTRUCTIONS (1/3) During

Copyright 2016 by The Boston Co onsulting Group, Inc. All rights reserved. Online Case Practice case Slides HTS de préparation - fev 2016_rev HC.pptx Draft for discussion only 0 INSTRUCTIONS (1/3) During

The challenge of competitiveness for the Greek Tourism Industry

The challenge of competitiveness for the Greek Tourism Industry George Drakopoulos Director General Deree Business Week Annual Forum, 18 th March 2010 About SETE SETE is a non-governmental, non-profit

The challenge of competitiveness for the Greek Tourism Industry George Drakopoulos Director General Deree Business Week Annual Forum, 18 th March 2010 About SETE SETE is a non-governmental, non-profit

The Economic Impact of Tourism Brighton & Hove Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism Brighton & Hove 2013 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

The Economic Impact of Tourism Brighton & Hove 2013 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

International economic context and regional impact

Contents I. GDP growth trends in Latin America and the Caribbean in 2012 II. Regional performance in 2012: Inflation, employment and wages External sector Policies: Fiscal and Monetary III. Conclusions

Contents I. GDP growth trends in Latin America and the Caribbean in 2012 II. Regional performance in 2012: Inflation, employment and wages External sector Policies: Fiscal and Monetary III. Conclusions

HIA-RP Data Residential Land Report

HIA-RP Data Residential Land Report March Qtr 29 Land s Back on the Rise The latest HIA-RP Data Residential Land Report highlights a rebound in raw land values following some moderation over 28. Median

HIA-RP Data Residential Land Report March Qtr 29 Land s Back on the Rise The latest HIA-RP Data Residential Land Report highlights a rebound in raw land values following some moderation over 28. Median

Belgrade City Report Q City Reports

Belgrade City Report Q2 2016 City Reports GDP Growth Q1 (y-o-y) Net Salary May Economy & Investment Economics 3.5% Inflation May y-o-y 0.7% 452 Unemployment Rate Q1 19% Retail Sales Index April y-o-y 7.4%

Belgrade City Report Q2 2016 City Reports GDP Growth Q1 (y-o-y) Net Salary May Economy & Investment Economics 3.5% Inflation May y-o-y 0.7% 452 Unemployment Rate Q1 19% Retail Sales Index April y-o-y 7.4%

TUI GROUP INVESTOR PRESENTATION

TUI GROUP INVESTOR PRESENTATION German Investment Conference UniCredit / Kepler Munich, 26-27 September 2012 Future-related statements This presentation contains a number of statements related to the future

TUI GROUP INVESTOR PRESENTATION German Investment Conference UniCredit / Kepler Munich, 26-27 September 2012 Future-related statements This presentation contains a number of statements related to the future

The Economic Impact of Tourism in Hillsborough County. July 2017

The Economic Impact of Tourism in Hillsborough County July 2017 Table of contents 1) Key Findings for 2016 3 2) Local Tourism Trends 7 3) Trends in Visits and Spending 12 4) The Domestic Market 19 5) The

The Economic Impact of Tourism in Hillsborough County July 2017 Table of contents 1) Key Findings for 2016 3 2) Local Tourism Trends 7 3) Trends in Visits and Spending 12 4) The Domestic Market 19 5) The

Tourist Traffic in the City of Rijeka For the Period Between 2004 and 2014

Tourist Traffic in the City of Rijeka For the Period Between 2004 and 2014 Rijeka, February 2015. Table of Contents Pg No. 1. Introduction 3 2. Physical indicators on an annual level 4 2.1. Structure and

Tourist Traffic in the City of Rijeka For the Period Between 2004 and 2014 Rijeka, February 2015. Table of Contents Pg No. 1. Introduction 3 2. Physical indicators on an annual level 4 2.1. Structure and

The Economic Impact of Tourism on Galveston Island, Texas

The Economic Impact of Tourism on Galveston Island, Texas 2017 Analysis Prepared for: Headline Results Headline results Tourism is an integral part of the Galveston Island economy and continues to be a

The Economic Impact of Tourism on Galveston Island, Texas 2017 Analysis Prepared for: Headline Results Headline results Tourism is an integral part of the Galveston Island economy and continues to be a

Economic impact of the Athens International Airport

FOUNDATION FOR ECONOMIC & INDUSTRIAL RESEARCH 11 T. Karatassou St, 11742 Athens, Greece, Tel: (+30) 210 9211 200-10, Fax: (+30) 210 9233 977, www.iobe.gr Economic impact of the Athens International Airport

FOUNDATION FOR ECONOMIC & INDUSTRIAL RESEARCH 11 T. Karatassou St, 11742 Athens, Greece, Tel: (+30) 210 9211 200-10, Fax: (+30) 210 9233 977, www.iobe.gr Economic impact of the Athens International Airport

Former Yugoslav Republic of Macedonia (FYROM)

") Former Yugoslav Republic of Macedonia (FYROM) Tourism in the economy Tourism directly contributed MKD 6.4 billion or 1.3% of GDP in 2013, and accounted for 3.3% of total employment. Estimates for 2014

Former Yugoslav Republic of Macedonia (FYROM) Tourism in the economy Tourism directly contributed MKD 6.4 billion or 1.3% of GDP in 2013, and accounted for 3.3% of total employment. Estimates for 2014

Flughafen Wien Group Maintains Upward Trend: Passenger Growth and Strong Earnings Improvement in the First Nine Months of 2016

Flughafen Wien Group Maintains Upward Trend: Passenger Growth and Strong Earnings Improvement in the First Nine Months of 2016 REVENUE increase to 545.4 million (+10.2%), EBITDA rise to 306.5 million (+13.1%

Flughafen Wien Group Maintains Upward Trend: Passenger Growth and Strong Earnings Improvement in the First Nine Months of 2016 REVENUE increase to 545.4 million (+10.2%), EBITDA rise to 306.5 million (+13.1%

GOING PLACES MACARTHURCOOK OFFICE PROPERTY TRUST

GOING PLACES MACARTHURCOOK OFFICE PROPERTY TRUST ANNUAL REPORT 2006 1 2 3 4 1 2 181 Miller Street, North Sydney, NSW 150 170 Leichhardt Street, Spring Hill, Brisbane, QLD 3 4 38 Akuna Street, Canberra,

GOING PLACES MACARTHURCOOK OFFICE PROPERTY TRUST ANNUAL REPORT 2006 1 2 3 4 1 2 181 Miller Street, North Sydney, NSW 150 170 Leichhardt Street, Spring Hill, Brisbane, QLD 3 4 38 Akuna Street, Canberra,

Quarterly Aviation Industry Performance

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance (March - June 17) Prepared by: Strategic Planning department 1 Quarterly

Quarterly Aviation Industry Performance ALAFCO Aviation Lease and Finance Company K.S.C.P. Quarterly Aviation Industry Performance (March - June 17) Prepared by: Strategic Planning department 1 Quarterly

How does my local economy function? What would the economic consequences of a project or action be?

June 5th,2012 Client: City of Cortez Shane Hale Report Prepared for SBDC Ft. Lewis Report Prepared by Donna K. Graves Information Services Executive Summary - At the request of Joe Keck at the Small Business

June 5th,2012 Client: City of Cortez Shane Hale Report Prepared for SBDC Ft. Lewis Report Prepared by Donna K. Graves Information Services Executive Summary - At the request of Joe Keck at the Small Business

RESEARCH INDUSTRIAL SNAPSHOT

RESEARCH INDUSTRIAL SNAPSHOT GREATER LONDON AND WESTERN HOME COUNTIES H1 2017 GREATER LONDON & WESTERN HOME COUNTIES LOGISTICS & INDUSTRIAL RESEARCH Introduction Our report provides an insight into the

RESEARCH INDUSTRIAL SNAPSHOT GREATER LONDON AND WESTERN HOME COUNTIES H1 2017 GREATER LONDON & WESTERN HOME COUNTIES LOGISTICS & INDUSTRIAL RESEARCH Introduction Our report provides an insight into the

Queensland Economic Update

Queensland Economic Update Chamber of Commerce & Industry March 2018 cciq.com.au Queensland Economic Update: Summary National Accounts GDP expanded 2.3% during calendar year 2017. QLD state final demand

Queensland Economic Update Chamber of Commerce & Industry March 2018 cciq.com.au Queensland Economic Update: Summary National Accounts GDP expanded 2.3% during calendar year 2017. QLD state final demand

RETAIL MARKET REPORT RESEARCH Q Moscow HIGHLIGHTS

Q1 2018 RETAIL MARKET REPORT Moscow HIGHLIGHTS A slight increase of the new supply was recorded at the level of 18,700 sq m (GLA) at the Moscow retail real estate market in Q1 2018. The stable dynamics

Q1 2018 RETAIL MARKET REPORT Moscow HIGHLIGHTS A slight increase of the new supply was recorded at the level of 18,700 sq m (GLA) at the Moscow retail real estate market in Q1 2018. The stable dynamics

Hospitality Market Snapshot Nairobi & Its Suburbs. June 2016

Hospitality Market Snapshot Nairobi & Its Suburbs June 2016 Kenya Nairobi In this issue 3 Nairobi Economic Overview Current Room Supply & Outlook 3 4 4 4 5 CBD 6 Westlands & Surrounds & Surrounds 7 Upper

Hospitality Market Snapshot Nairobi & Its Suburbs June 2016 Kenya Nairobi In this issue 3 Nairobi Economic Overview Current Room Supply & Outlook 3 4 4 4 5 CBD 6 Westlands & Surrounds & Surrounds 7 Upper

Location Report. Coffs Harbour U Retire ( ) Retire with Property

Retire with Property") Location Report Coffs Harbour Retire with Property 1300 U Retire (873 847) www.superannuationproperty.com Coffs Harbour Location Coffs Harbour is a regional town on the North Coast of New South Wales

Location Report Coffs Harbour Retire with Property 1300 U Retire (873 847) www.superannuationproperty.com Coffs Harbour Location Coffs Harbour is a regional town on the North Coast of New South Wales

CONTACT 2 Golgotha Str. Oasi Varipetrou GR Chania, GREECE Tel.: , Fax: Web:

CONTACT 2 Golgotha Str. Oasi Varipetrou GR 73100 Chania, GREECE Tel.: +302821029300, Fax: +302821029250 E-mail: oakae@oakae.gr Web: www.oakae.gr THE ORGANIZATION FOR THE DEVELOPMENT OF CRETE SA Founded

CONTACT 2 Golgotha Str. Oasi Varipetrou GR 73100 Chania, GREECE Tel.: +302821029300, Fax: +302821029250 E-mail: oakae@oakae.gr Web: www.oakae.gr THE ORGANIZATION FOR THE DEVELOPMENT OF CRETE SA Founded

SHIP MANAGEMENT SURVEY. July December 2017

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

The Economic Impact of Tourism Brighton & Hove Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism Brighton & Hove 2014 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

The Economic Impact of Tourism Brighton & Hove 2014 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

Australian Property Growth Fund

Australian Property Growth Fund Presentation Overview 2006/07 Key Highlights Property Trust Assets Funds Management & Development Company Projects Future Projects 2006/07 Key Highlights Profit after tax

Australian Property Growth Fund Presentation Overview 2006/07 Key Highlights Property Trust Assets Funds Management & Development Company Projects Future Projects 2006/07 Key Highlights Profit after tax

ANA HOLDINGS Financial Results for the Six Months Ended September 30, 2018

ANA HOLDINGS NEWS ANA HOLDINGS Financial Results for the Six Months Ended September 30, 2018 TOKYO, Nov. 2, 2018 ANA HOLDINGS INC. (hereinafter ANA HD ) today reports its financial results for the six

ANA HOLDINGS NEWS ANA HOLDINGS Financial Results for the Six Months Ended September 30, 2018 TOKYO, Nov. 2, 2018 ANA HOLDINGS INC. (hereinafter ANA HD ) today reports its financial results for the six

Economic Impact of Tourism in Hillsborough County September 2016

Economic Impact of Tourism in Hillsborough County - 2015 September 2016 Key findings for 2015 Almost 22 million people visited Hillsborough County in 2015. Visits to Hillsborough County increased 4.5%

Economic Impact of Tourism in Hillsborough County - 2015 September 2016 Key findings for 2015 Almost 22 million people visited Hillsborough County in 2015. Visits to Hillsborough County increased 4.5%

Tourism Barometer Snapshot Expectations of the Greek Hospitality Sector

Tourism Barometer Snapshot 2016 Expectations of the Greek Hospitality Sector January 2016 The analysis per hotel category shows that the 5 star hoteliers are the most optimistic as a vast majority is expecting

Tourism Barometer Snapshot 2016 Expectations of the Greek Hospitality Sector January 2016 The analysis per hotel category shows that the 5 star hoteliers are the most optimistic as a vast majority is expecting

El Al Israel Airlines announced today its financial results for the year 2016 and the fourth quarter of the year:

El Al Israel Airlines announced today its financial results for the year 2016 and the fourth quarter of the year: The Company's revenues in 2016 amounted to approx. USD 2,038 million, compared to approx.

El Al Israel Airlines announced today its financial results for the year 2016 and the fourth quarter of the year: The Company's revenues in 2016 amounted to approx. USD 2,038 million, compared to approx.

NEWSLETTER MARINA, HIGHWAY PRIVATIZATIONS

GREECE CONFIDENCE RETURNS MARINA, HIGHWAY PRIVATIZATIONS CALLING ON AUSTRALIAN INVESTORS The newsletter is a monthly publication of Enterprise Greece, the national trade and investment promotion agency.

GREECE CONFIDENCE RETURNS MARINA, HIGHWAY PRIVATIZATIONS CALLING ON AUSTRALIAN INVESTORS The newsletter is a monthly publication of Enterprise Greece, the national trade and investment promotion agency.

Estonia. Tourism in the economy. Tourism governance and funding

Estonia Tourism in the economy Tourism contributes directly around 4.6% of Estonia s GDP, rising to 6.6% if indirect impacts are also included. Export revenues from tourism amount to approximately EUR

Estonia Tourism in the economy Tourism contributes directly around 4.6% of Estonia s GDP, rising to 6.6% if indirect impacts are also included. Export revenues from tourism amount to approximately EUR

by Dr. Valia Kasimati Bank of Greece

by Dr. Valia Kasimati Bank of Greece ATINER s Public Lectures Series : Foreign Direct Investment Aim of the research A brief picture of the Greek Tourist Sector - General characteristics - Arrivals of

by Dr. Valia Kasimati Bank of Greece ATINER s Public Lectures Series : Foreign Direct Investment Aim of the research A brief picture of the Greek Tourist Sector - General characteristics - Arrivals of

1

213 Economic Outlook December 1, 212 Dr. Stephen P. A. Brown, Director Prepared by The Lee Lee Business School University of Nevada, Las Vegas University of Nevada, Las Vegas May 3, 212 December 1, 212

213 Economic Outlook December 1, 212 Dr. Stephen P. A. Brown, Director Prepared by The Lee Lee Business School University of Nevada, Las Vegas University of Nevada, Las Vegas May 3, 212 December 1, 212

4.5% 2.5% 2.3% Inflation. Purchasing power per capita 2016 Prague

City Report Q4 2017 4.5% 2.5% 2.3% GDP Growth F2017 Inflation December 2017 Unemployment rate December 2017 Prague 1,444 10,526 2.7% Average Monthly Salary Q3 2017 Prague Purchasing power per capita 2016

City Report Q4 2017 4.5% 2.5% 2.3% GDP Growth F2017 Inflation December 2017 Unemployment rate December 2017 Prague 1,444 10,526 2.7% Average Monthly Salary Q3 2017 Prague Purchasing power per capita 2016

Egypt. Tourism in the economy. Tourism governance and funding. Ref. Ares(2016) /06/2016

/06/2016") Ref. Ares(2016)3120133-30/06/2016 II. PARTNER COUNTRY PROFILES EGYPT Egypt Tourism in the economy International visitor arrivals to Egypt reached 9.9 million in 2014, generating a total of USD 7.2 billion

Ref. Ares(2016)3120133-30/06/2016 II. PARTNER COUNTRY PROFILES EGYPT Egypt Tourism in the economy International visitor arrivals to Egypt reached 9.9 million in 2014, generating a total of USD 7.2 billion

Travel and Tourism in Denmark to 2017

Travel and Tourism in Denmark to 2017 Growing Business Tourism and Promotional Activities by the Danish Tourist Board to Drive Tourism in Denmark Report Code: TT00103MR Publication Date: August 2013 www.timetric.com

Travel and Tourism in Denmark to 2017 Growing Business Tourism and Promotional Activities by the Danish Tourist Board to Drive Tourism in Denmark Report Code: TT00103MR Publication Date: August 2013 www.timetric.com

1.0% 3.6% 15.9% Inflation March 2017 y-o-y. Retail Sales,

City Report Q1 2017 1.0% 3.6% 15.9% GDP Growth Q1 2017 Inflation March 2017 y-o-y Unemployment rate 2016, Belgrade 495 11.4% 0.9% Salary March 2017, Belgrade Retail Sales, March 2017 y-o-y, Serbia Industrial

City Report Q1 2017 1.0% 3.6% 15.9% GDP Growth Q1 2017 Inflation March 2017 y-o-y Unemployment rate 2016, Belgrade 495 11.4% 0.9% Salary March 2017, Belgrade Retail Sales, March 2017 y-o-y, Serbia Industrial

Flughafen Wien Group Continues on Success Path in the First Quarter of 2016

Flughafen Wien Group Continues on Success Path in the First Quarter of 2016 Upward revaluation of stake in Malta Airport and good business development lead to strong increase in the net profit for the

Flughafen Wien Group Continues on Success Path in the First Quarter of 2016 Upward revaluation of stake in Malta Airport and good business development lead to strong increase in the net profit for the

Oct-17 Nov-17. Sep-17. Travel is expected to grow over the coming 6 months; at a slightly faster rate

Analysis provided by TRAVEL TRENDS INDEX SEPTEMBER 2018 CTI reading of.8 in September 2018 indicates that travel to or within the U.S. grew 1.6% in September 2018 compared to September 2017. LTI predicts

Analysis provided by TRAVEL TRENDS INDEX SEPTEMBER 2018 CTI reading of.8 in September 2018 indicates that travel to or within the U.S. grew 1.6% in September 2018 compared to September 2017. LTI predicts

III. TRADE IN COMMERCIAL SERVICES BY CATEGORY

.. TRADE IN COMMERCIAL SERVICES BY CATEGORY Transportation services China records impressive growth Exports of world transportation services reached $750 billion in 2007, an increase of 19 per cent, following

.. TRADE IN COMMERCIAL SERVICES BY CATEGORY Transportation services China records impressive growth Exports of world transportation services reached $750 billion in 2007, an increase of 19 per cent, following

Residential Property Price Index

An Phríomh-Oifig Staidrimh Central Statistics Office 24 January 2012 Residential Property Price Index Residential Property Price Index December 2011 Dec 05 Dec 06 Dec 07 Dec 08 National Dec 09 Dec 10 Excluding

An Phríomh-Oifig Staidrimh Central Statistics Office 24 January 2012 Residential Property Price Index Residential Property Price Index December 2011 Dec 05 Dec 06 Dec 07 Dec 08 National Dec 09 Dec 10 Excluding

Economic Climate Index - Latin America

Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

From: OECD Tourism Trends and Policies Access the complete publication at:

From: OECD Tourism Trends and Policies 2014 Access the complete publication at: http://dx.doi.org/10.1787/tour-2014-en Netherlands Please cite this chapter as: OECD (2014), Netherlands, in OECD Tourism

From: OECD Tourism Trends and Policies 2014 Access the complete publication at: http://dx.doi.org/10.1787/tour-2014-en Netherlands Please cite this chapter as: OECD (2014), Netherlands, in OECD Tourism

The Australian Property Institute Inc. Australian Property Directions Survey

The Australian Property Institute Inc. Australian Property Directions Survey SEPTEBER 2012 T his is the 29th API Australian Property Directions Survey conducted by the Australian Property Institute (NSW

The Australian Property Institute Inc. Australian Property Directions Survey SEPTEBER 2012 T his is the 29th API Australian Property Directions Survey conducted by the Australian Property Institute (NSW

Iceland. Tourism in the economy. Tourism governance and funding

Iceland Tourism in the economy Tourism has been among the fastest-growing industries in Iceland in recent years and has established itself as the third pillar of the Icelandic economy. Domestic demand

Iceland Tourism in the economy Tourism has been among the fastest-growing industries in Iceland in recent years and has established itself as the third pillar of the Icelandic economy. Domestic demand

MARKETBEAT. Queenstown Regional. Residential

Winter 2016 MARKETBEAT RESEARCH NEWSLETTER Queenstown Regional Queenstown is booming. A surging tourism sector drawing in more workers, coupled with an increasing wave of lifestylers and rising investor

Winter 2016 MARKETBEAT RESEARCH NEWSLETTER Queenstown Regional Queenstown is booming. A surging tourism sector drawing in more workers, coupled with an increasing wave of lifestylers and rising investor

Who goes where? How long do they stay? How much do they spend?

Who goes where? How long do they stay? How much do they spend? Analysis of inbound tourism by Region and Market Summary Evangelia Lamprou Researcher - Statistician Dr. Aris Ikkos, ISHC Research Director

Who goes where? How long do they stay? How much do they spend? Analysis of inbound tourism by Region and Market Summary Evangelia Lamprou Researcher - Statistician Dr. Aris Ikkos, ISHC Research Director

Moseley Gardens. surrendeninvest. Birmingham. residential. Exclusive to Surrenden Invest

surrendeninvest residential Moseley Gardens Birmingham Exclusive to Surrenden Invest Surrenden Invest the home of your portfolio Surrenden Invest unlock exclusive off market stock in high demand growth

surrendeninvest residential Moseley Gardens Birmingham Exclusive to Surrenden Invest Surrenden Invest the home of your portfolio Surrenden Invest unlock exclusive off market stock in high demand growth

Sofia City Report H City Reports

Sofia City Report H1 2016 City Reports Gross Salary Q1 Economy & Investment GDP growth Q1 y-o-y 2.9% 650 Inflation May y-o-y - 2.0% Unemployment Rate Q1 8.6% Source: National Statistical Institute of Republic

Sofia City Report H1 2016 City Reports Gross Salary Q1 Economy & Investment GDP growth Q1 y-o-y 2.9% 650 Inflation May y-o-y - 2.0% Unemployment Rate Q1 8.6% Source: National Statistical Institute of Republic

2011 Hotel investment strategy :

2011 Hotel investment strategy : What every developer should know New World Hotel 27 Sept, 2011 Presented by: Robert McIntosh, Executive Director, CBRE Hotels, Asia Pacific. SUMMARY Hotel Performance Hotel

2011 Hotel investment strategy : What every developer should know New World Hotel 27 Sept, 2011 Presented by: Robert McIntosh, Executive Director, CBRE Hotels, Asia Pacific. SUMMARY Hotel Performance Hotel

Acceleration of tourism

Belgrade 217 Tourism & Hotel Outlook Regulated by RICS Tourism & Hotel Market Outlook 217 LeRoy Realty Consultants 1 The growth of travel & tourism industry considerably outperforms that of the local economy

Belgrade 217 Tourism & Hotel Outlook Regulated by RICS Tourism & Hotel Market Outlook 217 LeRoy Realty Consultants 1 The growth of travel & tourism industry considerably outperforms that of the local economy

PRESS RELEASE SURVEY ON QUALITATIVE CHARACTERISTICS OF RESIDENT TOURISTS: 2016 (provisional data)

") Thousands HELLENIC REPUBLIC HELLENIC STATISTICAL AUTHORITY Piraeus, 8 September 217 PRESS RELEASE SURVEY ON QUALITATIVE CHARACTERISTICS OF RESIDENT TOURISTS: 216 (provisional data) The Hellenic Statistical

Thousands HELLENIC REPUBLIC HELLENIC STATISTICAL AUTHORITY Piraeus, 8 September 217 PRESS RELEASE SURVEY ON QUALITATIVE CHARACTERISTICS OF RESIDENT TOURISTS: 216 (provisional data) The Hellenic Statistical