Ship operating costs: Current and future trends

|

|

|

- Agnes Ryan

- 6 years ago

- Views:

Transcription

1 Ship operating costs: Current and future trends International Maritime Statistics Forum Richard Greiner, Moore Stephens LLP April 2013 Shipping PRECISE. PROVEN. PERFORMANCE.

2 Introduction Richard Greiner is a partner in the shipping industry group and has more than 30 years experience in providing assurance and advisory services to the shipping industry. He is a regular speaker at shipping and ship finance conferences and seminars and has written articles and papers on shipping finance and accounts. Richard leads the Moore Stephens ship operating costs benchmarking report, OpCost. richard.greiner@moorestephens.com

3 Overview Introduction to OpCost OpCost 2012 results Future cost trends

4

5 OpCost features Vessel operating cost benchmarking tool 26 vessel types: Including 5 Bulker, 12 Tanker and 3 Container ship types 12 cost categories: Including crew costs, stores, repairs & maintenance and insurance as well as dry-docking Over 2,700 vessels in OpCost 2012 database Exclusive to Moore Stephens

6 Benefits Assistance in improving cost control Backup figures in business plans Analysis of costs in new sectors and other ship types Helps to manage (and reduce) vessel operating costs

7 OpCost 2012 results OpCost indices (by sector) Proportional distribution of costs Daily running cost rates (by vessel type) Analysis of: Crew costs Stores Repairs and maintenance Insurance Drydock

8 OpCost indices Index points Year Bulker Tanker Container Source: Moore Stephens OpCost 2012

9 Operating cost trends Bulker Year OpCost index Change (%) year average 5.5% Source: Moore Stephens OpCost 2012

10 Operating cost trends Tanker Year OpCost index Change (%) year average 5.9% Source: Moore Stephens OpCost 2012

11 Operating cost trends Container ship Year OpCost index Change (%) year average 6.1% Source: Moore Stephens OpCost 2012

12 Proportional distribution Bulker Source: Moore Stephens OpCost 2012

13 Proportional distribution Tanker Source: Moore Stephens OpCost 2012

14 Total operating costs 2011:2010 Source: Moore Stephens OpCost 2012

15 Operating costs Bulker OpCost 2012 Daily Rate US$ Year on year change (%) Handysize 5, Handymax 6, Panamax* 6, Capesize* 7, Weighted average 1.7% * Daily rate for 2010, as previously reported, was adjusted to reflect this year s change in the Panamax and Capesize sizes. Source: Moore Stephens OpCost 2012

16 Operating costs Tanker OpCost 2012 Daily Rate US$ Year on year change (%) Product 8, Handysize Product 7, Panamax 8, Aframax 8, Suezmax 9, VLCC 10, Weighted average 1.7% Source: Moore Stephens OpCost 2012

17 Operating costs Container ship OpCost 2012 Daily Rate US$ Year on year change (%) Feedermax (100-1,000 TEU) 4, Container Ship (1,000-2,000 TEU) 5, Main Liner (2,000-6,000 TEU) 7, Weighted average 3.1% Source: Moore Stephens OpCost 2012

18 OpCost crew costs indices Crew wages, provisions and crew other 2.2% Index points % 3.4% Year Source: Moore Stephens OpCost 2012

19 OpCost stores indices Lubricants and stores other 200 Index points % 2.3% 3.5% Year Source: Moore Stephens OpCost 2012

20 OpCost repairs & maintenance indices Spares and other repairs & maintenance 170 Index points % 3.7% 0.8% Year Source: Moore Stephens OpCost 2012

21 OpCost insurance indices P&I and H&M 200 Index points % -3.4% 1.1% Year Source: Moore Stephens OpCost 2012

22 Drydock costs and duration Source: Moore Stephens OpCost 2012

23 OpCost 2012: A summary OpCost 2012 annual change (%): Bulker 1.7 Tanker 1.7 Container ship 3.1 Annual average change (%): Bulker 5.5 Tanker 5.9 Container ship 6.1

24 OpCost 2013 To be published September 2013 Aiming for increased participation and more vessel types Ideas for new features welcome

25 Future operating cost survey Respondents Expected cost increases Influencing factors

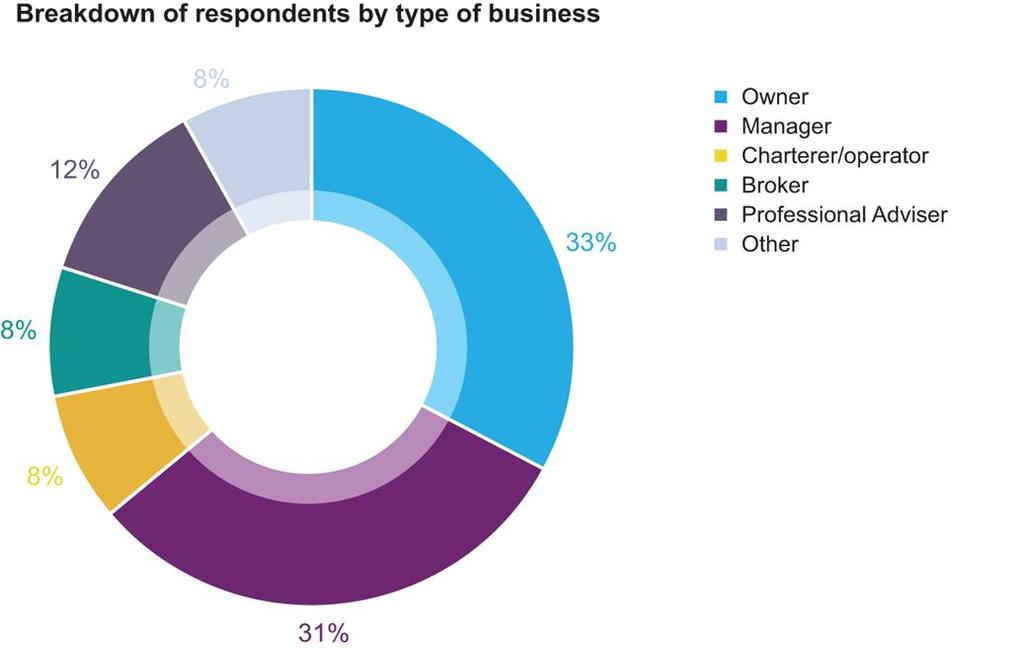

26 Respondents by type

27 Respondents by location

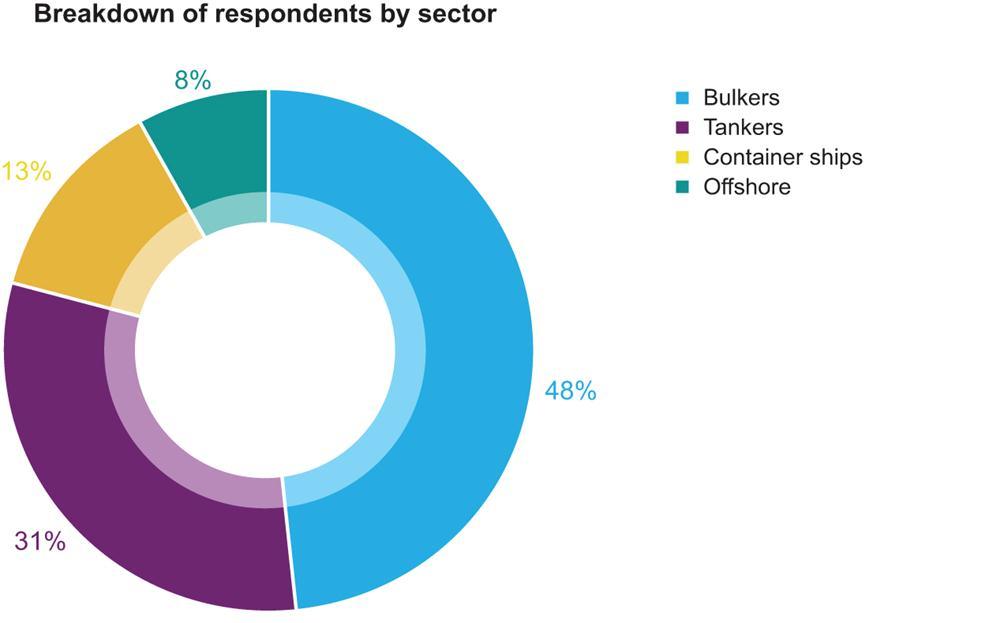

28 Respondents by sector

29 Expected cost increases Overall mean % % Source: Moore Stephens, 2012 Future operating costs survey

30 Expected increases by cost type Cost type mean Crew wages Other crew Lubricants Stores Spares R&M H&M P&I Management fees Drydock % 2.1% 2.9% 2.1% 2.2% 2.1% 1.9% 2.1% 1.3% 1.9% % 2.1% 2.8% 2.1% 2.2% 2.2% 2.0% 2.2% 1.4% 2.0% Source: Moore Stephens, 2012 Future operating costs survey

31 Factors influencing operating costs Finance costs 27% Crew Supply 20% Competition 18% Demand Trends 17% Labour costs 9% Raw Material Costs 7% Other 2% 0% 5% 10% 15% 20% 25% 30% Source: Moore Stephens, 2012 Future operating costs survey

32 Ship operating costs: Current and future trends International Maritime Statistics Forum Richard Greiner, Moore Stephens LLP April 2013 Shipping PRECISE. PROVEN. PERFORMANCE.

Ship operating costs: Current and future trends

Ship operating costs: Current and future trends Richard Greiner, Moore Stephens LLP December 2017 Shipping PRECISE. PROVEN. PERFORMANCE. Overview Introduction to OpCost OpCost 2017 results Future cost

Ship operating costs: Current and future trends Richard Greiner, Moore Stephens LLP December 2017 Shipping PRECISE. PROVEN. PERFORMANCE. Overview Introduction to OpCost OpCost 2017 results Future cost

The World s Largest Buyer of Ships and Offshore Assets

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

The World s Largest Buyer of Ships and Offshore Assets 9 th Annual Marine Money London Ship Finance Forum, 24 January 218 Evan F. Sproviero, Head of Projects, GMS 1 A. Recycling Prices and Residual Values

GOLDEN DESTINY MONTHLY NEWBUILDING REPORT

ISSUE NO.04/2013 APRIL 2013 MONTHLY NEWBUILDING REPORT ORDERING ACTIVITY (per vessel type) by Greek and Foreign Owners GOLDEN DESTINY MONTHLY NEWBUILDING REPORT highlights the volume of transactions in

ISSUE NO.04/2013 APRIL 2013 MONTHLY NEWBUILDING REPORT ORDERING ACTIVITY (per vessel type) by Greek and Foreign Owners GOLDEN DESTINY MONTHLY NEWBUILDING REPORT highlights the volume of transactions in

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 1 st November 2013 (Week 44, Report No: 44/13) (Given in good faith but without guarantee)

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st July 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH JULY 217

MONTHLY MARKET OVERVIEW 1st 31st July 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH JULY 217

Long Term Trends in Shipbuilding HVB Press Conference. 20 th September 2006 Stephen Gordon, Clarkson Research

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

Long Term Trends in Shipbuilding HVB Press Conference 20 th September 2006 Stephen Gordon, Clarkson Research Introduction Background to Shipbuilding Investment The Current Orderbook The Product Mix Regional

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW August SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH AUGUST BULKERS

MONTHLY MARKET OVERVIEW August SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH AUGUST BULKERS

OFFSHORE MONTHLY MARKET OVERVIEW

OFFSHORE MONTHLY MARKET OVERVIEW 1 st 3 th November 17 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity +44 () 3 6 vesselsvalue.com OFFSHORE VALUES

OFFSHORE MONTHLY MARKET OVERVIEW 1 st 3 th November 17 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity +44 () 3 6 vesselsvalue.com OFFSHORE VALUES

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

«Να κάνουμε την κρίση ευκαιρία" Ανάλυση των αγορών Bulkers & Tankers Aδελφότης των Υδραίων Αθηνών 3ο Ναυτιλιακό Συνέδριο Σεπτέμβριος 2011 Section 1: Dry Bulkers Presentation Contents Dry Bulker fleet overview:

Dry Bulk Market Weekly Highlights Week 17 - Dry Cargo Market Highlights for the period of 21-April-2011 until 28-April-2011

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

Dry Bulk Market ly Highlights 17 - Dry Cargo Market Highlights for the period of 21-April-211 until 28-April-211 17 28/4/211 Baltic Indices / Dry Bulk Spot Rates 16 21/4/211 ±% $/day $/day Point Diff 211

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

MONTHLY MARKET OVERVIEW 1 st 31 st August 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH AUGUST 217

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 15 th November 2013 (Week 46, Report No: 46/13) (Given in good faith but without guarantee)

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st March 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MARCH 217

MONTHLY MARKET OVERVIEW 1st 31st March 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MARCH 217

18th November 2013 GMS Ship Recycling Conference - Tokyo 1

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

18th November 2013 GMS Ship Recycling Conference - Tokyo 1 Agenda 1. Industry Facts 2. Ship recycling Boom and Corrections 3. Ship Recycling: Source of Recovery? 4. Changing Role of Cash Buyer 5. Closing

ECONOMIC CONSEQUENCES OF PIRACY AND ARMED ROBBERY ON SHIPPING

EUROPEAN COMMISSION SEMINAR PIRACY AND ARMED ROBBERY AGAINST SHIPPING BRUSSELS 21st JANUARY 2009 ECONOMIC CONSEQUENCES OF PIRACY AND ARMED ROBBERY ON SHIPPING Presentation by G. De Monie MSc. Senior Director

EUROPEAN COMMISSION SEMINAR PIRACY AND ARMED ROBBERY AGAINST SHIPPING BRUSSELS 21st JANUARY 2009 ECONOMIC CONSEQUENCES OF PIRACY AND ARMED ROBBERY ON SHIPPING Presentation by G. De Monie MSc. Senior Director

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 28 th February 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW 1 st 28 th February 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st July 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JULY 218

MONTHLY MARKET OVERVIEW 1 st 31 st July 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JULY 218

July 2018 RV PRODUCTION. Overview of towable and motorised recreational vehicles manufactured in Australia. Data Provided by nemaustralasia

y RV PRODUCTION Overview of towable and motorised recreational vehicles manufactured in Australia. Data Provided by nemaustralasia This research is undertaken in partnership between the National Association

y RV PRODUCTION Overview of towable and motorised recreational vehicles manufactured in Australia. Data Provided by nemaustralasia This research is undertaken in partnership between the National Association

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st October 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH OCTOBER

MONTHLY MARKET OVERVIEW 1 st 31 st October 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH OCTOBER

Tanker Market Outlook. 12th Mare Forum Ship Finance 2012 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 2012

Tanker Market Outlook 12th Mare Forum Ship Finance 212 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 212 Tanker Market Outlook 12th Mare Forum Ship Finance 212 Disclaimer The material and

Tanker Market Outlook 12th Mare Forum Ship Finance 212 Foteini Kanellopoulou, Senior Analyst Amsterdam, 31 October 212 Tanker Market Outlook 12th Mare Forum Ship Finance 212 Disclaimer The material and

S&P Market Trends during December: Secondhand Newbuilding Demolition

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 13 th December 2013 (Week 50, Report No: 50/13) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 13 th December 2013 (Week 50, Report No: 50/13) (Given in good faith but without guarantee)

ASL Marine Holdings Ltd.

ASL Marine Holdings Ltd. SHIPBUILDING SHIPREPAIR SHIPCHARTERING Pulse of Asia 2008 - Presentation 8 th July 2008 1 Presentation Outline Company Profile 9M FY2008 Financial Review Business Review - Shipbuilding

ASL Marine Holdings Ltd. SHIPBUILDING SHIPREPAIR SHIPCHARTERING Pulse of Asia 2008 - Presentation 8 th July 2008 1 Presentation Outline Company Profile 9M FY2008 Financial Review Business Review - Shipbuilding

The Economic Impact of Tourism Brighton & Hove Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism Brighton & Hove 2014 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

The Economic Impact of Tourism Brighton & Hove 2014 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

Who is the Biggest of the Clean?

Who is the Biggest of the Clean? In our January 9, 24 opinion report, The More Things Change The More They Stay the Same, we tracked the top charterers in the spot market for dirty cargoes. But the dirty

Who is the Biggest of the Clean? In our January 9, 24 opinion report, The More Things Change The More They Stay the Same, we tracked the top charterers in the spot market for dirty cargoes. But the dirty

SHIP MANAGEMENT SURVEY. July December 2017

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

SHIP MANAGEMENT SURVEY July December 2017 INTRODUCTION The Ship Management Survey is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates primarily on transactions between

Maritime Administration of Latvia Division for Investigation of Marine Accidents Summary of Marine accidents and incidents in 2010

Maritime Administration of Latvia Division for Investigation of Marine Accidents Summary of Marine accidents and incidents in 00 Division for Investigation of Marine Accidents of Maritime Administration

Maritime Administration of Latvia Division for Investigation of Marine Accidents Summary of Marine accidents and incidents in 00 Division for Investigation of Marine Accidents of Maritime Administration

Ship Scrapping - Market Pressures. IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 2012

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

Ship Scrapping - Market Pressures IMSF Oslo Foteini Kanellopoulou, Senior Analyst 23 May 212 Disclaimer The material and the information contained herein (together, the "Information") are provided by H.

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st May 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH MAY 217 BULKERS

MONTHLY MARKET OVERVIEW 1st 31st May 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH MAY 217 BULKERS

The Economic Impact of Tourism Brighton & Hove Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism Brighton & Hove 2013 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

The Economic Impact of Tourism Brighton & Hove 2013 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 1.1 Introduction 1 1.2

South Australian Tourism Industry Council SA Tourism Barometer March Quarter 2015

South Australian Tourism Industry Council SA Tourism Barometer March Quarter 2015 Headline: Events Season Provides a Lift In the March quarter 2015 survey the business activity index increased by 6% -

South Australian Tourism Industry Council SA Tourism Barometer March Quarter 2015 Headline: Events Season Provides a Lift In the March quarter 2015 survey the business activity index increased by 6% -

Monday, September 6, Week 36 The Week at a Glance

Monday, September 6, 21 - Week 36 The Week at a Glance "Lesson learned? Guess not." Baltic Dry Indices* Last Fridays Closing Weekly Difference Baltic Dry Index 2876 164 Baltic Cape index 3937 488 Baltic

Monday, September 6, 21 - Week 36 The Week at a Glance "Lesson learned? Guess not." Baltic Dry Indices* Last Fridays Closing Weekly Difference Baltic Dry Index 2876 164 Baltic Cape index 3937 488 Baltic

Innovative Shipyard Solutions

Innovative Shipyard Solutions 8 th Annual Capital Link Operational Excellence in Shipping Forum Athens, Greece 30 October 2018 S Content Who We Are: Introduction Newport Execution Organisation Chart Central

Innovative Shipyard Solutions 8 th Annual Capital Link Operational Excellence in Shipping Forum Athens, Greece 30 October 2018 S Content Who We Are: Introduction Newport Execution Organisation Chart Central

Monday, August 30, Week 35 The Week at a Glance

Monday, August 3, 21 - Week 35 The Week at a Glance Hunting Season? Vacations season is almost over and decision makers are getting back in to their usual schedules. Let s see whether September will be

Monday, August 3, 21 - Week 35 The Week at a Glance Hunting Season? Vacations season is almost over and decision makers are getting back in to their usual schedules. Let s see whether September will be

Golden Ocean Group Limited Q results March 1, 2007

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

Golden Ocean Group Limited Q4 2006 results March 1, 2007 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 Oct-Dec Oct-Dec Jan - Dec Jan - Dec Operating Revenues 37 292 91 253 Time charter revenues

MONTHLY NEW BUILDING REPORT

MONTHLY NEW BUILDING REPORT February 2006 Newbuilding Prices Chart $140,00 $120,00 $100,00 $80,00 $60,00 $40,00 $20,00 $0,00 8/1/04 9/1/04 10/1/04 11/1/04 12/1/04 1/1/05 2/1/05 3/1/05 4/1/05 5/1/05 6/1/05

MONTHLY NEW BUILDING REPORT February 2006 Newbuilding Prices Chart $140,00 $120,00 $100,00 $80,00 $60,00 $40,00 $20,00 $0,00 8/1/04 9/1/04 10/1/04 11/1/04 12/1/04 1/1/05 2/1/05 3/1/05 4/1/05 5/1/05 6/1/05

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

This Week s Overview of Shipping Investments SECONDHAND / DEMOLITION / NEW BUILDING MARKET ANALYSIS Week Ending: 8 th November 2013 (Week 45, Report No: 4513) (Given in good faith but without guarantee)

The Economic Impact of Tourism New Forest Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism New Forest 2008 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS Glossary of terms 1 1. Summary of Results 4 2. Table

The Economic Impact of Tourism New Forest 2008 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS Glossary of terms 1 1. Summary of Results 4 2. Table

SHIP MANAGEMENT SURVEY. January June 2018

CENTRAL BANK OF CYPRUS EUROSYSTEM SHIP MANAGEMENT SURVEY January June 2018 INTRODUCTION The Ship Management Survey (SMS) is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates

CENTRAL BANK OF CYPRUS EUROSYSTEM SHIP MANAGEMENT SURVEY January June 2018 INTRODUCTION The Ship Management Survey (SMS) is conducted by the Statistics Department of the Central Bank of Cyprus and concentrates

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 3th November 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH NOVEMBER

MONTHLY MARKET OVERVIEW 1st 3th November 217 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH NOVEMBER

WEEKLY MARKET REPORT October 17th, 2008 / Week 42

LY MARKET REPORT October 17th, 28 / Week 42 With all the indices in the red for the entire week and with the BDI down to levels last seen early in November 22 there is certainly no change in the mood for

LY MARKET REPORT October 17th, 28 / Week 42 With all the indices in the red for the entire week and with the BDI down to levels last seen early in November 22 there is certainly no change in the mood for

SHIP MANAGEMENT SURVEY* July December 2015

SHIP MANAGEMENT SURVEY* July December 2015 1. SHIP MANAGEMENT REVENUES FROM NON- RESIDENTS Ship management revenues dropped marginally to 462 million, following a decline in global shipping markets. Germany

SHIP MANAGEMENT SURVEY* July December 2015 1. SHIP MANAGEMENT REVENUES FROM NON- RESIDENTS Ship management revenues dropped marginally to 462 million, following a decline in global shipping markets. Germany

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st August 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH AUGUST

MONTHLY MARKET OVERVIEW 1st 31st August 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH AUGUST

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 3thApril 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH APRIL 217 BULKERS

MONTHLY MARKET OVERVIEW 1st 3thApril 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH APRIL 217 BULKERS

Monday, July 25, Week 30 The Week at a Glance

Baltic Dry Indices* Last Fridays Closing Weekly Difference Monday, July 25, 211 - Week 3 The Week at a Glance Butterfly effect..." Officials of the Euro-zone have come into agreement to assist Greece with

Baltic Dry Indices* Last Fridays Closing Weekly Difference Monday, July 25, 211 - Week 3 The Week at a Glance Butterfly effect..." Officials of the Euro-zone have come into agreement to assist Greece with

WEEKLY MARKET REPORT January 27th, 2012 / Week 4

WEEKLY MARKET REPORT January 27th, 2012 / Week 4 Whilst the capesize losses were just below 6% all other segments continue to suffer double digit losses with the panamaxes leading the way. The BPI lost

WEEKLY MARKET REPORT January 27th, 2012 / Week 4 Whilst the capesize losses were just below 6% all other segments continue to suffer double digit losses with the panamaxes leading the way. The BPI lost

CURRICULUM VITAE TONY GRAINGER Marine Engineer

Contact Details Address : 2 Herriot Way, Thirsk, North Yorkshire, YO7 1FL Home Telephone : +44 (0) 1845 524013 Mobile : +44 (0) 755 774 0222 E-mail : antonygrainger@hotmail.co.uk Nationality : British

Contact Details Address : 2 Herriot Way, Thirsk, North Yorkshire, YO7 1FL Home Telephone : +44 (0) 1845 524013 Mobile : +44 (0) 755 774 0222 E-mail : antonygrainger@hotmail.co.uk Nationality : British

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 31st May 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MAY

MONTHLY MARKET OVERVIEW 1st 31st May 218 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis info@ BULKER VALUES THROUGH MAY

Demand, Supply & Capacity in the Shipbuilding Industry

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

Demand, Supply & Capacity in the Shipbuilding Industry million dwt Ship completions by region 120 100 80 60 Other Europe Japan Korea China "Europe" includes Russia SOURCE: IHS-Fairplay 40 20 42.3 0 0.4

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 31 st January 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW 1 st 31 st January 219 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 () 23 26 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1 st 30 th November 2018 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 (0) 203 026 5555 vesselsvalue.com

MONTHLY MARKET OVERVIEW 1 st 30 th November 2018 SUMMARY OF CONTENT Value analysis Total second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis +44 (0) 203 026 5555 vesselsvalue.com

Greek Shipping : Greece s steaming force

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

Greek Shipping : Greece s steaming force Dr. Nikolas P. Tsakos President & CEO 1 Tsakos Energy Navigation, Ltd A New York Stock Exchange Listed Company WORLD FLEET by the nationality of owner WORLD FLEET

WEEKLY MARKET REPORT September 30th, 2011 / Week 39

LY MARKET REPORT September 30th, 2011 / Week 39 The capesize market started to decline early in the week, dragging the general index with it. They both ended the week in the red with the BCI down nearly

LY MARKET REPORT September 30th, 2011 / Week 39 The capesize market started to decline early in the week, dragging the general index with it. They both ended the week in the red with the BCI down nearly

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 2th June, 211 Volume 362 Week 25 Sale & Purchase Activity Week 25 SECOND HAND SALES DRY TONNAGE Type

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 2th June, 211 Volume 362 Week 25 Sale & Purchase Activity Week 25 SECOND HAND SALES DRY TONNAGE Type

WEEKLY SHIPPING MARKET REPORT

WEEKLY SHIPPING MARKET REPORT WEEK 42 (10 rd October to 16 th October 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

WEEKLY SHIPPING MARKET REPORT WEEK 42 (10 rd October to 16 th October 2015) Legal Disclaimer The information contained herein has been obtained by various sources. Although every effort has been made to

MONTHLY MARKET OVERVIEW

MONTHLY MARKET OVERVIEW 1st 3th June 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JUNE 217 BULKERS

MONTHLY MARKET OVERVIEW 1st 3th June 217 SUMMARY OF CONTENT Value analysis Second hand S&P activity Newbuilding activity Demolition activity Charter rate analysis BULKER VALUES THROUGH JUNE 217 BULKERS

The Economic Impact of Tourism on the District of Thanet 2011

The Economic Impact of Tourism on the District of Thanet 2011 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 2. Table of

The Economic Impact of Tourism on the District of Thanet 2011 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 2. Table of

The Economic Impact of Tourism Eastbourne Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism Eastbourne 2016 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS Page 1. Summary of Results 1 1.1 Introduction 1 1.2

The Economic Impact of Tourism Eastbourne 2016 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS Page 1. Summary of Results 1 1.1 Introduction 1 1.2

WEEKLY MARKET REPORT June 6th, 2008 / Week 23

LY MARKET REPORT June 6th, 2008 / Week 23 This year's Posidonia was bigger than ever, proving one more time the importance of Greece and Piraeus in particular as one of the largest shipping centers in

LY MARKET REPORT June 6th, 2008 / Week 23 This year's Posidonia was bigger than ever, proving one more time the importance of Greece and Piraeus in particular as one of the largest shipping centers in

Monday, December 12, Week 50 The Week at a Glance

Baltic Dry Indices* Monday, December 12, 211 - Week 5 The Week at a Glance 'China to the rescue?' Last Fridays Closing Weekly Difference Baltic Dry Index 1922 56 Baltic Cape index 3697 288 Baltic Panamax

Baltic Dry Indices* Monday, December 12, 211 - Week 5 The Week at a Glance 'China to the rescue?' Last Fridays Closing Weekly Difference Baltic Dry Index 1922 56 Baltic Cape index 3697 288 Baltic Panamax

Petrofin Research Greek fleet statistics

Petrofin Research 2 nd part of Petrofin Research : Greek fleet statistics In this 2 nd part of Petrofin research, the Greek Fleet Statistics, we analyse the composition of the Greek fleet, in terms of

Petrofin Research 2 nd part of Petrofin Research : Greek fleet statistics In this 2 nd part of Petrofin research, the Greek Fleet Statistics, we analyse the composition of the Greek fleet, in terms of

WEEKLY MARKET REPORT December 12th, 2014 / Week 50

LY MARKET REPORT December 12th, 2014 / Week 50 The capesize index continued to fall heavily this week posting a loss of just over 40%, dragging the overall index to a weekly loss of just over 12%. The

LY MARKET REPORT December 12th, 2014 / Week 50 The capesize index continued to fall heavily this week posting a loss of just over 40%, dragging the overall index to a weekly loss of just over 12%. The

Unlocking Panama? Some thoughts on the impact of the Canal expansion on liner and bulk sea trade

Unlocking Panama? Some thoughts on the impact of the Canal expansion on liner and bulk sea trade Presentation to the Maritime Law Association annual conference 2 September 2017 Trevor Jones Director Unit

Unlocking Panama? Some thoughts on the impact of the Canal expansion on liner and bulk sea trade Presentation to the Maritime Law Association annual conference 2 September 2017 Trevor Jones Director Unit

ATHENIAN SHIPBROKERS S.A.

17-19, Vas. Pavlou Str., GR 166 73, Voula, Athens, Greece Tel: 21 96597 - Fax: 21 89964 - Tlx: 22626 ATH GR Internet Mail athenian@atheniansa.gr Monthly Report November 28 PRICES TANKERS ($ MIO) 24 25

17-19, Vas. Pavlou Str., GR 166 73, Voula, Athens, Greece Tel: 21 96597 - Fax: 21 89964 - Tlx: 22626 ATH GR Internet Mail athenian@atheniansa.gr Monthly Report November 28 PRICES TANKERS ($ MIO) 24 25

WEEKLY MARKET REPORT October 12th, 2012 / Week 41

LY MARKET REPORT October 12th, 212 / Week 41 A huge increase in the panamax market with the BPI gaining just over 45% for the week. Panamax charter rates increased significantly as fixing was strengthened

LY MARKET REPORT October 12th, 212 / Week 41 A huge increase in the panamax market with the BPI gaining just over 45% for the week. Panamax charter rates increased significantly as fixing was strengthened

WEEKLY MARKET REPORT February 18th, 2011 / Week 7

LY MARKET REPORT February 18th, 2011 / Week 7 The market remained positive for this week as well even though the BCI ended marginally lower. The winners this week were the BCI and BSI which marked an increase

LY MARKET REPORT February 18th, 2011 / Week 7 The market remained positive for this week as well even though the BCI ended marginally lower. The winners this week were the BCI and BSI which marked an increase

Zihni Shipping Agency S. A. Company Presentation

Zihni Shipping Agency S. A. Company Presentation S Zihni Shipping Agency S. A. Founded in 1930, Zihni Shipping Agency is the most experienced agent in Turkey. Our ISO 9001-2000 certified service quality

Zihni Shipping Agency S. A. Company Presentation S Zihni Shipping Agency S. A. Founded in 1930, Zihni Shipping Agency is the most experienced agent in Turkey. Our ISO 9001-2000 certified service quality

WEEKLY MARKET REPORT December 16th, 2011 / Week 50

LY MARKET REPORT December 16th, 211 / Week 5 The market saw a correction this week on weaker demand for the capesize sector. After a positive end on Monday both the BDI and BCI fell for the remainder of

LY MARKET REPORT December 16th, 211 / Week 5 The market saw a correction this week on weaker demand for the capesize sector. After a positive end on Monday both the BDI and BCI fell for the remainder of

The Economic Impact of Tourism on Calderdale Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH

The Economic Impact of Tourism on Calderdale 2015 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 2. Table of Results Table

The Economic Impact of Tourism on Calderdale 2015 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 2. Table of Results Table

NILIMAR Ships Sale & Purchase MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011.

MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011. Whilst world financial markets continue to concern, and the gold price continues to rise (being seen as

MARKET REPORT WEEK 34 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 26 th AUGUST 2011. Whilst world financial markets continue to concern, and the gold price continues to rise (being seen as

Construction Industry Focus Survey. Sample

Construction Industry Focus Survey 1 CONTENTS Executive Summary 1 1. Leading Activity Indicator 2 2. Activity by sector and constraints Residential, Non-residential, Civil Engineering 3. Orders and Tenders

Construction Industry Focus Survey 1 CONTENTS Executive Summary 1 1. Leading Activity Indicator 2 2. Activity by sector and constraints Residential, Non-residential, Civil Engineering 3. Orders and Tenders

WEEKLY MARKET REPORT January 9th, 2015 / Week 01

LY MARKET REPORT January 9th, 2015 / Week 01 WISHING YOU A HEALTHY, HAPPY AND PROSPEROUS 2015. Like the previous week, all of the indices were in the red throughout this week. The BCI suffered another

LY MARKET REPORT January 9th, 2015 / Week 01 WISHING YOU A HEALTHY, HAPPY AND PROSPEROUS 2015. Like the previous week, all of the indices were in the red throughout this week. The BCI suffered another

WEEKLY MARKET REPORT January 25th, 2008 / Week 4

WEEKLY MARKET REPORT January 25th, 2008 / Week 4 Few sales to report the dry and wet sectors this week as in both cases the market seems to be adjusting itself currently. ON THE DRY we have noted quite

WEEKLY MARKET REPORT January 25th, 2008 / Week 4 Few sales to report the dry and wet sectors this week as in both cases the market seems to be adjusting itself currently. ON THE DRY we have noted quite

WEEKLY MARKET REPORT July 16th, 2010 / Week 28

LY MARKET REPORT July 16th, 21 / Week 28 All indices have continued their downward trend for another week, as the capesize rates continued their downward spiral. Very poor demand for iron ore has put pressure

LY MARKET REPORT July 16th, 21 / Week 28 All indices have continued their downward trend for another week, as the capesize rates continued their downward spiral. Very poor demand for iron ore has put pressure

The Economic Impact of Tourism on Scarborough District 2014

The Economic Impact of Tourism on Scarborough District 2014 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 2. Table of

The Economic Impact of Tourism on Scarborough District 2014 Prepared by: Tourism South East Research Unit 40 Chamberlayne Road Eastleigh Hampshire SO50 5JH CONTENTS 1. Summary of Results 1 2. Table of

LATENCY OF TOURISM PERMITS IN THE GREAT BARRIER REEF MARINE PARK AUDIT FOR THE YEAR 2000

LATENCY OF TOURISM PERMITS IN THE GREAT BARRIER REEF MARINE PARK AUDIT FOR THE YEAR 2 Tourism and Recreation Group December 2 DISCLAIMER The information provided in this Audit is for information and discussion

LATENCY OF TOURISM PERMITS IN THE GREAT BARRIER REEF MARINE PARK AUDIT FOR THE YEAR 2 Tourism and Recreation Group December 2 DISCLAIMER The information provided in this Audit is for information and discussion

IN THIS ISSUE NO. 2, OCTOBER 2016

NO. 2, OCTOBER 2016 Welcome to the second issue of the Marine Information System (MIS) newsletter. Comments following the first issue, which was released in June, were very positive and clearly showed

NO. 2, OCTOBER 2016 Welcome to the second issue of the Marine Information System (MIS) newsletter. Comments following the first issue, which was released in June, were very positive and clearly showed

WEEKLY MARKET REPORT April 20th, 2012 / Week 16

WEEKLY MARKET REPORT April 2th, 212 / Week 16 For a second consecutive week the BDI continued to increase, ending the week above the 1, benchmark (1,67 points / +9.77%) for the first time since 16th January

WEEKLY MARKET REPORT April 2th, 212 / Week 16 For a second consecutive week the BDI continued to increase, ending the week above the 1, benchmark (1,67 points / +9.77%) for the first time since 16th January

WEEKLY MARKET REPORT February 13th, 2015 / Week 07

LY MARKET REPORT February 13th, 2015 / Week 07 The only positive note in the depressed freight market is the panamax index which gained 69 points, an increase of approximately 16%. All other indices remain

LY MARKET REPORT February 13th, 2015 / Week 07 The only positive note in the depressed freight market is the panamax index which gained 69 points, an increase of approximately 16%. All other indices remain

ERA Monthly Market Analysis

ERA Monthly Market Analysis May 2016 Introduction For the production of these statistics in the following report, ERA has teamed up with partners Seabury and Innovata to provide a comprehensive analysis

ERA Monthly Market Analysis May 2016 Introduction For the production of these statistics in the following report, ERA has teamed up with partners Seabury and Innovata to provide a comprehensive analysis

Weekly Market Report

Week 31 Tuesday 4th August 9 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News China's economy should grow by 8% this year and next, but significant risks

Week 31 Tuesday 4th August 9 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News China's economy should grow by 8% this year and next, but significant risks

WEEKLY MARKET REPORT November 19th, 2010 / Week 46

WEEKLY MARKET REPORT November 19th, 2010 / Week 46 A difficult week for the panamax market with the BPI losing 327 points representing a loss of almost 14%. The BDI fell nearly 7% mostly due to the sharp

WEEKLY MARKET REPORT November 19th, 2010 / Week 46 A difficult week for the panamax market with the BPI losing 327 points representing a loss of almost 14%. The BDI fell nearly 7% mostly due to the sharp

COSCO CORPORATION. (SINGAPORE) LTD FY2003 Full Year Results. Presentation

LTD FY2003 Full Year Results. Presentation") COSCO CORPORATION (SINGAPORE) LTD FY2003 Full Year Results Presentation 11 February 2004 1 Outline of Presentation 1. Background & Corporate Restructuring Exercise 2. Operations Review 3. Financial Review

COSCO CORPORATION (SINGAPORE) LTD FY2003 Full Year Results Presentation 11 February 2004 1 Outline of Presentation 1. Background & Corporate Restructuring Exercise 2. Operations Review 3. Financial Review

WEEKLY MARKET REPORT May 31st, 2013 / Week 22

LY MARKET REPORT May 31st, 2013 / Week 22 Apart from the supramax sector which rose marginally (BSI up 1.63%) all other segments lost ground for yet another week. Worst affected was the panamax which lost

LY MARKET REPORT May 31st, 2013 / Week 22 Apart from the supramax sector which rose marginally (BSI up 1.63%) all other segments lost ground for yet another week. Worst affected was the panamax which lost

WEEKLY MARKET REPORT March 28th, 2014 / Week 13

LY MARKET REPORT March 28th, 2014 / Week 13 Baltic rates in all dry segments experienced a downturn this week. Major losses in the capesize and panamax sector forced the overall BDI in a 14% decrease compared

LY MARKET REPORT March 28th, 2014 / Week 13 Baltic rates in all dry segments experienced a downturn this week. Major losses in the capesize and panamax sector forced the overall BDI in a 14% decrease compared

Weekly Market Report

Week 7 Tuesday 17th February 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News President Barack Obama today signs into law one of the largest pieces

Week 7 Tuesday 17th February 29 Weekly Market Report Sale & Purchase Newbuilding Secondhand Demolition Chartering World Economy News President Barack Obama today signs into law one of the largest pieces

Benchmarking Travel & Tourism in United Arab Emirates

Benchmarking Travel & Tourism in United Arab Emirates How does Travel & Tourism compare to other sectors? Summary of Findings, November 2013 Sponsored by: Outline Introduction... 3 UAE summary...... 8

Benchmarking Travel & Tourism in United Arab Emirates How does Travel & Tourism compare to other sectors? Summary of Findings, November 2013 Sponsored by: Outline Introduction... 3 UAE summary...... 8

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 11th October, 21 Volume 326 Week 41 Sale & Purchase Activity Week 41 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 11th October, 21 Volume 326 Week 41 Sale & Purchase Activity Week 41 SECOND HAND SALES DRY TONNAGE

WEEKLY MARKET REPORT October 8th, 2010 / Week 40

LY MARKET REPORT October 8th, 2010 / Week 40 Surprisingly, even though China is still on holiday, the spot capesize rates have shot up to US$ 40,000 per day and as a result charterers are coming out for

LY MARKET REPORT October 8th, 2010 / Week 40 Surprisingly, even though China is still on holiday, the spot capesize rates have shot up to US$ 40,000 per day and as a result charterers are coming out for

MARKET REPORT WEEK 05

MARKET REPORT WEEK 05 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th FEBRUARY 2011 Last week was a predictably quieter one on the shipping markets due to the Chinese New Year Holidays ushering

MARKET REPORT WEEK 05 BASED ON SALES AND PURCHASES OF VESSELS WEEK ENDED FRIDAY 4 th FEBRUARY 2011 Last week was a predictably quieter one on the shipping markets due to the Chinese New Year Holidays ushering

WEEKLY MARKET REPORT December 5th, 2014 / Week 49

LY MARKET REPORT December 5th, 2014 / Week 49 The freight market continued to soften throughout this week with the BDI concluding at 982 points, down by almost 15%. The index for capesize sector seems

LY MARKET REPORT December 5th, 2014 / Week 49 The freight market continued to soften throughout this week with the BDI concluding at 982 points, down by almost 15%. The index for capesize sector seems

WEEKLY MARKET REPORT June 22nd, 2007 / Week 25

TELEPHONE: ONE EXECUTIVE DRIVE TELEFAX: 201-585-9999 FORT LEE, NEW JERSEY 07024 201-585-9998 ships@compassmar.com WEEKLY MARKET REPORT June 22nd, 2007 / Week 25 The highlight of the week was the Marine

TELEPHONE: ONE EXECUTIVE DRIVE TELEFAX: 201-585-9999 FORT LEE, NEW JERSEY 07024 201-585-9998 ships@compassmar.com WEEKLY MARKET REPORT June 22nd, 2007 / Week 25 The highlight of the week was the Marine

DryShips Inc. 4 th Quarter Ended December 31, 2012 Earnings Presentation NASDAQ: DRYS

4 th Quarter Ended December 31, 2012 Earnings Presentation NASDAQ: DRYS March 7, 2013 Forward Looking Statements Matters discussed in this presentation may constitute forward-looking statements. Forward-looking

4 th Quarter Ended December 31, 2012 Earnings Presentation NASDAQ: DRYS March 7, 2013 Forward Looking Statements Matters discussed in this presentation may constitute forward-looking statements. Forward-looking

WEEKLY MARKET REPORT March 9th, 2012 / Week 10

WEEKLY MARKET REPORT March 9th, 2012 / Week 10 Yet another week with the smaller sizes outperforming the others. The BSI and BHSI ended nearly 16% and over 7% higher respectively. Whilst the BCI ended

WEEKLY MARKET REPORT March 9th, 2012 / Week 10 Yet another week with the smaller sizes outperforming the others. The BSI and BHSI ended nearly 16% and over 7% higher respectively. Whilst the BCI ended

TANKER MARKET CAN A MIRACLE HAPPEN?

TEN Ltd THE TANKER MARKET CAN A MIRACLE HAPPEN? Nikolas P. Tsakos President & CEO, TEN November 19 th, 2008 1 Tanker Freight Rates Remain Healthy Charterer discrimination against single hull tonnage on

TEN Ltd THE TANKER MARKET CAN A MIRACLE HAPPEN? Nikolas P. Tsakos President & CEO, TEN November 19 th, 2008 1 Tanker Freight Rates Remain Healthy Charterer discrimination against single hull tonnage on

Clive George. Current Position at CWA. Career Summary

Clive George Qualifications / Affiliations Class 1 (Motor) Certificate of Competency, 1990 Class 2 (Motor) Certificate of Competency, 1985 Chemical and Oil Tanker Safety Courses leading to DCE endorsements

Clive George Qualifications / Affiliations Class 1 (Motor) Certificate of Competency, 1990 Class 2 (Motor) Certificate of Competency, 1985 Chemical and Oil Tanker Safety Courses leading to DCE endorsements

GRINDROD LIMITED AUDITED RESULTS AND DIVIDEND ANNOUNCEMENT for the year ended 31 December 2016

www.grindrod.com GRINDROD LIMITED AUDITED RESULTS AND DIVIDEND ANNOUNCEMENT for the year ended 31 December 2016 Wifi access guest@sun Presentation and Announcement download www.grindrod.com > Investor

www.grindrod.com GRINDROD LIMITED AUDITED RESULTS AND DIVIDEND ANNOUNCEMENT for the year ended 31 December 2016 Wifi access guest@sun Presentation and Announcement download www.grindrod.com > Investor

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007.

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007. Athens, Greece, November 15, 2007. Globus Maritime Limited (AIM: GLBS), a

Globus Maritime Limited Trading Update and Financial Highlights for the Three Months and Nine Months Ended September 30, 2007. Athens, Greece, November 15, 2007. Globus Maritime Limited (AIM: GLBS), a

Trend

Fact Sheet - Safety Safety Trends Accident Overview 2009 2010 2011 2012 2013 2014 Trend Average 2009-2013 Yearly Flights (Millions)* 33.2 34.0 35.0 35.6 36.2 38.0 34.8 Total Accidents 90 94 92 75 81 73

Fact Sheet - Safety Safety Trends Accident Overview 2009 2010 2011 2012 2013 2014 Trend Average 2009-2013 Yearly Flights (Millions)* 33.2 34.0 35.0 35.6 36.2 38.0 34.8 Total Accidents 90 94 92 75 81 73

1H 2003 Results Announcement. August 1, 2003 SUMMARY

1H 2003 Results Announcement August 1, 2003 SUMMARY SembCorp Marine s revenue declined by 0.4 per cent to $489.8 million Operating profit increased by 5.4 per cent to $40.7 million PBT (before exceptional

1H 2003 Results Announcement August 1, 2003 SUMMARY SembCorp Marine s revenue declined by 0.4 per cent to $489.8 million Operating profit increased by 5.4 per cent to $40.7 million PBT (before exceptional

Inverness, Culloden and Suburbs Settlement Economic Overview

Strategic planning and research Economic information December 2007 Inverness, Culloden and Suburbs Settlement Economic Overview Summary Between 2001 and 2006, the population of Inverness, Culloden and

Strategic planning and research Economic information December 2007 Inverness, Culloden and Suburbs Settlement Economic Overview Summary Between 2001 and 2006, the population of Inverness, Culloden and