Circumnavigation HELM PwC Economy of the Sea Barometer (World)

|

|

|

- Tobias Strickland

- 5 years ago

- Views:

Transcription

1 HELM PwC Economy of the Sea Barometer (World) In-depth HELM December 2015 Edition nº1

2 2

3 I really don't know why it is that all of us are so committed to the sea, except I think it's because in addition to the fact that the sea changes, and the light changes, and ships change, it's because we all came from the sea. And it is an interesting biological fact that all of us have in our veins the exact same percentage of salt in our blood that exists in the ocean, and, therefore, we have salt in our blood, in our sweat, in our tears. We are tied to the ocean. And when we go back to the sea - whether it is to sail or to watch it - we are going back from whence we came. [Remarks at the Dinner for the America's Cup Crews, September 14, 1962] John F. Kennedy 3

4 This communication is of informative nature and intended for general purposes only. It does not address any particular person or entity nor does it relate to any specific situation or circumstance. PwC will not accept any responsibility arising from reliance on information hereby transmitted, which is not intended to be a substitute for specific professional business advice. 4

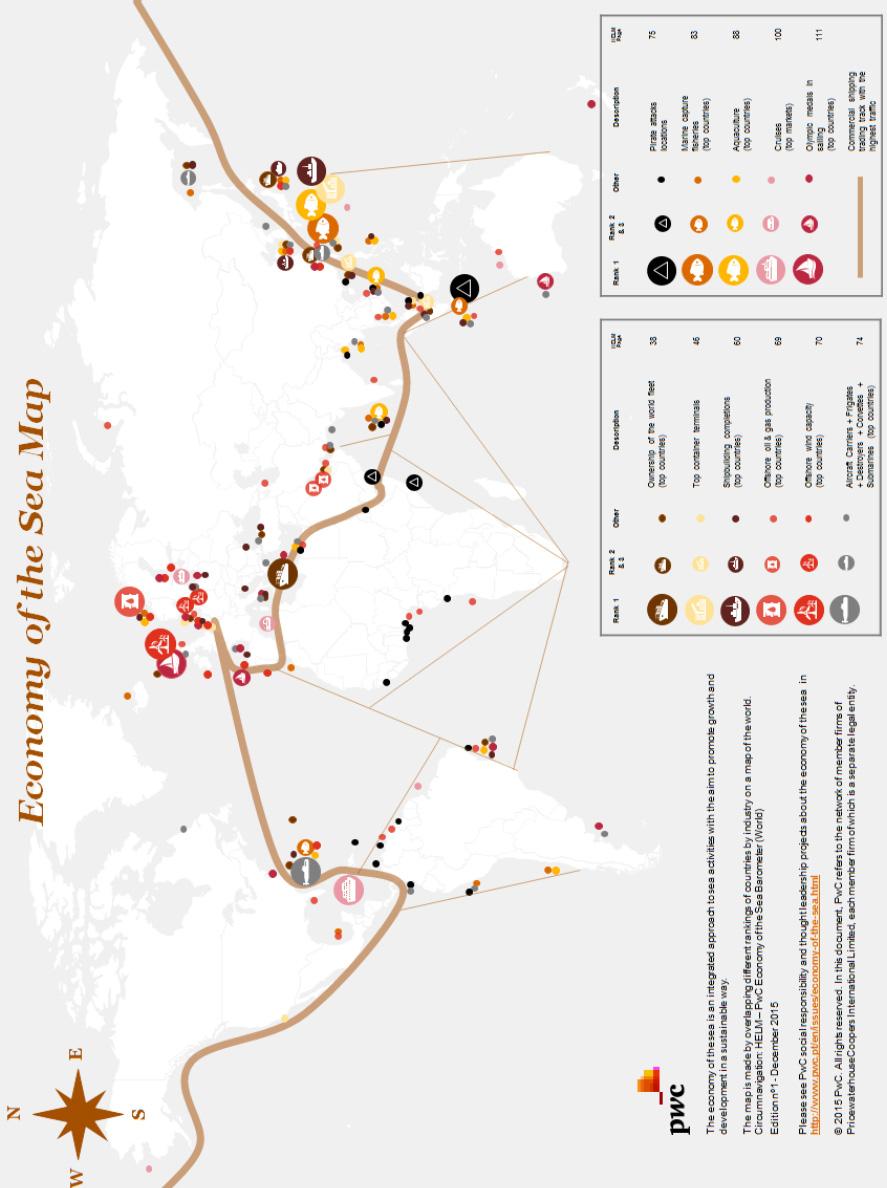

5 Index Introduction 7 Executive summary International context Maritime transport, ports and logistics Shipbuilding, maintenance and equipment Offshore energy Naval security power, piracy and maritime disasters (oil spills) Fishing and aquaculture Entertainment, sports, tourism and culture 97 Economy of the sea map List of Tables, Figures and Acronyms

6 : Edition nº1 - December 2015 is a PwC social responsibility and thought leadership initiative that includes three documents: - : Summary - : In-depth -EconomyoftheSeaMap The economy of the sea is an integrated approach to sea activities with the aim to promote growth and development in a sustainable way. Please see PwC social responsibility and thought leadership projects about the economy of the sea in 6

7 Introduction 7

8 8

9 Introduction The sea is a valuable global asset that needs to be preserved and valorised. Only with greater knowledge and an integrated view of this extensive resource are we able to ensure development in line with the principles of environmental, economic and social sustainability of marine resources. PwC s social responsibility project,, systematises, in a summarised form, quantitative information on various industries of the sea, enabling the identification of trends of ocean-related industries, and rankings, overlapped on a world map, to help identify the intensity of ocean use in every region of the world. The results of this exercise are clear. In the period 2005 to 2015, in which there was a profound financial and economic crisis on a global scale, during which time Asia - and in particular the China - took the lead in fisheries, aquaculture, cargo handling at ports and shipbuilding. The world's top 10 container ports are in Asia and seven of these are in China. In 2012, Chinese fisheries and aquaculture represented, respectively, 17% and 62% of total world output of these sectors. Only in the production of offshore energy, the ownership and operation of merchant ships, tourism (cruise) and sports does America and Europe remain ahead of Asia. Africa and South America are regions that will yet reveal important future economy of the sea opportunities. Australia and New Zealand, in particular, are references for the economy of the sea in Oceania and in the World. This period was also one of increased environmental stress (particularly oil spills) and sea piracy (more than 3,670 people were subjected to maritime piracy attacks, more than 3,300 were taken hostage and 27 were killed - Somalia, Nigeria and Indonesia are countries with the greatest incidence of attacks). As for the defence industry the United States of America, China and Russia are the three main naval powers. The five principal oceans: the Atlantic Ocean, the Indian Ocean, the Pacific Ocean, the Arctic Ocean and the Southern Ocean, together with the other seas of the world, are valuable assets that should be enjoyed by mankind sustainably. Several industries operate in or on this huge natural resource, producing wealth and generating jobs. In order to exploit all this wealth sustainably, it is essential to understand it better, becoming familiar with each of the industries, how they interact with each other, their evolution and how intensively they use the sea around the world. The is a contribution of reference about the economy of the sea in the world. It may be also seen as a voyage around the world in which the key countries for each sea industry are identified, this is why this publication has been entitled. José Bernardo Territory Senior Partner (Portugal) Miguel Marques Economy of the Sea Partner Henrik Steinbrecher Global Middle Market Leader Ricardo Frederico Correia Economy of the Sea Senior Manager 9

10 10

11 Executive summary 11

12 Executive summary The in-depth has two parts: 1. A summary of quantitative information on various subsectors that make up the economy of the sea in the world, including trend analysis and a number of rankings of countries by industry; 2. An economy of the sea map made by overlapping different rankings of countries by industry on a map of the world; The economy of the sea is a significant part of the world economy and, as such, is affected by the general evolution of macroeconomics. Taking into account growth rates of the various countries, it may be said that recent years have not been easy. In particular, the year 2009 was a particularly negative year in which the growth rate of global gross national product was negative (-2.1%), and the major contributors to this poor result were the developed economies (their gross domestic product fell in the order of -3.7%). In 2009, the low growth rate of gross domestic product in developing countries (+ 2.6%) was not enough to offset the negative growth in developed countries. The high growth rates of GDP recorded in 2006 (4.1%) have not yet been restored; the growth rate in 2013 was a mere 2.3%. 12

13 Executive summary Maritime transport, ports and logistics Recent years have been years of slowdown in global economic growth, which have negatively impacted the growth rate of the volume of exports and imports. As most of the load volume is transported by sea, the maritime transport sector has been considerably affected. Although oil and gas, as well as bulk, are the load types most transported by sea, containerized cargo has been growing. Between 2006 and 2013 there was a change in the relative importance of maritime trade in developed economies compared to developing economies. In 2006, developed economies accounted for approximately 53% of the tonnage of cargo transported by sea, a figure which fell to 39% in However, the share of developing economies in 2006 was 46% and increased to 60 % in This was primarily because Europe dropped from 54% in 2006 to 40% in 2013, while Asia rose from a 37% in 2006 to 49% in Between 1980 and 2014, bulk shipping and container shipping have gained weight compared to oil tankers and general load. Greece, Japan, China and Germany have the greatest concentration of ship ownership. Switzerland, Denmark, France, China and Germany are the countries where the headquarters of the leading transportation companies are primarily located. Panama, Liberia, The Marshall Islands, China and Singapore are the countries with largest ship registers. The world's ten largest container ports are Asian, and seven of these are Chinese. The world s five largest operators of ports have their headquarters in Singapore, the Netherlands, Unitied Arab Emirates or China. 13

14 Executive summary Shipbuilding, maintenance and equipment The order backlog in global shipyards grew between 2002 and 2008; thereafter, orders decreased until However, for the following three years (2012, 2013 and 2014), this trend has been reversed. At the end of 2014, more than half of ship orders were for solid bulk transport ships (52.2%), immediately followed by orders for tankers for the transport of crude oil (17.7%). In 2014, China had the highest volume of orders for ships (37.6%), followed by South Korea (28.9%) and Japan (16.1%). In fourth place appears the European Union 28+Norway (6.7%). In 2014, Asia (China, South Korea and Japan), completed more than 80% of the production of ships in that year (32.7%, 31.8% and 18.6% respectively). Ship production capacity drastically reduced in Europe 28 + Norway, but increased exponentially in China. China, India, Bangladesh and Pakistan were the locations where there was the most dismantling of bulk volume ships. Offshore energy In 2004, after the Middle East and North America and, Europe was the third largest oil and natural gas producing region of the world. By 2014, Europe had been relegated to 4th place; the Middle East continued to lead production, followed by South then North America. In 2014, more than half of the world's proven gas reserves belonged to Iran and the Russian Federation. Norway, Qatar and Saudi Arabia were the three main producers of offshore oil & gas, in the period 2010 to Since late 2014, the price of a barrel of Brent oil has been below 100 USD; in mid 2015, the price was slightly above 50 USD. The oil price decline has put pressure on the profitability of offshore operations, which are more expensive than onshore operations. Offshore wind power capacity in the world is led by four European countries (UK, Denmark, Germany and Belgium), representing 85.9% of total installed capacity in the world. In fifth place, China represents 7.5% of capacity. 14

15 Executive summary Naval security power, piracy and maritime disasters (oil spills) In 2015, the country with the largest naval fleet (aircraft carriers, frigates, destroyers, corvettes and submarines) is the US with 164, closely followed by China with 163. Russia is the third with 146 large naval craft. Somalia, Nigeria and Indonesia are countries with the greatest incidence of maritime piracy attacks in the period Between 2010 and 2014, about 3,670 people were subjected to maritime piracy attacks, more than 3,300 were taken hostage and 27 were killed. Accidents involving oil spills have been occurring over time, all over the world. Fishing and aquaculture Between 2002 and 2012, as the world population has grown, there has been an increase in the consumption of fish and other food products per capita. In 2002, per capita consumption was 16 kg, rising to a per capita consumption of 19.2 kg in This increase in per capita consumption was met by increased production in aquaculture. In 2002, production in onshore and offshore aquaculture reached about 24 and 16.4 million tons, respectively, rising to 41.9 and 24.7 million tons in Fish catches at sea continue to represent the largest contribution to the supply of fish, but have not grown in recent years. The top ten countries in terms of fishing, led by China with 17.4% of the catch, represent about 60% of the total of global fishing. The Pacific Ocean is where most of the fishing takes place, accounting for about 59% of the total. The fifteen species most fished represent about 1/3 of all fish caught. In 2012, 88% of world aquaculture was in Asia, and was responsible for the significant growth of aquaculture globally. Onshore aquaculture is the main contributor to the growth of aquaculture and China represents 61.7% of global aquaculture production. From 1974 to 2011, there was increasing pressure on fish stocks, significantly increasing the number of species that are in danger of overfishing. Africa and Latin America are the regions of the world with the lowest per capita consumption of fish and other sea products. 15

16 Executive summary Entertainment, sports, tourism and culture The revenue associated with cruise ships has been increasing. North America and Europe are the most important markets for cruise ships. The Caribbean still holds the largest market share in the business of cruise ships, closely followed by the Mediterranean and the rest of Europe. Between 2013 and 2014, the Caribbean and Europe (excluding the Mediterranean) enjoyed an increase in their overall market share in this business, while the Mediterranean region saw a reduction in its market share from 21.7% to 18,.9%. The number of people participating in cruises has increased. The largest cruise consumers are North Americans, immediately followed by the British and the Irish. The USA, Australia, New Zealand, Italy, France and the UK are countries of reference in terms of the recreational boating and marinas business. In the last three Olympic Games, Europe was the continent with more medals in canoeing, with Germany as the country that led with 20 medals. In sailing, while European countries, led by the UK, continue well classified, winning 16 medals at the last three Olympic Games, Australia appears in second place in the ranking with 10 medals. In rowing, the United Kingdom leads with 20 medals, soon followed by Australia (12) and New Zealand (9). In surfing, Australia has led consistently in recent years. 16

17 17

18 18

19 HELM PwC Economy of the Sea Barometer (World) 19

20 HELM PwC Economy of the Sea Barometer (World) More than 2/3 of the surface area of our planet is sea. The five principal oceans: the Atlantic Ocean, the Indian Ocean, the Pacific Ocean, the Arctic Ocean and the Southern Ocean, and the other of seas of the world, are valuable assets that should be enjoyed by mankind sustainably. Several industries operate in or on this huge natural resource, producing wealth and generating jobs. In order to enhance all this wealth in a sustainable way, it is essential to understand it better, becoming familiar with each of the industries, and how they interact with each other, their evolution and how intensively they use the sea around the world. The concept of Economy of the Sea is related to the valorisation of the ocean in environmental, social and economic terms, with the aim to achieve a holistic view of all human action on sea. It includes industries like maritime transport, ports and logistics, shipbuilding, ship maintenance and repair, offshore energy, security and defence, fisheries and aquaculture, entertainment, sport, tourism and leisure. Learning more about the oceans, also means learning more about maritime industries, in particular, it is crucial to quantify their economic development in each region. There has been some quantitative information by industry, but there are few studies that quantify the economic development of all the industries related with the sea. With, we intend to build a tool that allows us to clarify the current situation in respect of the sea as a resource in the world, as well as its development prospects in the future. The HELM is meant to be a monitoring tool that allows its users to draw useful information, easily and quickly. The HELM is a long-term project, which will act as a compilation of data for monitoring, over time, the evolution of the economy of the sea in the world and simultaneously enable us to analyse trends and the choices that are made by the various economic agents. Several efforts have been made by various entities in order to quantitatively evaluate the importance of the economy of the sea. Progress has been made; however, the weight of economic activities related to the sea in total world economy remains difficult to measure and evaluate. The indicators do not allow us to measure with complete accuracy or continuously, the actual impact of these activities in the global economy. 20

21 HELM PwC Economy of the Sea Barometer (World) The has two parts: 1. A summary of quantitative information on various subsectors that make up the economy of the sea in the world, including trend analysis and a number of rankings of countries by industry; 2. An economy of the sea map made by overlapping different rankings of countries by industry on a map of the world. Sea industries considered Relevant sub-sectors within the sea economy of the world considered in summary quantitative information: - Maritime transport, ports and logistics; - Shipbuilding, ship repair and maintenance; - Offshore energy; - Security and defence; - Fishing and aquaculture; - Entertainment, sport, tourism and leisure. There is another set of sub-sectors, such as offshore mineral resources and blue biotechnology that, although reveal a huge potential, will still take some time to gain importance in the global economy. Rankings Taking into account the existing quantitative information and respective representation that the variable has on the industry analysis, the following variables were selected for the preparation of rankings considered in the Economy of the Sea Map: - Ownership of the world fleet (top countries) - Top container terminals - Shipbuilding completions (top countries) - Offshore oil & gas production (top countries) - Offshore wind capacity (top countries) - Aircraft Carriers + Frigates + Destroyers + Corvettes + Submarines (top countries) - Pirate attacks locations - Marine capture fisheries (top countries) - Aquaculture (top countries) - Cruises (top markets) - Olympic medals in sailing(top countries) - Commercial shipping trading track with the highest traffic 21

22 HELM PwC Economy of the Sea Barometer (World) Update of the quantitative information (*) As mentioned above, quantification and measurement of the economy of the sea remains difficult. However, as time goes by, new sources of information appear and new reliable indicators may be used. In this context, every year we do a careful review of all the variables that compose the quantitative summary information and update it with relevant information, which has since become available. Similarly, every year, reconfirm that the comparative data of information sources quantitative information summary remain stable. In case of restatement, by the issuer, we proceed to the respective update summary quantitative information. Whenever new information is included in the quantitative information summary or where the variables considered in the economy of the sea map have been changed, the respective variables will be marked with an asterisk. 22

23 23

24 24

25 International context 25

26 International context Exclusive Economic Zones Countries with the largest exclusive economic zones have a bigger potential to have benefits from the oceans. Below is presented the ranking of the 25 countries with the largest exclusive economic zones. Table 1: Top 25 Exclusive Economic Zones (in millions of square kilometers), 2015 EEZ 2015 (Millions of Km2) USA 12.2 Federated States of Micronesia 3.0 France 10.1 Denmark 2.6 Australia 9.1 Norway 2.4 Russia 7.6 Papua New Guinea 2.4 United Kingdom 6.8 India 2.3 Indonesia 6.0 Marshall Islands 2.0 Canada 5.7 Philippines 1.8 New Zealand 4.1 Portugal 1.7 Japan 4.0 Solomon Islands 1.6 Brazil 3.7 South Africa 1.5 Chile 3.7 Mauritius 1.3 Kiribati 3.5 Seychelles 1.3 Mexico 3.3 Source: Marineregions.org 26

27 International context World Economic Growth The economy of the sea is a significant part of the world economy and, as such, is affected by the general evolution of macroeconomics. Taking into account growth rates of the various countries, it may be said that recent years have not been easy. In particular, the year 2009 was a particularly negative year in which the growth rate of global gross national product was negative (-2.1%), and the major contributors to this poor result were the developed economies (their gross domestic product fell in the order of -3.7%). In 2009, the low growth rate of gross domestic product in developing countries (+ 2.6%) was not enough to offset the negative growth in developed countries. The high growth rates of GDP recorded in 2006 (4.1%) have not yet been restored; the growth rate in 2013 was a mere 2.3%. Table 2: World GDP growth, (Annual percentage change) Region/country World 4.1% 4.0% 1.5% -2.1% 4.1% 2.8% 2.3% 2.3% 2.7% Developed countries 2.8% 2.5% 0.0% -3.7% 2.6% 1.4% 1.1% 1.3% 1.8% of which: Japan 1.7% 2.2% -1.0% -5.5% 4.7% -0.6% 1.4% 1.6% 1.4% United States 2.7% 1.8% -0.3% -2.8% 2.5% 1.6% 2.3% 2.2% 2.1% European Union (EU-28) 3.4% 3.2% 0.3% -4.6% 2.1% 1.7% -0.3% 0.1% 1.6% South-East Europe and CIS 8.5% 8.7% 5.3% -6.6% 4.8% 4.7% 3.3% 2.0% 1.3% b South-East Europe 4.6% 5.9% 5.0% -2.1% 1.7% 1.9% -0.8% 2.0% 2.0% CIS, incl. Georgia 8.7% 8.9% 5.3% -6.8% 4.9% 4.8% 3.5% 2.0% 1.2% of which: Russian Federation 8.2% 8.5% 5.2% -7.8% 4.5% 4.3% 3.4% 1.3% 0.5% Developing countries 7.7% 8.0% 5.4% 2.6% 7.8% 6.0% 4.7% 4.6% 4.7% Africa 5.8% 6.1% 5.5% 2.5% 4.9% 0.9% 5.3% 3.5% 3.9% Latin America and the Caribbean 5.5% 5.5% 3.7% -1.6% 5.7% 4.3% 3.0% 2.6% 1.9% Asia 8.7% 9.1% 6.0% 4.0% 8.9% 7.2% 5.2% 5.3% 5.6% of which: China 12.7% 14.2% 9.6% 9.2% 10.4% 9.3% 7.7% 7.7% 7.5% India 9.4% 10.1% 6.2% 5.0% 11.0% 7.9% 4.9% 4.7% 5.6% Oceania 2.8% 3.4% 2.7% 2.4% 3.7% 4.9% 4.3% 2.9% 3.2% Note: Calculations for country aggregates are based on GDP at constant 2005 dollars. a) Forecasts. b) Albania, Bosnia and Herzegovina, Montenegro, Serbia and the former Yugoslav Republic of Macedonia. Source: UNCTAD Trade and Development Report 2014 a 27

28 28

29 Maritime transport, ports and logistics 29

30 Maritime transport, ports and logistics Recent years have seen a slowdown in global economic growth, which resulted in a fall in the growth rate of export volume and import volumes. As shown in the table below, the growth rate of export volume in the world in 2010 was 13.9%, falling to 2.2% in The same goes in the growth rate of the import volume in the world: in 2010, it was 13.8%; by 2013, it was 2.1%. This decline in the growth rate of exports and imports affected all developed countries and all developing countries. Table 3: Growth in the volume of merchandise trade, (Annual percentage change) Exports Imports Countries/regions % 5.5% 2.3% 2.2% World 13.8% 5.4% 2.1% 2.1% a 12.9% 4.9% 0.5% 1.3% Developed economies 10.8% 3.4% -0.4% -0.4% of which: 11.6% 5.5% -0.1% 1.4% European Union (EU-28) 9.4% 2.8% -2.5% -1.2% 27.5% -0.6% -1.0% -1.8% Japan 10.1% 4.2% 3.8% 0.5% 15.4% 7.2% 4.0% 2.6% United States 14.8% 3.8% 2.8% 0.9% 16.0% 6.7% 4.6% 5.1% Developing economies 18.5% 7.7% 5.3% 5.5% of which: 10.3% -6.8% 7.8% -1.8% Africa 6.5% 3.9% 11.8% 5.6% 8.1% 5.1% 3.1% 1.5% Developing America 22.3% 11.3% 3.1% 2.4% 18.2% 8.5% 4.5% 4.3% Asia 19.3% 7.3% 5.1% 6.1% of which: 29.5% 13.4% 7.4% 4.8% China 25.0% 10.7% 6.1% 8.8% 14.0% 15.0% -1.8% 7.6% India 13.8% 9.7% 5.5% 0.1% 4.2% 9.1% 9.8% 2.2% Western Asia 8.6% 8.2% 8.7% 8.6% 11.4% 4.1% 1.3% 1.0% Transition economies 17.6% 16.8% 5.0% 2.7% Note: Data on trade volumes are derived from international merchandise trade values deflated by UNCTAD unit value indices. Source: UNCTAD - Review of Maritime Transport

31 Maritime transport, ports and logistics Most of the load volume is transported by sea and, consequently, the maritime transport sector was impacted by slowing growth of exports and imports globally. Although oil and gas, as well as bulk, are the load types most transported by sea, containerized cargo has been growing. Table 4: International seaborne trade, selected years (Millions of tons loaded) Year Container Other dry cargo Five major bulks Oil and gas , , , , , ,125 1,105 2, ,928 1,295 2, ,009 1,709 2,422a ,076 2,112 1,814 2, ,193 2,141 1,953 2, ,249 2,173 2,065 2, ,127 2,004 2,085 2, ,280 2,022 2,335 2, ,393 2,112 2,486 2, ,445 2,169 2,742 2, ,524 2,260 2,920 2,844 Source: UNCTAD - Review of Maritime Transport 2014 Figure 1: International seaborne trade, selected years (Millions of tons loaded) Oil and gas Five major bulks Other dry cargo Container

32 Maritime transport, ports and logistics Between 2006 and 2013 there was a change in the relative importance of maritime trade in developed economies compared to developing economies. In 2006, developed economies accounted for approximately 53% of the tonnage of cargo transported by sea, a figure which fell to 39% in However, the share of developing economies in 2006 was 46% and increased to 60 % in This was primarily because Europe dropped from 54% in 2006 to 40% in 2013, while Asia rose from a 37% in 2006 to 49% in 2013 Table 5: World seaborne trade in , by type of cargo, country group and region (Millions of tons) Goods unloaded (Millions of tons) Region/country Year Total Crude Petroleum products and gas Dry cargo Share of the total World Developed economies Transition economies Developing economies Africa America Asia Europe Oceania ,879 1, , % ,505 1,889 1,091 6, % ,165 1, ,347 53% ,668 1, ,093 39% % % , ,644 46% , ,290 60% % % % % , ,105 37% , ,550 49% ,235 1, ,409 54% ,817 1, ,235 40% % % a Source: UNCTAD - Review of Maritime Transport

33 Maritime transport, ports and logistics The largest consumers of oil and natural gas worldwide are East Asia and North America. Table 6: Major producers and consumers of oil and natural gas, 2013 (Percentage world market share) World oil production World oil consumption Western Asia 33% Asia Pacific 33% Transition economies 17% North America 23% North America 16% Europe 15% Developing America 12% Developing America 10% Africa 10% Western Asia 10% Asia Pacific 9% Transition economies 5% Europe 3% Africa 4% a World natural gas production World natural gas consumption North America 25% North America 25% Transition economies 23% Asia Pacific 19% Western Asia 17% Transition economies 16% Asia Pacific 14% Europe 14% Europe 8% Western Asia 14% Developing America 7% Developing America 8% Africa 6% Africa 4% Note: Oil includes crude oil, shale oil, oil sands and natural gas liquids. The term excludes liquid fuels from other sources such as biomass and coal derivatives. Source: UNCTAD - Review of Maritime Transport

34 Maritime transport, ports and logistics At a global level, shipping containers have increased a lot; however, with the 2009 global crisis and a decrease of world gross domestic product, there was a negative growth of containerization in that year. Figure 2: Global containerized trade, (Millions of TEUs and percentage annual change) Million TEUs (left) Percentage annual change (right) Source: UNCTAD - Review of Maritime Transport

35 Maritime transport, ports and logistics In terms of container transport, the transatlantic route in 2014 represented about 6.5% of total TEU s transported, while the transpacific route accounted for about 22.7%. Table 7: Distribution of global containerized trade by route, (Millions of TEUs) Year Intraregional & South-South North-South Trans-Pacific (Millions of TEUs) Far East- Europe Secondary East-West Transatlantic Source: UNCTAD - Review of Maritime Transport 2014 Figure 3: Distribution of global containerized trade by route, (Millions of TEUs) Intraregional & South-South North-South Trans-Pacific Far East-Europe Secondary East-West Transatlantic

36 Maritime transport, ports and logistics Asia, and particularly China, is the main importer of steel, iron, coal and grain, while the American Continent and Australia are the main exporters of these strategic products. Table 8: Some major dry bulks and steel: Main producers, users, exporters and importers, 2013 (Percentage world market share) Steel producers % Steel users % China 49% China 47% Japan 7% European Union 10% United States 5% North America 9% India 5% Transition economies 4% Russian Federation 4% Developing America 3% Republic of Korea 4% Western Asia 3% Germany 3% Africa 2% Turkey 2% Other 22% Brazil 2% Ukraine 2% Other 17% Iron ore exporters % Iron ore importers % Australia 49% China 67% Brazil 27% Japan 11% South Africa 5% European Union 9% Canada 3% Republic of Korea 5% Sweden 3% Other 8% Other 13% Coal exporters % Coal importers % Indonesia 34% China 19% Australia 32% Japan 17% United States 9% European Union 16% Colombia 7% India 16% Russian Federation 7% Republic of Korea 11% South Africa 6% China, Taiwan Province of 5% Canada 3% Malaysia 2% Other 2% Thailand 2% Other 12% Grain exporters % Grain importers % United States 19% Asia 31% Argentina 12% Developing America 21% European Union 11% Africa 20% Australia 10% Western Asia 18% Ukraine 9% Europe 7% Canada 8% Transition economies 3% Others 31% Source: UNCTAD - Review of Maritime Transport

37 Maritime transport, ports and logistics From 1980 to 2014 bulk ship and containers have gained relative weight compared to oil and general load tankers. Table 9: World fleet by principal vessel types, (Beginning-of-year figures, percentage share of dwt) Year Other Container General cargo Dry bulk Oil tanker % 1.6% 17.0% 27.2% 49.7% % 3.9% 15.6% 35.6% 37.4% % 8.0% 12.7% 34.6% 35.4% % 13.3% 8.5% 35.8% 35.3% % 12.8% 4.6% 42.9% 28.5% Note: All propelled seagoing merchant vessels of 100 GT and above, excluding inland waterway vessels, fishing vessels, military vessels, yachts, and offshore fixed and mobile platforms and barges (with the exception of FPSOs and drill ships). Source: UNCTAD - Review of Maritime Transport 2014 Figure 4: World fleet by principal vessel types, (Beginning-of-year figures, percentage share of dwt) 100% 90% 80% 70% 60% 50% 40% 30% Oil tanker Dry bulk General cargo Container Other 20% 10% 0%

38 Maritime transport, ports and logistics Greece, Japan, China and Germany are the countries with the highest concentration of ship ownership. Table 10: Ownership of the world fleet, as of 1 January 2014 (dwt and nº of ships) Dead-weight tonnage (thousand dwt) Beneficial Owner Location aª Number of ships Greece 258,484 3,826 Japan 228,553 4,022 China 200,179 5,405 Germany 127,238 3,699 Republic of Korea 78,240 1,568 Singapore 74,064 2,120 United States 57,356 1,927 United Kingdom 52,821 1,233 Taiwan 47, Norway 42,972 1,864 Denmark 40, Bermuda 36, Turkey 29,266 1,547 Hong Kong SAR (China) 26, Italy 24, India 21, Brazil 19, United Arab Emirates 19, Russian Federation 18,883 1,734 Iran (Islamic Republic of) 18, Note: Vessels of 1,000 GT and above. a Beneficial ownership location indicates the country/economy in which the company that has the main commercial responsibility for the vessel is located. Source: UNCTAD - Review of Maritime Transport 2014 Ranking included in the economy of the sea map. 38

39 Maritime transport, ports and logistics Switzerland, Denmark, France, China and Germany are the countries where the headquarters of the leading transportation companies are primarily located. Table 11: The 20 leading liner companies (headquarters country), 1 January 2014 (Number of ships and total shipboard capacity deployed, in TEUs, ranked by TEU) Ranking Headquarters Vessels TEU 1 Switzerland 461 2,609,181 2 Denmark 456 2,505,935 3 France 348 1,508,007 4 Taiwan 229 1,102,245 5 China ,696 6 Germany ,613 7 China ,644 8 Republic of Korea ,210 9 Singapore , United Arab Emirates , Japan , Taiwan , Germany , China , Japan , Republic of Korea , Japan , Singapore , Chile , Israel ,192 Note: Includes all container-carrying ships known to be operated by liner shipping companies. Source: UNCTAD - Review of Maritime Transport

40 Maritime transport, ports and logistics Panama, Liberia, The Marshall Islands, China and Singapore are the countries with largest ship registers. Table 12: The 20 flags of registration with the largest registered fleets, as of 1 January 2014 (dwt) Flag of registration Number of ships Dead-weight tonnage (thousand dwt) Per cent of world total (dwt) Panama 7, , % Liberia 3, , % Marshall Islands 2, , % China, Hong Kong SAR 2, , % Singapore 2, , % Greece , % Bahamas 1,327 74, % China 2,802 73, % Malta 1,698 72, % Cyprus , % Isle of Man , % Italy , % United Kingdom , % a Norway (NIS) , % Japan , % Republic of Korea , % Germany , % India , % a Denmark (DIS) , % Indonesia 1,609 13, % Rest of the World 16, , % Total World 47,601 1,676, % Note: Propelled seagoing merchant vessels of 1,000 GT and above; ranked by dead-weight tonnage. For a complete list of all countries for ships of 100 GT and above see NIS: Norwegian International Ship Register; DIS: Danish International Ship Register. Source: UNCTAD - Review of Maritime Transport

41 Maritime transport, ports and logistics Most ship owners register their ships in different location from the country where they are located, looking for better conditions. Figure 5: Top 20 ship owning nations, beneficial ownership, 1 January 2014 (1,000 dwt, by country/economy of ownership) Greece Japan China Germany Republic of Korea Singapore United States United Kingdom Taiwan Norway Denmark Bermuda Turkey China, Hong Kong SAR Italy India Brazil United Arab Emirates Russian Federation Islamic Republic of Iran Foreign flag Note: Propelled seagoing merchant vessels of 1,000 GT and above. Source: UNCTAD - Review of Maritime Transport 2014 National flag 41

42 Maritime transport, ports and logistics Most ships are registered in developing countries. Table 13: Distribution of dwt capacity of vessel types, by country group of registration, January 2014 (Beginning-of-year figures, per cent of dwt) Total fleet Oil tankers Bulk carriers General cargo Container ships Others World total 100% 100% 100% 100% 100% 100% Developed countries 23.28% 26.38% 18.52% 28.91% 27.55% 25.96% Countries with economies in transition 0.72% 0.76% 0.27% 5.18% 0.04% 1.17% Developing countries 75.76% 72.80% 81.16% 65.10% 72.40% 71.40% of which: Africa 13.69% 17.53% 10.14% 5.66% 23.07% 9.93% America 28.57% 21.17% 34.80% 24.86% 22.73% 32.52% Asia 24.57% 21.69% 27.69% 32.14% 22.36% 19.53% Oceania 8.92% 12.41% 8.53% 2.44% 4.24% 9.42% Unknown and other 0.24% 0.06% 0.05% 0.81% 0.01% 1.47% Note: Propelled seagoing merchant vessels of 100 GT and above. Source: UNCTAD - Review of Maritime Transport

43 Maritime transport, ports and logistics The years 2009, 2011 and 2013 were years of decline in freight prices. Table 14: Container freight markets and rates Freight markets Trans-Pacific a ($ per FEU) Shanghai - United States West Coast 1,372 2,308 1,667 2,287 2,033 Percentage change 68% -28% 37% -11% Shanghai - United States East Coast 2,367 3,499 3,008 3,416 3,290 Percentage change 48% -14% 14% -4% Far East-Europe ($ per TEU) Shanghai - Northern Europe 1,395 1, ,353 1,084 Percentage change 28% -51% 54% -20% Shanghai-Mediterranean 1,397 1, ,336 1,151 Percentage change 24% -44% 37% -14% North-South ($ per TEU) Shanghai-South America (Santos) 2,429 2,236 1,483 1,771 1,380 Percentage change -8% -34% 19% -22% Shanghai-Australia/New Zealand (Melbourne) 1,500 1, Percentage change -21% -35% 20% -12% Shanghai-West Africa (Lagos) 2,247 2,305 1,908 2,092 1,927 Percentage change 3% -17% 10% -8% Shanghai-South Africa (Durban) 1,495 1, , Percentage change -1% -33% 6% -23% Intra-Asian ($ per TEU) Shanghai-South-East Asia (Singapore) Percentage change -34% 22% -10% Shanghai-East Japan Percentage change 7% 2% 0% Shanghai-Republic of Korea Percentage change 3% -8% 8% Shanghai-Hong Kong (China) Percentage change 34% -15% -35% Shanghai-Persian Gulf (Dubai) Percentage change 44% -9% 17% -21% Note: Data based on yearly averages. a FEU: 40-foot equivalent unit. Source: UNCTAD - Review of Maritime Transport

44 Maritime transport, ports and logistics In the period , the supply of transport in containers always grew; however, in 2009, the demand decreased. The growth in demand after 2009, on average, is lower than the growth in demand before Table 15: Growth of demand and supply in container shipping, (Annual growth rates) Year Demand Supply % 7.8% % 8.5% % 8.0% % 8.0% % 8.0% % 10.5% % 13.6% % 11.8% % 10.8% % 4.9% % 8.3% % 6.8% % 4.9% % 4.7% % 3.7% Note: Supply data refer to the total capacity of the container-carrying fleet, including multi-purpose and other vessels with some degree of container carrying capacity. Demand growth is based on million TEU lifts. The data for 2014 are projected figures. Source: UNCTAD - Review of Maritime Transport 2014 Figure 6: Growth of demand and supply in container shipping, (Annual growth rates) 15,00% 10,00% 5,00% 0,00% Demand Supply -5,00% -10,00% -15,00% 44

45 Maritime transport, ports and logistics The Baltic Dry Index is a reference index in the analysis of the price of maritime transport. Figure 7: Baltic Exchange Dry Index, (19 August 2015) (Index base year 1985 = 1,000 points) 2500 Baltic Exchange Dry Index Note: The BDI is a composite of 3 sub-indices, each covering a different carrier size: Capesize, Panamax, and Supramax. Capesize carriers are the largest ships with a capacity greater than 150,000 DWT. Panamax refers to the maximum size allowed for ships travelling through the Panama Canal, typically 65,000-80,000 DWT. The Supramax Index covers carriers with a capacity of 50,000-60,000 DWT. Source: 45

46 Maritime transport, ports and logistics The world's ten largest container ports are Asian, seven are Chinese. Table 16: Top 20 container terminals and their throughput for 2011, 2012 and 2013 (Million TEUs and percentage change) Port Name Country Preliminary figures for 2013 Percentage change Percentage share in the world Million TEUs Shanghai China % 5.6% Singapore Singapore % 5.0% Shenzhen China % 3.6% Hong Kong (China) Hong Kong, China % 3.4% Busan Republic of Korea % 2.7% Ningbo China % 2.7% Qingdao China % 2.4% Guangzhou China % 2.3% Dubai United Arab Emirates % 2.1% Tianjin China % 2.0% Rotterdam Netherlands % 1.8% Port Klang Malaysia % 1.6% Dalian China % 1.5% Kaohsiung Taiwan % 1.5% Hamburg Germany % 1.4% Long Beach United States % 1.3% Antwerp Belgium % 1.3% Xiamen China % 1.2% Los Angeles United States % 1.2% Tanjung Pelepas Malaysia % 1.2% Total top % 46.0% Note: In this list Singapore does not include the port of Jurong. Source: UNCTAD - Review of Maritime Transport 2014 Ranking included in the economy of the sea map. 46

47 Maritime transport, ports and logistics The five largest ports operators in the world have their headquarters in Singapore, the Netherlands, United Arab Emirates or China. Table 17: Top 10 global terminal operators (headquarters country), 2012 (Million TEUs and market share) Headquarters Million TEUs %share 1 Singapore % 2 Hong Kong, China % 3 Netherlands % 4 United Arab Emirates % 5 China % 6 Luxemburg % 7 China % 8 Republic of Korea % 9 Taiwan % 10 Germany 6.5 1% Source: UNCTAD - Review of Maritime Transport

48 48

49 Shipbuilding, maintenance and equipment 49

50 Shipbuilding, maintenance and equipment The order backlog in global shipyards grew between 2002 and 2008; thereafter, orders decreased until However, for the following three years (2012, 2013 and 2014), this trend has been reversed. Table 18: Summary of activity in World Shipyards (Thousands of CGT) Year Order book New orders Completions ,946 20,471 21, ,807 41,705 22, ,800 45,128 25, ,200 39,588 29, ,000 57,315 34, ,740 85,277 34, ,166 42,953 41, ,200 16,554 44, ,013 38,581 51, ,442 30,823 51, ,300 24,713 47, ,900 53,839 38, ,146 45,592 36,450 Note: CGT - Compensated Gross Tonnage- International unit of measure that facilitates the comparison of different shipyards production regardless of the types of vessel produced. The CGT of a ship is calculated using a table of conversion factors published by OECD. The conversion factors vary with ship type. GT Gross Tonnage; unit of 100 cubic feet or cubic meters, used in arriving at the calculation of gross tonnage. Source: Sea Europe, Shipbuilding Market Monitoring 2014 Figure 8: Summary of activity in World Shipyards (Thousands of CGT) Order book New orders Completions

51 Shipbuilding, maintenance and equipment The evolution of activity in Chinese shipyards has followed the trend in the shipyards globally, although the growth recorded between 2002 and 2008 was more significant than that in the rest of the world. Table 19: Summary of activity in Chinese shipyards (Thousands of CGT) Year Order book New orders Completions ,943 2,669 1, ,327 5,235 2, ,589 5,691 2, ,629 6,067 4, ,701 13,366 5, ,221 28,925 6, ,011 13,864 9, ,359 7,113 12, ,923 16,102 18, ,878 8,339 19, ,209 8,555 19, ,649 21,402 13, ,641 16,900 11,907 Source: Sea Europe, Shipbuilding Market Monitoring 2014 Figure 9: Summary of activity in Chinese shipyards (Thousands of CGT) Order book New orders Completions

52 Shipbuilding, maintenance and equipment Although in general, the activity of South Korean shipyards is below the activity of Chinese shipyards, at the end of 2014, the number of finished ships was very similar. Table 20: Summary of activity in South Korean shipyards (Thousands of CGT) Year Order book New orders Completions ,215 5,663 6, ,368 18,671 7, ,365 15,806 8, ,243 13,960 10, ,544 21,884 11, ,389 32,969 11, ,357 14,780 14, ,576 3,383 14, ,145 11,915 14, ,529 13,615 15, ,517 7,111 13, ,169 17,437 12, ,244 12,588 11,606 Source: Sea Europe, Shipbuilding Market Monitoring 2014 Figure 10: Summary of activity in South Korean shipyards (Thousands of CGT) Order book New orders Completions

53 Shipbuilding, maintenance and equipment Japanese shipyards have also seen a recovery in the last three years, both in terms of order book and in terms of new orders, although the number of finished ships has fallen over the same period. Table 21: Summary of activity of Japanese shipyards (Thousands of CGT) Year Order book New orders Completions ,052 7,965 6, ,076 11,779 6, ,113 13,675 7, ,894 8,620 8, ,372 11,193 9, ,714 10,125 8, ,649 7,820 9, ,460 3,877 9, ,836 5,374 9, ,132 4,118 9, ,534 4,396 8, ,615 7,550 7, ,442 10,256 6,768 Source: Sea Europe, Shipbuilding Market Monitoring 2014 Figure 11: Summary of activity of Japanese shipyards (Thousands of CGT) Order book New orders Completions

54 Shipbuilding, maintenance and equipment European yards also have experienced a recovery as from 2012, with new orders at the same level as 2007, before the global economic crisis. Table 22: Summary of activity of EU28+ Norway shipyards (Thousands of CGT) Year Order book New orders Completions ,666 2,341 4, ,610 3,951 4, ,406 6,798 4, ,738 7,226 3, ,430 5,597 4, ,376 5,257 4, ,209 2,229 4, , , ,495 2,487 4, ,836 1,830 2, ,058 1,859 2, ,705 2,515 1, ,247 3,394 2,179 Source: Sea Europe, Shipbuilding Market Monitoring 2014 Figure 12: Summary of activity of EU28+ Norway shipyards (Thousands of CGT) Order book New orders Completions

55 Shipbuilding, maintenance and equipment At the end of 2014, more than half of the order ships refer to solid bulk load ship (52.2%), immediately followed by orders for tankers for the transport of crude oil (17.7%). Table 23: Orderbook by Ship Types Types NO GT CGT DWT % DWT Crude Oil Tanker ,819 8,724 48, % Oil Products Tanker 177 2,494 1,670 4, % Chemical Tanker ,307 7,023 16, % Other Liquids % Tankers ,623 17,425 69, % Bulk Dry 1,687 78,857 33, , % Bulk Dry / Oil % Self-Discharging Bulk Dry % Other Bulk Dry % Bulk Carriers 1,713 79,351 33, , % General Cargo 331 3,253 2,849 4, % Container ,920 15,803 34, % Refrigerated Cargo % Ro-Ro Cargo 115 4,804 2,669 1, % Other Dry Cargo % Dry Cargoes ,845 21,896 42, % LNG Tanker ,636 12,219 11, % LPG Tanker 228 6,222 4,450 6, % Gastankers ,858 16,669 18, % Passenger/Ro-Ro Cargo % Passenger (Cruise) 40 3,973 4, % Other Passenger Vessels/Ferries % Ferries / Passenger Ships 169 4,639 4, % Fish Catching % Other Fishing % Offshore Supply 768 2,107 4, % Other Offshore 318 7,614 6, % Research % Towing / Pushing % Dredging % Other Activities % Other Non Cargo Vessels 2,047 11,075 13, % Total 6, , , , % Source: Sea Europe, Shipbuilding Market Monitoring

56 Shipbuilding, maintenance and equipment In 2014, China had the highest volume of orders for ships (37.6%), followed by South Korea (28.9%) and Japan (16.1%). Fourth, is the European Union 28+ Norway with 6.7%. Table 24: Orderbook by Country Country NO GT % CGT % Croatia % % Germany 28 1, % 1, % Italy 26 1, % 1, % Netherlands % % Poland % % Romania 82 2, % 1, % Spain % % Other EU , % 1, % EU , % 6, % Norway % % Russia % % Turkey % % Other % % Other European % % Japan , % 17, % South Korea , % 31, % China 2,454 80, % 40, % Brazil 163 3, % 2, % India % % Indonesia % % Malaysia % % Philippines 83 4, % 2, % Singapore % % Taiwan 40 1, % % USA 124 1, % 1, % Vietnam 181 1, % 1, % Others % % Rest of World 1,269 14, % 10, % World Total 6, , % 108, % Source: Sea Europe, Shipbuilding Market Monitoring

57 Shipbuilding, maintenance and equipment At the end of 2014, more than half of the new order ships refer to solid bulk load ships (54.1%), immediately followed by new orders tanks for the transport of crude oil (19.5%). Table 25: New Orders by Ship types 2014 Types NO GT CGT DWT % DWT Crude Oil Tanker ,395 4,198 23, % Oil Products Tanker 64 1, , % Chemical Tanker 186 3,164 2,497 4, % Tankers ,591 7,349 30, % Bulk Dry ,336 14,765 64, % Bulk Dry / Oil % Other Bulk Dry % Bulk Carriers ,565 14,930 64, % General Cargo 164 1,431 1,233 2, % Container ,035 5,724 12, % Refrigerated Cargo % Ro-Ro Cargo 48 1, % Other Dry Cargo % Dry Cargoes ,429 8,168 15, % LNG Tanker 74 7,624 5,961 5, % LPG Tanker 102 3,017 2,106 3, % Gastankers ,641 8,067 9, % Passenger/Ro-Ro Cargo % Passenger (Cruise) 15 1,806 1, % Other Passenger Vessels/Ferries % Ferries / Passenger Ships 83 2,147 2, % Fish Catching % Other Fishing % Offshore Supply , % Other Offshore 118 1,363 1, % Research % Towing / Pushing % Dredging % Other Activities % Other Non Cargo Vessels 956 2,858 4, % Total 2,744 83,230 45, , % Source: Sea Europe, Shipbuilding Market Monitoring

58 Shipbuilding, maintenance and equipment Table 26: New Orders by Country 2014 Country NO GT % CGT % Croatia % % Germany % % Italy % % Netherlands % % Poland % % Romania % % Spain % % Other EU % % EU , % 3, % Norway % % Russia % % Turkey % % Other European % % Japan , % 10, % South Korea , % 12, % China 1,130 32, % 16, % Brazil % % India % % Indonesia % % Malaysia % % Philippines 38 1, % % Singapore % % Taiwan % % USA % % Vietnam % % Others % % Rest of World 390 2, % 2, % World Total 2,744 83, % 45, % Source: Sea Europe, Shipbuilding Market Monitoring

59 Shipbuilding, maintenance and equipment At the end of 2014, 52.7% of completed ships worldwide were related to transport dry bulk ships, 20% of completed ships refer to container carriers, and 12.1% for transport tanks of crude oil. Table 27: Completions by Ship types 2014 Types NO GT CGT DWT % DWT Crude Oil Tanker 50 5,611 1,750 10, % Oil Products Tanker % Chemical Tanker 162 3,282 2,079 5, % Other Liquids % Tankers 332 9,479 4,395 16, % Bulk Dry ,592 10,992 46, % Bulk Dry / Oil % Self-Discharging Bulk Dry % Other Bulk Dry % Bulk Carriers ,200 11,331 47, % General Cargo 179 1,358 1,238 1, % Container ,414 7,887 17, % Refrigerated Cargo % Ro-Ro Cargo 86 1,810 1, % Other Dry Cargo % Dry Cargoes ,754 10,383 20, % LNG Tanker 30 3,258 2,548 2, % LPG Tanker % Gastankers 83 4,010 3,212 3, % Passenger/Ro-Ro Cargo % Passenger (Cruise) % Other Passenger Vessels/Ferries % Ferries / Passenger Ships , % Fish Catching % Other Fishing % Offshore Supply , % Other Offshore 116 2,328 2, % Research % Towing / Pushing % Dredging % Other Activities % Other Non Cargo Vessels 1,331 4,230 6, % Total 2,950 64,607 36,450 88, % Source: Sea Europe, Shipbuilding Market Monitoring

60 Shipbuilding, maintenance and equipment In 2014, Asia (China, South Korea and Japan), completed more than 80% of the production of ships in that year (32.7%, 31.8% and 18.6% respectively). In the European Union 28 + Norway finished only 6% of all finished ships worldwide. Table 28: Completions by Countries 2014 Country NO GT % CGT % Croatia % % Germany % % Italy % % Netherlands % % Poland % % Romania % % Spain % % Other EU % % EU , % 1, % Norway % % Russia % % Turkey % % Other % % Other European % % Japan , % 6, % South Korea , % 11, % China , % 11, % Brazil % % India % % Indonesia % % Malaysia % % Philippines 45 1, % % Singapore % % Taiwan % % USA % % Vietnam % % Others % % Rest of World 828 3, % 3, % World Total 2,950 64, % 36, % Source: Sea Europe, Shipbuilding Market Monitoring 2014 Ranking included in the economy of the sea map. 60

61 Shipbuilding, maintenance and equipment The ship production capacity has drastically reduced in Europe 28 + Norway, but has increased exponentially in China. In Asia, countries like Japan and South Korea that have seen an increase of ship production capacity between 2002 and 2008; since 2008, there has been a decline in the same production capacity. Figure 13: Completions in global shipyards (in CGT) EU 28 + Norway Japan South Korea China Others Source: Sea Europe, Shipbuilding Market Monitoring

62 Shipbuilding, maintenance and equipment China, India, Bangladesh and Pakistan were the locations where there was the most dismantling of bulk volume ships. India was the country that dismantled most container ships. Pakistan was the country that dismantled most tankers. Table 29: Tonnage reported sold for demolition, major vessel types and countries where demolished, 2013 (Thousands of GT) China India Bangladesh Pakistan Others Indian subcontinent Turkey Others World total Oil tankers , ,844 Bulk carriers 3,524 2,934 4,222 1, ,665 General cargo ,211 Containerships 795 3, ,223 Gas carriers Chemical tankers Offshore ,429 Ferries and passenger ships Other Total 6,124 8,409 6,506 5, ,336 29,052 Note: Propelled seagoing merchant vessels of 100 GT and above. Source: UNCTAD - Review of Maritime Transport

63 63

64 64

65 Offshore energy 65

66 Offshore energy In 2004, after the Middle East and North America and, Europe was the third largest oil and natural gas producing region of the world. By 2014, Europe had been relegated to 4th place; the Middle East continued to lead production, followed by South then North America. Table 30: Total onshore and offshore proved reserves of Oil by country At end 2004 Thousand million barrels At end 2013 Thousand million barrels At end 2014 Thousand million barrels Share of the world total US % Canada % Mexico % Total North America % Brazil % Ecuador % Venezuela % Other S. & Cent. America % Total S. & Cent. America % Azerbaijan % Kazakhstan % Norway % Russian Federation % United Kingdom % Other Europe & Eurasia % Total Europe & Eurasia % Iran % Iraq % Kuwait % Oman % Qatar % Saudi Arabia % United Arab Emirates % Yemen % Other Middle East % Total Middle East % Algeria % Angola % Egypt % Libya % Nigeria % South Sudan % Other Africa % Total Africa % Australia % China % India % Indonesia % Malaysia % Vietnam % Other Asia Pacific % Total Asia Pacific % Total World 1, , , % Source: BP Statistical Review

67 Offshore energy In 2014, more than half of the world's proven gas reserves belonged to Iran and the Russian Federation. Table 31: Total proved reserves of natural gas by country At end 2004 Trillion cubic metres At end 2013 Trillion cubic metres At end 2014 Trillion cubic metres US Other North America Total North America Venezuela Other S. & Cent. America Total S. & Cent. America Russian Federation Turkmenistan Other Europe & Eurasia Total Europe & Eurasia Iran Iraq Qatar Saudi Arabia United Arab Emirates Other Middle East Total Middle East Algeria Nigeria Other Africa Total Africa Australia China Other Asia Pacific Total Asia Pacific Total World Source: BP Statistical Review

68 Offshore energy Since late 2014, the price of a barrel of Brent oil has been below 100 USD; in mid 2015, the price was slightly above 50 USD. The oil price decline has put pressure on the profitability of offshore operations, which are more expensive than onshore operations. Table 32: Evolution of the Brent s price in the last 5 years Figure 14: Evolution of the Brent s price in the last 5 years USD Date Price in USD Date Price in USD Date Price in USD Date Price in USD , Source: Bloomberg Note: The price corresponds to the last working day of the month

69 Offshore energy From 2010 to 2014 the top 3 countries in offshore oil and gas production were Norway, Qatar and Saudi Arabia. Table 33: Offshore Oil & Gas Production (Million kbbl/d) Country Total Norway 3, , , , , ,113.2 Qatar 3, , , , , ,050.8 Saudi Arabia 3, , , , , ,995.0 Mexico 2, , , , , ,432.1 Iran 2, , , , , ,427.6 United States 2, , , , , ,502.9 Brazil 2, , , , , ,749.5 Nigeria 2, , , , , ,041.8 Angola 1, , , , , ,311.2 United Kingdom 2, , , , , ,771.2 UAE 1, , , , , ,471.6 Malaysia 1, , , , , ,459.0 Azerbaijan 1, , , , , ,083.0 Australia 1, , , , , ,800.2 Indonesia 1, , , , , ,546.0 China 1, , ,940.4 India 1, , ,766.8 Egypt 1, , , ,734.4 Venezuela ,086.0 Trinidad and Tobago ,666.0 Thailand ,455.6 Russia ,932.9 Vietnam ,479.6 Equatorial Guinea ,294.1 Netherlands ,727.5 Other Countries 3, , , , , ,046.3 Total 44, , , , , ,884.4 Source: FLAD and Rystad Energy Ranking included in the economy of the sea map. 69

70 Offshore energy Offshore wind power capacity in the world is led by four European countries (UK, Denmark, Germany and Belgium), representing 85.9% of total installed capacity in the world. Fifth, China represents 7.5% of capacity. Table 34: Global cumulative offshore wind capacity in 2014 Total 2011 Total 2012 Total 2013 Total 2014 (MW) Share of the total UK 2,094 2,948 3,681 4, % Denmark ,271 1, % Germany , % Belgium % PR China % Netherlands % Sweden % Japan % Finland % Ireland % Korea % Spain % Norway % Portugal % USA % Total 4,119 5,415 7,047 8, % Source: Global Wind Report Market update 2014 Figure 15: Global cumulative offshore wind capacity in 2014 MW Cumulative Capacity 2013 Cumulative Capacity 2014 Ranking included in the economy of the sea map. Figure 16: Annual cumulative capacity ( ) MW 0 4,119 5,415 7,047 8,

Non-EU 49% EU 51% Source: 2014 JRC Ocean Energy Status Report 71")

71 Offshore energy Figure 17: Distribution of tidal companies in the world (2014) Non-EU 49% EU 51% Source: 2014 JRC Ocean Energy Status Report 71

72 72

73 Naval security power, piracy and maritime disasters (oil spills) 73

74 Naval security power, piracy and maritime disasters (oil spills) In 2015, the country with the largest navy fleet (aircraft carriers, frigates, destroyers, corvettes and submarines) is the US with 164, closely followed by China with 163. Russia is the third with 146 large naval craft. Table 35: Total Naval Ship Power by Countries, 2015 (Sum of the number Aircraft Carriers, Frigates, Destroyers, Corvettes and Submarines) Top 25 Year 2015 Total (Aircraft Carriers + Frigates + Destroyers + Corvettes + Submarines) 1 USA China Russia North Korea 76 5 India 66 6 Japan 61 7 Republic of Korea 55 8 Iran 41 9 Turkey France Indonesia Italy UK Taiwan Greece Brazil Germany Australia Egypt Vietnam Peru Thailand Pakistan Singapore Canada 17 Source: Global Firepower September 2015 Ranking included in the economy of the sea map. 74

75 Naval security power, piracy and maritime disasters (oil spills) Somalia, Nigeria and Indonesia are countries with greatest incidence of attacks in the period Table 36: Locations of actual and attempted attacks ( ) Locations Total Indonesia South East Asia Malaysia Singapore Straits Other Asia South China Sea Far East Vietnam Other Far East Indian Sub Continent Bangladesh India Brazil Colombia Ecuador South America Guyana Haiti Peru Venezuela Other South America Benin Egypt Guinea Gulf of Aden a Ivory Coast Africa Nigeria Red Sea a Somalia a Togo The Congo Other Africa Rest of the World Total ,690 Source: ICC International Maritime Bureau - Piracy and Armed Robbery Against Ships All Incidents with a above are attributed to Somali pirates Ranking included in the economy of the sea map. 75

76 Naval security power, piracy and maritime disasters (oil spills) Between 2010 and 2014, there was a downward trend of pirate attacks at sea. Of the 1690 attacks recorded between 2010 and 2014, only 317 did not have more serious consequences. In 931 cases, the pirates managed to board ships. In 159 of the attacks, there were abductions of people. Table 37: Comparisons of the type of attacks ( ) Category Total Attempted Boarded Fired upon Hijack Total ,690 Source: ICC International Maritime Bureau - Piracy and Armed Robbery Against Ships Between 2010 and 2013, there was a reduction in the level of violence of attacks on ships' crews and, between 2013 and 2014, the level of violence increased again. Between 2010 and 2014, about 3,670 people were subjected to maritime piracy attacks, more than 3,300 were taken hostage and 27 were killed. Table 38: Types of violence to crew ( ) Types of Violence Total Assaulted Hostage 1, ,307 Injured Kidnap/Ransom Killed Missing Threatened Total 1, ,679 Source: ICC International Maritime Bureau - Piracy and Armed Robbery Against Ships 76

77 Naval security power, piracy and maritime disasters (oil spills) In 2014, the types of ships that were the target of pirate attacks were transport ships of chemicals and bulk products. Table 39: Types of vessels attacked ( ) Type Total Bulk Carrier Container General Cargo Tanker Chem / Product Tanker Crude Oil Trawler/Fishing Tug Other Total at year end ,690 Source: ICC International Maritime Bureau - Piracy and Armed Robbery Against Ships Of the 245 ships attacked in 2014, 44 were sailing under the flag of Panama, 36 of The Marshall Islands and 32 of Singapore. Table 40: Nationalities of ships attacked ( ) Flag State Total Antigua Barbuda Bahamas Hong Kong (SAR) Liberia Malaysia Malta Marshall Islands Panama Singapore Other Total year end ,690 Source: ICC International Maritime Bureau - Piracy and Armed Robbery Against Ships 77

78 Naval security power, piracy and maritime disasters (oil spills) Accidents involving oil spills have been occurring over time, all over the world. Table 41: Location of major shipping oil spills (Since 1967) Top 20 Shipname Year Location Spill size (thousand tonnes) 1 Atlantic Empress 1979 Off Tobago, West Indies ABT Summer nautical miles off Angola Castillo de Bellver 1983 Off Saldanha Bay, South Africa Amoco Cadiz 1978 Off Brittany, France Haven 1991 Genoa, Italy Odyssey nautical miles off Nova Scotia, Canada Torrey Canyon 1967 Scilly Isles, UK Sea Star 1972 Gulf of Oman Irenes Serenidade 1980 Navarino Bay, Greece Urquiola 1976 La Coruna, Spain Hawaiian Patriot nautical miles off Honolulu Independenta 1979 Bosphorus, Turkey Jakob Maersk 1975 Oporto, Portugal Braer 1993 Shetland Islands, UK Aegean Sea 1992 La Coruna, Spain Sea Empress 1996 Milford Haven, UK Khark nautical miles off Atlantic coast of Morocco Nova 1985 Off Kharg Island, Gulf of Iran Katina P 1992 Off Maputo, Mozambique Prestige 2002 Off Galicia, Spain 63 Source: ITOPF Oil Tanker Spill Statistics 2014 Table 42: Other relevant offshore spills Description Year Location 1 Deepwater Horizon 2010 Mexican Gulf 2 Ixtoc 1 Oil Well 1979 Bay of Campeche, Mexico 3 Nowruz Oil Field 1983 Persian Gulf Source: The Telegraph 78

79 79

80 80

81 Fishing and aquaculture 81

82 Fishing and aquaculture Between 2002 and 2012, as the world population has grown, there has been an increase in the consumption of fish and other food products per capita. In 2002, per capita consumption was 16 kg, rising to a per capita consumption of 19.2 kg in This increase in per capita consumption was met by increased production in aquaculture. In 2002, production in onshore and offshore aquaculture reached about 24 and 16.4 million tons, respectively, rising to 41.9 and 24.7 million tons in Fish catches at sea continue to represent the largest contribution to the supply of fish, but have not grown in recent years. Table 43: World fisheries and aquaculture production and utilization Production 1 Note:Data in this section for 2012 are provisional estimates. Source: FAO - The State of the World Fisheries and Aquaculture in (Million tonnes) Inland Capture Aquaculture Total inland Marine Capture Aquaculture Total marine Total capture Total aquaculture TOTAL WORLD FISHERIES UTILIZATION 1 Human consumption Non-food uses Population (billions) Per capita food fish supply (kg) Figure 18: Total Capture, Total Aquaculture and Total World fisheries in million tonnes Total Capture Total Aquaculture Total World Fisheries 82

83 Fishing and aquaculture The top ten countries in terms of fishing, led by China with 17.4% of the catch, represent about 60% of the total global fishing. Table 44: Marine capture fisheries: major producer countries Weight Variation 2012 Ranking Country /2012 (Million tonnes) (Percentage) (Percentage) 1 China % 13.6% 2 Indonesia % 27.0% 3 USA % 4.0% 4 Peru % -20.6% 5 Russian Federation % 31.6% 6 Japan % -21.9% 7 India % 15.1% 8 Chile % -28.8% 9 Vietnam % 46.8% 10 Myanmar % 121.4% 11 Norway % -15.6% 12 Philippines % 4.6% 13 Republic of Korea % 0.7% 14 Thailand % -39.2% 15 Malaysia % 14.7% 16 Mexico % 16.7% 17 Iceland % -27.0% 18 Morocco % 26.3% Total 18 major countries % 3.3% Rest of the world % -9.2% World total % 0.0% Share 18 major countries (percentage) Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Million tonnes Figure 19: Marine capture fisheries: major producer countries Ranking included in the economy of the sea map

84 Fishing and aquaculture The Pacific Ocean is where most of the fishing takes place, representing about 59% of the total. Table 45: Marine capture: major fishing areas Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Weight 2012 Variation 2003/2012 Fishing area name (area code) (Million Tonnes) (Percentage) (Percentage) Atlantic, Northwest (21) % -13.8% Atlantic, Northeast (27) % -21.1% Atlantic, Western Central (31) % -17.4% Atlantic, Eastern Central (34) % 14.3% Mediterranean and Black Sea (37) % -13.3% Atlantic, Southwest (41) % -5.5% Atlantic, Southeast (47) % -10.0% Indian Ocean, Western (51) % 1.9% Indian Ocean, Eastern (57) % 38.7% Pacific, Northwest (61) % 8.0% Pacific, Northeast (67) % 0.0% Pacific, Western Central (71) % 11.5% Pacific, Eastern Central (77) % 9.7% Pacific, Southwest (81) % -17.7% Pacific, Southeast (87) % -21.4% Arctic and Antarctic areas (18,48,58,88) % 25.4% World total % 0.0% Figure 20: Marine capture: major fishing areas Arctic and Antarctic areas (18,48,58,88) Pacific, Southeast (87) Pacific, Southwest (81) Pacific, Eastern Central (77) Pacific, Western Central (71) Pacific, Northeast (67) Pacific, Northwest (61) Indian Ocean, Eastern (57) Indian Ocean, Western (51) Atlantic, Southeast (47) Atlantic, Southwest (41) Mediterranean and Black Sea (37) Atlantic, Eastern Central (34) Atlantic, Western Central (31) Atlantic, Northeast (27) Atlantic, Northwest (21)

85 Fishing and aquaculture The fifteen species most fished represent about 1/3 of all fish caught. Table 46: Marine capture: major species and genera 2012 Ranking Scientific name 1 Engraulis ringens 2 Theragra chalcogramma FAO English name Anchoveta (= Peruvian anchovy) Alaska pollock (= walleye pollock) Note: nei = not elsewhere included. 1 - Catches for single species have been added to those reported for the genus. Source: FAO - The State of the World Fisheries and Aquaculture in Figure 21: Marine capture: major species and genera (Million Tonnes) Weight 2012 Variation 2003/2012 (Percentage) (Percentage) % -24.4% % 13.3% 3 Katsuwonus Pelamis Skipjack tuna % 28.0% 4 Sardinella spp. 1 Sardinellas nei % 14.2% 5 Clupea harengus Atlantic herring % -5.6% 6 Scomber Japonicus Chub mackerel % -13.4% 7 Decapterus spp. 1 Scads nei % 0.2% 8 Thunnus Albacares Yellowfin tuna % -9.8% 9 Engraulis Japonicus Japanese anchovy % -31.8% 10 Trichiurus Lepturus Largehead hairtail % -1.1% 11 Gadus morhua Atlantic cod % 31.3% 12 Sardina Pilchardus European pilchard (= sardine) % -3.1% 13 Mallotus villosus Capelin % -12.0% 14 Dosidicus gigas Jumbo flying squid % 136.4% 15 Scomberomorus spp. 1 Seerfishes nei % 30.3% Total 15 major species and genera % -1.8% Rest of the world % 1.0% World total % 0.0% Share 15 major species and genera (percentage) Million tonnes

86 Fishing and aquaculture Worldwide, the inland freshwater fish catch is also led by China. Table 47: Inland waters capture: major producer countries 2012 Ranking Weight 2012 Variation 2003/2012 Country (Million Tonnes) (Percentage) (Percentage) 1 China % 7.6% 2 India % 92.8% 3 Myanmar % 329.6% 4 Bangladesh % 34.9% 5 Cambodia % 45.4% 6 Uganda % 68.6% 7 Indonesia % 27.5% 8 United Republic of Tanzania % 4.3% 9 Nigeria % 78.3% 10 Brazil % 16.9% 11 Russian Federation % 37.7% 12 Egypt % -23.5% 13 Thailand % 12.1% 14 Democratic Republic of the Congo % -7.1% 15 Vietnam % -2.6% Total 15 major countries % 40.2% Rest of the world % 18.3% World total % 35.1% Share 15 major countries (percentage) Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Figure 22: Inland waters capture: major producer countries in 2012 (in percentage of the total) China India Myanmar Bangladesh Cambodia Uganda Indonesia United Republic of Tanzania Nigeria Brazil Russian Federation Egypt Thailand Democratic Republic of Congo Vietnam Rest of the world 86

87 Fishing and aquaculture In 2012, 88% of world aquaculture was in Asia, and was responsible for the significant growth of aquaculture globally. Table 48: Aquaculture production by region: quantity of world total production Weight Selected groups and countries Variation 2000/2012 (Million Tonnes) (Percentage) (Percentage) Africa % 272% North Africa % 200% Sub-Saharan Africa % 716% Americas % 124% Caribbean % -28% Latin America % 221% North America % 2% Asia % 107% China % 91% Central and Western Asia % 153% Southern and Eastern Asia (excluding China) % 158% Europe % 40% European Union (28) % -10% Other European countries % 149% Oceania % 52% World % 106% Notes: Data exclude aquatic plants and non-food products. Data for 2012 for some countries are provisional and subject to revisions. For the purpose of this table, Cyprus, classified as part of Asia by FAO, is included under Europe as one of the 28 members of European Union (Member Organization). Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Figure 23: Aquaculture production by region: quantity of world total production (in million tonnes), 2000 and 2012 Figure 24: Aquaculture production by region: quantity of world total production (weight in percentage), Africa Americas Asia Europe Oceania Africa Americas Asia Europe Oceania 87

88 Fishing and aquaculture Onshore aquaculture is the main contributor to the growth of aquaculture and China represents 61.7% of global aquaculture production. Table 49: Farmed food fish production by top 15 producers and main groups of farmed species in 2012 Producer Finfish Inland aquaculture Mariculture a Other speciesª National total Share in world total (Million Tonnes) (Million Tonnes) (Percentage) China % India % Vietnam % Indonesia % Bangladesh % Norway % Thailand % Chile % Egypt % Myanmar % Philippines % Brazil % Japan % Republic of Korea % USA % Top 15 subtotal % Rest of the world % World % Note: The symbol means the production data are not available or the production volume is regarded as negligibly low. a Other species includes crustaceans, molluscs and other species. Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Figure 25: Farmed food fish production share of the top 15 producers in 2012 (in percentage of the total) China India Vietnam Indonesia Bangladesh Norway Thailand Chile Egypt Myanmar Philippines Brazil Japan Republic of Korea USA Rest of the world Ranking included in the economy of the sea map. 88

89 Fishing and aquaculture Asia is responsible for the production of more than 90% of aquaculture algae. Table 50: Aquaculture production of farmed aquatic plants in the world and selected major producers Weight Variation /2012 (Million Tonnes) (Percentage) (Percentage) China % 84.9% Indonesia % % Philippines % 147.7% Republic of Korea % 173.0% Japan % -16.7% Malaysia % % Zanzibar (Tanzania) % 202.3% Solomon Islands % Subtotal % 161.4% Rest of the world % 48.1% World % 155.5% Notes: The Democratic People s Republic of Korea and Vietnam are among the major producers of farmed seaweeds. They are not listed separately in this table due to the unavailability of reliable statistics data. Instead, they are included in Rest of world.... = data not available. Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Figure 26: Aquaculture production of farmed aquatic plants in the world per country (in million tonnes), 2000 and 2012 Figure 27: Aquaculture production of farmed aquatic plants in the world and selected major producers (Weight in percentage), China Indonesia Philippines Republic of Korea Japan Malaysia Zanzibar (Tanzania) Solomon Islands 89

90 Fishing and aquaculture In 2012, Asian fishermen and aquaculture producers represented 84% of employment in this sector. In addition to the growth registered in Asia (23.7%) between 2000 and 2012, there was growth in Africa (41%), in Latin America (26.9%) and a decrease in Europe (-16.9%). Table 51: World fishers and fish farmers by region Weight 2012 Variation 2000/2012 (Thousands) (Percentage) (Percentage) Africa 4,175 5,027 5, % 41.0% Asia 39,646 49,345 49, % 23.7% Europe % -16.9% Latin America and the Caribbean 1,774 2,185 2, % 26.9% North America % -6.6% Oceania % 0.8% World 46,845 57,667 58, % 24.4% Of which, fish farmers Africa % 227.5% Asia 12,211 17,915 18, % 48.8% Europe % 0.0% Latin America and the Caribbean % 25.7% North America % 50.0% Oceania % 20.0% World 12,632 18,512 18, % 49.3% Notes: Some statistics provided to FAO by national offices, in particular those for , are provisional and may be amended in future editions, and in other FAO publications. Source: FAO - The State of the World Fisheries and Aquaculture in 2014 Figure 28: World fishers and fish farmers by region Africa Asia Europe Latin America and the Caribbean North America Oceania 90

91 Fishing and aquaculture In 2012, 72% of motorised fishing ships were in Asia. Figure 29: Distribution of motorized fishing vessels by region in 2012 Asia 72% Latin America and the Caribbean 9% Africa 6% Europe 4% North America 4% Near East 4% Pacific and Oceania 1% Source: FAO - The State of the World Fisheries and Aquaculture in

92 Fishing and aquaculture From 1974 to 2011, there has been a significant increase in the pressure on fish stocks, causing overfishing - or at the limit of what is acceptable - of a number of species. Figure 30: Global trends in the state of world marine fish stocks, Percentage of stocks assessed At biologically unsustainable levels Within biologically sustainable levels Source: FAO - The State of the World Fisheries and Aquaculture in

93 Fishing and aquaculture China is currently the greatest exporter of food products from the sea, while Japan is the most importer country. Table 52: Top ten exporters and importers of fish and fishery products Annual Growth (US$ millions) (%) Exporters China 4,485 18, % Norway 3,569 8, % Thailand 3,698 8, % Vietnam 2,037 6, % USA 3,260 5, % Chile 1,867 4, % Canada 3,044 4, % Denmark 2,872 4, % Spain 1,889 3, % Netherlands 1,803 3, % Top ten subtotal 28,525 67, % Rest of the World total 29,776 61, % World total 58, , % Importers Japan 13,646 17, % USA 10,634 17, % China 2,198 7, % Spain 3,853 6, % France 3,207 6, % Italy 2,906 5, % Germany 2,420 5, % United Kingdom 2,328 4, % Republic of Korea 1,874 3, % China, Hong Kong SAR 1,766 3, % Top ten subtotal 44,830 77, % Rest of the world total 17,323 51, % World total 62, , % Source: FAO - The State of the World Fisheries and Aquaculture in

94 Fishing and aquaculture Africa and Latin America are the regions of the world with the lowest per capita consumption of fish and other sea products. Table 53: Per capita food fish supply by continent and economic grouping in 2010 Per capita sea food supply (kg/year) World 18.9 World (excluding China) 15.4 Africa 9.7 North America 21.8 Latin America and the Caribbean 9.7 Asia 21.6 Europe 22.0 Oceania 25.4 Industrialized countries 27.4 Other developed countries 13.5 Least-developed countries 11.5 Other developing countries 18.9 LIFDCs - Low-income food-deficit countries Source: FAO - The State of the World Fisheries and Aquaculture in

95 Fishing and aquaculture Since 1970, aquaculture has increased its relative importance in the supply of food from the sea, reaching a similar weight to the fisheries in Figure 31: Relative contribution of aquaculture and capture fisheries to food fish consumption Percentage of fishery food supply (kg/capita) Aquaculture Capture Source: FAO - The State of the World Fisheries and Aquaculture in

96 96

97 Entertainment, sports, tourism and culture 97

98 Entertainment, sports, tourism and culture Gross revenue associated with the cruise ship activity has been increasing. Figure 32: Revenue of the cruise industry worldwide from 2008 to 2014 (in billion U.S. dollars) Revenue in billion U.S. dollars ª 2011ª 2012ª 2013ª 2014 Source: Cruise industry - Statista Dossier a Forecast 98

99 Entertainment, sports, tourism and culture North America and Europe are the most important markets for cruise ships. Figure 33: Market size of the global cruise industry in 2014, by region (in billion U.S. dollars) Market size in billion U.S. dollars North America Europe Asia 1.80 South America 1.27 Australia and New Zealand 1.13 Middle East and Africa 0.07 Source: Cruise industry - Statista Dossier 99

100 Entertainment, sports, tourism and culture The Caribbean still holds the largest market share in the business of cruise ships, closely followed by the Mediterranean and the rest of Europe Between 2013 and 2014, the Caribbean and Europe (excluding the Mediterranean) enjoyed an increase in their overall market share in this business, while the Mediterranean region saw a reduction in its market share from 21.7% to 18. 9%. Figure 34: Global cruise industry deployment market share in 2013 and 2014, by region % 35% 34.4% 37.3% 30% Market share 25% 20% 15% 10.9% 11.1% 21.7% 18.9% 15.8% 14.5% 10% 5% 4.8% 4.5% 3.9% 3.3% 4.4% 3.4% 5.9% 5.0% 0% Alaska Caribbean South America Europe Mediterranean Asia Australasia Other markets (without Mediterranean) Source: Cruise industry - Statista Dossier Ranking included in the economy of the sea map. 100

101 Entertainment, sports, tourism and culture The number of people participating in cruise travel has increased. Figure 35: Number of cruise passengers worldwide from 2005 to 2013 (in millions) Number of passengers in millions Source: Cruise industry - Statista Dossier 101

102 Entertainment, sports, tourism and culture The largest cruise consumers are North Americans, immediately followed by the British and the Irish. Figure 36: Leading passenger source countries in the global cruise industry in 2013 Global passenger share 0% 10% 20% 30% 40% 50% 60% United States 51.7% UK & Ireland Germany 8.1% 7.7% Italy Australia Canada Brazil Spain France Scandinavia & Finland 4.0% 3.6% 3.4% 3.4% 2.8% 2.4% 1.6% Source: Cruise industry - Statista Dossier 102

103 Entertainment, sports, tourism and culture The cruise industry has been increasing its overall capacity. Figure 37: Passenger capacity of the global cruise industry from 2007 to 2014 (in thousands) 600 Passenger capacity in thousands Source: Cruise industry - Statista Dossier 103

104 Entertainment, sports, tourism and culture By the end of 2014, in terms of business volume, the three biggest companies involved in cruise line activity have their headquarters in Miami (USA). The fourth largest company is headquartered in the UK. Figure 38: Leading cruise line companies headquarters location worldwide in 2014, by revenue (in billion U.S. dollars) Revenue in billion U.S. dollars Miami, USA Miami, USA 8.07 Miami, USA 3.13 a Geneva, CH a Miami, USA a Luton, UK a Kowloon, HK a / b Tromsø, Norway a Los Angeles, USA a Monaco a Via Cruise Market Watch b Figure was converted from Norwegian krone to U.S. dollars (exchange rate of 1 krone = 0.17 U.S. dollars was used). Source: Cruise industry - Statista Dossier 104

105 Entertainment, sports, tourism and culture In 2013, in a comparison of the "accommodation" on cruises, the ranking of the world's largest companies are headquartered in the US, UK, Italy and the Netherlands. Figure 39: Leading cruise lines headquarters location worldwide in 2013, by number of lower berths Lower berths Miami, USA Miami, USA 61,941 59,882 Los Angeles, USA Genoa, IT 37,374 40,070 Miami, USA Geneva, CH 30,500 30,100 Miami, USA Seattle, USA 25,034 23,541 Miami, USA Southampton, UK 8,505 6,672 Source: Cruise industry - Statista Dossier 105

106 Entertainment, sports, tourism and culture The USA, Australia, New Zealand, Italy, France and the UK are the countries of reference in terms of the recreational boating and marinas business. According to ten 2014 edition of Pleasure Boat International Resource Guide Published by the National USA Marine Manufacturers Association, the USA exports of recreational marine craft and accessories totaled USD 2.3 billion in The United States is also a net exporter in this industry, exporting USD 446 million more than it imported. The U.S. recreational marine market makes up approximately 75 percent of the entire world market for these products. Table 54: US Exports Top 20 Markets by FAS Value Recreational Marine Craft, Parts, and Accessories, as defined by the Harmonized Tariff System. Top 20 Markets by FAS Value (Annual + Year-To-Date Data from January October, USD Thousands) Country YTD 2013 YTD Change YTD Canada 477, , , , , , % Australia 116, , , , , , % Mexico 76,527 97,573 84, ,357 92,289 80, % Belgium 81, ,003 92, ,472 93,319 97, % Brazil 37,789 66,131 72,240 84,255 65,144 58, % Japan 25,826 25,055 35,088 61,033 49,111 36, % Italy 85,007 92,861 70,197 53,814 50,244 51, % Germany 46,248 54,879 51,137 49,880 43,518 37, % UAE 47,409 38,627 29,916 45,905 33,145 29, % Venezuela 30,261 32,992 34,544 41,126 32,344 22, % Costa Rica 26,820 31,653 33,560 40,027 10,323 8, % China 13,029 24,104 36,860 37,369 34,796 37, % Argentina 10,789 28,867 24,504 36,275 23,346 22, % New Zealand 15,463 19,132 24,288 35,849 17,022 22, % Netherlands 46,917 49,105 57,220 35,664 31,003 27, % Sint Maarten N ,626 33,099 27,821 17, % Russia 14,033 12,862 17,974 30,673 29,770 24, % Spain 27,260 34,587 41,467 29,616 25,722 40, % UK 56,101 44,969 38,645 29,589 25,696 19, % France 30,606 34,192 29,383 26,671 23,972 23, % Subtotal 1,265,785 1,634,388 1,674,388 1,777,643 1,452,929 1,432, % All Other 507, , , , , , % World Total 1,773,592 2,193,815 2,193,024 2,270,404 1,838,996 1,802, % Source: Pleasure boat International Resource Guide, A Reference for U.S. Exporters, 2014 Edition 106

107 Entertainment, sports, tourism and culture USA marina industry According to the National Maritime Manufacturers Association (NMMA), there are more than 10,000 marinas in the United States of America. In the state of Florida alone there are more than 2,200 marinas, which is a number that is higher than the number of marinas in several other well-known recreational boat countries. Nationwide, the number of berths available in the marina industry is estimated to be over 1.1 million. The marina industry is a sound contributor to the US employment statistics, it is believed that for each 100 berths there are 3 jobs created, which results in a total of 32,000 full-time workers in the whole country. (In marinamanagement December 2001) 107