City and County of San Francisco

|

|

|

- Francine Blankenship

- 6 years ago

- Views:

Transcription

1 City and County of San Francisco Office of the Controller City Services Auditor AIRPORT COMMISSION: Administration of the SFO Shuttle Bus Company Contract Needs to Be Significantly Improved October 25, 2010

2 CONTROLLER S OFFICE CITY SERVICES AUDITOR The City Services Auditor was created within the Controller s Office through an amendment to the City Charter that was approved by voters in November Under Appendix F to the City Charter, the City Services Auditor has broad authority for: Reporting on the level and effectiveness of San Francisco s public services and benchmarking the city to other public agencies and jurisdictions. Conducting financial and performance audits of city departments, contractors, and functions to assess efficiency and effectiveness of processes and services. Operating a whistleblower hotline and website and investigating reports of waste, fraud, and abuse of city resources. Ensuring the financial integrity and improving the overall performance and efficiency of city government. The audits unit conducts financial audits, attestation engagements, and performance audits. Financial audits address the financial integrity of both city departments and contractors and provide reasonable assurance about whether financial statements are presented fairly in all material aspects in conformity with generally accepted accounting principles. Attestation engagements examine, review, or perform procedures on a broad range of subjects such as internal controls; compliance with requirements of specified laws, regulations, rules, contracts, or grants; and the reliability of performance measures. Performance audits focus primarily on assessment of city services and processes, providing recommendations to improve department operations. We conduct our audits in accordance with the Government Auditing Standards published by the U.S. Government Accountability Office (GAO). These standards require: Independence of audit staff and the audit organization. Objectivity of the auditors performing the work. Competent staff, including continuing professional education. Quality control procedures to provide reasonable assurance of compliance with the auditing standards. Audit Team: Helen Storrs, Audit Manager Donna Crume, Associate Auditor Renato Lim, Associate Auditor

complied with contract terms and conditions in providing shuttle bus services to the San")

3 City and County of San Francisco Office of the Controller City Services Auditor Airport Commission: Administration of the SFO Shuttle Bus Company Contract Needs to Be Significantly Improved October 25, 2010 Purpose of the Audit The purpose of this audit was to determine if SFO Shuttle Bus Company (Shuttle) complied with contract terms and conditions in providing shuttle bus services to the San Francisco International Airport (Airport), and to evaluate the extent to which the Airport provided sufficient contract administration in accordance with contract provisions. The audit period covered the time from January 1, 2007, through January 31, Highlights Shuttle has been providing bus service to the Airport since the inception of the contract in During the audit period, January 1, 2007, through January 31, 2009, the Airport reimbursed Shuttle a total of $15,563,391 for claimed service costs. The audit found the Airport needs to reform the contract; the current contract language is unclear and the contract s basic provisions reflect multiple contract types. These deficiencies contributed to weaknesses in the Airport s administration of the contract, which resulted in overpayments and questioned costs. The Airport: Paid Shuttle two profits during the audit period, for a total of $518,516. One of these profits was considered an additional management profit and was based on a verbal agreement. Is not reflected as a secured party in the financing agreement for the seven buses that Shuttle was directed to purchase, which exposes the Airport to financial loss. Directed Shuttle to provide baggage handling services and did not modify the contract to reflect this service enhancement. Reimbursed Shuttle for administrative costs totaling $270,037 based on a budgeted amount instead of actual costs incurred. Approved a $1.60 per service hour supplemental charge for unanticipated health expenses in 2007 that resulted in approximately $122,174 in payments to Shuttle. The hourly charge was in addition to a $24,662 payment for additional 2007 health benefit costs in May 2008, resulting in potential overpayments. Recommendations The audit report includes 28 recommendations for the Airport to improve the language and administration of the shuttle bus service contract, and to provide direction to Shuttle in order to strengthen inventory controls and compliance with contract terms and conditions. The Airport should: Clarify the contract type and include language limiting cost reimbursement to those that are necessary and reasonable for providing shuttle service. Replace the term guaranteed profit with an appropriate term, consistent with the contract type, and consider establishing a performance-based fee to address significant changes in service hours. Direct Shuttle to modify the current bus purchase financing agreement to include the Airport as a secured party. Execute formal contract modifications when adding services and programs to the contract. Direct Shuttle to revise the 2007 health cost reconciliation to reflect the $122,174 in payments for the unanticipated health expense supplemental charge; review all amounts paid and collect any overcharges. Copies of the full report may be obtained at: Controller s Office City Hall, Room Dr. Carlton B. Goodlett Place San Francisco, CA or on the Internet at

4 Page intentionally left blank.

5 CITY AND COUNTY OF SAN FRANCISCO OFFICE OF THE CONTROLLER Ben Rosenfield Controller Monique Zmuda Deputy Controller October 25, 2010 San Francisco Airport Commission John L. Martin P.O. Box 8097 Airport Director San Francisco International Airport P.O. Box 8097 San Francisco, CA San Francisco International Airport San Francisco, CA President and Members, and Mr. Martin: The Controller's Office, City Services Auditor (CSA), presents its audit report on the shuttle bus services contract between the City and County of San Francisco (City) and SFO Shuttle Bus Company (Shuttle). The objectives of the audit were to evaluate Shuttle s compliance with the terms and conditions of the contract, and to determine whether the administration of the contract by San Francisco International Airport (Airport) was adequate. The audit found that the Airport reimbursed Shuttle a total of $15,563,391 for claimed service costs during the January 1, 2007, through January 31, 2009, period covered by the audit. The audit team identified significant concerns regarding some of the amounts paid, which resulted from weaknesses in the contract s commercial terms and in the Airport s administration of the agreement. This report includes recommendations to modify the contract with Shuttle to better define key commercial terms, so that the agreement is more consistent with sound business practices and can be more appropriately administered. CSA found that Shuttle was generally in compliance with the contract s terms and conditions as currently written. However, the audit team found that Shuttle needs to better safeguard parts and tire inventories by improving controls over its inventory system and by providing for proper segregation of the purchasing and receiving duties. The audit report includes 28 recommendations for the Airport to improve contract language and better administer the contract. The Airport s response to the audit report is attached as Appendix A and Shuttle s response is attached as Appendix B. We appreciate the assistance and cooperation of Airport and Shuttle staff during the audit. Respectfully, Tonia Lediju Director of Audits City Hall 1 Dr. Carlton B. Goodlett Place Room 316 San Francisco CA FAX

6 cc: Mayor Board of Supervisors Budget Analyst Civil Grand Jury Public Library

7 TABLE OF CONTENTS Introduction... 1 Chapter 1 Contract Language Does Not Adequately Define Key Commercial Terms... 5 Finding 1.1 The contract s language does not adequately define key commercial terms... 5 Finding 1.2 The Airport was apparently overcharged for health and welfare costs... 9 Finding 1.3 Shuttle received both a guaranteed profit and additional management profit during the audit period Finding 1.4 Contractual insurance requirements need to be clarified to ensure that Shuttle maintains proper coverage and does not bill the Airport more than required Finding 1.5 Shuttle service performance reporting is not adequate in some respects and is not fully consistent with contract requirements Chapter 2 Improvements in Contract Administration and Monitoring Are Needed to Prevent Loss to the Airport Finding 2.1 The Airport needs to maintain a proper arm s-length business relationship with Shuttle Finding 2.2 The Airport added baggage handling services to the contract s scope of work without modifying the contract Finding 2.3 Shuttle made purchases without competitive solicitations and without ensuring compliance with the City s procurement policies Finding 2.4 The Airport s financial interest in the buses were not adequately protected, because Shuttle and the Airport did not comply with the contract s bus purchase terms Finding 2.5 The process for developing Shuttle s budget may not result in the best financial terms for the Airport... 20

8 Finding 2.6 Current processes for reviewing and approving Shuttle invoices and monitoring contract costs are inadequate and expose the Airport to overpayments Finding 2.7 Significant assets are not reflected in the Airport s fixed asset accounting records Finding 2.8 Weaknesses in Shuttle s tires and bus part inventory controls expose the Airport to loss Finding 2.9 The Airport did not maintain current copies of automobile liability insurance certificates, and neither Shuttle nor the Airport could provide proof of compliance with the contract performance bond requirement for part of the audit period Finding 2.10 Shuttle was unable to locate and provide all requested documents for the audit period Appendix A Airport s Response... A-1 Appendix B Shuttle s Response... B-1 Appendix C Rebuttal to Shuttle s Response... C-1

9 LIST OF ABBREVIATIONS AND ACRONYMS CSA DBA FY OCA City Services Auditor Doing Business As Fiscal Year Office of Contract Administration

10 Page intentionally left blank.

11 INTRODUCTION Audit Authority Background The Airport administers ground transportation services This audit was conducted under the authority of the Charter of the City and County of San Francisco (City), which requires that the Office of the Controller (Controller), City Services Auditor (CSA), conduct periodic, comprehensive financial and performance audits of City departments, services, and activities. Additionally, this audit was conducted pursuant to an audit plan agreed to by the Controller and the Airport. The Operations & Security Division of San Francisco International Airport (Airport) is responsible for managing the airfield, public transportation, terminals, and airport security. Landside Operations, a unit of the Operations and Security Division, oversees the Airport s ground transportation services. Among the Airport s ground transportation services is a 24 hour-a-day, seven day-aweek scheduled shuttle bus service. The service is offered free of charge to passengers, Airport employees, and other users of the Airport. The service offers routes between the Airport terminals and long term parking for airline passengers, and between the Airport terminals and employee parking lots for Airport and airline employees. A fleet of 23 buses is operated to meet service requirements. The Airport s contractor, SFO Shuttle Bus Company (Shuttle), is responsible for bus procurement and fleet maintenance. Contract provisions provide Shuttle with full reimbursement of all costs incurred to procure, maintain, and operate the fleet. The Airport Commission originally awarded the shuttle services contract to Shuttle in May 1996 for 10 years The Airport Commission exercised two one-year options to extend the contract In May 1996, the San Francisco Airport Commission (Commission) awarded a ten-year contract to Shuttle to provide the Airport s shuttle bus service. The original duration of the contract was from January 1, 1998, through December 31, The contract provided the option to the City, at the discretion of the Commission, to extend the duration of the contract for five additional one-year periods. The Commission exercised the first one-year option to extend the contract on October 30, The second oneyear option to extend the contract was approved by the Commission on January 20, 2009, and extended the contract to December 31,

12 Contract compensation Contract compensation is paid monthly based on work performed in the previous month. The Airport Director or authorized representative is expected to verify that Shuttle s monthly billings reflect the costs associated with providing a satisfactory level of service as addressed in the contract. The contract requires a minimum level of 199 hours of daily service with an option, at the direction of the Airport, to provide a maximum of 250 hours of daily service. Labor costs associated with service delivery are compensated using a basic and incremental service rate. The contract does not specify the methodology to be used in determining these rates, and only lists the positions and a corresponding flat hourly labor rate for each. The basic service rate is comprised of the total hourly labor rates, including benefits, for all bus operations and management positions. The incremental service rate excludes supervisory and management positions. The service rates are developed during the preparation of the Proposition J analysis by both Shuttle and the Airport; the resulting rates are reviewed and approved by the Commission annually. Proposition J contracting, taking the name from a proposition in the November 1983 election, authorizes an exception to City Charter Section , which addresses civil service appointment exclusions. This exception allows outside contracting of existing services provided the cost is lower than if performed by civil servants. The Proposition J analysis is designed to provide an annual cost comparison for private service contracts that compares the contract cost to the estimated cost of performing the services using City personnel and resources. The contract also provides for direct reimbursement of the following costs: Bus lease payments Uniforms Fuel, lubricants, and utilities Insurance Bus maintenance Administrative/office costs Unanticipated operational expenditures Guaranteed profit Reimbursements are not limited to Shuttle s monthly 2

13 billings. Administrative/office costs and guaranteed profit are generally billed to the Airport in January of each year. Also, additional payments for labor rate and health and welfare costs increases are authorized by the Commission and billed throughout the year. Exhibit 1 reflects the total payments made by the Airport to Shuttle for services during the audit period. EXHIBIT Airport Payments to SFO Shuttle Bus Company January 1, 2007, Through January 31, 2009 Period Payments January 1, 2007, to June 30, 2007 $3,766,121 July 1, 2007, to June 30, ,013,075 July 1, 2008, to January 31, ,784,195 Total $15,563,391 Source: Airport Accounting. Objectives The objectives of the audit were to determine whether: 1. Internal controls over the administration of the contract by the Airport were adequate. This included contract monitoring, reporting, and invoice review and approval. 2. The contract provisions addressing compensation clearly defined allowable charges. 3. Shuttle complied with contract requirements when billing the Airport, and properly billed the Airport for shuttle service expenses. 4. Shuttle entered into the appropriate lease-purchase agreements when acquiring buses, and properly transferred title to the Airport. 5. Shuttle complied with the shuttle bus service and maintenance provisions of the contract. Scope and Methodology The audit covered the period from January 1, 2007, through January 31, To conduct the audit, the audit team: Reviewed and gained an understanding of the contract 3

14 terms and conditions, and modifications. Interviewed Airport and Shuttle personnel to gain an understanding of the billing, accounting, and contract monitoring procedures. Verified whether shuttle service expenses claimed for reimbursement were: o Allowable under the contract. o Submitted with adequate documentation to support amounts billed. o Properly reviewed by Airport staff prior to payment. o Incurred by Shuttle. Observed shuttle bus and maintenance facility operations. Tested, on a sample basis, whether Shuttle was properly transferring bus titles to the Airport, and whether the Airport reflected these assets in its accounting records. This performance audit was conducted in accordance with generally accepted government auditing standards. These standards require planning and performing the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for the findings and conclusions based on the audit objectives. We believe that the evidence obtained provides a reasonable basis for the findings and conclusions based on the audit objectives. 4

15 CHAPTER 1 Contract Language Does Not Adequately Define Key Commercial Terms Summary Finding 1.1 The auditors found that the basic commercial terms of the contract between the Airport Department (Airport) and SFO Shuttle Bus Company (Shuttle) are poorly constructed and overly broad. The categories of billable costs are not adequately defined, and the contract s language reflects multiple contract types; some terms are consistent with a cost-plus-fee contract, while other provisions are more consistent with time-and-materials and fixed-price contracts 1. These deficiencies in the contract s construction contributed to weaknesses in contract administration and monitoring, resulting in overpayments and questioned costs. The contract s language does not adequately define key commercial terms. Deficiencies in the contract s construction contributed to significant weaknesses in the Airport s administration of the contract. Some terms of the contract reflect a cost-plus-fee agreement, while other aspects are time-and-materials and fixed-price contract provisions, which could lead to potential payment of the same costs under multiple categories. Moreover, the contract contains unclear, overly broad language. Contract weaknesses and resulting overpayments and questioned costs include: Contract terms that provide reimbursement for all costs and additional sums in various categories. An Other rate for unanticipated health and welfare costs included in the overall 2007 service rate, resulting in potential overpayments of approximately $122,174. Administrative and office costs reimbursed based on 1 A cost-plus-fee contract is a cost-reimbursement contract that provides for payment of actual costs and a negotiated fee that is often fixed at the inception of the contract. The fee typically does not vary with actual costs, but can be adjusted as a result of changes to the contract scope of work or, can include a performance-based incentive. A time-and-materials contract provides for acquiring services based on a) direct labor at specified fixed hourly rates for wages, overhead, administrative expenses, and profit, and b) the actual cost of materials. A fixed-price contract provides for a firm price or an adjustable price with a ceiling and/or target price. 5

16 budgeted amounts instead of actual costs. Total payments to Shuttle for administrative and office costs for the audit period were $270,037. Payments for two profits, a guaranteed profit and an additional management profit. Profit payments for the audit period totaled $518,516. The contract s description of reimbursable costs is overly broad and inclusive. The contract provides for an hourly personnel service rate that is consistent with a time-and-materials contract. The contract also includes other terms that provide for reimbursement of all other costs associated with providing shuttle bus service for the Airport; the direct reimbursement of some of these costs is more characteristic of a cost-plusfee contract. Contract Appendix B, Calculation of Charges, describes reimbursable costs as: All expenditures for fuel, lubricants, and utilities. All liability, property, and workman s compensation premiums. All parts and other costs in conjunction with maintaining the buses. All unanticipated operational expenditures authorized by the Director. Additional sums for employee uniforms. Additional sums for demonstrated administrative and other office costs. The auditors also found that the terms all and additional sums imply that there are no limits to the amount of reimbursement that can be claimed by Shuttle. For instance, Shuttle is reimbursed for all expenditures for parts and other costs for bus maintenance; there is no requirement for Shuttle to submit an annual maintenance plan for the Airport s review to determine whether the expenditures are necessary and reasonable to providing shuttle service. There are also no explicit requirements for Shuttle to obtain the best price for parts or to pursue volume discounts for parts and materials used in maintaining the buses. Some costs reimbursed under the unanticipated operational expenditure category appear to be recurring in nature. The contract allows for the reimbursement of all unanticipated expenses, and describes these expenses as costs related to the operation of the system such as, but not limited to, repairs and replacement of bus shelters and signs. The audit team found that costs billed under this 6

17 category included additional annual payments for health and welfare costs, additional annual payments for service rate increases, and the annual payment for additional management profit. Since these expenses are recurring, they are not, by definition, unanticipated. To ensure that the Airport pays the correct amounts for all costs, these expenses should be budgeted and billed in an appropriate category, such as service rates or profit. Multiple provisions for health and welfare costs apparently resulted in overpayments. Administrative and office costs were paid based on budgeted amounts. The Airport annually modifies the contract to allow for additional payments to reflect increases in Shuttle s labor and health and welfare and pension benefit costs that are not reflected in the approved service rate; the additional amounts are billed as unanticipated operational expenses. For 2007, the Airport included an Other rate of $1.60 per service hour for unanticipated health and welfare costs. The total billed amount for this Other rate, which is discussed in detail under Finding 1.2, was approximately $122,174. However, this hourly charge was in addition to a $24,662 payment for additional health and welfare and pension benefit costs approved by the Commission in May It therefore appears that the Airport was overcharged for health and welfare costs. Contract provisions for reimbursement of administrative and office costs provide for additional sums for demonstrated administrative and other office costs. The term demonstrated implies that these expenses have been incurred and paid by Shuttle. However, the Airport reimbursed Shuttle for administrative and office costs based on an annual budgeted lump sum amount. Airport staff confirmed that Shuttle was paid the budgeted amount, and stated that the practice was consistent with Section 7 and Appendix B of the contract. Section 7 of the contract requires the preparation of an annual budget which is submitted to the Commission, and also requires monthly payments based on work performed. Appendix B, Calculation of Charges, details billing rates and other costs. The auditors found that that payment of budgeted amounts for these costs was not consistent with the contract s provisions, and exposed the Airport to excess payments. The contract with Shuttle is not a fixed price contract; therefore, making contract payments based on budgeted amounts is not consistent with Section 7, nor is it a sound business practice. Reimbursement for administrative and office costs needs to be based on actual costs, incurred and paid, which are necessary and reasonable to providing 7

18 shuttle service. For the audit period, Shuttle was paid $270,037 for budgeted administrative and office costs. Contract terms provide Shuttle with an annual guaranteed profit Contract Appendix B, Calculation of Charges, provides for a payment to Shuttle for guaranteed profit of $100,000 on January 1, 1998, and additional sums on January 1st for the remainder of the contract. The term guaranteed profit is unusual and not a sound business practice. A guaranteed profit implies that Shuttle is released from any financial risk associated with performance under the contract. This provides no incentive for Shuttle to control costs or meet performance standards. Further, when service hours increased early in the contract period, the Airport granted Shuttle an additional management profit. This additional profit was based on a verbal agreement, not a contract modification. As a result, Shuttle receives two annual profit payments, a guaranteed and an additional management profit. These profit payments totaled $518,516.for the audit period. As the contract allows for reimbursement for all costs and additional sums, it appears that the contract s compensation terms factor in cost increases associated with a corresponding increase in service hours. Therefore, it is unclear why additional profit payments are necessary. Recommendations The Airport should reform the contract with Shuttle to: 1. Clarify the contract type (i.e. cost-plus-fee or time and materials) and ensure that all contract provisions are consistent with the contract type. 2. Include language limiting the reimbursement of costs to those that are necessary and reasonable and are actually incurred and paid. 3. Provide for payment of indirect or overhead costs instead of the poorly defined administrative/office costs, and adequately define all allowable costs, including health and welfare costs. 4. Replace the term guaranteed profit with an appropriate term that is consistent with the type of contract, such as fixed management fee for a costplus-fee contract. 8

19 Finding 1.2 The Airport was apparently overcharged for health and welfare costs. The multiple provisions for health and welfare costs apparently resulted in overpayments. As discussed under Finding 1.1, the 2007 service rates included an hourly charge of $1.60 per service hour for unanticipated health and welfare 2 costs, which resulted in approximately $122,174 in additional payments to Shuttle. This supplemental rate was included in Contract Modification 15, which was approved by the Commission in April In addition to the $1.60 per service hour reimbursement, Shuttle prepared and submitted a reconciliation at the end of 2007 claiming an additional $24,662 for employee health and welfare and pension premiums paid by Shuttle which were in excess of amounts previously approved by the Commission. The additional $24,662 payment was included in Contract Modification 17, which was approved by the Commission in May Therefore, it appears the Airport paid Shuttle $24,662 for unanticipated health and welfare and pension benefits, in addition to the $122,174 paid in the $1.60 per hour supplemental service rate. The Airport does not require Shuttle to provide an annual reconciliation of all incurred labor and health and welfare and pension benefit costs to all amounts invoiced for these costs, regardless of how they were billed, and therefore cannot properly determine the appropriateness of amounts paid. The amount of the additional payments is supported by a reconciliation that compares health and welfare and pension benefit costs incurred by Shuttle to amounts billed to the Airport in the billed service hours. The reconciliation provided to the auditors did not include the $1.60 per service hour payments made by the Airport during 2007, which would be necessary to consider when arriving at any additional health and welfare reimbursements due to Shuttle. In response to the audit team s inquiries, Airport staff has directed Shuttle to identify additional health and welfare and pension benefit premium payments received from the 2 Contract modifications refer to payments as employee pension and health and welfare premiums while the Proposition J analysis references reflects that the Other supplemental service rate is for unanticipated health and welfare costs. 9

20 Airport for the 2007 service year. To determine the proper total amount that Shuttle should have been paid for 2007, Shuttle needs to revise the reconciliation to reflect payments made by the Airport that were billed at the $1.60 hour supplemental service rate, and to include all amounts paid for this cost category. Recommendations The Airport should: 5. Require Shuttle to revise the 2007 health and welfare reconciliation to include the estimated $122,174 of health and welfare and benefit premiums paid throughout 2007 in the $1.60 per hour supplemental service rate, in addition to all one-time payments. 6. Collect the total amount of overpayments for health and welfare and benefit premiums. Finding 1.3 Shuttle received both a guaranteed profit and additional management profit during the audit period. As discussed under Finding 1.1, the contract guarantees a fixed amount of profit per year regardless of Shuttle s performance. Besides this guaranteed profit, Airport Management granted Shuttle an additional management profit based on a verbal agreement. For the audit period, Shuttle received guaranteed profit payments totaling $161,000: $53,000 in January 2007 $54,000 in January 2008 $54,000 in January 2009 While reviewing a contract operational budget spreadsheet used by the Airport to monitor billings and payments, the auditors found additional profit payments to Shuttle totaling $357,516 for the audit period: $108,692 in January 2007 $114,610 in January 2008 $134,213 in January 2009 These payments were categorized as unanticipated 10

21 expenses. The auditors found that the additional payments were actually for a second guaranteed profit referred to by the Airport and Shuttle as an additional management profit, not for unanticipated expenses. The Airport considered the additional profit payments to be unanticipated expenses because they were granted in response to an increase in service hours over the life of the contract. As discussed under Finding 1.1, the Airport used the unanticipated operational expense category for recurring payments that are not, by definition, unanticipated. According to the Airport manager responsible for administering the contract, this additional profit was based on a verbal agreement made by a prior Airport manager in the early years of the contract. Airport management staff indicated that the additional profit was approved through modifications 3 and 4. However, these modifications were for service increases specific to the 1998 and 1999 calendar years. The additional payments approved for those years were $13,400 and $13,375, respectively, significantly less than the $357,516 in additional management profit payments made during the audit period. The audit team found that a contract modification to reflect the significant amounts paid for additional management profit over the remainder of the contract was not prepared and approved. Airport staff did include the additional profit as an unanticipated operational expense in the Proposition J analyses it used to develop proposed service billing rates, and considered this inclusion as evidence that the additional management profit was approved annually by the Commission. However, this practice was insufficient, due to the lack of explicit identification and approval for the additional profit. Recommendations The Airport should: 7. Classify the additional management profit in the profit expense category, instead of unanticipated expenses, and ensure that all past and future payments receive proper review and approval. 8. Consider establishing a performance-based incentive fee to address changes in service hours, if it wants to make fee payments to Shuttle in addition to the profit payments provided for in the contract. 11

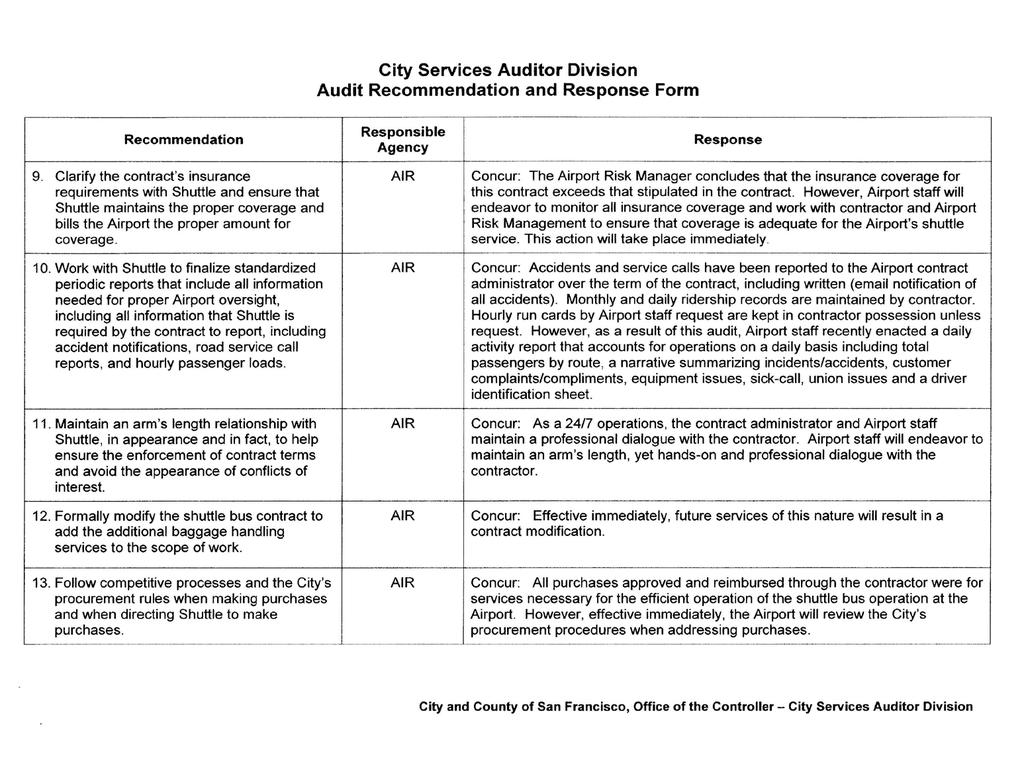

22 Finding 1.4 Contractual insurance requirements need to be clarified to ensure that Shuttle maintains proper coverage and does not bill the Airport more than required. Shuttle is purchasing automobile insurance coverage that the Airport believes is already provided for in a comprehensive general liability policy and an excess umbrella liability policy. The contract requires Shuttle to maintain comprehensive automobile liability insurance with limits of not less than $5 million each occurrence of combined single limit for bodily injury and property damage. The Airport and Shuttle have different interpretations of this provision. The Airport's Risk Management Office stated that Shuttle meets the coverage requirement by maintaining excess/umbrella liability coverage of $20 million and comprehensive general liability coverage of $5 million. However, Shuttle believes that the excess/umbrella liability does not include any coverage for automobile liability, and that a separate $5 million comprehensive automobile liability policy is necessary in order to meet the contract s requirements. The cost of the annual comprehensive automobile policy, which was renewed in January 2009, is $120,989. Recommendation The Airport should: 9. Clarify the contract s insurance requirements with Shuttle and ensure that Shuttle maintains the proper coverage and bills the Airport the proper amount for coverage. Finding 1.5 Shuttle service performance reporting is not adequate in some respects and is not fully consistent with contract requirements. Shuttle service performance reports submitted to the Airport may not provide the Airport with the information needed for proper oversight of Shuttle s operations, and do not fully comply with contract requirements. The contract lists a variety of required reports, such as trip, road service call, and accident notification reports, that Shuttle is required to submit to the Airport. The contract also requires Shuttle to report the number of passengers carried hourly, and to provide reports in a format specified by the Airport Director. The audit team found that: Some required information, including accident notifications, was being submitted by Shuttle in a 12

23 variety of formats, including verbally and by , and was not centralized and easily accessible. Required road service call reports were not being submitted. Shuttle was reporting passengers carried on a daily basis, not hourly. Recommendation The Airport should: 10. Work with Shuttle to finalize standardized periodic reports that include all information needed for proper Airport oversight, including all information that Shuttle is required by the contract to report, including accident notifications, road service call reports, and hourly passenger loads. 13

24 Page intentionally left blank. 14

25 CHAPTER 2 Improvements in Contract Administration and Monitoring Are Needed to Prevent Loss to the Airport Summary The audit found several areas in which the Airport needs to improve monitoring and administration of the shuttle bus contract. The Airport: Is not maintaining an arm s-length business relationship with Shuttle. Did not modify the contract to reflect additional baggage handling services. Directed Shuttle to make purchases that were made without competitive solicitations and without ensuring compliance with City procurement policies. Did not ensure that the City s financial interest in the buses was protected, because Shuttle and the Airport did not comply with the contract s bus purchase terms. Used a process for developing Shuttle s budget that may not result in the best financial terms for the Airport. Had inadequate processes for reviewing and approving Shuttle invoices and monitoring contract costs that exposed the Airport to overpayments. Finding 2.1 The Airport needs to maintain a proper arm s-length business relationship with Shuttle. Several of the audit findings discussed in this report, as well as additional observations by the audit team, suggest that the Airport needs to do a better job of maintaining an arm slength business relationship with Shuttle 3. For example: The auditors obtained copies of the vehicle registrations for the most recently purchased buses and found that their ownership was reflected as City and County of San Francisco DBA (doing business as) SFO Shuttle Bus Company. This implies Shuttle is a City agency or 3 An arm s length agreement is an agreement made by two parties freely and independently of each other, and without some special relationship, such as one party having complete control of the other. 15

26 other related entity, instead of a City contractor. The most recent purchase of seven buses was made in a manner that did not protect the City s financial interest in the buses. In addition, the Airport did not complete the transfer of title for other buses that were purchased and paid in full by Shuttle using Airport funds, exposing the City to potential loss due to a lack of a secured interest in the buses. The Airport works with Shuttle to establish Shuttle s budget for each fiscal year. To ensure it arrives at the best financial terms possible, the Airport should follow sound business practices and require Shuttle to first submit for Airport review its proposed costs and fees for service, and then negotiate with Shuttle to arrive at the best terms possible. Further, the Airport is accepting estimated costs from Shuttle at face value, without adequately questioning whether the estimates are reasonable and whether all costs are necessary. The Airport s payments for annual administrative costs based on budgeted, fixed amounts are a primary example of this practice. Cell phones included in Shuttle s phone plan have been issued to Airport employees. Airport staff explained the phones are necessary due to the 24 hour/7 day a week nature of the shuttle bus operations. However, phone equipment needed by City employees should be issued and monitored by the Airport, not Shuttle. Additionally, one Airport staff member who was issued a phone is also responsible for reviewing Shuttle s billings for accuracy, which is a potential conflict of interest. The organization chart provided by the Airport for shuttle bus operations included the Shuttle s general manager along with Airport employees. Maintaining an arm s-length relationship with City contractors, in appearance and in fact, helps ensure the enforcement of contact terms and helps avoid the appearance of conflicts of interest. Recommendation The Airport should: 11. Maintain an arm s-length relationship with Shuttle, in appearance and in fact, to help ensure the enforcement of contact terms and avoid the appearance of conflicts of interest. 16

27 Finding 2.2 The Airport added baggage handling services to the contract s scope of work without modifying the contract. The Airport did not formally modify the contract to reflect the addition of baggage handling services to the scope of work. In April 2006, the Airport directed Shuttle to provide customer assistance with loading and offloading baggage during peak periods. In order to meet this requirement, Shuttle obtained bids and entered into a contract with a baggage handling company. The Airport considered the costs associated with the service to be unanticipated operational expenses, and therefore did not modify the contract. However, the audit team found that these services represented a significant addition to the contract s scope of work, not unanticipated operational expenses. The Airport reimbursed Shuttle $838,944 for baggage handling services during the audit period. Recommendation The Airport should: 12. Formally modify the shuttle bus contract to add the additional baggage handling services to the scope of work. Finding 2.3 Shuttle made purchases without competitive solicitations and without ensuring compliance with the City's procurement policies. The Airport directed Shuttle to purchase two software systems, bus signs, and electrical services for a total cost of $117,047. The purchases were made without competitive solicitations and without ensuring compliance with the City's procurement policies. Purchases included: $11,642 for a software program to provide flight arrival information. $42,500 for bus scheduling software that assists in developing schedules and routes to efficiently determine the required level of service frequency. $31,835 for digital bus signs to assist passengers in determining the location of new stops after the opening of the long-term parking garage. 17

28 $31,070 for electrical infrastructure improvements at each bus stop to accommodate the installation of a new automated vehicle locator system. The City s procurement policies for purchases less than $50,000 require: Submittal of a requisition to the Office of Contract Administration (OCA) for commodity purchases greater than $10,000. Formal bidding for general and professional services over $29,000. Informal solicitation is required for purchases between $10,000 and $29,000. For purchases less than $10,000, bidding is encouraged but not required. Airport staff provided the auditors with the business justification for having Shuttle make these purchases. For example, Airport staff stated that the software programs purchased by Shuttle were commercially available products and the least expensive, and that the electrical work was performed by a reputable firm familiar with complex building inspection and code enforcement requirements at the Airport. Nevertheless, the Airport should have followed competitive processes to ensure that it obtained the best available pricing, and to avoid the appearance that the contract with Shuttle was being used to circumvent the City s procurement rules. Recommendation The Airport should: 13. Follow competitive processes and the City s procurement rules when making purchases and when directing Shuttle to make purchases. Finding 2.4 The Airport s financial interest in the buses was not adequately protected because Shuttle and the Airport did not comply with the contract s bus purchase terms. The audit team found that the Airport s financial interest in the buses was not adequately protected. The most recent purchase of seven buses was made using a fixed-term installment note between Shuttle and the lender that did not reflect the City s interest in the buses. Airport management was aware of this financing agreement, and considered 18

29 Shuttle s registration of the buses with the California Department of Motor Vehicles under the name, City and County of San Francisco DBA SFO Shuttle Bus Company, with the same listing on the certificates of title, as a sufficient method of securing the City s interest. However, this method does not protect the City s interest. Modification 15 of the contract required Shuttle to acquire seven low-floor compressed natural gas transit buses for delivery and operation by December 31, 2007, and to provide title to the City for the buses by December 31, The modification also specified that Shuttle would: Obtain prior approval from the City before entering into a lease-purchase agreement for procurement of the buses, with terms that were consistent with the modification and that specify that the Airport has the right to assume Shuttle's position in the lease-purchase agreement. Provide to the City evidence of a security interest for the seven buses upon execution of the lease-purchase documents. At that time, Shuttle would also provide evidence of a security interest for the existing fleet of 16 buses sufficient to ensure the City's ability to assume all agreements entered into by Shuttle in the event of default by Shuttle. The Airport did not require Shuttle to comply with Modification 15, and instead allowed Shuttle to purchase the buses using a fixed-rate installment note that does not contain language specifying that the Airport can assume Shuttle s position in the agreement. Further, the installment note does not contain provisions to secure the City s interest in the buses, which are listed as collateral. As previously discussed, the Airport considered Shuttle s registration of the buses under the name, City and County of San Francisco DBA SFO Shuttle Bus Company, as a sufficient method of securing the City s interest in the buses. However, this method is not appropriate; Shuttle is a City contractor and not a related City entity doing business under a fictitious name. As a result, the City apparently does not have a security interest in the seven buses, and could be exposed to loss if Shuttle defaulted on the loan or entered bankruptcy. In addition, the Airport did not complete the transfer of title for other buses that were purchased and paid in full by 19

30 Shuttle using Airport funds. The auditors obtained copies of the certificates of title on file with the Airport for two of 16 buses that had been paid in full. Although Shuttle had signed over title to the Airport and released its interest in the buses, the Airport did not complete the title transfer transactions by updating the registrations with the California Department of Motor Vehicles. As a result, the City was not reflected as the registered owner, exposing the City to potential loss due to a lack of a secured interest in the buses. Recommendation The Airport should: 14. Consult with the City Attorney s Office to determine the appropriate method of securing the City s interest in all buses, and properly secure the City s interest. Finding 2.5 The process for developing Shuttle s budget may not result in the best financial terms for the Airport. As discussed under Finding 2.1, the Airport works with Shuttle to establish Shuttle s budget for each fiscal year, instead of requiring Shuttle to first submit for Airport review its proposed costs and fees. The annual budget is then submitted to the Airport Commission for approval. The Airport uses its annual Proposition J (Prop J) analysis of the Shuttle contract to prepare and document each year s budget for the shuttle services contract. 4 However, the Prop J process is not intended to be used as a budget for contracted services; it is designed to provide an annual comparison of proposed contract costs with the costs of providing the same services with City employees and resources. To ensure an accurate, economical estimate of operating expenses for each year. Shuttle should prepare and submit a budget based on cost proposals that align with the contract terms, which, as discussed in Finding 1.1, need to be clarified. Airport staff stated that using the Prop J analysis to prepare 4 As discussed in the Background section of this report, Prop J authorizes outside contracting of existing services, wherever a service can be performed by a private contractor at a cost lower than the same service performed by civil servants. The authorization is obtained by submitting an analysis for the Controller s review and approval that demonstrates the cost-effectiveness of contracting for the services versus performing the services with City employees. 20

31 and document Shuttle s budget believed their actions was an efficient use of the analysis. However, as discussed under Finding 1.1, current practices do not ensure that the Airport receives the best financial terms possible. This would best be accomplished by following sound business practices and requiring Shuttle to submit for Airport review its proposed costs and fees for service; this would be followed by negotiations with Shuttle to arrive at the best terms possible. This would also help ensure that Shuttle adequately considers cost and efficiency when planning its service delivery to the Airport for each fiscal year. Recommendations The Airport should: 15. Require Shuttle to prepare and submit an annual budget proposal. 16. Review each year s proposed budget to ensure it is cost effective, consistent with the contract, and that it meets the Airport s business needs. 17. Negotiate with Shuttle to arrive at the best terms possible. Finding 2.6 Current processes for reviewing and approving Shuttle invoices and monitoring contract costs are inadequate and expose the Airport to overpayments. Weaknesses in the Airport s processes for reviewing and approving Shuttle invoices and monitoring contract costs expose the Airport to overpayments and other errors. The audit team found that: The Airport made a $25,803 duplicate payment of a bus financing invoice for March The duplicate payment was made because Shuttle incorrectly submitted the same cost for reimbursement twice, once supported by the original invoice and once supported by a copy of the invoice. The duplicate payment was made despite the Airport s policy to pay only on original invoices, unless justified and approved by a Deputy Director. Shuttle, not the Airport, identified the duplicate payment and credited the Airport. The Airport incorrectly adjusted a payment to Shuttle for an $18,945 credit that it was not entitled to. Shuttle inadvertently made an extra payment of $18,945 to a 21

32 bus lease vendor in December 2007, which was not included in its December 2007 billing to the Airport. Although Shuttle did not bill the Airport for the extra payment, it incorrectly credited the Airport for it when billing the Airport for January The Airport approved the billing and Airport Accounting processed the payment that included the erroneous $18,945 credit. Some invoices were approved and paid without sufficient supporting documentation, including a: o o o $3,802 invoice for communications equipment paid solely based on a Shuttle purchase order, with no supporting third party invoice. $6,507 invoice for vendor travel expenses paid without any supporting receipts. $14,941 invoice for customer service training classes by Shuttle s Human Resources Director, which was paid without proof of attendance, as required by the contract, or receipts for the cost of invoiced materials. There were material errors in the spreadsheet the Airport uses to track Shuttle invoices and monitor contract spending. The cost tracking spreadsheet: o Understated FY expenses by $200,455. o Overstated FY expenses by $14,942. The Airport does not have written procedures in place to document and communicate the invoice review and approval steps and documentation necessary to ensure that amounts billed by Shuttle are correct and adequately supported. In addition, current practices do not include periodic reconciliation of amounts approved for payment and entered into the Airport s tracking spreadsheet with the Airport s accounting records. Written procedures and periodic reconciliation to the Airport s accounting records would help ensure that amounts paid are proper and that Shuttle costs are properly monitored. Recommendations The Airport should: 18. Develop written desk procedures that specify the invoice review and approval steps and documentation necessary to ensure that amounts billed by Shuttle are correct and adequately supported prior to payment. 22

33 Among other requirements, the procedures should specify required documentation for third party costs and training, and should include review steps to prevent duplicate payments. 19. Ensure that staff more carefully enters expenses in the cost tracking spreadsheet and perform monthly reconciliations with the Airport s accounting records. 20. Reimburse Shuttle $18,945 for the invalid credit, and ensure that all charges and credits are applicable to the current billing period prior to submission to Airport Accounting for processing. Finding 2.7 Significant assets are not reflected in the Airport s fixed asset accounting records. Significant assets purchased through the Shuttle contract are not being properly identified and added to the Airport s fixed asset accounting records, because the Airport s existing procedures for recording and accounting for fixed assets are not being followed, As a result, there are inaccuracies in the Airport s financial records and an increased risk of assets being misappropriated. Shuttle is reimbursed for all costs associated with providing shuttle bus service to the Airport. This includes the purchase of fixed assets such as shuttle buses, bus lifts, bus signs, and other vehicles. These items are Airport assets and should be reflected in the Airport s accounting records. However, because documentation such as invoices and purchase orders for these assets are not forwarded to Airport Accounting, the assets are not tagged, properly tracked, and recorded in the Airport s accounting records. The value of these assets is significant; for example, the purchase cost of the seven buses currently acquired in 2007 was approximately $2,500,000. Shuttle is currently operating a fleet of 23 buses. Recommendation The Airport should: 21. Ensure that all assets paid for by the City through the contract are identified as City property, tagged with asset tags, and recorded in the Airport s accounting records. 23

34 Finding 2.8 Weaknesses in Shuttle s tires and bus parts inventory controls expose the Airport to loss. The Airport is exposed to loss because Shuttle does not maintain an accurate, up-to-date, inventory of leased tires and purchased bus parts. Shuttle maintains a vehicle maintenance database system to account for parts used to maintain the shuttle bus fleet. Parts are entered into the system after purchase orders are closed and parts are received. However, the use of parts is not necessarily entered into system, resulting in inaccurate inventory information, and Shuttle does not conduct a periodic physical parts inventory to verify that accounting records are accurate. In addition, the same Shuttle employee is responsible for both ordering and receiving bus parts and equipment. Sound business practices dictate that certain functions, such as the ordering and receiving of parts, be performed by different individuals, in order to minimize the risk of theft or misappropriation. Tires used in the shuttle operations are leased. The audit team found that, although new tires are secured in a locked storage cabinet, used tires are kept outside next to the bus maintenance facility and are not secured. Shuttle staff stated that the tires are too heavy to be stolen and are not commonly used on most vehicles. In addition, although tire inventory is taken annually by the tire leasing company, Shuttle staff was unable to locate the last annual tire inventory report prepared by the tire lease provider. As a result, the audit team could not substantiate that all used tire inventory was properly accounted for. Given the manner in which the Airport administers the contract, the Airport would be responsible for paying for incurred losses. Recommendations The Airport should direct Shuttle to: 22. Enter parts used in its vehicle maintenance database. 23. Conduct periodic physical inventories of parts and tires to ensure that all inventories are accounted for. 24. Separate the parts ordering and receiving functions or implement effective compensating controls such as unannounced physical inventory counts. 25. Secure the used tire inventory. 24

35 Finding 2.9 The Airport did not maintain current copies of automobile liability insurance certificates, and neither Shuttle nor the Airport could provide proof of compliance with the contract performance bond requirement for part of the audit period. The Airport did not maintain current proof of comprehensive automobile liability insurance required under the contract. Shuttle did comply with this contract requirement and provided the auditors with proof of coverage. As discussed under Finding 1.4, the Airport believed an umbrella policy and a general liability policy included coverages for comprehensive automobile liability insurance, and therefore did not request copies of the comprehensive automobile liability insurance certificates. Additionally, the Airport may not have been adequately protected from loss, because it is not clear that Shuttle complied with the contract s performance bond requirement for part of the audit period. The contract requires Shuttle to renew, on an annual basis, a performance bond in the amount of $1,500,000. This bond is to be maintained at Shuttle s cost. In 2003, the Airport modified the contract to reduce the bond amount to $1,000,000. Airport staff indicated that Shuttle s standby letter of credit, which is an acceptable substitute for a performance bond, was automatically renewed on November 30 th of each year. However, the copy of the performance bond provided to the auditors reflected an expiration date of November 30, 2008, and neither Shuttle nor the Airport could provide documentation to substantiate that Shuttle was in compliance with the contract requirement from December 1, 2008, to January 31, Airport staff indicated the letter of credit is automatically renewed every year and it does not expire, and that Shuttle was therefore in compliance with the contract s requirement. However, later in the audit, Airport staff provided a standby letter of credit from a different bank dated February 4, 2009, which reflected an expiration date of January 28, The February 2009 standby letter of credit does contain a provision for automatic extension every year. However, Airport staff did not provide evidence that the previous standby letter of credit, which reflected an expiration date of November 30, 2008, was automatically extended for the period from December 1, 2008, to February 3,

36 Recommendations The Airport should: 26. Ensure it maintains all current certificates of insurance for coverage required by the contract. 27. Ensure that a copy of the current standby letter of credit is maintained on file, regardless of whether the letter of credit contains an automatic renewal provision, in order to ensure that Shuttle s compliance with the contract s performance bond requirements is documented. Finding 2.10 Shuttle was unable to locate and provide all requested documents for the audit period. During the course of the audit, Shuttle was unable to locate a financing agreement for bus purchases and an annual tire inventory report. The contract s audit clause requires Shuttle to maintain, and make available to the City, all books and records related by the contract. These records must be maintained for a period of five years following the final contract payment. Recommendation The Airport should: 28. Remind Shuttle to retain all records in accordance with contract requirements. 26

37 APPENDIX A: AIRPORT S RESPONSE A-1

38 Page intentionally left blank. A-2

39 AUDIT RECOMMENDATIONS AND RESPONSES Office of the Controller, City Services Auditor A-3

40 A-4

41 A-5

42 A-6

43 A-7

44 A-8

45 A-9

46 Page intentionally left blank. A-10

47 APPENDIX B: SHUTTLE S RESPONSE B-1

48 B-2 Office of the Controller, City Services Auditor

49 B-3

50 B-4 Office of the Controller, City Services Auditor

51 B-5

52 B-6 Office of the Controller, City Services Auditor

53 B-7

54 B-8 Office of the Controller, City Services Auditor

55 B-9

56 B-10 Office of the Controller, City Services Auditor

City and County of San Francisco

City and County of San Francisco Office of the Controller City Services Auditor AIRPORT COMMISSION: Asiana Airlines Paid All Landing Fees Due but Incurred $12,846 in Late Charges for 2010 Through 2012

City and County of San Francisco Office of the Controller City Services Auditor AIRPORT COMMISSION: Asiana Airlines Paid All Landing Fees Due but Incurred $12,846 in Late Charges for 2010 Through 2012

City and County of San Francisco

City and County of San Francisco Office of the Controller City Services Auditor RECREATION AND PARK DEPARTMENT: Concession Audit of Stow Lake Corporation March 3, 2009 CONTROLLER S OFFICE CITY SERVICES

City and County of San Francisco Office of the Controller City Services Auditor RECREATION AND PARK DEPARTMENT: Concession Audit of Stow Lake Corporation March 3, 2009 CONTROLLER S OFFICE CITY SERVICES

REPORT 2014/111 INTERNAL AUDIT DIVISION. Audit of air operations in the United Nations Operation in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2014/111 Audit of air operations in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of air operations in the United Nations

INTERNAL AUDIT DIVISION REPORT 2014/111 Audit of air operations in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of air operations in the United Nations

Terms of Reference: Introduction

Terms of Reference: Assessment of airport-airline engagement on the appropriate scope, design and cost of new runway capacity; and Support in analysing technical responses to the Government s draft NPS

Terms of Reference: Assessment of airport-airline engagement on the appropriate scope, design and cost of new runway capacity; and Support in analysing technical responses to the Government s draft NPS

EAST 34 th STREET HELIPORT. Report 2007-N-7

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objectives... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objectives... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and

STATE OF NEVADA DEPARTMENT OF BUSINESS AND INDUSTRY TRANSPORTATION SERVICES AUTHORITY AUDIT REPORT

STATE OF NEVADA DEPARTMENT OF BUSINESS AND INDUSTRY TRANSPORTATION SERVICES AUTHORITY AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 7 Background... 7 Scope and Objective...

STATE OF NEVADA DEPARTMENT OF BUSINESS AND INDUSTRY TRANSPORTATION SERVICES AUTHORITY AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 7 Background... 7 Scope and Objective...

OFFICE OF THE AUDITOR

OFFICE OF THE AUDITOR DEPARTMENT OF AVIATION AIR WISCONSIN AIRLINES CORPORATION REVENUE AND CONTRACT COMPLIANCE AUDIT OCTOBER 2007 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County

OFFICE OF THE AUDITOR DEPARTMENT OF AVIATION AIR WISCONSIN AIRLINES CORPORATION REVENUE AND CONTRACT COMPLIANCE AUDIT OCTOBER 2007 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County

Nova Southeastern University Joint-Use Library Agreement: Review of Public Usage

Exhibit 1 Nova Southeastern University Joint-Use Library Agreement: Robert Melton, CPA, CIA, CFE, CIG County Auditor Audit Conducted by: Gerard Boucaud, CISA, Audit Manager Dirk Hansen, CPA, Audit Supervisor

Exhibit 1 Nova Southeastern University Joint-Use Library Agreement: Robert Melton, CPA, CIA, CFE, CIG County Auditor Audit Conducted by: Gerard Boucaud, CISA, Audit Manager Dirk Hansen, CPA, Audit Supervisor

Official Journal of the European Union L 7/3

12.1.2010 Official Journal of the European Union L 7/3 COMMISSION REGULATION (EU) No 18/2010 of 8 January 2010 amending Regulation (EC) No 300/2008 of the European Parliament and of the Council as far

12.1.2010 Official Journal of the European Union L 7/3 COMMISSION REGULATION (EU) No 18/2010 of 8 January 2010 amending Regulation (EC) No 300/2008 of the European Parliament and of the Council as far

OFFICE OF THE AUDITOR

OFFICE OF THE AUDITOR DEPARTMENT OF AVIATION (FORMERLY AMERICAN TRANS AIR, INC.) REVENUE AND CONTRACT COMPLIANCE AUDIT JUNE 2006 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County

OFFICE OF THE AUDITOR DEPARTMENT OF AVIATION (FORMERLY AMERICAN TRANS AIR, INC.) REVENUE AND CONTRACT COMPLIANCE AUDIT JUNE 2006 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County

Summit County Fiscal Office Auditor Division; Accounting Department Preliminary Audit Report. PREPARED FOR: John A. Donofrio Audit Committee

09-Accounting.Fiscal-64 PREPARED FOR: John A. Donofrio Audit Committee Approved by Audit Committee December 11, 2009 Summit County Internal Audit Department 175 South Main Street Akron, Ohio 44308 Bernard

09-Accounting.Fiscal-64 PREPARED FOR: John A. Donofrio Audit Committee Approved by Audit Committee December 11, 2009 Summit County Internal Audit Department 175 South Main Street Akron, Ohio 44308 Bernard

NEW JERSEY LAW REVISION COMMISSION. Final Report Relating to Unclaimed Property. December 20, 2018

NEW JERSEY LAW REVISION COMMISSION Final Report Relating to Unclaimed Property December 20, 2018 The work of the New Jersey Law Revision Commission is only a recommendation until enacted. Please consult

NEW JERSEY LAW REVISION COMMISSION Final Report Relating to Unclaimed Property December 20, 2018 The work of the New Jersey Law Revision Commission is only a recommendation until enacted. Please consult

REPORT 2014/065 INTERNAL AUDIT DIVISION. Audit of air operations in the United. Nations Assistance Mission in Afghanistan

INTERNAL AUDIT DIVISION REPORT 2014/065 Audit of air operations in the United Nations Assistance Mission in Afghanistan Overall results relating to the effective management of air operations in the United

INTERNAL AUDIT DIVISION REPORT 2014/065 Audit of air operations in the United Nations Assistance Mission in Afghanistan Overall results relating to the effective management of air operations in the United

Air Operator Certification

Civil Aviation Rules Part 119, Amendment 15 Docket 8/CAR/1 Contents Rule objective... 4 Extent of consultation Safety Management project... 4 Summary of submissions... 5 Extent of consultation Maintenance

Civil Aviation Rules Part 119, Amendment 15 Docket 8/CAR/1 Contents Rule objective... 4 Extent of consultation Safety Management project... 4 Summary of submissions... 5 Extent of consultation Maintenance

COMMISSION IMPLEMENTING REGULATION (EU)

") 18.10.2011 Official Journal of the European Union L 271/15 COMMISSION IMPLEMENTING REGULATION (EU) No 1034/2011 of 17 October 2011 on safety oversight in air traffic management and air navigation services

18.10.2011 Official Journal of the European Union L 271/15 COMMISSION IMPLEMENTING REGULATION (EU) No 1034/2011 of 17 October 2011 on safety oversight in air traffic management and air navigation services

March 4, Mr. H. Dale Hemmerdinger Chairman Metropolitan Transportation Authority 347 Madison Avenue New York, NY Re: Report 2007-F-31

THOMAS P. DiNAPOLI STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER March 4, 2008 Mr. H. Dale Hemmerdinger Chairman Metropolitan Transportation

THOMAS P. DiNAPOLI STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER March 4, 2008 Mr. H. Dale Hemmerdinger Chairman Metropolitan Transportation

NIAGARA MOHAWK POWER CORPORATION. Procedural Requirements

NIAGARA MOHAWK POWER CORPORATION Procedural Requirements Initial Effective Date: November 9, 2015 Table of Contents 1. Introduction 2. Program Definitions 3. CDG Host Eligibility Provisions 4. CDG Host

NIAGARA MOHAWK POWER CORPORATION Procedural Requirements Initial Effective Date: November 9, 2015 Table of Contents 1. Introduction 2. Program Definitions 3. CDG Host Eligibility Provisions 4. CDG Host

COMMISSION OF THE EUROPEAN COMMUNITIES. Draft. COMMISSION REGULATION (EU) No /2010

No /2010") COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX Draft COMMISSION REGULATION (EU) No /2010 of [ ] on safety oversight in air traffic management and air navigation services (Text with EEA relevance)

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX Draft COMMISSION REGULATION (EU) No /2010 of [ ] on safety oversight in air traffic management and air navigation services (Text with EEA relevance)

Shuttle Membership Agreement

Shuttle Membership Agreement Trend Aviation, LLC. FlyTrendAviation.com Membership with Trend Aviation, LLC. ("Trend Aviation") is subject to the terms and conditions contained in this Membership Agreement,

Shuttle Membership Agreement Trend Aviation, LLC. FlyTrendAviation.com Membership with Trend Aviation, LLC. ("Trend Aviation") is subject to the terms and conditions contained in this Membership Agreement,

INTERNAL AUDIT REPORT

REPORT SLOA III Airline Agreement Compliance with Calculation of Rates Limited Operational Audit January 1, 2013 December 31, 2014 ISSUE DATE: February 10, 2015 REPORT NO. 2015-04 TABLE OF CONTENTS TRANSMITTAL

REPORT SLOA III Airline Agreement Compliance with Calculation of Rates Limited Operational Audit January 1, 2013 December 31, 2014 ISSUE DATE: February 10, 2015 REPORT NO. 2015-04 TABLE OF CONTENTS TRANSMITTAL

PUBLIC ACCOUNTABILITY PRINCIPLES FOR CANADIAN AIRPORT AUTHORITIES

PUBLIC ACCOUNTABILITY PRINCIPLES FOR CANADIAN AIRPORT AUTHORITIES The Canadian Airport Authority ( CAA ) shall be incorporated in a manner consistent with the following principles: 1. Not-for-profit Corporation

PUBLIC ACCOUNTABILITY PRINCIPLES FOR CANADIAN AIRPORT AUTHORITIES The Canadian Airport Authority ( CAA ) shall be incorporated in a manner consistent with the following principles: 1. Not-for-profit Corporation

MANASSAS REGIONAL AIRPORT

Appendix F MANASSAS REGIONAL AIRPORT Non-Commercial Self-Fueling Permit Applicant: Authorized Representative: Title: Aircraft Storage Location/Hangar Address: Aircraft to be Fueled (List Type & N number):

Appendix F MANASSAS REGIONAL AIRPORT Non-Commercial Self-Fueling Permit Applicant: Authorized Representative: Title: Aircraft Storage Location/Hangar Address: Aircraft to be Fueled (List Type & N number):

CHG 0 9/13/2007 VOLUME 2 AIR OPERATOR AND AIR AGENCY CERTIFICATION AND APPLICATION PROCESS

VOLUME 2 AIR OPERATOR AND AIR AGENCY CERTIFICATION AND APPLICATION PROCESS CHAPTER 5 THE APPLICATION PROCESS TITLE 14 CFR PART 91, SUBPART K 2-536. DIRECTION AND GUIDANCE. Section 1 General A. General.

VOLUME 2 AIR OPERATOR AND AIR AGENCY CERTIFICATION AND APPLICATION PROCESS CHAPTER 5 THE APPLICATION PROCESS TITLE 14 CFR PART 91, SUBPART K 2-536. DIRECTION AND GUIDANCE. Section 1 General A. General.

Planning Issues in Aircraft Management Agreements

Moscow Office Chaplygina House, 20/7 Chaplygina Street, Moscow, 105062, Russia St. Petersburg Office Bolloev Center, 4 Grivtsova Lane, St. Petersburg, 190000, Russia By: Derek Bloom, Partner Capital Legal

Moscow Office Chaplygina House, 20/7 Chaplygina Street, Moscow, 105062, Russia St. Petersburg Office Bolloev Center, 4 Grivtsova Lane, St. Petersburg, 190000, Russia By: Derek Bloom, Partner Capital Legal

OVERSEAS TERRITORIES AVIATION REQUIREMENTS (OTARs)

") OVERSEAS TERRITORIES AVIATION REQUIREMENTS (OTARs) Part 173 FLIGHT CHECKING ORGANISATION APPROVAL Published by Air Safety Support International Ltd Air Safety Support International Limited 2005 ISBN 0-11790-410-4

OVERSEAS TERRITORIES AVIATION REQUIREMENTS (OTARs) Part 173 FLIGHT CHECKING ORGANISATION APPROVAL Published by Air Safety Support International Ltd Air Safety Support International Limited 2005 ISBN 0-11790-410-4

Administration Policies & Procedures Section Commercial Ground Transportation Regulation

OBJECTIVE METHOD OF OPERATION Definitions To promote and enhance the quality of Commercial Ground Transportation, the public convenience, the safe and efficient movement of passengers and their luggage

OBJECTIVE METHOD OF OPERATION Definitions To promote and enhance the quality of Commercial Ground Transportation, the public convenience, the safe and efficient movement of passengers and their luggage

Working Draft: Time-share Revenue Recognition Implementation Issue. Financial Reporting Center Revenue Recognition

March 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Time-share Revenue Recognition Implementation Issue Issue #16-6: Recognition of Revenue Management Fees Expected Overall Level

March 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Time-share Revenue Recognition Implementation Issue Issue #16-6: Recognition of Revenue Management Fees Expected Overall Level

ALASKA AIRLINES AND VIRGIN AMERICA AVIATION SAFETY ACTION PROGRAM (ASAP) FOR FLIGHT ATTENDANTS MEMORANDUM OF UNDERSTANDING

FOR FLIGHT ATTENDANTS MEMORANDUM OF UNDERSTANDING") ALASKA AIRLINES AND VIRGIN AMERICA AVIATION SAFETY ACTION PROGRAM (ASAP) FOR FLIGHT ATTENDANTS MEMORANDUM OF UNDERSTANDING 1. GENERAL. Alaska Airlines and Virgin America (AS/VX) are Title 14 of the Code

ALASKA AIRLINES AND VIRGIN AMERICA AVIATION SAFETY ACTION PROGRAM (ASAP) FOR FLIGHT ATTENDANTS MEMORANDUM OF UNDERSTANDING 1. GENERAL. Alaska Airlines and Virgin America (AS/VX) are Title 14 of the Code

Various Counties MINUTE ORDER Page 1 of I

TEXAS TRANSPORTATION COMMISSION Various Counties MINUTE ORDER Page 1 of I Various Districts Texas Government Code, Chapter 2056, requires that each state agency prepare a five-year strategic plan every

TEXAS TRANSPORTATION COMMISSION Various Counties MINUTE ORDER Page 1 of I Various Districts Texas Government Code, Chapter 2056, requires that each state agency prepare a five-year strategic plan every

OFFICE OF THE AUDITOR

OFFICE OF THE AUDITOR DEPARTMENT OF AVIATION REVENUE AND CONTRACT COMPLIANCE AUDIT NOVEMBER 2007 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County of Denver 201 West Colfax Ave.,

OFFICE OF THE AUDITOR DEPARTMENT OF AVIATION REVENUE AND CONTRACT COMPLIANCE AUDIT NOVEMBER 2007 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County of Denver 201 West Colfax Ave.,

TRAVEL POLICY FOR THE U.S. SCIENCE SUPPORT PROGRAM OFFICE (USSSP)

") TRAVEL POLICY FOR THE U.S. SCIENCE SUPPORT PROGRAM OFFICE (USSSP) Table of Contents IMPORTANT INFORMATION 2 TRAVEL AUTHORIZATION 2 AIR TRANSPORTATION GENERAL 2 EXPEDITION-RELATED TRAVEL 3 AIR CARRIER SELECTION

TRAVEL POLICY FOR THE U.S. SCIENCE SUPPORT PROGRAM OFFICE (USSSP) Table of Contents IMPORTANT INFORMATION 2 TRAVEL AUTHORIZATION 2 AIR TRANSPORTATION GENERAL 2 EXPEDITION-RELATED TRAVEL 3 AIR CARRIER SELECTION

CLASS SPECIFICATION 5/12/11 SENIOR AIRPORT ENGINEER, CODE 7257

Form PDES 8 THE CITY OF LOS ANGELES CIVIL SERVICE COMMISSION CLASS SPECIFICATION 5/12/11 SENIOR AIRPORT ENGINEER, CODE 7257 Summary of Duties: A Senior Airport Engineer performs the more difficult and

Form PDES 8 THE CITY OF LOS ANGELES CIVIL SERVICE COMMISSION CLASS SPECIFICATION 5/12/11 SENIOR AIRPORT ENGINEER, CODE 7257 Summary of Duties: A Senior Airport Engineer performs the more difficult and

AIRPORT SPONSORSHIP POLICY

AIRPORT SPONSORSHIP POLICY The Muskegon County Airport (MKG) Sponsorship policy (Policy) is intended to ensure Airport sponsorships are coordinated and aligned with its business goals, maximize opportunity

AIRPORT SPONSORSHIP POLICY The Muskegon County Airport (MKG) Sponsorship policy (Policy) is intended to ensure Airport sponsorships are coordinated and aligned with its business goals, maximize opportunity

APPLICATION FORM FOR APPROVAL AS AN IATA PASSENGER SALES AGENT

APPLICATION FORM FOR APPROVAL AS AN IATA PASSENGER SALES AGENT The information requested below is required by IATA to assist in determining the eligibility of the application for inclusion on the IATA

APPLICATION FORM FOR APPROVAL AS AN IATA PASSENGER SALES AGENT The information requested below is required by IATA to assist in determining the eligibility of the application for inclusion on the IATA

[Docket No. FAA ; Directorate Identifier 2005-NM-056-AD; Amendment ; AD ]

![[Docket No. FAA ; Directorate Identifier 2005-NM-056-AD; Amendment ; AD ]](/thumbs/90/103474126.jpg "[Docket No. FAA ; Directorate Identifier 2005-NM-056-AD; Amendment ; AD ]") [Federal Register: June 7, 2006 (Volume 71, Number 109)] [Rules and Regulations] [Page 32811-32815] From the Federal Register Online via GPO Access [wais.access.gpo.gov] [DOCID:fr07jn06-3] DEPARTMENT OF

[Federal Register: June 7, 2006 (Volume 71, Number 109)] [Rules and Regulations] [Page 32811-32815] From the Federal Register Online via GPO Access [wais.access.gpo.gov] [DOCID:fr07jn06-3] DEPARTMENT OF

EXHIBIT K TERMINAL PROJECT PROCEDURES PHASE I - DEVELOPMENT OF TERMINAL PROGRAM & ALTERNATIVES

EXHIBIT K TERMINAL PROJECT PROCEDURES PHASE I - DEVELOPMENT OF TERMINAL PROGRAM & ALTERNATIVES Over the term of the Master Amendment to the Airline Use and Lease Agreement, the Kansas City Aviation Department

EXHIBIT K TERMINAL PROJECT PROCEDURES PHASE I - DEVELOPMENT OF TERMINAL PROGRAM & ALTERNATIVES Over the term of the Master Amendment to the Airline Use and Lease Agreement, the Kansas City Aviation Department

REPORT 2014/113 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/113 Audit of air operations in the United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Overall results relating to the effective

INTERNAL AUDIT DIVISION REPORT 2014/113 Audit of air operations in the United Nations Organization Stabilization Mission in the Democratic Republic of the Congo Overall results relating to the effective

Current Rules Part 175 Aeronautical Information Service Organisations - Certification Pending Rules

Subpart B Certification Requirements 175.51 Personnel Requirements (a) Each applicant for the grant of an aeronautical information service certificate shall engage, employ or contract: (1) a senior person

Subpart B Certification Requirements 175.51 Personnel Requirements (a) Each applicant for the grant of an aeronautical information service certificate shall engage, employ or contract: (1) a senior person

Review of Aviation Real Property Leases at Fort Lauderdale-Hollywood International Airport

Exhibit 1 Review of Aviation Real Property Leases at Fort Lauderdale-Hollywood International Airport Robert Melton, CPA, CIA, CFE, CIG County Auditor Audit Conducted by: Jenny Jiang, CPA, Audit Manager

Exhibit 1 Review of Aviation Real Property Leases at Fort Lauderdale-Hollywood International Airport Robert Melton, CPA, CIA, CFE, CIG County Auditor Audit Conducted by: Jenny Jiang, CPA, Audit Manager

Safety Regulatory Oversight of Commercial Operations Conducted Offshore